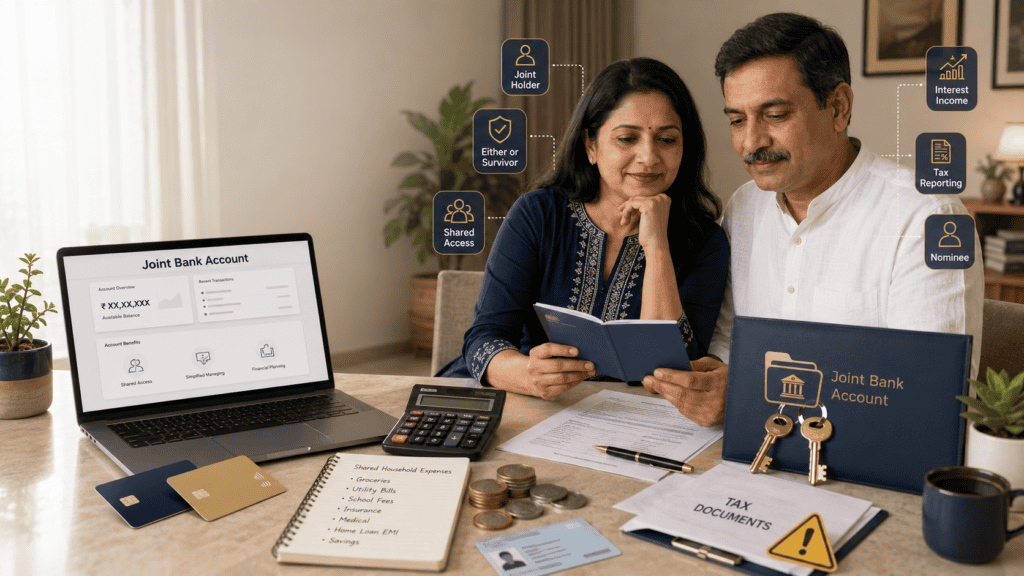

Most families open a joint bank account without reading a single word of the account mandate form. The account gets used for grocery transfers, rent payments, and school fee deductions — and nobody thinks twice about whose money it actually is, or who pays tax on the interest. That works fine until it doesn’t: a sudden medical emergency, a spouse who needs urgent access, a joint FD that throws up a mismatch in Form 26AS, or a family dispute over whose savings are in the account.

Joint account rules in India cover more than just who can deposit and withdraw. They determine how interest income is taxed, how TDS is reported against a PAN, which holder survives the account after a death, and how a nominee fits into the picture. This guide explains each of these clearly, so you can use a joint account with confidence — not assumption.

Quick Answer: Joint Account Rules in India

Joint account rules in India decide who can operate the account, how funds are accessed, and how interest income is reported for tax. A joint account may help families manage expenses, but each holder should understand survivor options, ownership source, nomination, and the ₹10,000 savings interest deduction applicable under Section 80TTA for non-senior citizens.

Key Takeaways

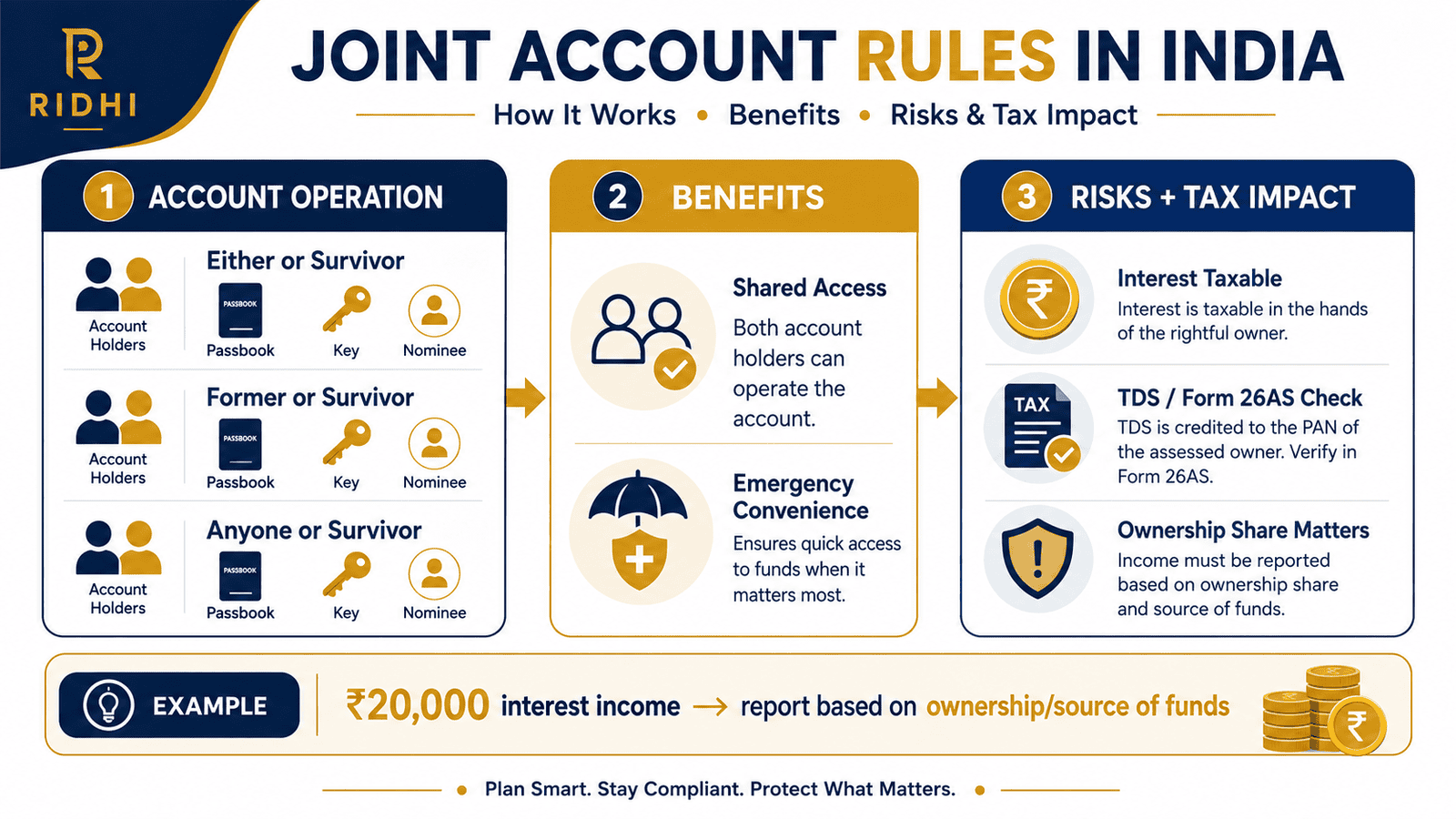

- The account mandate — Either or Survivor, Former or Survivor, or Jointly — decides whether one holder or all holders must authorise every transaction. Check this before signing.

- Tax on interest income follows the source of funds, not the number of names on the account. If one spouse contributes 100% of the deposit, 100% of the interest is taxable in their hands.

- TDS on joint FD interest is typically deducted against the primary (first) account holder’s PAN — the secondary holder’s Form 26AS may show nothing, even if economic ownership is shared.

- A nominee is not a joint holder. A nominee receives access to funds for settlement purposes after a holder’s death; legal heirs may still have a claim depending on succession laws.

- Savings account interest up to ₹10,000 per year is deductible under Section 80TTA for non-senior citizens — but both joint holders cannot each claim a separate ₹10,000 deduction on the same interest amount.

- Check your AIS and Form 26AS before filing your ITR every year — a mismatch in reported interest from a joint account is one of the most common reasons for income tax notices.

- Joint accounts work best when purpose, contribution ratio, and account mandate are discussed and agreed upfront — not assumed.

Key Facts at a Glance

| Parameter | Rule / Detail | Source |

|---|---|---|

| Who can open | Two or more individuals; most banks allow up to 4 holders | Bank account opening policy |

| Operation modes | Either or Survivor, Former or Survivor, Anyone or Survivor, Jointly | RBI / bank mandate form |

| Tax on savings interest | Interest taxable in the hands of the contributing holder; deduction up to ₹10,000 under Section 80TTA (non-senior citizens) | incometax.gov.in |

| TDS on joint FD interest | TDS deducted against primary (first) holder’s PAN; threshold ₹40,000 per year for general depositors, ₹50,000 for senior citizens | incometax.gov.in |

| Nominee vs joint holder | Nominee receives funds for settlement after death; legal heirs have separate rights under succession law | Bank terms; succession law |

| Survivor clause | Surviving holder continues account operation per mandate — does not automatically make them the legal owner of all funds | Bank mandate / RBI guidelines |

| KYC requirement | All holders must complete full KYC including PAN and Aadhaar linking | RBI KYC norms |

How a Joint Bank Account Works in India

A joint bank account is a standard savings, current, or fixed deposit account held in the names of two or more people. Every holder is formally on record with the bank, completes KYC, and is linked by PAN. But being named on the account is not the same as having the right to operate it independently — that depends entirely on the account mandate.

What the Account Mandate Actually Controls

When you open a joint account, the bank asks you to select an operation mode. This is the mandate. The mandate controls who can sign cheques, initiate transfers, operate net banking, and access the debit card. The most common modes are Either or Survivor, Former or Survivor, and Jointly — each of which works very differently in practice. A joint savings account with an Either or Survivor mandate means either holder can walk into the bank or log in online and transfer the entire balance without the other person’s knowledge or approval.

Banks may also issue debit cards and net banking credentials to each holder separately under certain mandates. This has convenience benefits for couples managing shared household expenses, but it also means one holder can spend freely without the other’s sign-off. Understanding savings interest calculation is a useful first step before opening any shared savings account, because the way interest accrues and is credited affects how much is reportable for tax each year.

Primary Holder, Secondary Holder, and What Those Terms Mean

Banks typically refer to the first named account holder as the primary holder and subsequent holders as secondary. This distinction matters more than most people realise. TDS on fixed deposit interest, for example, is generally deducted and reported against the primary holder’s PAN — even if the secondary holder contributed more of the deposited amount. The primary holder’s Form 26AS and AIS will reflect the interest; the secondary holder’s may not show anything at all.

This also affects who files what in their Income Tax Return. According to Income Tax Department guidelines on interest income, each individual is responsible for reporting income that is beneficially theirs — regardless of whose PAN the bank has reported it against. If you are the secondary holder but contributed 100% of the FD principal, the interest is still taxable in your hands, even if TDS was deducted against the primary holder’s PAN.

Joint FD vs Joint Savings Account: Key Differences

Joint savings accounts and joint fixed deposits follow broadly similar mandate rules, but FDs have a sharper tax exposure because interest amounts are typically larger and TDS kicks in once the annual interest crosses ₹40,000 for general depositors (₹50,000 for senior citizens, as per current Section 194A rules). A joint savings account earning ₹8,000 in interest a year may stay below the TDS threshold — but a ₹10 lakh joint FD at 7% earns ₹70,000 in a year, which triggers TDS automatically against the primary holder’s PAN.

Operation-wise, most banks apply the same mandate to the FD as to the linked savings account — but this is not universal. Some banks require a separate mandate for FD accounts. Always verify the FD-specific mandate when opening a joint fixed deposit, particularly for senior citizen family accounts where the account may be opened in a parent’s name with a child as second holder.

Real Example: Meera and Vikram, Pune

Meera, 38, is a project manager in Pune earning ₹14 lakh per year. Her husband Vikram, 40, is self-employed and earns roughly ₹6 lakh per year. They open a joint savings account with an Either or Survivor mandate for household expenses — groceries, rent, school fees, and emergency savings. Both transfer money into the account regularly: Meera puts in ₹25,000 a month and Vikram puts in ₹10,000.

By the end of the financial year, the account has earned ₹4,200 in savings interest. Since Meera contributed roughly 71% of all deposits and Vikram 29%, ₹2,982 of that interest is economically Meera’s and ₹1,218 is Vikram’s. Each should report their proportional share in their ITR under “Income from Other Sources.”

They also open a joint FD for ₹5 lakh at 7% per annum, with Meera as primary holder. The FD earns ₹35,000 in interest. TDS is not deducted because ₹35,000 is below the ₹40,000 threshold — but the full ₹35,000 appears in Meera’s AIS. Since Vikram contributed nothing toward this FD (the money came from Meera’s salary savings), the entire ₹35,000 is taxable in Meera’s hands. If Meera had not checked her AIS before filing, she might have missed this — and that mismatch would have generated an income tax notice.

Key insight: Even when both names are on the account, the tax responsibility tracks the money’s origin — not the account structure.

How to Calculate Joint Account Interest and Tax Reporting

Proportional Interest = (Your Contribution ÷ Total Deposits) × Total Interest Earned

Using Meera and Vikram’s savings account example from above:

| Scenario | Key Inputs | Taxable Interest |

|---|---|---|

| Both contribute equally (50:50) | Total interest ₹4,200; each contributes 50% | ₹2,100 each — report in individual ITR |

| One holder contributes 100% | Total interest ₹4,200; one holder funded all deposits | ₹4,200 fully taxable in sole contributor’s hands |

| Joint FD — primary holder fully funds | ₹5 lakh FD at 7%; interest ₹35,000; TDS against primary PAN | ₹35,000 reportable in primary holder’s ITR; check AIS before filing |

For FD interest specifically, review the detailed breakdown of FD tax treatment before you file, especially if TDS has been deducted against the primary holder’s PAN. Use an income tax calculator to estimate how much additional tax you may owe after adding joint account interest income to your salary.

Note that your AIS (Annual Information Statement) available on the Income Tax Department’s portal at incometax.gov.in reflects interest reported by the bank against your PAN. If the bank has reported the full FD interest under the primary holder’s PAN and you are the secondary holder who funded the deposit, the AIS mismatch needs to be addressed before you file. Consult a qualified tax professional if your joint account interest reporting is complex.

Comparison: Joint Account Operation Modes

| Operation Mode | Who Can Transact | Best Suited For |

|---|---|---|

| Either or Survivor | Any one holder can independently operate during lifetime; surviving holder continues after death | Married couples, shared household accounts |

| Former or Survivor | First (former) named holder operates during lifetime; second holder gets access after first holder’s death | Parent-child accounts where child manages after parent’s death |

| Anyone or Survivor | Any one holder among three or more can transact; survivor continues after others’ death | Accounts with three or more holders (e.g., siblings) |

| Jointly | All named holders must authorise every transaction together | Business accounts, high-value shared FDs requiring dual control |

The exact wording and availability of these mandates can vary from bank to bank. Some banks use slightly different terminology or may not offer all four modes. Always confirm your account’s mandate by reading the account opening form — do not assume. For a deeper understanding of how FDs are structured within joint accounts, the article on fixed deposit basics explains how FD tenures, interest payout options, and renewal work, which is relevant when deciding how to structure a joint FD.

How to Decide What’s Right for You

You and your spouse both earn separately and want a shared account only for household expenses — THEN open one joint account with Either or Survivor mandate, keep personal salary accounts separate, and document each person’s contribution to the joint account.

You are an adult child helping an elderly parent manage their savings — THEN a Former or Survivor account may be appropriate, with the parent as primary holder, so the parent retains full control during their lifetime.

You want a joint FD for a specific savings goal and both people are contributing equally — THEN record the 50:50 contribution formally, so each person correctly reports 50% of the interest in their individual ITR.

Your family needs an emergency fund with fast access for either spouse — THEN a joint Either or Survivor savings account is practical; pair it with a clear contribution record so tax reporting stays simple. Use the emergency fund planning tool to size this fund correctly.

One holder has existing debts or legal disputes — THEN adding them as a joint holder on a savings account or FD could expose the account to legal attachment or recovery proceedings. Evaluate this risk carefully.

You are unsure whether you want to share full transactional access — THEN avoid Either or Survivor; consider a Jointly operated account, which requires both parties to authorise every transaction.

A joint account is NOT a good fit if you want complete privacy over your savings, salary income, or investment amounts — or if the relationship involves an unresolved dispute over asset ownership. In these situations, a personal account is safer and simpler for tax purposes.

Common Mistakes to Avoid

Assuming Tax Is Automatically Split 50:50

Most families believe that having two names on an account means the interest income is automatically halved for tax purposes.

It doesn’t work that way. The Income Tax Department looks at the source of the funds, not the number of names. If one spouse funded the entire FD, 100% of the interest is taxable in that person’s hands — regardless of the account structure. Misreporting this could result in an income tax notice or demand.

Track contributions carefully and report proportional interest in each person’s ITR.

Adding a Joint Holder Without Understanding Withdrawal Rights

An Either or Survivor account gives any one holder full and independent transactional access.

This means the second holder can withdraw the entire balance, close the account, or break an FD without the first holder’s knowledge or consent under an Either or Survivor mandate. Families have encountered serious disputes because of this assumption gap.

Read the mandate section of your account opening form before signing. If you want dual authorisation, choose a Jointly operated account.

Filing Form 15G or 15H Incorrectly for Joint FDs

Form 15G (for non-senior citizens) and Form 15H (for senior citizens) can be submitted to request that no TDS is deducted on FD interest — but only when the total taxable income is below the exemption threshold.

In a joint FD, both holders may need to submit these forms separately depending on the bank’s process. Submitting only one form, or submitting the wrong form, can result in TDS being deducted unexpectedly or incorrectly. For a full breakdown, review the guide on Form 15G and 15H eligibility before the bank’s annual cut-off date.

Confirm your bank’s specific requirement for joint FDs — it varies.

Ignoring AIS and Form 26AS Before Filing ITR

Banks report FD interest against the primary holder’s PAN. If you are the primary holder and you don’t check your AIS before filing, you may miss declaring income that the Income Tax Department already knows about.

Even a small mismatch — ₹500 in unreported interest — is enough to generate a compliance notice. Log into incometax.gov.in, download your AIS, and reconcile every interest entry before filing.

Do this every year, not just in years when you expect large interest income.

Treating Nominee as the Legal Owner After Death

A nominee receives the account balance from the bank after a holder’s death — but only for safe custody and distribution. The nominee is not automatically the legal owner of those funds.

Legal heirs can claim their share under succession law (Hindu Succession Act, Indian Succession Act, or personal law as applicable), even if they are not nominated. Families have faced disputes where funds were paid to a nominee but contested by heirs.

A will, a clear succession plan, and legal advice from a qualified professional are still important even if nomination is in place.

Opening a Joint Account Without a Clear Purpose

A joint account where all salary income, personal savings, investment proceeds, and household expenses flow together becomes very difficult to unwind — and even harder to report for tax.

Define the purpose upfront: is this account for household expenses only, emergency savings only, or a specific savings goal? That decision drives contribution clarity, tax reporting simplicity, and exit planning if the account ever needs to be closed.

When This May Not Be the Right Choice

A joint account is not the right structure for every family situation. Consider these scenarios before opening one:

One holder has existing debt or legal disputes. If a joint holder has outstanding loans, a court order, or a legal proceeding against them, the bank account they are named on could potentially be attached or frozen by a recovery proceeding. Your funds in that account may be affected.

You want privacy over your salary or savings. Either or Survivor accounts give both holders equal visibility. If knowing each other’s exact balance, transaction history, and FD maturity amounts creates friction in the relationship, a joint account amplifies that friction rather than resolving it.

Elderly parent’s funds may be disputed later by siblings. A joint account with one adult child as second holder can be interpreted differently by other children when inheritance questions arise. The surviving child may have access, but legal heirs may challenge distribution. This is a genuine and common family dispute scenario in India.

Tax reporting is too complex for mixed or unclear contributions. If multiple people are contributing with no documentation of amounts or dates, correctly reporting proportional interest income at tax time becomes burdensome and error-prone.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Joint account rules in India sit at the intersection of banking regulation and income tax law. No single document covers everything — you need to verify from the right source for each issue.

- RBI (rbi.org.in): Banking regulation, customer rights, account operation guidelines, KYC norms, and the framework governing savings and FD accounts.

- Income Tax Department (incometax.gov.in): Interest income taxability, TDS rules under Section 194A, Section 80TTA deduction, AIS and Form 26AS, and ITR filing requirements for interest income.

- Your bank’s account opening form and terms and conditions: The specific mandate wording, survivor clause, debit card access rules, and FD operation terms are bank-specific and must be confirmed directly with your bank.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Open a joint account for one defined purpose — not as a catch-all. A joint account used exclusively for household expenses is easy to manage and tax-report. A joint account where salary, FDs, investments, and expenses all flow in together becomes a tax and documentation burden quickly.

- Keep a simple log of who deposited what and when. A basic spreadsheet recording each person’s monthly transfers into the joint account will make proportional interest reporting straightforward at year-end — and will hold up if a tax officer ever asks for it.

- Read the mandate section of the account opening form before you sign — not after. Most people discover their mandate type only when something goes wrong. The mandate is the single most important operational decision in a joint account.

- Update nominee details separately for each account and FD. Nomination does not automatically carry over from a savings account to a linked FD. Confirm nomination for every product — savings account, FD, recurring deposit — individually.

- Log into incometax.gov.in and download your AIS before you start filing your ITR. As of recent data, the AIS now captures FD interest, savings interest, and dividend income reported by financial institutions against your PAN. Cross-check every line item against your own records before submitting your return.

- If you are the secondary holder and funded the FD, note this in writing. An email or a written contribution record is not a legal instrument, but it establishes intent — useful if there is ever a question about whose income the interest represents.

- Discuss survivor and closure procedures with your bank before you need them. Know what documents are required to operate or close the account after a holder’s death. Many families discover these requirements only at a difficult moment — asking proactively costs nothing.

Frequently Asked Questions

Is interest on a joint savings account taxable for both holders?

Interest income is taxable based on who contributed the funds — not on how many names are on the account. If both holders contributed equally, each reports 50% of the interest. If only one person funded the account, 100% of the interest is taxable in that person’s hands. Each holder should report their proportionate share under “Income from Other Sources” in their ITR.

Who pays tax on joint FD interest?

Tax follows the source of funds, not the account structure. The person who deposited the principal is treated as the beneficial owner of the interest. However, TDS on FD interest is typically deducted against the primary (first) holder’s PAN by the bank. If you are the primary holder, ensure you account for all FD interest in your ITR, even if a secondary holder contributed part or all of the principal — and vice versa if you are the secondary holder who funded the deposit.

Can one holder withdraw all the money from a joint account?

This depends on the account mandate. In an Either or Survivor account, yes — either holder can independently withdraw the full balance at any time. In a Jointly operated account, all named holders must authorise the transaction. Check your mandate by looking at the account opening form or your account statement header. If you are unsure, contact your bank directly.

What is Either or Survivor in a joint account?

Either or Survivor means any one of the joint holders can independently operate the account during the lifetime of all holders. If one holder passes away, the surviving holder(s) can continue to operate the account as per the original mandate. This is the most common mode for family savings accounts in India because it provides the most transactional flexibility.

Is a nominee the same as a joint account holder?

No. A nominee is designated to receive the funds held in the account from the bank after the death of all account holders — primarily for safe custody and settlement convenience. A joint holder is a co-owner with rights to operate the account during their lifetime. A nominee does not have rights to operate the account while the holder is alive, and nomination does not override the legal rights of heirs under applicable succession law.

Is a joint savings account good for a husband and wife?

A joint account with an Either or Survivor mandate is practical for managing shared household expenses, rent, school fees, and emergency savings. The key is to keep individual salary accounts separate, define the purpose of the joint account, document contribution amounts, and ensure both partners review interest income reporting at tax time. A joint account simplifies family banking — it doesn’t automatically simplify tax reporting.

Can a senior citizen open a joint account with their adult child?

Yes. Banks allow this and it is a common setup for elderly parents who want a trusted family member to help manage banking transactions. A Former or Survivor mandate is typically used — the senior citizen operates the account as the primary (former) holder during their lifetime, with the child getting survivor access after the parent’s death. The senior citizen remains the primary holder for TDS and interest reporting purposes. Confirm the mandate and operation details with your bank.

What happens to a joint account after one holder dies?

This depends on the mandate. In an Either or Survivor account, the surviving holder typically continues to operate the account. In a Formerly or Survivor account, the surviving (second) holder gets operational access after producing the required documents, such as a death certificate. The bank will generally process the claim according to the mandate and the bank’s internal procedures. The nominee, if any, may be involved in settlement. Legal heirs can also make claims under succession law if ownership is disputed.

Does the ₹10,000 Section 80TTA deduction apply to joint account interest?

Section 80TTA provides a deduction of up to ₹10,000 on savings account interest for individuals who are not senior citizens. In a joint account, each holder can claim the deduction on their proportional share of the interest — not on the full interest amount. So if total savings interest is ₹8,000 and you contributed 50%, your reportable interest is ₹4,000 and your 80TTA deduction is limited to that ₹4,000. Senior citizens claim a larger deduction under Section 80TTB instead.

What should I check on AIS before filing my ITR for joint account interest?

Log into incometax.gov.in and open the Annual Information Statement (AIS) under the e-File section. Look for savings interest and FD interest entries reported by your bank against your PAN. If you are the primary holder of a joint FD, the bank may have reported the full interest against your PAN — even if a secondary holder contributed part of the principal. Verify each entry against your own deposit records and, if there is a genuine ownership split, consult a tax professional before filing.

Final Verdict

Joint account rules in India are not complicated — but they are misunderstood by most families. The account mandate controls who can access money. The source of funds controls who pays tax on the interest. The nominee handles settlement after death, but does not override legal heirship. These three points alone cover most of the confusion around joint banking in India.

A joint account works well when both holders understand exactly how it operates, who is contributing what, and how interest will be reported at tax time. It creates problems when these questions are assumed rather than answered. Open a joint account for a specific, defined purpose. Read the mandate. Track contributions. Check your AIS before you file. And review the details of FD tax treatment if you are operating a joint fixed deposit — the reporting rules are stricter than most people expect.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Meera Iyer writes about banking, fixed deposits, recurring deposits, savings accounts, emergency funds, senior citizen deposits, and safe cash management for Indian readers. Her work is especially useful for families, retirees, conservative savers, and beginners who want to understand where to keep short-term or low-risk money.

She covers topics such as FD meaning, FD calculator, RD calculator, FD vs RD, simple interest vs compound interest, savings account interest, sweep-in FD, premature FD withdrawal, senior citizen FD rules, TDS on FD interest, Form 15G, Form 15H, joint account rules, zero balance accounts, minimum balance charges, small finance bank FDs, post office FD vs bank FD, and emergency fund planning.

Meera’s content focuses on safety, liquidity, taxation, and practical decision-making. She avoids hype and explains both benefits and limitations of banking products. Since deposit interest rates, TDS rules, penalty charges, DICGC coverage, and bank policies can change, readers should always confirm the latest details from their bank, RBI, DICGC, India Post, or relevant official sources before making decisions.