You paid the minimum amount due before the due date. Your account shows no overdue amount. And yet, the next credit card statement arrives with a line called “finance charges” — sometimes ₹300, sometimes ₹900, sometimes more. This is what the credit card interest rate actually looks like in practice, and it catches most first-time cardholders completely off guard. A credit card is not structured like a personal loan where you know your EMI from day one. The interest mechanics are tied to your billing cycle, statement date, due date, and whether you cleared the full outstanding or only part of it. If you are just getting started with credit cards, this beginner credit card guide gives you the full foundation before we get into the numbers. This article explains, step by step and with real Indian figures, exactly how credit card interest is calculated and how to avoid paying it.

Quick Answer: Credit Card Interest Rate

Credit card interest rate is the finance charge applied when you do not pay the full outstanding amount by the due date. In India, banks often quote a monthly rate such as 3%–4%, which can become a much higher annual percentage rate when carried forward. The exact rate depends on your card issuer and card type — always check the Most Important Terms and Conditions (MITC) or Key Fact Statement (KFS) provided by your issuer for the rate that applies to your specific account.

Key Takeaways

- Paying the total amount due in full by the due date typically removes interest on purchases — this is the interest-free period benefit, and it disappears the moment you carry any unpaid balance forward.

- Paying only the minimum amount due keeps your account in good standing but does not stop finance charges from accruing on the remaining unpaid balance — the interest appears on your very next statement.

- Indian card issuers generally calculate interest on a daily basis using an annual rate derived from the monthly rate — every extra day an unpaid balance sits on your account adds to the cost.

- A monthly rate of 3.5% converts to an annual percentage rate of approximately 42% — this is significantly higher than most personal loans, and one of the most expensive forms of routine borrowing available to individuals in India.

- Cash withdrawals using a credit card attract interest from the date of withdrawal — there is no grace period — plus a one-time cash advance fee on top.

- The exact interest rate, fee structure, and calculation methodology for your account are stated in the MITC or Key Fact Statement — not in the welcome kit or advertising brochure.

Key Facts at a Glance

| Term | What It Means | Where to Verify |

|---|---|---|

| Credit Card Interest Rate | Finance charge on any unpaid outstanding balance after the due date | Card MITC / KFS |

| Monthly Percentage Rate (MPR) | Interest rate stated per month — as of recent data, typically 3%–4% across Indian issuers | Card MITC / KFS |

| Annual Percentage Rate (APR) | Monthly rate × 12; represents the annual cost of carrying an unpaid balance | Card MITC / KFS |

| Finance Charge | Actual rupee amount of interest billed on your monthly statement | Monthly credit card statement |

| Interest-Free Period | Days between transaction and due date with no interest — applies only when full dues are paid | Card MITC / KFS |

| Minimum Amount Due | Smallest payment to keep account active; does not prevent interest on remaining balance | Monthly credit card statement |

| Cash Advance Fee | One-time fee on cash withdrawal using credit card; interest also starts immediately from withdrawal date | Card MITC / KFS |

| Revolving Credit | Carrying an unpaid balance from one billing cycle into the next, attracting continuous finance charges | Card MITC / KFS |

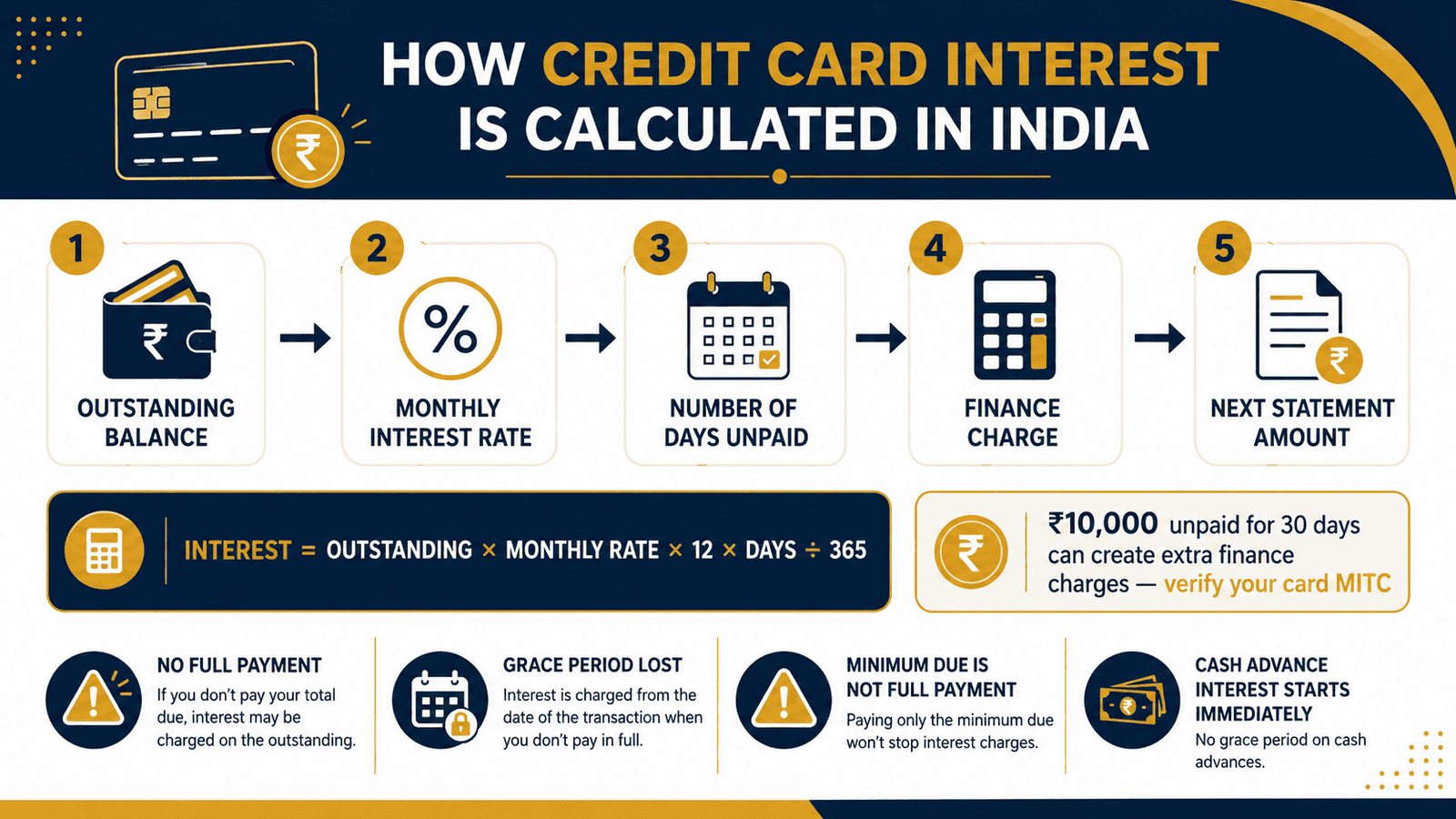

How Credit Card Interest Rate Works in India

Every credit card operates on a billing cycle — typically 30 days. When the cycle closes, your bank generates a statement listing all transactions, the total outstanding amount, the minimum amount due, and the payment due date. Understanding where these three dates fall — and what happens if you pay less than the full outstanding — is the entire foundation of how credit card interest works.

Transaction Date, Statement Date, and Due Date

When you spend ₹8,000 at an electronics store, your card records the transaction date. Your billing cycle closes on the statement date, at which point the bank generates a statement showing the full balance owed. The bank then allows a further window — typically 18 to 21 days — before the payment due date.

The combined window from your transaction date to the due date can range from a few days to more than 50 days, depending entirely on when in the billing cycle the purchase was made. A purchase made on the first day of a 30-day billing cycle, with a 20-day payment window after the statement date, gives you the full benefit. A purchase made on the last day of the cycle gets only the 20-day post-statement window. For a complete breakdown of how these dates work together, read how the billing cycle and grace period work.

The Interest-Free Period — When It Actually Applies

The interest-free period is the window during which your purchases attract zero interest. This benefit applies only under one condition: you must pay the total amount due in full by the due date. Paying even ₹1 less than the full outstanding breaks this benefit.

There is a second, less obvious condition. If you are carrying any unpaid balance from the previous billing cycle, the interest-free period on new purchases in the current cycle may not apply at all. Fresh transactions can begin accruing interest from their transaction date immediately — not from the due date. This is why one missed full payment can trigger interest charges across the next several cycles of spending, even on purchases you intended to pay in full.

What Happens When You Pay Less Than the Full Balance

If the full outstanding is not paid by the due date, the bank applies finance charges on the unpaid amount. According to RBI guidelines on credit card operations, issuers are required to state the interest rate and the method of calculation clearly in the MITC and KFS. Most Indian card issuers calculate this charge using a daily rate derived from the annual percentage rate.

For example, an APR of 42% works out to a daily rate of approximately 0.115%. On an unpaid balance of ₹25,000, that is roughly ₹28.75 per day, or approximately ₹862 over 30 days. This amount appears on your next statement as “finance charges” or “interest charged.” It is charged in addition to your regular outstanding balance — so the total you owe keeps growing as long as any unpaid balance remains.

How New Purchases Are Affected by a Carried Balance

Once an unpaid balance rolls into the next cycle, interest may apply to new purchases from their transaction date — not from the next due date. The grace period effectively disappears until you clear the full outstanding amount. Many cardholders discover this only after paying minimums for two or three cycles and finding the balance has not reduced as expected.

How Issuers Determine the Calculation Method

The actual calculation methodology can vary between issuers. Some banks apply interest from the transaction date on the full original purchase amount once full payment is missed. Others apply interest only on the net unpaid balance. Some use the daily balance method; others use the average daily balance. The specifics are in the MITC or KFS — not in the annual report or the welcome letter. RBI directions on credit cards require all these terms to be disclosed, but the method itself is set by each issuer within regulatory limits.

GST on Finance Charges

Finance charges and late payment fees are classified as financial services, so 18% GST applies on top of the interest amount billed. This means the effective cost of carrying an unpaid balance is marginally higher than the stated interest rate alone. The GST amount will appear as a separate line on your statement and should be factored into any repayment estimate.

Real Example: Aarav’s First Credit Card Bill

Aarav, 29, is a software engineer in Bengaluru earning ₹95,000 per month. He got his first credit card six months ago and uses it for fuel, grocery delivery, and online shopping. His billing cycle closes on the 5th of each month, with a due date on the 25th.

This month, his statement showed a total outstanding of ₹30,000. Aarav checked his bank balance, found it a little tight, and decided to pay ₹5,000 — the minimum amount due — before the 25th. His account registered no overdue flag.

What Aarav did not see coming: the remaining ₹25,000 became an unpaid interest-accruing balance. Using a monthly rate of 3.5% (verify the current rate from your specific card’s MITC before relying on this figure), the finance charge on ₹25,000 for the next 30 days works out to approximately ₹875. On his next statement, this ₹875 appears as a finance charge — not as a late fee, and not because Aarav missed a payment date.

Additionally, because Aarav now carries an unpaid balance into the new cycle, any new purchases he makes this month may begin accruing interest from their transaction dates. The interest-free benefit he had assumed would always apply is now suspended until he clears the full outstanding.

Paying the minimum due is not the same as clearing your dues. Read why the minimum amount due can be a dangerous long-term habit and how it keeps balances alive longer than most cardholders expect.

How to Calculate Credit Card Finance Charges

The simplified formula for estimating credit card finance charges uses the annual percentage rate and the number of days the balance is held:

Finance Charge = Outstanding Balance × Annual Rate ÷ 365 × Number of Days

Using a monthly rate of 3.5% — which equals an APR of 42% — on an unpaid balance of ₹10,000 held for 30 days:

Finance Charge = ₹10,000 × 42% ÷ 365 × 30 = ₹10,000 × 0.001151 × 30 ≈ ₹345

Alternatively, the simplified monthly approach gives: ₹10,000 × 3.5% = ₹350 for one full month. The small difference is a rounding artefact from the daily method.

This is a simplified estimate. Your actual statement figure may be higher because the issuer may apply interest from the transaction date on the full original purchase amount, compounding can apply if the balance rolls across multiple cycles, and 18% GST is added on top of the interest amount billed.

| Scenario | Unpaid Balance and Illustrative Rate | Estimated Monthly Finance Charge |

|---|---|---|

| Low outstanding | ₹10,000 at 3.5% per month | ≈ ₹350 |

| Mid outstanding | ₹25,000 at 3.5% per month | ≈ ₹875 |

| High outstanding | ₹50,000 at 3.5% per month | ≈ ₹1,750 |

Rates shown are illustrative — verify the current rate from your card’s MITC before using these estimates for any repayment decision. Use the credit card interest calculator to plug in your card’s specific rate and outstanding balance for a more accurate estimate.

Comparison: Interest and Fee Impact by Payment Behaviour

| Payment Situation | Interest and Finance Charge Impact | Grace Period Status on New Purchases |

|---|---|---|

| Full amount paid by due date | No interest on purchases | Grace period active next cycle |

| Minimum amount due paid; balance remaining | Finance charges on full unpaid balance | Grace period typically lost |

| Partial payment — more than minimum, less than full | Finance charges on remaining unpaid balance | Grace period typically lost |

| No payment by due date | Finance charges plus late payment fee | Grace period lost; account flagged overdue |

| Cash withdrawal using credit card | Interest from day one; cash advance fee also charged | No grace period — ever |

How to Decide What’s Right for You

your salary arrives before the payment due date and the full outstanding is within your monthly budget — pay the total amount due in full every cycle. You pay zero interest on purchases and retain the full grace period benefit next month.

you are temporarily short on funds this month — pay as much above the minimum as your cash flow allows, stop non-essential new spending on the card, and aim to clear the remaining balance within the next one or two cycles before finance charges compound.

your unpaid balance has grown to more than 50% of your credit limit and you are paying only the minimum each cycle — check whether your issuer offers a balance-to-EMI conversion at a lower interest rate, and calculate the total payable including all fees before agreeing to any conversion.

you have a large planned purchase coming up — make the transaction at the start of your billing cycle to maximise the interest-free window, and commit to paying the full outstanding by the due date rather than splitting the repayment across months.

you are considering a cash withdrawal from your credit card for an urgent need — evaluate whether the urgency is genuine. Interest begins the same day, the cash advance fee adds to the cost, and the effective annual rate is among the highest available to individuals in India.

you consistently have surplus income to clear the full outstanding each cycle — a credit card is not a revolving line of credit to lean on month after month. Carrying an unpaid balance across cycles at 36%–48% per year erodes savings faster than almost any financial product can earn — this pattern is worth addressing before it grows.

Common Mistakes to Avoid

Paying Only the Minimum Due, Every Single Month

The minimum amount due prevents an overdue flag on your account — nothing more. Paying only ₹5,000 on a ₹30,000 statement leaves ₹25,000 accruing finance charges. At a monthly rate of 3.5%, that is approximately ₹875 added to your next statement even if you make no new purchases.

Pay the highest amount your cash flow allows each cycle. Even clearing ₹20,000 of the ₹30,000 balance reduces your interest cost significantly compared to paying only the minimum.

Withdrawing Cash Using Your Credit Card

A credit card cash advance is one of the most expensive financial transactions available to a salaried individual in India. It triggers a one-time cash advance fee plus daily interest from the date of withdrawal — no grace period, no exceptions. The combined effective annual cost can exceed 50% once the advance fee is factored in. Read the full breakdown of credit card cash advance charges and why to avoid them before considering this option.

Use a debit card, UPI, or a personal loan for urgent cash needs — almost all alternatives are cheaper.

Assuming Reward Points Offset Finance Charges

Most reward programmes return between 0.5% and 2% of spend as points or cashback. A single month of finance charges at 3.5% on even a modest unpaid balance wipes out months of reward accumulation. Rewards are a benefit of disciplined usage — not a reason to carry a balance.

Ignoring the Statement Date Versus the Due Date

Many cardholders confuse the statement generation date with the payment due date and assume they have more time than they do. Missing the due date by one day can trigger both a late payment fee and a full month of finance charges simultaneously.

Set a calendar reminder three days before the due date — not on it.

Looking at the EMI Amount Without Calculating Total Cost

Converting an unpaid balance to an EMI may carry a processing fee and an interest rate that is sometimes comparable to the revolving credit rate. Always compute the total amount payable — principal plus all fees and interest — across the full EMI tenure before agreeing to a conversion.

Believing Interest Stops After a Partial Payment

Paying ₹15,000 against a ₹30,000 balance reduces the principal, but finance charges continue on the remaining ₹15,000 from the payment date until the full balance reaches zero. Interest does not pause or reset at any point once you are in a revolving balance situation.

When This May Not Be the Right Choice

Using a credit card — or continuing to carry a revolving balance — may not suit your current situation if any of the following apply.

Your income is irregular, freelance-based, or commission-driven, making it difficult to predict with confidence whether the full outstanding will be available by the due date each month. Missed full payments in this pattern quickly compound.

You already carry high-interest personal loan debt at 14%–20% per year. Adding revolving credit card balances at up to 48% annually creates multiple expensive borrowing layers simultaneously — and the credit card balance is likely the most expensive one.

You have established a habit of paying only the minimum amount due for three or more consecutive months, meaning the balance is growing, not reducing.

You are currently using the credit card to fund routine monthly living expenses — rent, groceries, utilities — that cannot be cleared from the same month’s income. This creates a structural dependence on revolving credit that is difficult to exit without a lump-sum payment.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card interest rates, finance charges, late payment fees, and billing methodology are governed by RBI directions on credit card and debit card operations. The Reserve Bank of India publishes all regulatory guidelines, circulars, and directions at rbi.org.in. Your card issuer — whether a scheduled commercial bank or an NBFC — is required by RBI to disclose all applicable rates, fees, and calculation methods in the Most Important Terms and Conditions (MITC) or Key Fact Statement (KFS), available from your issuer’s website or customer care at any time.

- RBI regulatory guidelines and directions: rbi.org.in

- Card-specific interest rate, fees, and billing terms: MITC / KFS from your issuer’s official website or app

- Actual finance charges billed to your account: your monthly credit card statement

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

To locate and understand the finance charge, payment due date, and billing cycle entries on your own bill, read how to read a credit card statement line by line.

Expert Tips

- Set autopay for the total amount due — not the minimum. Most Indian card issuers allow this through net banking or the mobile app. One-time setup eliminates the risk of accidentally paying only the minimum and triggering finance charges you did not intend to incur.

- Track your statement date and due date as two separate calendar events. The statement generates on one date; the due date is typically 18–21 days later. Confusing them is one of the most common reasons for missed full payments.

- Never use your credit card at an ATM for cash unless it is a genuine emergency. The combination of a one-time cash advance fee and daily interest with no grace period makes it one of the most expensive ways to access money in India — UPI, debit, or a short-term personal loan are almost always cheaper.

- Keep credit utilisation below 30% of your total limit before the statement date. At a ₹1,00,000 credit limit, spending above ₹30,000 before the statement generates can affect your CIBIL score and indicates higher credit dependence — paying down before the statement date may help maintain disciplined usage over time.

- Read the MITC before accepting a card upgrade or a new card offer. Interest rates and fee structures differ between card variants even from the same issuer — the rate on your existing card is not automatically the rate on an upgraded card.

- If you spot an unexpected finance charge on your statement, contact customer care immediately and quote your MITC. A one-time waiver is sometimes available for first-time delays — but only if you clear the full outstanding balance at the same time. Repeat occurrences are rarely waived.

Frequently Asked Questions

What is credit card interest rate?

Credit card interest rate is the finance charge applied on the unpaid outstanding balance when you do not pay the full amount due by the due date. In India, it is typically quoted as a monthly percentage rate, with the annual equivalent — the Annual Percentage Rate (APR) — disclosed in the card’s MITC or Key Fact Statement. As of recent data, monthly rates across Indian issuers typically range from 3% to 4%, but verify your specific card’s current rate from the MITC before relying on any figure.

Is interest charged even if I pay the minimum amount due on time?

Yes. Paying the minimum amount due keeps your account from being marked overdue, but any remaining unpaid balance continues to attract full finance charges. Interest accrues on every rupee of the balance that was not cleared by the due date. Paying the total amount due in full is the only way to stop interest from accruing on purchases.

Does credit card interest start only after the due date?

For purchases, interest begins accruing after the due date if the full payment is not made. However, once you carry an unpaid balance into a new billing cycle, new purchases may attract interest from their individual transaction dates — not from the next due date — because the grace period is suspended. For cash withdrawals, interest starts from the date of withdrawal regardless of any due date.

How do I convert a monthly credit card rate to an annual rate?

Multiply the monthly rate by 12. A monthly rate of 3% equals an APR of 36%; a monthly rate of 4% equals an APR of 48%. Many issuers also state the APR directly in the MITC or KFS. When comparing two card offers, always compare using the APR — not the monthly rate — for a consistent view of the annual cost of carrying a balance.

Does a cash withdrawal using a credit card get a grace period?

No. Cash advances on a credit card begin attracting interest from the date of the withdrawal itself. There is no grace period under any circumstances. A one-time cash advance fee is charged separately and appears on the same statement. Both the fee and the daily interest are stated in the card’s MITC.

Can credit card interest be reversed?

Some issuers offer a one-time interest waiver for cardholders experiencing their first delay, provided the full outstanding balance is cleared immediately when requesting the waiver. This is not guaranteed and depends entirely on the issuer’s internal policy. Do not plan your repayment around the possibility of a waiver — assume the charge will stand and clear the full balance as quickly as possible.

What is the difference between a finance charge and a late payment fee?

Finance charges are interest on the unpaid outstanding balance — they apply even if you paid the minimum amount due on time, as long as any balance remains unpaid. A late payment fee is a fixed or percentage-based penalty charged specifically when even the minimum amount due is not paid by the due date. Both can appear on the same statement simultaneously if a full payment was missed.

What is the interest-free period on a credit card and when does it apply?

The interest-free period is the window between a purchase transaction date and the payment due date during which no interest is charged — typically up to 50 days for purchases made early in the billing cycle. This benefit applies only when you pay the total amount due in full by the due date each cycle. If you carry any unpaid balance from a previous cycle, the interest-free period on new purchases may not apply in the current cycle.

Final Verdict

The credit card interest rate is a charge you can almost always avoid entirely. Pay the full outstanding balance by the due date every cycle, and the credit card interest rate remains a number in a terms document that never appears on your actual statement. Use the card for planned, budgeted purchases, collect whatever rewards the card offers, and treat the payment due date as a hard deadline — not a guideline.

The moment you start carrying an unpaid balance or making cash withdrawals, the effective annual cost rises to 36%–48% or higher — as of recent data — making it one of the most expensive forms of routine borrowing available to individuals in India. Minimum due payments and revolving balances are easy to enter and slow to exit. The only durable strategy is full repayment, every cycle.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.