You earn ₹15 LPA, your employer provides some health cover, and every year the plan to sort out personal insurance gets pushed to next quarter. Most salaried employees in Bengaluru, Mumbai, or Delhi follow this exact pattern — until a family hospitalisation bill arrives and the employer’s ₹3–5 lakh group cover covers less than half of it.

Health insurance cover for 15 LPA income is not a single fixed number. It depends on how many people you cover, which city you live in, whether your parents are dependants, and how large a bill you can absorb before it drains savings you have spent years building. A ₹5 lakh cover bought three years ago for a single person is a different conversation from the cover a married couple with ageing parents needs in a metro city today.

This article builds a salary-linked decision framework — covering base plans, super top-ups, family floaters, and employer cover limitations — so you can choose the right structure, not just the cheapest plan. For a broader starting point, read our insurance guide for Indian families.

Quick Answer: How Much Health Insurance Cover for ₹15 LPA Income?

Health insurance cover for 15 LPA income is usually around ₹10–25 lakh base cover, or ₹5–10 lakh base plus ₹20–50 lakh top-up. The right amount depends on city, age, family size, employer cover and comfort with large hospital bills.

Key Takeaways

- A ₹5 lakh base cover is often insufficient for a metro private hospital bill — a single cardiac procedure or cancer treatment in Bengaluru or Mumbai can cost ₹8–20 lakh.

- ₹10–25 lakh base cover is a practical range for a ₹15 LPA earner in a Tier-1 city, depending on family size, age, and existing employer cover.

- A super top-up plan with ₹25–50 lakh cover can significantly extend protection at a fraction of the cost of buying an equally large standalone base policy.

- Employer group insurance stops on resignation — it should be treated as a supplement to personal cover, not your primary protection.

- A family floater shares the sum insured across all members: one large parental claim can leave the rest of the family with minimal cover for the remainder of that policy year.

- Section 80D allows a deduction of up to ₹25,000 per year on premiums for self and family, and up to ₹50,000 for premiums paid for senior citizen parents (aged 60 and above).

- Medical inflation in India consistently runs above 10% annually — cover that felt adequate five years ago may no longer be adequate today.

Comparison: Health Insurance Cover Structures for ₹15 LPA Income

Before the detailed explanation, here is how common cover structures compare for a salaried person earning ₹15 LPA. The right structure depends on your specific profile — use this table to identify where you sit.

| Cover Structure | Who It Typically Suits | Key Trade-Off |

|---|---|---|

| ₹5 lakh base only | Single person, Tier-2 or Tier-3 city, low-risk health profile, strong employer cover already in place | Likely insufficient for a single major metro private hospital admission above ₹5 lakh |

| ₹10 lakh base only | Couple without dependants in a metro; no senior parents on the policy; buying personal cover for the first time | Reasonable starting floor; no buffer if claims are multiple or very large in a single year |

| ₹10 lakh base + ₹25 lakh super top-up | Metro resident with family; cost-conscious buyer wanting strong catastrophic cover without a very large base premium | Strong structure; top-up only activates after aggregate claims cross the deductible — base must cover routine claims first |

| ₹15–25 lakh family floater | Couple with one child; no senior dependants; all members in good health with no chronic conditions | More comprehensive base, but shared pool — one large claim reduces cover for every other member for the rest of that policy year |

| Separate individual cover for each member | Families with senior parents, pre-existing diseases in the household, or members with elevated hospitalisation history | Higher combined premium; each member retains full sum insured independently — no shared-pool risk |

For a detailed breakdown of how individual and floater policies compare across claim scenarios, read our guide on individual vs family floater health insurance.

Key Facts at a Glance

| Factor | Detail | Why It Matters |

|---|---|---|

| Income level | ₹15 LPA (approx. ₹1.25 lakh/month) | Higher income means both more capacity for premium and more accumulated savings to protect from a large medical bill |

| Suggested personal base cover | ₹10–25 lakh depending on family profile | Covers most major metro private hospital procedures without wiping out savings |

| Super top-up option | ₹25–50 lakh above a defined deductible | Extends protection for catastrophic hospitalisation at significantly lower incremental premium than a larger base plan |

| 80D deduction — self and family | Up to ₹25,000 per year | Reduces taxable income; applicable on premium paid for self, spouse, and dependent children |

| 80D deduction — senior citizen parents | Up to ₹50,000 per year | Additional deduction for premiums paid for parents aged 60 or above |

| Typical employer group cover limitation | Often ₹3–5 lakh; not portable on resignation | Can change terms every year; may not cover parents; stops immediately when employment ends |

Understanding Health Insurance Cover for Salaried Employees in India

Sum Insured Is Not the Same as Premium

Sum insured is the maximum amount your insurer pays for hospitalisation in a policy year. Premium is the annual cost you pay to keep the policy active. These two numbers do not move in a straight line — a ₹25 lakh sum insured does not cost five times the premium of a ₹5 lakh plan, especially if you build your protection using a base-plus-top-up structure.

Many first-time buyers equate higher cover with an unaffordable premium and never revise their sum insured beyond ₹5 lakh. That decision often leads to a large out-of-pocket payment during an actual hospitalisation. Before choosing a cover amount, it helps to understand exactly what your policy will and will not pay — read our full guide on what health insurance covers and what it does not.

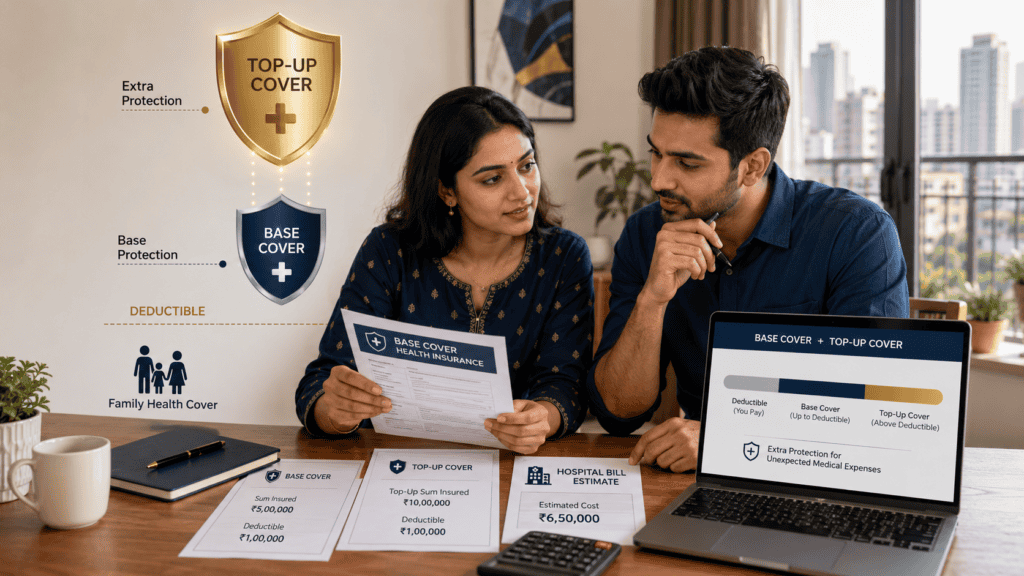

Base Plan vs Super Top-Up: Two Layers, One Framework

A base health insurance plan activates from the first rupee of a hospitalisation bill, subject to waiting periods and exclusions. A super top-up plan activates only after your total hospitalisation expenses in a policy year cross a predefined deductible — for example, ₹10 lakh.

The logic is efficient: you buy a ₹10 lakh base plan that handles most admissions. You simultaneously buy a ₹25–50 lakh super top-up with a ₹10 lakh deductible. If a single hospitalisation or the combined bills in a year cross ₹10 lakh, the top-up pays the excess. Your effective protection reaches ₹35–60 lakh — at a total premium substantially lower than buying a standalone ₹35 lakh base policy. According to IRDAI’s consumer awareness material, understanding how deductibles work is one of the most important factors before selecting a top-up plan.

Family Floater Means One Shared Pool

A family floater policy covers all enrolled members under a single sum insured. If your ₹15 lakh floater covers two adults and one child, and one member is hospitalised for ₹12 lakh, the remaining ₹3 lakh is the only protection available for the rest of the family for the remainder of that policy year.

Individual covers assign a separate sum insured to each member. The combined premium is higher — but each person retains their full cover regardless of what any other member claims. For families with senior parents, chronic conditions, or members who have had recent hospitalisations, individual covers are usually worth the difference in premium.

Employer Group Insurance: Useful While It Lasts

Your employer’s group health insurance is a meaningful benefit while you are employed at that company. The day you resign, the cover ends. When you join a new employer, the new group plan typically has its own waiting period for pre-existing conditions before you are fully protected. In between — during notice period, between jobs, or during job hunting — you may have no active cover at all.

Group policies are also renewed annually by your employer. The insurer, the terms, the sum insured, and any sub-limits can change every renewal cycle without your input. A room-rent cap that was acceptable in 2021 may be entirely inadequate against 2025 private hospital charges in Bengaluru or Hyderabad. Treat employer cover as useful backup — not as your primary or permanent health insurance.

Room Rent Limits, Co-Payment, and Waiting Periods

Three policy features determine whether your sum insured delivers its full value in a real claim. Room rent limits cap how much the insurer pays for your daily hospital room — and many policies proportionally reduce all other claim components, including surgery and ICU charges, if you choose a room above that cap. Co-payment clauses require you to bear a fixed percentage of every claim from your own pocket, regardless of the sum insured. Waiting periods — typically two to four years for pre-existing diseases — mean a condition you develop today may not be covered in your new policy for several years.

A ₹25 lakh policy with aggressive sub-limits can behave like a ₹12–15 lakh policy in an actual claim. Always read the full policy document before buying. The brochure and the policy schedule are different documents.

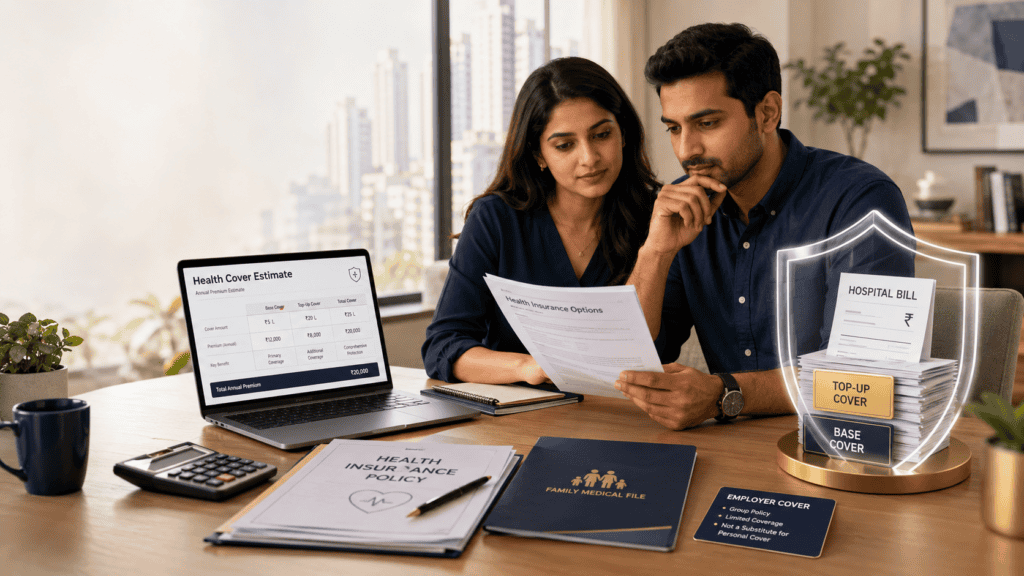

Real Example: Rohit’s Cover Decision in Bengaluru

Rohit is 31 years old, works as a software engineer in Bengaluru, and earns ₹15 LPA. His employer provides group health insurance of ₹5 lakh for employees only. He is married, has no children yet, and his parents — aged 58 and 62 — live in Pune and are not covered under his employer plan.

A cardiologist evaluation, stenting procedure, and post-operative care at a leading private hospital in Bengaluru can cost ₹7–12 lakh. If Rohit or his wife needed a similar procedure, the ₹5 lakh employer cover would fall well short. After reviewing his situation, Rohit buys a ₹10 lakh family floater base plan for himself and his wife, plus a ₹25 lakh super top-up with a ₹10 lakh deductible. For his parents, given his father’s age and a managed blood pressure condition, he buys separate individual senior citizen health policies rather than adding them to the floater.

His approximate annual premium for the couple’s ₹10 lakh base floater is ₹15,000–₹18,000, and the super top-up adds roughly ₹6,000–₹10,000 per year — a total of ₹21,000–₹28,000. His effective protection for any claim exceeding ₹10 lakh rises to ₹35 lakh, without paying the premium of a standalone ₹35 lakh base policy. This is an illustrative scenario — actual premiums vary by age, health condition, insurer, city, and policy terms.

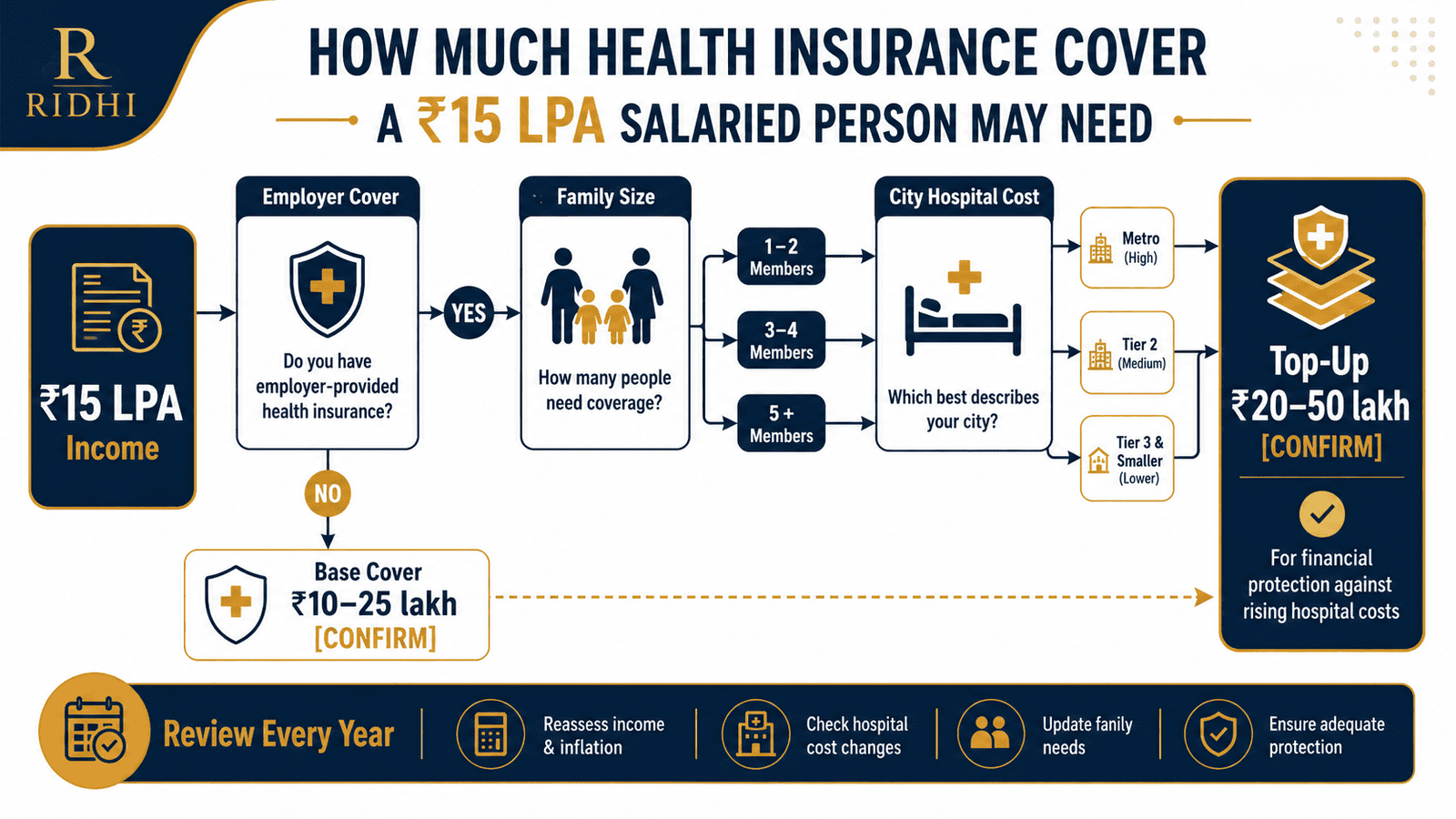

How to Calculate the Right Health Insurance Cover

Minimum Cover Needed = Realistic Major Hospital Bill (your city) − Employer Cover Available + Buffer for Dependants and Medical Inflation

Step 1 — Estimate one major private hospital bill in your city. In metro cities, a cardiac bypass or valve surgery costs ₹5–12 lakh. A cancer treatment cycle — chemotherapy plus hospitalisation — can run ₹8–20 lakh. A 7–10 day ICU stay at a top private hospital in Bengaluru, Mumbai, or Delhi can approach ₹4–8 lakh. For Tier-2 cities, use roughly 40–50% of metro figures as a reference point.

Step 2 — Subtract your existing employer cover. If your employer provides ₹5 lakh, your uncovered gap on a ₹12 lakh procedure is ₹7 lakh. If employer cover is nil or you are between jobs, the entire amount is your personal liability.

Step 3 — Set your base cover at or above the gap. A ₹10 lakh base plan covers the gap from Step 2 and also handles most moderate hospitalisations independently. This is your first layer of financial protection.

Step 4 — Add a super top-up for catastrophic risk. Use the top-up to cover the scenario where a single hospitalisation or multiple admissions in one year push the total well beyond your base. A ₹25 lakh super top-up with a ₹10 lakh deductible costs significantly less than adding ₹25 lakh more to your base plan. For a full explanation of how this mechanism works in practice, read our guide on top-up health insurance and how it extends your coverage.

Step 5 — Test the total premium against your budget. At ₹15 LPA, a combined annual health premium of ₹25,000–₹35,000 for base and top-up covers for a couple in their early 30s is typically manageable. After the Section 80D deduction, the net after-tax premium cost is lower still.

| Scenario | Cover Structure | Effective Max Protection |

|---|---|---|

| Employer cover only | ₹5 lakh group plan | ₹5 lakh — ends on resignation |

| Personal base plan only | ₹10 lakh individual or floater | ₹10 lakh personal + ₹5 lakh employer = ₹15 lakh while employed |

| Base plus super top-up | ₹10 lakh base + ₹25 lakh super top-up | Up to ₹35 lakh personal protection, independent of employment |

How to Decide What’s Right for You

You are single, living in a Tier-2 city, and your employer provides ₹5 lakh group cover — THEN a personal base plan of ₹5–10 lakh provides a reasonable starting floor, giving you portable cover that survives a job change and a buffer above employer limits.

You are married with no children in a metro city and your employer cover is ₹3–5 lakh — THEN a ₹10 lakh personal family floater plus a ₹25 lakh super top-up is a widely adopted structure for this income and life stage, giving meaningful catastrophic protection without a very large base premium.

You have a child or are planning to start a family in the next one to two years — THEN add the child to your floater and confirm that your policy covers maternity and newborn complications under the terms applicable at the time of birth, including any applicable waiting periods.

You have dependent parents aged 60 or above — THEN evaluate separate individual senior citizen policies for them, rather than adding them to your personal family floater, so that one large parental claim cannot reduce your family’s available cover for the rest of the policy year.

You are planning to change jobs, go freelance, or take a career break within the next 12–18 months — THEN buy a personal base plan now, before the change, so you have continuous cover and waiting periods have already begun running before your employment status changes.

You may not need to add a super top-up immediately if your existing personal base cover (independent of employer plan) already exceeds ₹20–25 lakh with no significant sub-limits, and you have no dependants with elevated health risk or chronic conditions — in that case, reviewing your base cover comprehensiveness may be the more useful step.

To test how different cover amounts and structures affect your annual premium before committing, use the health insurance premium calculator for salaried families.

Common Mistakes to Avoid

Relying Only on Employer Group Insurance

Employer group cover ends the moment you resign, are laid off, or retire early.

If you develop a chronic condition during employment and then leave the job, the new employer’s group plan will likely impose a waiting period on that condition — leaving you uninsured on that disease precisely when you need cover. The gap between two jobs, even a short one, carries real financial risk.

Buy a personal health insurance policy while your employer cover is active, so you always have portable continuity cover regardless of employment status.

Choosing the Cheapest Plan Without Reading the Policy Document

A ₹10 lakh plan with aggressive room-rent sub-limits and a co-payment clause can deliver far less than ₹10 lakh in an actual claim.

If your policy caps room rent at ₹2,500 per day and you stay in a ₹6,000-per-day room, many insurers will proportionally reduce your entire claim — not just the room cost, but surgery charges, ICU costs, and other components. A ₹10 lakh policy with this structure may pay out ₹4–5 lakh on a ₹9 lakh bill.

Compare actual policy terms — room-rent cap, co-pay clause, disease sub-limits — not just the headline premium.

Adding Senior Parents to a Family Floater Without Evaluating the Risk

Enrolling parents aged 60–70 in a family floater concentrates high-probability claim risk into a shared pool.

If your mother is hospitalised for ₹9 lakh in February under a ₹10 lakh family floater, only ₹1 lakh remains to protect your spouse and yourself for the rest of that policy year. One large parental claim — a cardiac event, a hip replacement, a cancer diagnosis — can leave the entire family effectively uninsured until the next renewal.

Consider separate individual senior citizen policies for parents so that each member’s sum insured is fully independent.

Not Disclosing Pre-existing Diseases at the Time of Application

Concealing hypertension, diabetes, a previous surgery, or any known chronic condition to secure a lower premium is one of the most expensive mistakes an Indian health insurance buyer can make.

If the insurer discovers non-disclosure at claim time — and most do, through medical records, discharge summaries, and investigation — the claim can be rejected entirely. A premium saving of ₹3,000–₹5,000 per year is not worth a rejected claim of ₹8–15 lakh. IRDAI guidelines require full and accurate disclosure of all known health conditions at the time of application.

Disclose everything honestly. Many conditions are still insurable — often with a waiting period or a loading on premium — and honesty at application protects your claim.

Ignoring Waiting Periods When Buying or Switching a Policy

Most health insurance policies carry a two-to-four-year waiting period for pre-existing diseases and a one-to-two-year waiting period for specific listed conditions such as cataracts, hernia, or joint replacement.

If you buy a new policy after a condition has developed, that condition is not covered for several years. The waiting period clock restarts with every new policy, unless you port the policy using the IRDAI-mandated portability process and maintain continuity of cover without a break.

Do not wait until you are unwell to review or increase your health insurance.

Never Reviewing Cover After Major Life Events

A ₹5 lakh policy bought at age 26 for a single person in Pune does not serve a 33-year-old married person with a child in Bengaluru.

Medical inflation in India consistently runs above 10% annually. The ₹5 lakh that covered a procedure in 2016 may cover half of the equivalent procedure today. Cover that was adequate at your last policy review may leave a significant gap by the time you actually need it.

Review your sum insured after marriage, childbirth, a parent becoming a dependant, a city change, or a significant salary increase — whichever comes first.

Treating Super Top-Up as a Standalone Policy

A super top-up plan requires that the total hospitalisation bill in a policy year crosses the deductible before it pays a single rupee.

If you buy a ₹25 lakh super top-up with a ₹10 lakh deductible but have no base plan that covers the first ₹10 lakh, you are personally responsible for that entire deductible out of pocket in any given hospitalisation. A super top-up only works as intended when paired with a base plan whose sum insured at least equals the deductible.

Always structure base cover and top-up cover together — not as independent, unconnected products.

When This May Not Be the Right Choice

A ₹10–25 lakh base cover recommendation is not the right starting point for every ₹15 LPA earner.

If you already hold a personal health policy with ₹20 lakh or more, no room-rent sub-limits, and a low waiting period remaining on existing conditions, adding more base cover may not be the immediate priority. A super top-up or a critical illness rider may be a more efficient next step.

If you or a close family member has a serious pre-existing condition, recent major hospitalisation, or an active treatment plan, standard retail health policies may impose high premium loading or broad exclusions. A specialist insurer or a group policy with less restrictive underwriting may need separate evaluation before committing to a standard retail plan.

If your employer provides an unusually comprehensive group plan — ₹15 lakh or above, no sub-limits, covering parents, with a portability agreement on exit — the urgency for an equally large personal base plan is lower, though personal cover for continuity is still advisable.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Health insurance in India is regulated by the Insurance Regulatory and Development Authority of India (IRDAI). Rules on portability, waiting periods, standardised exclusions, and claim settlement timelines are set and updated by IRDAI.

- IRDAI — irdai.gov.in: For regulatory guidelines, approved insurers, consumer awareness resources, and the grievance redressal process.

- Your insurer’s policy document: The exact sum insured, room-rent limits, co-payment clauses, waiting periods, and exclusions are defined in the policy schedule — not the brochure or the sales illustration. These two documents are not the same.

- Income Tax Department — incometax.gov.in: For current Section 80D deduction limits, eligibility conditions, and tax filing procedures.

Premiums vary by age, health condition, insurer, and policy terms. Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

For worked examples and current limits on the tax side, read our guide on 80D deduction for health insurance.

Expert Tips

- Buy a personal health policy while you are young and healthy — premiums are meaningfully lower before age 35, and the waiting period clock on pre-existing diseases starts running immediately. Every year you delay, both the premium and the risk of exclusions on developing conditions increase.

- Do not treat employer group cover as permanent. If you are planning a job change, a sabbatical, or a move to freelance work in the next 12 months, buy personal cover now — not after the change — so you have continuous cover without waiting periods restarting from zero.

- If you are in the 30% tax bracket and pay ₹25,000 per year in health insurance premium for yourself and your family, your effective tax saving under Section 80D is approximately ₹7,800 per year, bringing your net after-tax premium cost down to roughly ₹17,200.

- When comparing health plans, prioritise policies with no room-rent sub-limits and no co-payment clause, even if the premium is slightly higher. In an actual high-value claim, these two features have a larger impact on your payout than almost any other policy feature.

- Match your top-up deductible exactly to your base cover’s sum insured. A ₹25 lakh super top-up with a ₹10 lakh deductible only works seamlessly if your base plan covers at least ₹10 lakh. A mismatch creates a personal-liability gap between the two layers.

- Keep your emergency fund entirely separate from your health insurance cover. Insurance is not a liquid instrument — it pays the hospital directly or reimburses documented expenses, not cash-on-demand for incidental costs, lost income, or family travel during a hospitalisation.

- Set a calendar reminder to review your sum insured every three years at minimum — and immediately after marriage, childbirth, a parent becoming a dependant, or a significant salary increase. Medical inflation above 10% annually means passive inaction is effectively a slow reduction in real cover.

Frequently Asked Questions

Is ₹10 lakh health insurance cover enough for ₹15 LPA income?

₹10 lakh can be a reasonable base cover for a couple in their early 30s in a metro city with no senior dependants. However, for families with ageing parents, dependants with pre-existing conditions, or anyone in a city with high private hospital costs, ₹10 lakh base cover paired with a ₹25–50 lakh super top-up provides substantially stronger financial protection. Whether ₹10 lakh is enough depends on your city, family profile, and what a realistic worst-case hospitalisation in your nearest private hospital would actually cost.

Should I buy a top-up health insurance plan?

A super top-up is worth serious consideration if you want total protection in the ₹35–60 lakh range without paying the premium of a standalone ₹35 lakh base policy. The super top-up activates once your aggregate hospitalisation expenses in a policy year cross the deductible — making it especially valuable for metro residents, families with senior parents, and anyone with a family history of high-cost illness. It must be paired with a base plan that covers the deductible amount first.

Is employer health insurance enough as my only cover?

It is rarely enough on its own. Employer group insurance stops on resignation, can change terms or insurer every year at renewal, and typically comes with sub-limits on room rent and ICU that reduce real payout. More critically, you have no control over it. A personal health insurance policy that you own and renew independently gives you continuous cover regardless of employment status — which is the core gap employer cover cannot fill.

Should my parents be in the same family floater as me?

For parents aged 60 and above, adding them to your personal family floater carries meaningful risk. One large hospitalisation — a cardiac event, joint replacement, or cancer diagnosis — can exhaust most of the shared pool and leave your immediate family with minimal cover for the rest of the year. Separate individual senior citizen health policies for parents mean each member retains their full sum insured independently, regardless of what others claim.

Can I claim the 80D deduction on health insurance premium?

Yes. Under Section 80D of the Income Tax Act, you can deduct up to ₹25,000 per year for health insurance premiums paid for yourself, your spouse, and your dependent children. If you pay premiums for parents who are senior citizens (aged 60 or above), you can claim a further deduction of up to ₹50,000 per year. Verify current limits and conditions at incometax.gov.in before filing your return.

What happens to my health insurance when I change jobs?

Your employer group insurance ends when you leave. Your personal health insurance — bought and owned independently — continues as long as you keep paying the renewal premium. This is one of the strongest practical reasons to buy personal cover while employer cover is active, not after leaving. If you want to use the IRDAI portability facility to carry over waiting period credit when moving between personal policies, apply for portability before your current policy expires.

How often should I review my health insurance cover amount?

At least once every three years, and immediately after any significant life change — marriage, childbirth, a new city, a parent becoming a dependant, or a salary jump. Medical inflation in India consistently runs above 10% annually. ₹10 lakh of cover today buys less hospitalisation protection in five years if you do not revise the sum insured to keep pace.

Is a family floater always cheaper than individual covers for each member?

A family floater is typically cheaper in total premium for a young, healthy family where the probability of multiple large claims in the same year is low. Individual covers cost more in combined premium but give each member a fully independent sum insured. For families where any member has a chronic condition, elevated hospitalisation history, or is above age 60, the effective protection of individual covers often justifies the higher premium.

Can I hold both employer health insurance and a personal health insurance policy at the same time?

Yes, and it is generally advisable. There is no restriction on holding both. For a single hospitalisation, you can claim from one policy first and submit the balance to the second insurer, subject to each insurer’s co-ordination of benefits terms. More practically, having both means you are never entirely without cover during job transitions — the personal policy continues independently of what happens to the employer plan.

What is the difference between a top-up and a super top-up plan?

A regular top-up plan pays only when a single hospitalisation bill crosses the deductible. A super top-up plan counts all hospitalisation bills in a policy year cumulatively — once the total across all admissions crosses the deductible, the super top-up pays the excess. If you have multiple hospitalisations in a year, a super top-up gives you far broader protection than a standard top-up plan at a similar or comparable premium.

Final Verdict

Health insurance cover for 15 LPA income is not a single number — it is a layered structure. For most salaried employees in metro cities, a personal base plan of ₹10–15 lakh combined with a ₹25–50 lakh super top-up provides meaningful protection against both routine hospitalisations and catastrophic bills, without requiring the premium of a very large standalone base policy.

Employer group cover is useful while it lasts. It should not be your only protection — it ends the moment your employment does. A personal health insurance policy that is portable, that grows with your family responsibility, and that you renew on your own terms is the foundation of sound financial planning at ₹15 LPA income and beyond.

Compare cover structures carefully — not just premium. Room-rent limits, co-payment clauses, waiting periods, and claim settlement history matter far more than the brochure sum insured. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.