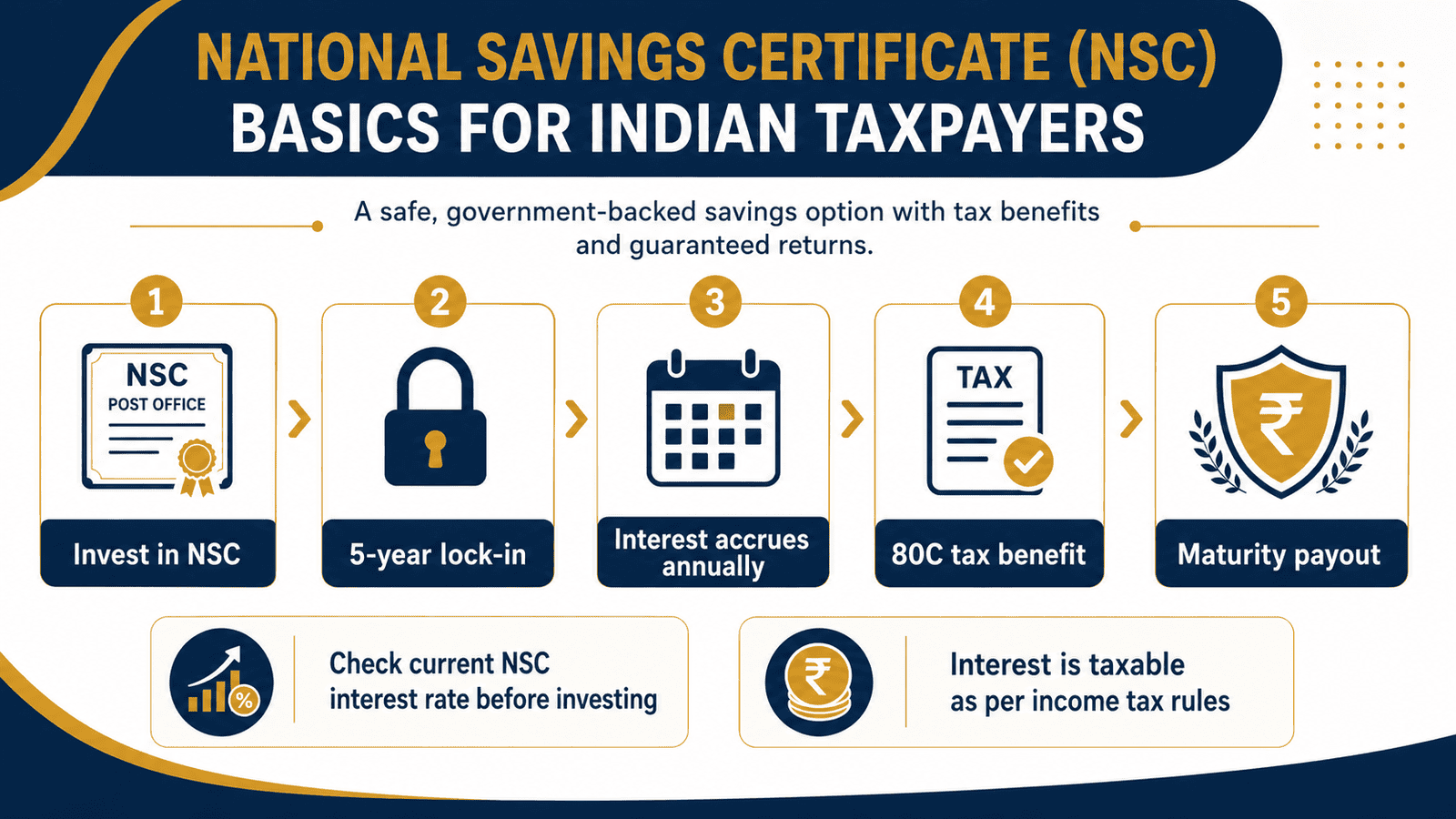

If you’ve ever searched “NSC interest rate” and ended up more confused than when you started — you’re not alone. The National Savings Certificate is one of India’s most misunderstood small savings products. The interest looks simple. The lock-in seems clear. But the tax treatment? That’s where most salaried investors — including those who file their own ITR — get it completely wrong. This article separates the four things you actually need to know before investing: how the interest works, what the 5-year lock-in means in practice, exactly when the 80C deduction applies, and when the accrued interest becomes taxable. NSC is not the same as PPF, FD, or ELSS — and the difference matters. Rates and tax rules can change with each Budget or quarterly government notification, so verify current figures from official sources before committing.

Quick Answer: National Savings Certificate

National Savings Certificate is a government-backed small savings scheme with a fixed lock-in period of 5 years. It offers interest set by the government, allows 80C deduction up to the eligible limit, and the accrued interest is generally taxable under income tax rules.

Key Takeaways

- NSC is a fixed-income government small savings scheme available through post offices — not a market-linked product. Your principal is not exposed to equity risk.

- The lock-in is 5 years with no ordinary premature exit. Never invest money you might need before maturity.

- The principal qualifies for Section 80C deduction up to ₹1.5 lakh per year — but only if you use the old tax regime. Under the new regime, no 80C benefit applies.

- Interest is compounded annually but paid only at maturity — no annual payouts. Your cash flow is entirely locked for the full 5-year term.

- Accrued interest in years 1–4 is deemed reinvested under the IT Act and qualifies for 80C deduction in those respective years, effectively offsetting the tax. Year-5 interest has no such offset and is fully taxable as Income from Other Sources.

- NSC interest is not subject to TDS — but this does not mean it is tax-free. You must self-declare the accrued interest in your ITR every year.

Key Facts at a Glance

| Feature | NSC Rule | Important Note |

|---|---|---|

| Product Type | Government-backed small savings scheme | Available at post offices and select authorised banks |

| Lock-in Period | 5 years | No voluntary early exit; exceptions only on death, court order, or pledgee forfeiture |

| Interest Rate | 7.7% p.a. | Revised quarterly by government; rate is locked on your purchase date |

| Interest Compounding | Annually, paid at maturity | No annual payout — full accumulated amount received at the end of year 5 |

| Section 80C Deduction | Up to ₹1.5 lakh per year | Available under old tax regime only; not applicable under new regime |

| TDS on Interest | No TDS deducted | Interest must be self-declared in ITR every year under Income from Other Sources |

| Minimum Investment | ₹1,000 | No upper limit on investment amount; 80C cap applies to deduction only |

How National Savings Certificate Works

What NSC Is — and Where It Fits Among Small Savings Schemes

National Savings Certificate (NSC) is part of India’s National Small Savings Schemes, managed under the Ministry of Finance. It sits alongside PPF, Senior Citizens Savings Scheme, and Sukanya Samriddhi Yojana in the post office small savings umbrella. Unlike PPF — which has a 15-year tenure and fully tax-free interest — NSC is a 5-year fixed-income product where the interest is taxable but partially offset through Section 80C of the Income Tax Act, according to Income Tax Department guidelines.

NSC is not equity, not market-linked, and not a mutual fund. The interest rate is fixed on the date you purchase — it does not change if the government revises the rate in a later quarter. You know exactly what your maturity amount will be the day you invest. That certainty is both the appeal and the constraint.

Buying NSC: How the Process Works

NSC can be purchased at any post office or through the Department of Posts (DOP) online platform linked to India Post Payments Bank. The minimum purchase is ₹1,000, with no upper ceiling on the investment amount. However, only up to ₹1.5 lakh per year qualifies for Section 80C deduction — amounts beyond that are invested without a tax deduction benefit.

New NSC purchases are now issued in electronic form (e-NSC), stored in your DOP account. Physical certificates issued before the switchover remain valid and can still be encashed at maturity. You can hold multiple certificates with different purchase dates, building a staggered maturity ladder if that suits your cash-flow planning.

How the Interest Accrues and How Maturity Works

NSC uses annual compounding. Interest is calculated on the outstanding principal at the end of each year and added to the balance — but it is never paid out during the 5-year term. You receive the entire maturity amount — original principal plus five years of compounded interest — in one lump sum at the end of year 5.

This matters practically. If you invest ₹1 lakh in NSC, you will not see a single rupee of return for 5 years. There are no monthly, quarterly, or annual interest credits to your bank account. If you are comparing NSC to an FD that offers monthly interest payouts, you are comparing two structurally different cash-flow products — not just two interest rates.

Section 80C: How the Deduction Actually Works Year by Year

This is the most misunderstood part of NSC. Most investors know the principal is deductible — but few understand what happens in years 2 through 5. Here is how Section 80C applies across the entire NSC tenure:

Year 1: You invest ₹50,000. The full principal — ₹50,000 — qualifies for Section 80C deduction, subject to the overall ₹1.5 lakh cap across all 80C investments in that year.

Years 2 to 4: The interest accrued each year is “deemed to have been reinvested” under the Income Tax Act. This means the accrued interest is simultaneously taxable as Income from Other Sources and deductible as a Section 80C investment in that same year. The two effects largely cancel each other out for most taxpayers under the old regime — your effective tax on years 2–4 NSC interest is approximately zero.

Year 5: The accrued interest of the final year is not deemed reinvested. There is no corresponding 80C deduction. This year’s interest is fully taxable as Income from Other Sources — and you receive it as part of the lump sum at maturity without any offsetting deduction.

To understand how NSC compares with the full range of instruments competing for your 80C limit, see our complete 80C deduction options guide.

What Changes Under the New Tax Regime

If you opt for the new tax regime, Section 80C does not apply at all. The principal investment in NSC gives you no deduction. The accrued interest each year is taxable as Income from Other Sources without any offsetting 80C deduction. Over 5 years, all the interest you earn is fully taxed at your applicable slab rate — no netting, no offset.

This fundamentally changes the NSC return calculation. A 7.7% pre-tax yield for a 30% bracket taxpayer under the new regime becomes approximately 5.3% post-tax — comparable to or lower than some bank FD options. Always calculate your post-tax yield at your actual bracket before treating the headline rate as the real return.

Who Typically Considers NSC

NSC is most commonly considered by salaried taxpayers under the old regime who have unused 80C space after EPF and LIC, conservative investors who want government-backed fixed income without equity risk, and families saving toward a specific 5-year goal like a child’s education or a home purchase down-payment. It is generally not used by investors who need liquidity, want market-linked growth, or have already switched to the new tax regime.

Real Example: Rahul in Pune Evaluates NSC

Rahul, 34, is an IT professional in Pune earning ₹14 lakh per year. He files under the old tax regime. His 80C basket for the year already has ₹90,000 from EPF and ₹30,000 from a LIC premium — leaving ₹30,000 of unused 80C space. He decides to invest ₹30,000 in NSC.

In Year 1, Rahul claims ₹30,000 as a Section 80C deduction. At his effective 30% bracket, this saves approximately ₹9,270 in tax (₹30,000 × 30.9% including cess).

In Years 2–4, the accrued interest on his ₹30,000 is reported as Income from Other Sources and simultaneously claimed as an 80C deduction — the two offset each other, net tax impact close to zero.

In Year 5, the final year’s accrued interest — approximately ₹3,100 — is fully taxable. At 30%, Rahul pays around ₹957 in tax on this amount. His total 5-year gain from the ₹30,000 investment, after accounting for this tax, remains solidly positive.

But Rahul’s actual benefit depends on which regime he files in each of those 5 years. He uses our tax calculator comparison to model whether remaining on the old regime through maturity is the right call for his salary structure.

How to Calculate NSC Maturity Amount

NSC compounds annually. The formula is straightforward:

Maturity Amount = P × (1 + r)^n

Where P = principal invested, r = annual interest rate as a decimal, n = 5 years. Using ₹10,000 at 7.7% (illustrative — verify the current government-notified rate before investing):

| Year | Opening Balance | Interest Accrued |

|---|---|---|

| Year 1 | ₹10,000 | ₹770 |

| Year 2 | ₹10,770 | ₹829 |

| Year 3 | ₹11,599 | ₹893 |

| Year 4 | ₹12,492 | ₹962 |

| Year 5 | ₹13,454 | ₹1,036 |

Maturity value: approximately ₹14,490. Total interest earned: ₹4,490. Under the old regime, years 1–4 interest (₹3,454) is offset by 80C deductions across those ITR years. Only the year-5 interest of ₹1,036 is the net taxable amount at maturity. Under the new regime, the full ₹4,490 is taxable, spread across 5 ITR years as self-declared income.

For a deeper understanding of how fixed-income maturity calculations work across different products, see our guide on FD interest calculation.

Comparison: NSC vs PPF and FD

NSC vs PPF

| Feature | NSC | PPF |

|---|---|---|

| Lock-in | 5 years | 15 years |

| Interest taxation | Taxable (partially offset via 80C in years 1–4 under old regime) | Fully tax-free |

| 80C on principal | Yes | Yes |

| Partial withdrawal | Not allowed ordinarily | Permitted after year 7 |

| Interest rate structure | Locked on purchase date | Revised quarterly, applies to full balance |

| Best suited for | 5-year fixed goals, 80C top-up | Long-term tax-free corpus building |

If fully tax-free long-term accumulation is your goal, understand the PPF account basics before making the NSC vs PPF decision.

NSC vs Bank Fixed Deposit

| Feature | NSC | Bank FD |

|---|---|---|

| Backed by | Government of India | DICGC deposit insurance up to ₹5 lakh |

| 80C deduction | Yes (old regime) | 5-year tax-saving FD only |

| TDS on interest | No TDS | TDS applicable above threshold |

| Premature exit | Generally not permitted | Permitted with interest penalty |

| Interest payout | At maturity only | Monthly, quarterly, or at maturity (flexible) |

| Tenure options | 5 years (fixed) | 7 days to 10 years (flexible) |

For a side-by-side look at government savings deposits versus bank deposits including interest rate differences and safety aspects, see our post office FD comparison guide.

How to Decide What’s Right for You

You file under the old tax regime, have unused 80C capacity after EPF and LIC, and are confident you will not need the money for 5 years — NSC may be a practical, low-effort way to top up your tax-saving plan with a government-backed return.

You earn below ₹7 lakh and opt for the new tax regime — the 80C benefit of NSC does not apply, and the locked-in taxable return may not justify the illiquidity compared to a short-term FD or liquid fund.

You want a fully tax-free long-term corpus and can stay invested for 15 years — PPF is more tax-efficient than NSC, even accounting for the shorter NSC lock-in.

You are investing for a specific known expense in 5 years — a child’s school fees, a vehicle purchase, or a home renovation — NSC’s fixed return with no market volatility aligns well with this type of goal.

You need regular income from your investment during the year — NSC is unsuitable. Choose an FD with monthly or quarterly interest payouts instead, and compare the post-tax yields using a post office FD comparison.

You are not confident you can hold the investment for the full 5-year term without needing the principal — do not invest in NSC. Premature encashment is generally not permitted, and financial pressure before maturity will leave you with no exit options in normal circumstances.

Your 80C basket is already at ₹1.5 lakh from EPF, home loan principal, and ELSS — NSC adds no further principal deduction. In that case, evaluate whether the locked-in post-tax return at your bracket justifies the 5-year illiquidity against other options.

Common Mistakes to Avoid

Assuming 80C Deduction Means NSC Returns Are Tax-Free

The Section 80C deduction applies to the principal invested — not to the returns. NSC interest is taxable every year, unlike PPF where the interest itself is fully exempt under current rules.

Many investors discover at maturity that they owe tax on year-5 interest — sometimes ₹8,000–₹25,000 in additional tax on a ₹1–3 lakh investment — because they never planned for it during the 5 years.

Calculate the post-tax effective yield before investing. Compare it honestly against alternatives at your tax slab.

Not Reporting Accrued NSC Interest in ITR Every Year

NSC interest accrues annually and must be declared under “Income from Other Sources” in your ITR every year — not only in the year of maturity. You do not receive any cash during the 5 years, but the accrual is a taxable event regardless.

Skipping annual declaration means your ITR understates income for multiple years. When the full maturity amount arrives, the accumulated interest may trigger a scrutiny notice if it appears as unexplained income in one year.

Report the accrued amount each year and simultaneously claim the Section 80C deduction for years 1–4 to offset it.

Investing Money That Might Be Needed Before 5 Years

NSC cannot be liquidated early under ordinary circumstances. Investing funds earmarked for medical emergencies, job-loss contingencies, or unplanned large expenses creates a situation where the money is completely inaccessible at the worst possible moment.

Build 3–6 months of expenses in a liquid instrument before investing anything in NSC. Illiquidity is not a minor inconvenience — it is a structural constraint of the product.

Comparing NSC Rate Against FD Rate Without Accounting for Tax

If NSC offers 7.7% and a bank FD offers 7.5%, the comparison seems easy — NSC wins. But both products have taxable interest. Under the new regime, both are taxed at your slab rate, and the difference shrinks to a few basis points. Under the old regime, NSC’s 80C benefit on years 1–4 interest genuinely adds value — but only if you have unused 80C space.

Always compare post-tax effective yields at your actual bracket, not headline rates.

Not Verifying Whether 80C Limit Is Already Exhausted

If your EPF contributions, LIC premium, home loan principal, and existing ELSS investments already total ₹1.5 lakh or more, NSC adds zero further deduction on the principal. The benefit shrinks to the narrower years 2–4 accrued interest offset — which is meaningful but not the headline advantage most investors expect.

Calculate your total 80C utilisation for the year before purchasing NSC.

Not Confirming the Current NSC Rate Before Purchasing

The government revises small savings scheme rates quarterly. The rate applicable to your NSC is the rate on the date of purchase — not the rate you read about in an article from a previous quarter. Buying without confirming the current notified rate means you may be locked in at a rate different from your assumption — for 5 full years.

Always confirm the current rate at the official post office or government notification source before purchasing.

When This May Not Be the Right Choice

NSC may not be appropriate if you need access to your money before 5 years. The lock-in is strict — premature encashment is only permitted in specific exceptional circumstances such as the holder’s death, a court order, or forfeiture by a pledgee when the certificate has been pledged as collateral. There is no voluntary early exit option for personal financial needs.

If you have already opted for the new tax regime, the Section 80C benefit that anchors the NSC value proposition does not apply. All interest becomes taxable without any offsetting deduction, which changes the effective yield calculation significantly.

If you are seeking market-linked growth or want to meaningfully beat inflation over time, NSC’s fixed return structure will not meet this goal — equity-oriented products or market-linked instruments may be more suitable depending on your risk profile.

If your priority is fully tax-free interest, PPF or — for eligible investors — Sukanya Samriddhi Yojana may be worth exploring under current rules before committing to NSC.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

NSC interest rates, Section 80C limits, lock-in rules, and tax treatment are all subject to change with each Budget or quarterly government notification. Do not rely on any article — including this one — as the final word on current figures. Verify from these official sources before purchasing:

- Income Tax Department — incometax.gov.in (for Section 80C deduction eligibility, annual accrued interest treatment, and ITR reporting requirements)

- Reserve Bank of India — rbi.org.in (for small savings scheme notifications and related regulatory circulars)

- Department of Posts — indiapost.gov.in (for current NSC interest rate, e-NSC purchase process, and maturity redemption rules)

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

To understand how taxable NSC interest accrual affects your total taxable income and ITR reporting, see our guide on taxable income calculation.

Expert Tips

- If you are in the 30% bracket under the old regime with unused 80C space, every ₹10,000 invested in NSC saves approximately ₹3,090 in tax in year 1 alone — that is a guaranteed immediate return before a single day of compounding begins. Factor this into your yield comparison.

- NSC can be pledged as collateral for a loan at many banks and NBFCs. This adds a thin layer of liquidity in genuine emergencies — you can borrow against the certificate without breaking it. Confirm the terms with your specific bank before assuming this option is available.

- Report accrued NSC interest in your ITR every year — not just in the year of maturity. Bunching five years of interest into one ITR is technically incorrect reporting and may attract scrutiny. The correct approach is to declare year-1 interest in year-1 ITR, year-2 in year-2, and so on.

- Keep your e-NSC purchase receipt, passbook entry, or DOP account confirmation stored safely. If documentation is lost, you will need to go through a formal application process at the post office to claim maturity — which can be time-consuming.

- Before investing, confirm your total 80C utilisation for that financial year. If EPF alone exceeds ₹1.5 lakh, NSC gives no additional deduction on the principal — re-evaluate whether the locked-in post-tax return justifies the 5-year commitment.

- Match NSC to a specific, named 5-year goal — a child’s Class 9 fee corpus, a vehicle replacement fund, or a home renovation budget. Goal-tagging your certificate reduces the temptation to try to break the investment when markets look attractive or short-term needs arise.

Frequently Asked Questions

Is NSC interest taxable in India?

Yes, NSC interest is taxable. Each year’s accrued interest is treated as Income from Other Sources under the Income Tax Act, even though you do not receive any cash during the 5-year term. Under the old tax regime, the interest for years 1–4 is deemed reinvested and qualifies for a Section 80C deduction in those years, effectively offsetting the tax for most taxpayers. Year-5 interest has no such offset and is fully taxable when you receive the maturity amount. Under the new tax regime, all five years of interest are taxable without any Section 80C offset.

Is NSC eligible for Section 80C deduction?

Yes, the principal invested in NSC qualifies for Section 80C deduction up to the overall annual limit, which applies only under the old tax regime. The accrued interest for years 1–4 also qualifies as an 80C deduction in those respective years, as it is treated as reinvested under the IT Act. If you have switched to the new tax regime, the 80C deduction does not apply — neither for the principal nor for the accrued interest. Verify the current 80C limit at incometax.gov.in before relying on this for planning.

What is the NSC lock-in period?

The NSC lock-in is 5 years. You cannot voluntarily withdraw your investment before maturity. Early encashment is only permitted in specific circumstances: the death of the certificate holder, a court or tribunal order, or forfeiture by a pledgee when the certificate has been used as collateral for a loan. There is no provision for voluntary premature redemption for personal financial needs. Verify current rules at indiapost.gov.in before investing.

Is NSC better than PPF?

It depends on your goal and tax situation. NSC has a shorter lock-in (5 years vs 15 years for PPF), but NSC interest is taxable while PPF interest is fully tax-free under current rules. If you want a long-term tax-free corpus and can stay invested for 15 years, PPF is generally more tax-efficient over the full tenure. If you have a specific 5-year goal, prefer government-backed certainty, and have unused 80C space, NSC may complement your plan. Neither is universally better — the right answer depends on your time horizon, tax regime, and liquidity needs.

Can NSC be withdrawn before maturity?

Generally no. NSC does not permit voluntary premature withdrawal for personal reasons. The exceptions are the holder’s death, a court order, and forfeiture by a pledgee when the certificate is held as loan collateral. There is no penalty-based early exit option as with bank FDs. If there is any possibility you will need the funds before 5 years, NSC is not the appropriate product for that money.

Is there TDS on NSC interest?

No, TDS is not deducted on NSC interest. However, “no TDS” does not mean “no tax.” It means the tax responsibility rests entirely with you to self-declare the accrued interest each year in your ITR under Income from Other Sources. Many investors misread no-TDS as tax-exempt, which is incorrect — the tax obligation exists; only the automatic deduction mechanism does not.

What happens to my NSC deduction if I switch to the new tax regime?

If you switch to the new tax regime in any year after purchasing NSC, you cannot claim the 80C deduction for that year — neither for the principal (if still in year 1) nor for the accrued interest. The interest remains fully taxable with no offsetting deduction. If you plan to switch regimes during the NSC tenure, model the tax impact across all 5 years before purchasing, not just year 1.

Is the entire maturity amount of NSC taxable?

No — the taxation is spread across all 5 years, not applied to the full maturity amount in year 5. Under the old regime: year-1 principal was claimed as an 80C deduction; years 2–4 accrued interest was reported and offset by 80C each year; only year-5 interest is net taxable at maturity. Under the new regime, all five years of accrued interest are taxable, but each year’s amount should be declared in that year’s ITR — not consolidated into year 5.

Can I buy NSC for a minor child?

Yes, NSC can be purchased on behalf of a minor. The certificate is held in the child’s name with a parent or guardian as the guardian for the account. The investment and any 80C deduction would be claimed by the parent or guardian making the investment under the applicable rules. Verify the current documentation and account-type requirements for minor investors at your local post office or indiapost.gov.in.

Final Verdict

National Savings Certificate is a credible, low-risk option for conservative salaried taxpayers under the old regime who want fixed-income certainty, a moderate government-backed return, and a practical 80C top-up for unused deduction space. It is not the right choice for investors who need liquidity within 5 years, expect fully tax-free returns, or have already moved to the new tax regime. The headline interest rate matters — but the tax treatment matters equally. A salaried professional comparing NSC against FD, PPF, or ELSS should always run a post-tax comparison at their actual income bracket before deciding. Verify the current NSC interest rate, 80C limits, and accrued interest rules before committing. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Suresh Nair writes about Indian government savings schemes, post office schemes, and conservative long-term savings options. His content is especially useful for families, parents, senior citizens, and low-risk savers who want to understand scheme rules before depositing money.

He covers topics such as Public Provident Fund, Sukanya Samriddhi Yojana, Senior Citizens’ Savings Scheme, National Savings Certificate, Kisan Vikas Patra, Post Office Monthly Income Scheme, National Pension System, post office fixed deposits, post office recurring deposits, child savings schemes, senior citizen savings options, maturity rules, withdrawal rules, lock-in periods, and tax treatment.

Suresh’s writing is mature, rule-focused, and cautious. He explains eligibility, deposit limits, tenure, interest calculation, tax benefits, withdrawal conditions, and practical use cases in simple language. His articles are useful for readers who prefer safety and predictable rules over high-risk investments. Since government scheme interest rates, deposit limits, lock-in rules, and tax treatment may change through official notifications, readers should verify current details from India Post, PFRDA, Income Tax Department, or relevant government sources before investing.