If you are a salaried professional trying to make your Section 80C deduction work harder, the PPF vs ELSS question comes up every year — usually around February or March, right before the tax-saving deadline. Both instruments tick the 80C box. Both are popular with Indian taxpayers. But they are fundamentally different products built for different investor profiles, and choosing the wrong one — or splitting money between them without a clear plan — can mean a difference of ₹15–20 lakh or more over a 15-year horizon. PPF offers government-backed safety and fully tax-free maturity; ELSS offers equity-linked growth potential with the shortest lock-in period of any 80C option. This article breaks down PPF vs ELSS across every dimension that actually matters — returns, risk, lock-in, tax treatment, liquidity, and the tax regime question that most comparisons leave out — so you can make a decision grounded in your own situation.

Quick Answer: PPF vs ELSS

PPF vs ELSS depends on whether you prefer safe, tax-free maturity or market-linked growth. PPF suits low-risk savers with long horizons, while ELSS suits investors comfortable with equity volatility. Both can qualify under Section 80C up to ₹1.5 lakh, but tax regime and liquidity matter.

Key Takeaways

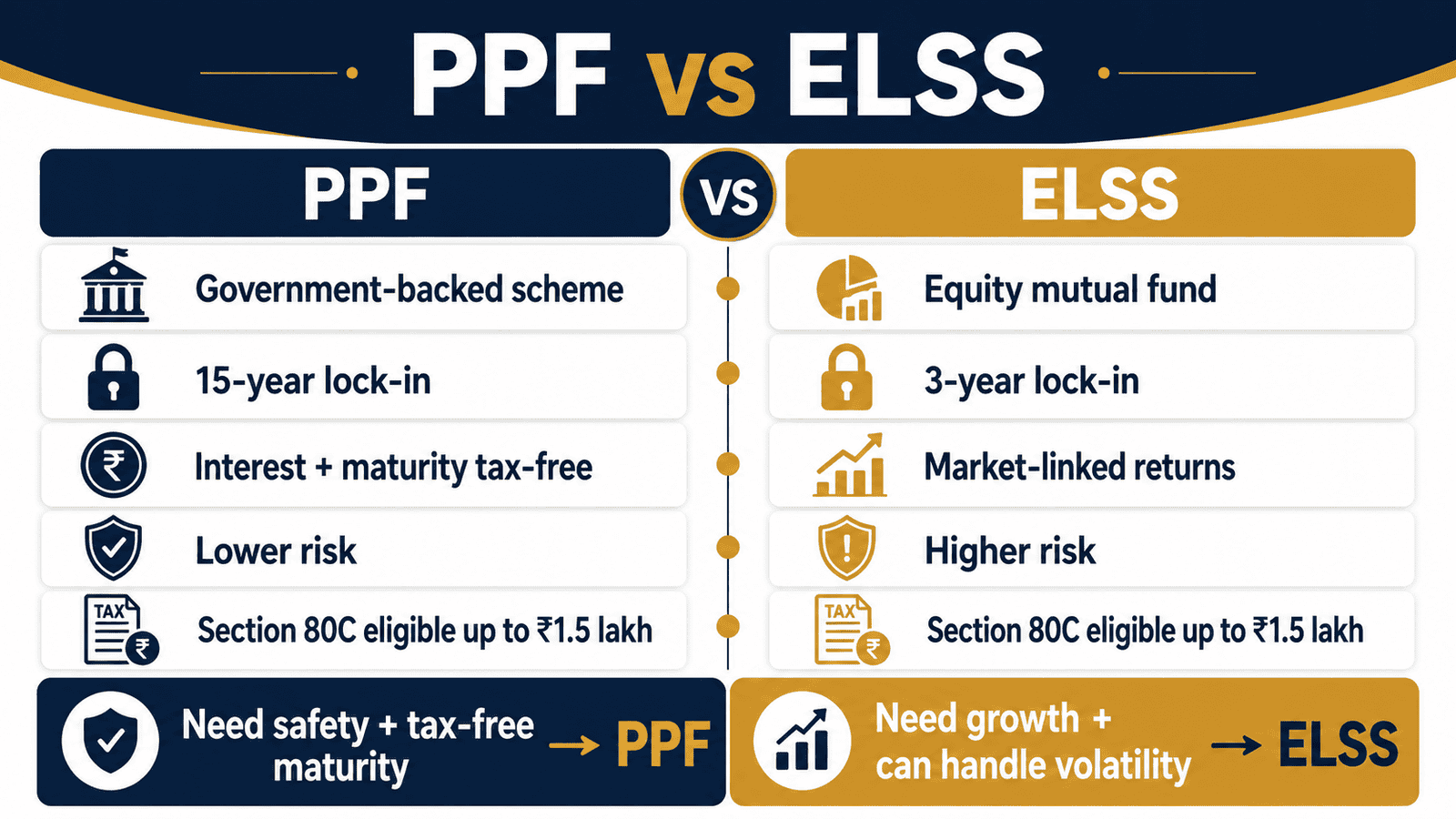

- PPF is a government-backed savings scheme with a 15-year tenure; ELSS is an equity mutual fund with a 3-year lock-in — the shortest of all Section 80C options and five times shorter than PPF.

- PPF enjoys EEE (Exempt-Exempt-Exempt) treatment: your contribution, interest earned, and maturity proceeds are all fully tax-free — no capital gains tax on exit.

- ELSS gains above ₹1.25 lakh per financial year are taxed at 12.5% as long-term capital gains — it is not a tax-free instrument at redemption, unlike PPF.

- PPF currently earns 7.1% per annum (government-declared, subject to quarterly revision); ELSS funds have historically delivered 12–14% CAGR over rolling 10-year periods, though returns are market-linked and not guaranteed.

- Investing ₹1.5 lakh per year for 15 years at 7.1% in PPF yields approximately ₹40.8 lakh — entirely tax-free; the same amount in ELSS at an assumed 12% CAGR yields roughly ₹62.6 lakh before LTCG tax.

- Under the new tax regime, Section 80C deductions are not available — so neither PPF nor ELSS gives you a tax benefit on the contribution if you file under the new regime.

- For most 30–40 year-old salaried investors with a 10+ year horizon and moderate risk tolerance, ELSS tends to build more inflation-adjusted wealth; for capital protection and predictability, PPF remains unmatched.

Comparison: PPF vs ELSS

| Parameter | PPF | ELSS |

|---|---|---|

| Investment type | Government savings scheme | Equity mutual fund (SEBI-regulated) |

| Expected returns | 7.1% p.a. (government-declared) | 12–14% CAGR historically (not guaranteed) |

| Risk level | Zero — sovereign guarantee | Medium-High — equity market risk |

| Lock-in period | 15 years (partial withdrawal from Year 7) | 3 years per investment unit |

| Section 80C deduction | Yes (old regime only) | Yes (old regime only) |

| Tax on maturity / gains | Fully tax-free (EEE status) | 12.5% LTCG on gains above ₹1.25 lakh/year |

| Liquidity | Low — 15-year tenure; partial from Year 7 | Low during 3-year lock-in; fully redeemable after |

| Best suited for | Capital protection, predictable tax-free corpus | Long-term wealth creation, inflation-beating growth |

Key Facts at a Glance

| Feature | PPF | ELSS |

|---|---|---|

| Full form | Public Provident Fund | Equity Linked Savings Scheme |

| Governed by | Ministry of Finance / Post Office / Banks | SEBI-regulated Asset Management Companies |

| Annual investment limit (80C) | ₹500 minimum; ₹1.5 lakh maximum | ₹500/month SIP; ₹1.5 lakh ceiling for 80C benefit |

| Tenure | 15 years (extendable in 5-year blocks) | No fixed tenure; 3-year lock-in per unit/SIP instalment |

| Tax treatment | EEE — contribution, interest, maturity all tax-free | EET — contribution deductible; LTCG taxable on gains above ₹1.25L |

| Mode of investment | Post Office, bank branch, net banking | Online, Demat account, fund house website, SIP |

Both PPF and ELSS sit within the broader ₹1.5 lakh Section 80C deduction basket alongside EPF contributions, LIC premiums, and home loan principal repayment. If you want to understand how much 80C room you actually have after accounting for mandatory EPF, see the complete Section 80C deduction list before deciding how to split your remaining limit between PPF and ELSS.

Understanding PPF as a Tax-Saving Instrument

The Public Provident Fund is one of the oldest and most trusted savings instruments available to Indian residents. It is backed by the Government of India, which means your principal is fully protected and the interest rate — currently 7.1% per annum, compounded annually — is declared quarterly by the Ministry of Finance and is never negative.

The key feature that makes PPF exceptional from a tax perspective is its EEE status. Your annual contribution (up to ₹1.5 lakh) is deductible under Section 80C of the Income Tax Act. The interest you earn each year is entirely exempt from tax. And when your account matures after 15 years, every rupee you receive — principal plus all accumulated interest — is tax-free in your hands. This triple exemption is rare in Indian personal finance.

PPF is not without limitations, however. The 15-year tenure is the most significant constraint. While partial withdrawals are permitted from the 7th financial year, and a loan facility is available from Year 3, your core corpus is locked away for a long time. You cannot exit early if you change your mind or face an emergency. The annual investment ceiling of ₹1.5 lakh also means it cannot be your only wealth-building vehicle if your income is higher.

The interest rate, though stable, is subject to revision each quarter. It has been 7.1% for several quarters, but it was as high as 8.7% in 2013 and as low as 7.1% in recent years. Over a 15-year horizon, you are exposed to rate revision risk — your actual compounding rate may vary from what you assume today. For a full explanation of how a PPF account works, including deposit rules, partial withdrawal conditions, and extension rules, see our Public Provident Fund guide.

Understanding ELSS as a Tax-Saving Mutual Fund

ELSS — Equity Linked Savings Scheme — is a category of mutual fund defined and regulated by SEBI. At least 80% of an ELSS fund’s corpus must be invested in equities. This is what makes it fundamentally different from PPF: ELSS gives you market-linked returns, which means both higher growth potential and real downside risk.

The 3-year lock-in period is the shortest mandatory holding period of any Section 80C instrument. Compare this to PPF’s 15 years, NPS’s retirement-linked lock-in, or NSC’s 5 years. For an investor who wants the 80C deduction but does not want to lock money away for over a decade, ELSS is the most flexible option in the basket.

The tax treatment of ELSS is more nuanced than PPF. Your investment qualifies for a Section 80C deduction in the year of investment — so a ₹1.5 lakh ELSS investment saves you ₹46,800 in tax if you are in the 30% bracket under the old regime. But when you redeem, gains above ₹1.25 lakh in a financial year are taxed at 12.5% as long-term capital gains. This is the critical difference: PPF gives you EEE, ELSS gives you EET — the exit is taxable.

Returns from ELSS are not guaranteed. Diversified equity mutual funds have historically delivered 12–14% CAGR over rolling 10-year periods, but individual fund performance varies significantly. A poorly chosen ELSS fund can underperform the index. Selecting a fund with a strong long-term track record, a consistent investment style, and a low expense ratio matters. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. According to SEBI guidelines, investors should read scheme-related documents carefully before investing. For a deeper explanation of how ELSS works as an 80C instrument, see our ELSS fund explainer.

The New Tax Regime Changes Everything

One dimension most PPF vs ELSS comparisons skip: if you have opted for the new tax regime, the entire 80C deduction is unavailable. That means neither PPF nor ELSS gives you any tax saving on the contribution. PPF still earns tax-free interest, which retains some value — but ELSS loses its primary tax advantage entirely. If you are unsure which regime you are in, this distinction is critical before you commit money to either instrument purely for tax saving.

Real Example: Rohit’s PPF vs ELSS Decision

Rohit, 32, works as a product manager at a tech company in Bengaluru. His CTC is ₹18 lakh per year. After mandatory EPF contributions of ₹21,600 per year, he has roughly ₹1,28,400 of his Section 80C limit remaining under the old regime. He wants to deploy this intelligently.

His LIC premium already uses ₹25,000 of that. So his actual remaining 80C room is ₹1,03,400. He decides to compare putting ₹1 lakh per year into PPF versus ₹1 lakh per year into an ELSS fund, both for 15 years.

At PPF’s current 7.1%, his ₹1 lakh per year yields approximately ₹27.1 lakh after 15 years — entirely tax-free. The same ₹1 lakh per year in ELSS, at an assumed 12% CAGR over 15 years, grows to approximately ₹41.8 lakh before LTCG tax, and roughly ₹38–39 lakh after estimated tax on gains. Even after tax, ELSS delivers ₹11–12 lakh more than PPF over 15 years at these assumptions.

Rohit’s key insight: his risk tolerance, not just the return difference, should drive this choice. He has no existing fixed-income buffer beyond his EPF. For him, splitting — ₹50,000 in PPF for safety, ₹50,000 in ELSS for growth — may be smarter than an all-or-nothing call.

How to Calculate PPF vs ELSS Long-Term Returns

PPF Maturity = P × [((1 + r)^n − 1) ÷ r] × (1 + r)

ELSS SIP Maturity (approximate) = P × [((1 + r)^n − 1) ÷ r] × (1 + r)

Where P = annual investment, r = annual rate, n = years. PPF: r = 7.1%. ELSS: r = assumed CAGR (historical range: 12–14%).

Using Rohit’s scenario of ₹1.5 lakh per year for 15 years:

| Scenario | Key Inputs | Estimated Maturity Value |

|---|---|---|

| PPF (conservative) | ₹1.5L/year × 15 years at 7.1% | ~₹40.8 lakh (fully tax-free) |

| ELSS (moderate) | ₹1.5L/year × 15 years at 12% CAGR | ~₹62.6 lakh before LTCG tax |

| ELSS (after estimated LTCG) | 12.5% tax on gains above ₹1.25L/year | ~₹57–58 lakh (approximate post-tax) |

These figures are illustrative. ELSS returns are not guaranteed and actual post-tax values depend on the year-by-year redemption pattern, prevailing LTCG rates, and the ₹1.25 lakh annual exemption available at the time of redemption. Use the PPF maturity calculator for a detailed year-by-year PPF breakdown, and the SIP wealth calculator to model your ELSS growth assumptions with different CAGR inputs.

How to Decide What’s Right for You

you are in the old tax regime, in the 20% or 30% bracket, and want a guaranteed, fully tax-free corpus for a goal 15+ years away — PPF is a very strong fit for at least part of your 80C allocation.

you have a 10+ year investment horizon, can tolerate seeing your portfolio fall 25–40% in a bad year without panic-selling, and want to beat inflation meaningfully — ELSS via monthly SIP is likely to outperform PPF over that period.

you have no fixed-income savings at all (no FD, no debt fund, no EPF balance above 6 months’ expenses) — use PPF first as your safe-money anchor before putting anything into ELSS.

you want the shortest possible lock-in within 80C — ELSS at 3 years is the only option; PPF ties your money for a minimum of 15 years.

you have already opted for the new tax regime — neither PPF nor ELSS provides a contribution deduction; invest in PPF for its tax-free interest, or in ELSS purely for long-term growth, not for 80C saving.

you are 45 or older and this money is earmarked for retirement in 10–12 years — consider a split: PPF for capital protection, ELSS for growth, rather than all-in on either.

you are comfortable with equity markets moving sharply in either direction — do not put emergency funds, short-term savings, or money you cannot afford to watch drop by 30% into ELSS, regardless of the return potential.

Your tax regime choice is the upstream decision that determines whether PPF or ELSS even gives you an 80C benefit. Before committing, read through our old vs new tax regime comparison to confirm which regime actually suits your income structure.

Common Mistakes to Avoid

Investing in ELSS purely because returns look higher on paper

Comparison articles often show ELSS delivering 12–14% vs PPF’s 7.1%, leading investors to pile into ELSS without considering risk. A 30% market fall — which has happened in India in 2008, 2020, and 2022 — can leave your ELSS portfolio worth less than your total investment in the first 3–5 years.

Do not choose ELSS solely based on projected return figures. Assess your genuine risk tolerance before allocating.

Assuming ELSS is tax-free because it qualifies under 80C

Many investors confuse the entry tax benefit (80C deduction) with the exit tax treatment. ELSS gains above ₹1.25 lakh per year are taxed at 12.5% as LTCG. Over 15 years, this can reduce your post-tax corpus by ₹4–6 lakh on a ₹1.5 lakh/year investment. PPF’s EEE status means no such haircut on exit.

Always account for LTCG when comparing ELSS maturity values to PPF’s tax-free corpus.

Treating PPF’s 15-year lock-in as flexible because partial withdrawal exists

Partial withdrawals from PPF are available from the 7th financial year, but they are capped: you can withdraw up to 50% of the balance at the end of the 4th year preceding the withdrawal year, or 50% of the balance at the end of the preceding year — whichever is lower. This is not freely accessible money. Do not treat PPF as a liquid emergency fund.

Keep a separate liquid emergency fund outside PPF and ELSS entirely.

Stopping PPF contributions midway because rates feel low

The power of PPF comes from 15-year compounding at a tax-free rate. If you stop contributing in Year 6 because the 7.1% rate feels unattractive, you lose the compounding benefit on the remaining 9 years. Worse, you can be charged a ₹50 penalty per year for not maintaining the ₹500 minimum annual contribution on a dormant PPF account.

If you start a PPF account, plan to maintain it for the full tenure.

Investing a lump sum in ELSS in March purely to save tax

Lump-sum ELSS investments made in March — when most salaried employees rush to claim 80C — expose you to sequence-of-returns risk. If the market corrects immediately after your investment, you are locked in at a high price for 3 years. A monthly SIP across 12 months smooths out this entry risk through rupee cost averaging.

Start your ELSS SIP in April, not March.

Ignoring which tax regime you are in before deciding

If you have opted for the new tax regime and still invest in ELSS expecting an 80C deduction, you are making a mistake that cannot be reversed mid-year. The new regime does not allow Section 80C deductions. Your ₹1.5 lakh ELSS investment will not reduce your taxable income at all.

Confirm your tax regime for the financial year before making any 80C investment.

Not reviewing ELSS fund performance before auto-renewing SIPs

ELSS funds are not interchangeable. A fund that topped the charts in 2018 may be a consistent underperformer by 2024. Auto-renewed SIPs in poor-performing funds quietly erode wealth over the years. Review your ELSS fund’s 5-year and 10-year rolling return against its benchmark annually.

If your fund has underperformed its benchmark for 3 or more consecutive years, evaluate a switch.

When This May Not Be the Right Choice

ELSS may not be right for you if your investment horizon is under 5 years, even though the technical lock-in is 3 years. Equity markets can stay depressed for 3–4 years — you could end up redeeming at a loss or a low gain. If your goal is within 5 years, debt instruments or PPF are safer options.

PPF may not be right as your primary wealth-building vehicle if you are under 35 with a stable income and a 15+ year horizon. At 7.1% pre-inflation, PPF barely keeps pace with India’s long-term inflation in real terms. Relying on PPF alone to build retirement wealth means your purchasing power grows slowly.

Neither PPF nor ELSS makes sense as your first financial priority if you carry high-interest debt — personal loans, credit card outstanding, or education loans above 10% interest. Paying off ₹5 lakh at 14% interest saves you more than PPF earns at 7.1%.

ELSS via lump sum is not right if you cannot predict your cash flow — irregular income, a business with seasonal revenue, or a job transition. A SIP structure is safer for those who cannot commit to annual lump sums without financial stress.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

PPF interest rates, annual investment limits, and withdrawal rules are set by the Government of India and can change with each Budget or quarterly notification. ELSS taxation — including LTCG rates, the annual exemption threshold, and fund-level SEBI regulations — is governed separately and is subject to revision in each Union Budget.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department (Section 80C rules, LTCG rates) — incometax.gov.in

- SEBI (ELSS fund regulations, mutual fund guidelines) — sebi.gov.in

- EPFO (EPF contribution and PPF context) — epfindia.gov.in

- India Post / National Savings Institute (PPF account rules) — indiapost.gov.in

Expert Tips

- Start your ELSS SIP in April, not March. Spreading 12 monthly instalments across the full financial year smooths your entry price and eliminates the last-minute lump-sum risk. A ₹12,500/month SIP achieves the full ₹1.5 lakh 80C ceiling with none of the timing stress.

- If you are 30–40 years old, have your EPF running, and want to add one more fixed-income layer, ₹50,000/year in PPF alongside ₹1 lakh/year in ELSS is a balanced structure — not an all-or-nothing call.

- Check whether your employer’s EPF contribution is already consuming most of your ₹1.5 lakh 80C limit. Many salaried employees earning above ₹12 lakh find that EPF alone uses ₹60,000–₹75,000 of the limit, leaving far less room than they assumed for PPF or ELSS.

- If you have a PPF account from your 20s with 8–10 years already run, do not abandon it. Extend it in 5-year blocks after Year 15 — you can continue contributing with the same EEE benefit and no fresh lock-in of the original tenure.

- Choose a direct ELSS plan, not a regular plan. Regular plans pay distributor commissions embedded in a higher expense ratio — typically 0.5–1% more per year than the direct plan of the same fund. Over 15 years, this 1% difference compounds into a meaningfully lower corpus on the same investment.

- Do not redeem ELSS units the moment the 3-year lock-in expires if you have no near-term goal. Unnecessary redemptions trigger LTCG tax and break your compounding. Stay invested if your goal is still 5+ years away.

- If you are close to the ₹1.25 lakh LTCG exemption threshold in a financial year, stagger your ELSS redemptions across two financial years where possible — redeem partly in March and partly in April — to use the annual exemption in both years and reduce your tax outflow.

Frequently Asked Questions

Can I invest in both PPF and ELSS in the same year?

Yes. You can invest in both PPF and ELSS within the same financial year. The combined deduction under Section 80C is capped at ₹1.5 lakh per year across all eligible instruments. If your PPF investment is ₹50,000 and ELSS is ₹1 lakh, your total 80C deduction is ₹1.5 lakh — provided you are in the old tax regime.

Is PPF interest taxable under any circumstances?

No. PPF interest is fully exempt from income tax under Section 10(11) of the Income Tax Act. This applies regardless of the amount — even if your PPF account earns ₹3–4 lakh in interest in a single year, it is not included in your taxable income. This is a statutory exemption, not a deduction.

What happens to my ELSS investment after the 3-year lock-in expires?

After the 3-year lock-in, your ELSS units become fully redeemable at any time. There is no obligation to redeem. Most advisors recommend staying invested beyond 3 years if your financial goal is still some years away — the compounding benefit of equity mutual funds typically shows up more meaningfully after 7–10 years than at the 3-year mark.

Is ELSS safe for someone investing in equity for the first time?

ELSS is equity — it is subject to market volatility. In a bad year, the value of your investment can fall 25–30%. It is not suitable as a substitute for a savings account or emergency fund. For a first-time equity investor, starting with a ₹500/month SIP in a diversified large-cap ELSS fund is a reasonable entry point — but understanding that short-term losses are part of the process is non-negotiable.

Can I invest more than ₹1.5 lakh in ELSS?

Yes. You can invest any amount in an ELSS fund. However, only ₹1.5 lakh per year qualifies for the Section 80C deduction. Any amount above ₹1.5 lakh does not give you an additional tax benefit under 80C, but the investment itself continues to grow — and all gains above ₹1.25 lakh at redemption are taxed at 12.5% as LTCG, regardless of whether the investment was within or beyond the 80C limit.

What is the LTCG exemption for ELSS, and how does it work?

Long-term capital gains on equity mutual funds — including ELSS — are exempt up to ₹1.25 lakh per financial year. Gains above this threshold are taxed at 12.5%. For example, if you redeem ₹5 lakh in ELSS units in a year with ₹2.5 lakh in gains, your taxable LTCG is ₹1.25 lakh (₹2.5L minus ₹1.25L exemption). Your tax is 12.5% × ₹1.25 lakh = ₹15,625.

Can I withdraw money from PPF before 15 years?

Partial withdrawals from PPF are allowed from the 7th financial year — not before. The maximum partial withdrawal is 50% of the balance at the end of the 4th year preceding the year of withdrawal, or 50% of the balance at the end of the preceding year, whichever is lower. Only one partial withdrawal is permitted per financial year. Full premature closure before 15 years is allowed only in very specific circumstances such as life-threatening illness or higher education, and typically comes with a 1% interest rate reduction.

Does ELSS qualify for deduction under the new tax regime?

No. Under the new tax regime, Section 80C deductions — including those for ELSS — are not available. If you file your income tax return under the new regime, your ELSS investment does not reduce your taxable income. ELSS still works as a wealth-creation instrument under the new regime, but it no longer serves a tax-saving purpose in the traditional sense.

Which is better for a 10-year retirement goal — PPF or ELSS?

For a 10-year horizon, ELSS has historically delivered better inflation-adjusted growth than PPF, assuming a diversified, well-managed fund. At 12% CAGR, ₹1.5 lakh/year over 10 years grows to approximately ₹28.5 lakh before LTCG tax. PPF at 7.1% over the same period delivers approximately ₹21.8 lakh tax-free. However, PPF’s tax-free status and guaranteed principal mean the gap narrows after accounting for LTCG on ELSS gains. A split between the two reduces risk without giving up all growth potential.

Is there a minimum number of ELSS funds I should hold?

One well-chosen ELSS fund is sufficient for your 80C ELSS allocation. Holding three or four ELSS funds does not meaningfully reduce risk — they all invest in Indian equities and tend to be correlated. Multiple funds add complexity without proportional diversification. Pick one fund with a consistent 10-year track record, a reasonable expense ratio in the direct plan, and a stable fund manager, and stay with it.

Final Verdict

PPF vs ELSS is not a straight winner-takes-all comparison. PPF is the better choice if your primary goal is a guaranteed, tax-free corpus with zero principal risk — particularly if you are in the old tax regime and want a long-term savings anchor to sit alongside equity exposure elsewhere. ELSS is the better choice if you have a 10+ year horizon, are comfortable with equity market swings, and want the shortest possible 80C lock-in with higher growth potential. For most salaried investors in their 30s with stable income, a combination — PPF as your fixed-income 80C layer, ELSS as your equity growth layer — serves both goals without forcing a binary call. Confirm your tax regime before allocating to either. For those already using NPS, PPF, and EPF together, the right ELSS allocation will depend on how much equity exposure you already carry. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Suresh Nair writes about Indian government savings schemes, post office schemes, and conservative long-term savings options. His content is especially useful for families, parents, senior citizens, and low-risk savers who want to understand scheme rules before depositing money.

He covers topics such as Public Provident Fund, Sukanya Samriddhi Yojana, Senior Citizens’ Savings Scheme, National Savings Certificate, Kisan Vikas Patra, Post Office Monthly Income Scheme, National Pension System, post office fixed deposits, post office recurring deposits, child savings schemes, senior citizen savings options, maturity rules, withdrawal rules, lock-in periods, and tax treatment.

Suresh’s writing is mature, rule-focused, and cautious. He explains eligibility, deposit limits, tenure, interest calculation, tax benefits, withdrawal conditions, and practical use cases in simple language. His articles are useful for readers who prefer safety and predictable rules over high-risk investments. Since government scheme interest rates, deposit limits, lock-in rules, and tax treatment may change through official notifications, readers should verify current details from India Post, PFRDA, Income Tax Department, or relevant government sources before investing.