Your child is three years old. College feels far away. But if you are planning to fund a degree at a top Indian engineering or medical college — or even a postgraduate programme abroad — you are looking at a cost that could easily touch ₹40–70 lakh by the time your child turns 18. The question most parents ask is simple: “How much should I invest every month?” A goal based SIP calculator answers exactly that — but only if you feed it the right inputs. Get the inputs wrong and the number the calculator gives you will be as useful as a weather forecast from the wrong city.

This article explains how to use a goal-based SIP calculator correctly for child education planning, what assumptions drive the output, and what to do when the number feels out of reach.

Quick Answer: Goal Based SIP Calculator

A goal based SIP calculator estimates the monthly SIP needed for a future target like a child’s education corpus. For example, if the future goal is ₹50 lakh in 15 years, the required SIP depends on expected return, inflation, and whether you increase SIP every year.

How to Calculate Your Monthly SIP for Child Education

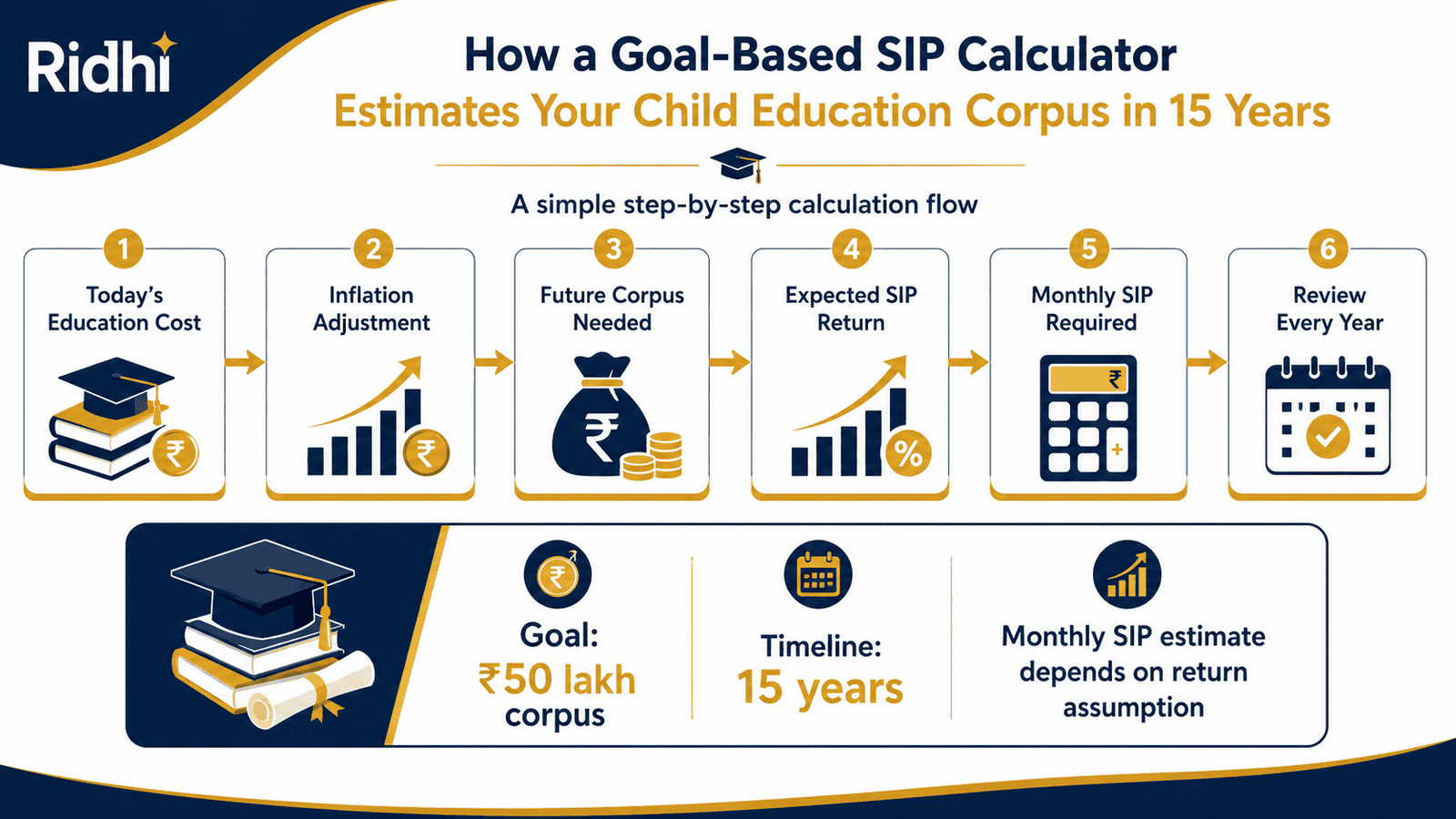

A goal-based SIP calculator uses a standard future value formula in reverse. Instead of telling you what your SIP will grow to, it tells you what SIP you need to reach a specific target. Here is the five-step process:

Step 1: Estimate the future education cost. Start with today’s cost — not tomorrow’s. If a private engineering degree costs ₹15 lakh today, you cannot invest for ₹15 lakh. Education inflation in India typically runs at 8–10% per year. At 9% inflation, ₹15 lakh today becomes approximately ₹54.7 lakh in 15 years. That is your real target.

Step 2: Fix your timeline. If your child is 3 years old and college begins at 18, you have 15 years. This is your investment horizon. The longer it is, the more compounding works in your favour — and the lower your required monthly SIP for the same corpus.

Step 3: Choose an expected annual return assumption. This is the most sensitive input. A 10% assumed return gives a very different SIP from a 12% return. Be conservative — do not plug in 15% just because some equity fund delivered that in a good year. Use 10–11% for long-term equity SIP scenarios; use 7–8% if you plan a balanced or debt-heavy approach.

Step 4: Choose fixed SIP or step-up SIP. A fixed SIP keeps the same monthly amount for 15 years. A step-up SIP (also called a top-up SIP) increases by a fixed percentage — say 10% — every year. Step-up SIP reduces the starting amount significantly. The calculator will show both options if you enter the step-up percentage.

Step 5: Review the output and adjust assumptions. The number the calculator returns is an estimate, not a contract. Change the return assumption by 1% and the required SIP can shift by ₹2,000–4,000 per month for a ₹50 lakh goal. Always run at least three scenarios — conservative (9% return), base (11% return), and optimistic (13% return).

Monthly SIP Formula = FV × r / [(1 + r)^n − 1]

Where: FV = inflation-adjusted future goal value | r = monthly return rate (annual rate ÷ 12) | n = total months (years × 12)

For a ₹50 lakh target in 180 months (15 years) at 11% annual return: monthly r = 0.11/12 = 0.00917. Required SIP ≈ ₹10,800 per month. At 10% assumed return, the same goal requires approximately ₹12,200/month. At 12% return, approximately ₹9,500/month. That ₹2,700/month difference — driven purely by a 1% return assumption — is why the input matters enormously.

Use our monthly investment estimate calculator to explore how different inputs change the output for your goal.

Key Takeaways

- Always calculate from the inflation-adjusted future cost — not today’s education fee. At 9% education inflation, ₹15 lakh today becomes approximately ₹54.7 lakh in 15 years.

- Changing your return assumption by just 1% can shift the required SIP by ₹2,000–4,000/month for a ₹50 lakh goal.

- A step-up SIP of 10% per year can reduce your starting SIP by 30–40% compared to a flat fixed SIP for the same corpus.

- The goal-based SIP calculator gives an estimate — not a guarantee. Actual mutual fund returns are market-linked and vary year to year.

- Reviewing your education SIP every year — especially after salary hikes or school fee revisions — is as important as the initial calculation.

- Begin de-risking your portfolio 3–5 years before the education date to protect the corpus from a market downturn at the worst time.

Key Facts at a Glance

| Parameter | What It Means | Typical Range / Example |

|---|---|---|

| Today’s Education Cost | Starting point for inflation adjustment | ₹10–25 lakh (India, undergraduate) |

| Education Inflation | Rate at which costs rise yearly (assumption) | 8–10% per year |

| Future Education Cost | Inflation-adjusted target corpus | ₹40–70 lakh in 15 years |

| Expected Return | Annual return assumed on SIP (assumption) | 10–12% (equity-oriented, not guaranteed) |

| Investment Horizon | Years available to invest | 15 years |

| Monthly SIP (Fixed) | Flat monthly investment for 15 years | ₹9,500–₹12,200 for ₹50L goal |

| Step-Up % | Yearly SIP increase to reduce starting load | 10% per year is common |

| Review Frequency | How often to recalculate and rebalance | Once a year, minimum |

How Goal-Based Investing Works for Child Education

Goal-based investing is simply matching a specific financial target — a corpus of money — to a specific date. Your child’s college education is a textbook goal-based investing scenario: the target is fixed (the course fees), the date is known (age 18), and there is a long runway to build the corpus. Unlike retirement, where you can delay spending, you cannot defer a college admission. The date is hard.

This is why a goal based SIP calculator is more useful than a generic SIP calculator for this purpose. A generic calculator asks: “How much will ₹10,000/month grow in 15 years?” A goal-based calculator asks the right question: “How much do I need to invest monthly to reach ₹54.7 lakh in 15 years?” The direction of calculation is reversed — and that makes all the difference for planning.

Why Education Inflation Changes Everything

General consumer price inflation in India has hovered around 5–6% in recent years according to RBI data. Education inflation has historically run faster — closer to 8–10% annually, driven by fee hikes at private institutions, coaching costs, and rising hostel and living expenses. If you ignore education inflation and only plan for ₹15 lakh (today’s cost), you will arrive at the goal date with only a fraction of what you actually need. Always use an inflation-adjusted figure as your SIP target.

Families planning for study abroad face an additional layer: currency risk. A US or UK degree in 2039 will cost significantly more in rupee terms even if tuition stays flat in dollar terms, because of potential rupee depreciation. For overseas goals, add a currency buffer of 2–3% on top of your inflation assumption.

For a deeper walkthrough of how to structure the full education planning timeline, read our guide on child education planning: how to build a ₹50 lakh corpus by age 18.

SIP Is a Tool, Not a Guarantee

SIP (Systematic Investment Plan) spreads your investment across market cycles, reducing the impact of buying at market peaks. But it does not eliminate market risk. In any given 15-year period, the actual return from an equity mutual fund could be 8%, 12%, or 14% — the calculator cannot tell you which. If you are new to how SIP works, read our SIP meaning and how SIP works article before setting an expectation on returns.

The key discipline for goal-based SIP is this: pick a return assumption you would be comfortable with even in a modest scenario, and review it every year. If the market has delivered well above your assumption in Year 3, you do not need to chase higher return inputs — your corpus may already be on track or ahead.

Real Example: Rohit’s Daughter’s Education Fund

Rohit, 35, is a product manager in Bengaluru earning ₹28 lakh per year. His daughter Priya is 3 years old. Rohit wants to fund an undergraduate engineering degree for Priya, which costs approximately ₹18 lakh today at a top private institution. College begins when Priya turns 18 — a 15-year horizon.

At 9% education inflation, today’s ₹18 lakh becomes approximately ₹65.7 lakh in 15 years. Rohit enters this into a goal-based SIP calculator with three return scenarios:

| Return Assumption | Monthly Fixed SIP | Step-Up SIP Start (10% yearly) |

|---|---|---|

| 10% per annum | ₹16,100 | ₹10,700 |

| 11% per annum | ₹14,100 | ₹9,300 |

| 12% per annum | ₹12,400 | ₹8,100 |

Rohit finds the ₹16,100 fixed SIP uncomfortable given his existing EMIs. He chooses the step-up SIP route: start at ₹9,300/month at 11% assumed return, and increase by 10% every April after his annual salary increment. The key insight: starting at a manageable level with a commitment to increase is far better than delaying until you “can afford” the full SIP.

Comparison: Fixed SIP vs Step-Up SIP vs Lumpsum + SIP

| Strategy | How It Works | Best For |

|---|---|---|

| Fixed SIP | Same amount every month for 15 years | Stable income, simple automation preference |

| Step-Up SIP | Start smaller, increase by 10% each year | Early-career parents expecting income growth |

| Lumpsum + SIP | Deploy existing savings as lumpsum; top up with monthly SIP | Parents who have existing savings but limited monthly surplus |

| Conservative Allocation Near Goal | Shift from equity to debt 3–5 years before the date | Everyone — reduces sequence-of-returns risk near goal date |

If you are considering the step-up SIP route, our article on step-up SIP: how to increase your SIP amount yearly covers the mechanics and automation options in detail.

You have 15+ years until your child’s education date and a stable monthly income — THEN a step-up SIP starting at a manageable amount is likely more practical than stretching for a high fixed SIP from Day 1.

You already have ₹5–10 lakh in savings earmarked for education — THEN deploy it as a lumpsum to reduce the monthly SIP burden immediately.

You are within 5 years of the education date — THEN start shifting the accumulated corpus toward lower-volatility instruments to protect what you have built.

Your required SIP is more than 20% of your take-home salary and you have no emergency fund — THEN build the emergency fund first before locking into a large SIP commitment.

You cannot tolerate seeing your portfolio drop 20–30% in a bad market year — THEN a 100% equity SIP may not suit you, even over 15 years. A blended allocation with some debt exposure may be more appropriate for your risk profile.

Common Mistakes to Avoid

Using Today’s Education Cost as the Target

Many parents enter ₹15 lakh into a calculator because that is what an engineering degree costs today.

Education inflation of 9% per year will make that same degree cost ₹54–65 lakh in 15 years. Planning for today’s cost leaves a massive shortfall — potentially ₹30–40 lakh — at exactly the moment you need the money.

Always calculate the inflation-adjusted future cost before entering any number into the calculator.

Assuming Peak Returns Will Continue

Some parents enter 15–16% return assumptions because their current fund delivered that last year.

Equity mutual fund returns are cyclical. A 15-year average of 10–12% is a more realistic and commonly used planning assumption. Overestimating returns by 3–4% can leave you ₹15–20 lakh short of your target in a more modest market environment.

Use 10–11% as a base-case return assumption and run a conservative 8–9% scenario as a stress test.

Starting Too Late and Then Over-Investing

Delaying by 3–5 years dramatically increases the required SIP — often by 50–80%.

A parent who starts at 30 may need ₹8,000/month for the same corpus a parent starting at 35 would need ₹14,000/month to reach. Starting late and then over-investing to compensate can crowd out other financial goals like retirement or emergency funds.

Start with whatever you can afford today, and increase it with income growth.

Not Increasing SIP After Income Grows

A fixed SIP set at today’s income level loses its proportional weight as your salary grows.

If you earn ₹28 lakh today and grow to ₹40 lakh in five years, the same ₹10,000 SIP represents a shrinking share of your capacity. Not increasing SIP means you are likely under-investing relative to your goal.

Set a calendar reminder every April to increase your education SIP by at least 10%.

Not Reviewing the Goal After Major Life Events

School fee revisions, a change of city, or a shift in career ambition can change the education cost estimate significantly.

A child who switches from a government school to an international school may now be targeting a foreign university — a completely different corpus requirement. Not recalculating after such events leaves the plan misaligned with reality.

Review the calculator inputs at least once a year and after any major family or financial change.

Ignoring Asset Allocation as the Goal Approaches

Staying 100% in equity SIPs all the way to the education date exposes the corpus to sequence-of-returns risk.

A 30% market drop in Year 14 — with only one year left — could wipe out 3–4 years of SIP gains. Unlike retirement, you cannot delay college admission by two years to wait for a recovery.

Begin moving a portion of the corpus to lower-volatility debt or hybrid instruments 3–5 years before the goal date.

When This May Not Be the Right Choice

A long-term equity SIP for child education may not be the right primary approach in every situation. If your child’s college date is less than 3–5 years away, the investment horizon is too short for equity SIPs to smooth out volatility — capital protection matters more than growth at this stage. If your household has no emergency fund, locking a large amount into market-linked SIPs creates fragility: one unexpected expense could force a premature redemption at a loss. If you or your family cannot mentally absorb seeing the corpus fall 20–30% during a market correction, the psychological cost of staying invested in a bad year can lead to panic withdrawals that permanently damage the plan. And if the education goal requires guaranteed liquidity at a precise date — admission fees due in a specific month — pure equity SIPs do not offer that guarantee; a combination with fixed-maturity or liquid instruments may be more appropriate.

“If any of these apply to your situation, it may be worth exploring alternatives before committing.”

Official Rules and Where to Verify

Mutual fund SIPs in India are regulated by the Securities and Exchange Board of India. SEBI sets rules for fund registration, disclosure norms, and investor protection. Before investing in any mutual fund scheme, read the Scheme Information Document (SID) and Key Information Memorandum (KIM) provided by the fund house — these contain the official risk factors, expense ratio, and investment mandate.

For return and inflation context, the Reserve Bank of India publishes monetary policy reports and inflation data at rbi.org.in. This does not constitute investment advice but provides macro context for your return assumptions.

- SEBI — sebi.gov.in (mutual fund regulation, investor education, riskometer disclosures)

- RBI — rbi.org.in (inflation data, monetary policy reports)

- AMC / Fund House websites — for scheme-specific SID, KIM, and factsheets

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

To understand why the return figure you see in a fund factsheet may differ from your actual experience, read our explanation of CAGR vs absolute vs XIRR: how mutual fund returns are calculated.

Expert Tips

- Always run three return scenarios. Use 9% (conservative), 11% (base), and 13% (optimistic) in the goal-based SIP calculator. Invest for the 9% scenario — anything better is a bonus, not a plan.

- Separate the education corpus from retirement savings. Use a dedicated folio or fund for the education goal so you can track progress independently and de-risk the education portfolio without disturbing your retirement allocation.

- Review and recalculate every April. Salary increments, school fee hikes, and market performance all affect whether you are on track. A 20-minute annual review can catch a ₹10–15 lakh drift before it becomes uncorrectable.

- Start de-risking 3–5 years before the education date. At Year 10, shift 20–30% of the corpus to lower-volatility instruments. At Year 13, consider shifting 50–70%. The goal is to arrive at the education date with a corpus that is protected from a sudden market fall — not one that is still maximising growth.

- Do not stop SIP during a market downturn. If your goal is 8–10 years away, a market correction is an opportunity to buy more units at lower NAV. Stopping SIP during a downturn is one of the costliest planning errors.

- Use the step-up SIP feature from the start. Even a 5% annual step-up significantly reduces the starting monthly commitment and keeps your SIP growing in line with income. Read more on the power of compounding to see why early step-up SIPs outperform flat SIPs started later.

Frequently Asked Questions

How much SIP is needed for child education in 15 years?

It depends on the inflation-adjusted future cost of the course you are planning for and your return assumption. For a ₹50 lakh target in 15 years, the required fixed SIP ranges from approximately ₹10,800/month (at 11% assumed return) to ₹12,200/month (at 10%). For a ₹65 lakh target, those figures rise to approximately ₹14,100 and ₹16,100 respectively. Use a goal-based SIP calculator with your specific cost estimate and return assumption for a personalised figure.

Is SIP good for child education planning?

Yes — for a 15-year horizon, SIP in equity-oriented mutual funds is a commonly used approach because it spreads investment over time, reduces timing risk, and has historically generated inflation-beating returns over long periods. However, mutual fund investments are subject to market risks. Past performance does not guarantee future returns. SIP is not a guaranteed savings instrument and should be reviewed regularly.

Should I use fixed SIP or step-up SIP for child education?

If your current income makes a high fixed SIP uncomfortable, step-up SIP is a practical alternative. Starting at a lower amount and increasing by 10% per year keeps the plan affordable now and grows the corpus as your income grows. Fixed SIP is simpler and requires no annual action — both approaches can work if the total contribution over 15 years is sufficient.

What return assumption should I use in the calculator?

Use 10–11% as a base assumption for a long-term equity-oriented SIP and also run a conservative 8–9% scenario. Avoid using past peak returns (14–16%) as your planning assumption — if those returns do not materialise, the corpus shortfall can be very large. The more conservative your assumption, the more buffer you build in.

What if I cannot invest the required SIP amount right now?

Start with what you can genuinely commit to — even ₹3,000–5,000/month — and use the step-up SIP feature to increase it each year. A smaller SIP started today is significantly better than a large SIP deferred by two or three years. The first few years of a 15-year SIP have the highest compounding impact.

Can I use a goal-based SIP calculator for study abroad planning?

Yes, but add a currency buffer to your future cost estimate. If a foreign degree costs USD 80,000 today and the rupee depreciates at 2–3% annually, the rupee cost in 15 years could be substantially higher than today’s exchange rate suggests. Use a higher future corpus target — or plan a separate foreign-currency instrument — for overseas education goals.

What happens if the market falls just before my child’s college date?

This is sequence-of-returns risk — the most dangerous scenario for a time-bound goal. If you have followed the de-risking step (shifting to lower-volatility instruments 3–5 years before the goal), the impact of a market fall is limited. If you stay 100% in equity until Year 14 and the market drops 30%, the corpus can be severely impaired with no time to recover.

Is it better to open a dedicated fund account for my child’s education?

Using a dedicated folio or separate SIP specifically tagged for the education goal makes tracking straightforward. It also prevents the temptation to redeem education savings for other purposes — which is one of the most common reasons parents arrive at the goal date underprepared. For how SIP works and how to start one, read SIP meaning and how SIP works.

Final Verdict

A goal based SIP calculator is one of the most useful planning tools a parent can use — but only if the inputs are realistic. Plug in an inflation-adjusted education cost, use a conservative return assumption, and run at least three scenarios before settling on a monthly SIP amount. The calculator tells you direction, not destiny. Starting early gives you the most important asset in long-term investing: time. A parent who starts at 30 needs roughly half the monthly SIP of one who starts at 35 for the same ₹65 lakh corpus. If today’s required SIP feels too high, start with less using a step-up SIP and commit to increasing it every year. The only real mistake is not starting at all. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Ishita Sharma writes about goal-based financial planning for Indian families and individuals. Her content connects saving, budgeting, investing, insurance, and debt decisions to real-life goals such as child education, marriage, retirement, home buying, emergency funds, family protection, and long-term wealth building.

She covers topics such as child education planning, marriage goal planning, retirement planning, home-buying goals, inflation-based goal estimation, monthly investment planning, savings timelines, emergency buffers, asset allocation basics, family financial milestones, and goal calculators.

Ishita’s writing is structured, thoughtful, and decision-oriented. She helps readers move from vague goals like “save more” to clearer questions such as how much may be needed, by when, what assumptions matter, and what trade-offs exist. Her articles use Indian examples, timelines, ₹ amounts, and simple planning frameworks. Her content is educational and should not be treated as personalised investment, tax, loan, or insurance advice. Since future costs, inflation, returns, product rules, and tax treatment can change, readers should verify current information before acting.