Your health insurance premium has just climbed 20% at renewal — or the hospital your family trusts has been quietly delisted from the cashless panel. Switching insurers seems like the obvious move, except you’ve spent three or four years building up a pre-existing disease waiting period credit. Walk away from that, and you’re starting from zero with the next insurer.

Health insurance portability rules exist for exactly this situation. Under IRDAI guidelines, you can move to a different insurer at renewal and carry forward eligible continuity benefits. But porting is not the same as buying a fresh policy — and it does not mean the new insurer copies every term of your old one. Premiums, sub-limits, room rent caps, and network hospitals can all change even when waiting period credit is preserved.

This article explains what transfers when you port, what can change, how to time your application correctly, and which mistakes can cost you years of built-up continuity.

Quick Answer: Health Insurance Portability Rules

Health insurance portability rules allow you to switch insurers at renewal while carrying forward eligible waiting period credit, but not every benefit or term stays unchanged. Apply at least 45 days before renewal, compare exclusions and premium carefully, and wait for written approval before cancelling your old policy.

Key Takeaways

- Portability is only available at renewal — IRDAI health insurance portability rules do not permit mid-term switches under any circumstance.

- Apply to the new insurer at least 45 days before your renewal date; a late application can cause your portability request to lapse for that renewal cycle entirely.

- Waiting period credit applies only to the sum insured you are porting — if you increase your cover, the additional amount may attract a fresh waiting period at the new insurer.

- No claim bonus treatment is not automatic; it varies by insurer and policy wording, so confirm it in writing before accepting a portability offer.

- Premium, room rent caps, disease-wise sub-limits, exclusions, and network hospitals can all change even when waiting period credit is preserved — compare policy documents, not just brochures.

- Never cancel your old policy until the new insurer confirms acceptance in writing; an unconfirmed port leaves you without active cover.

Key Facts at a Glance

| Rule | What it means | What to check |

|---|---|---|

| When you can port | Only at renewal — not mid-policy year | Your exact renewal date |

| Application deadline | At least 45 days before renewal date | Written acknowledgement from new insurer |

| Waiting period credit | Eligible continuity for pre-existing diseases carries forward | Applies to ported sum insured only — not any top-up amount |

| What can change | Premium, exclusions, room rent, sub-limits, network hospitals | Compare both policy documents line by line before accepting |

| Who approves the port | New insurer after medical underwriting | Get written approval before cancelling old policy |

| No claim bonus (NCB) | Not universally transferred — depends on insurer policy wording | Ask new insurer for written NCB treatment terms |

Understanding Health Insurance Portability Rules in India

What portability means — and what it does not

Health insurance portability rules were introduced by IRDAI to prevent policyholders from being trapped with underperforming insurers. Before these rules, switching effectively meant losing all waiting period credit — a powerful deterrent that kept people in poor-quality policies year after year. Portability changed that by allowing continuity benefits to follow the policyholder, not the insurer.

In practical terms, portability means you can move your individual or family floater health policy from one general or stand-alone health insurer to another at the time of renewal, and carry forward eligible waiting period credit. According to IRDAI guidelines, this applies to standard individual and family floater health insurance products. Group health insurance policies provided by employers follow entirely different rules — porting from a group policy to an individual plan is not covered by the same portability framework.

What portability does not do: it does not obligate the new insurer to replicate the terms of your old policy. Room rent limits, disease-wise sub-limits, restoration benefits, co-pay clauses, and exclusions are set by the new insurer based on its own product structure and underwriting guidelines. Before you compare policies, ensure you understand the core coverage differences at stake — our guide on basic health cover explains the key terms you need to compare.

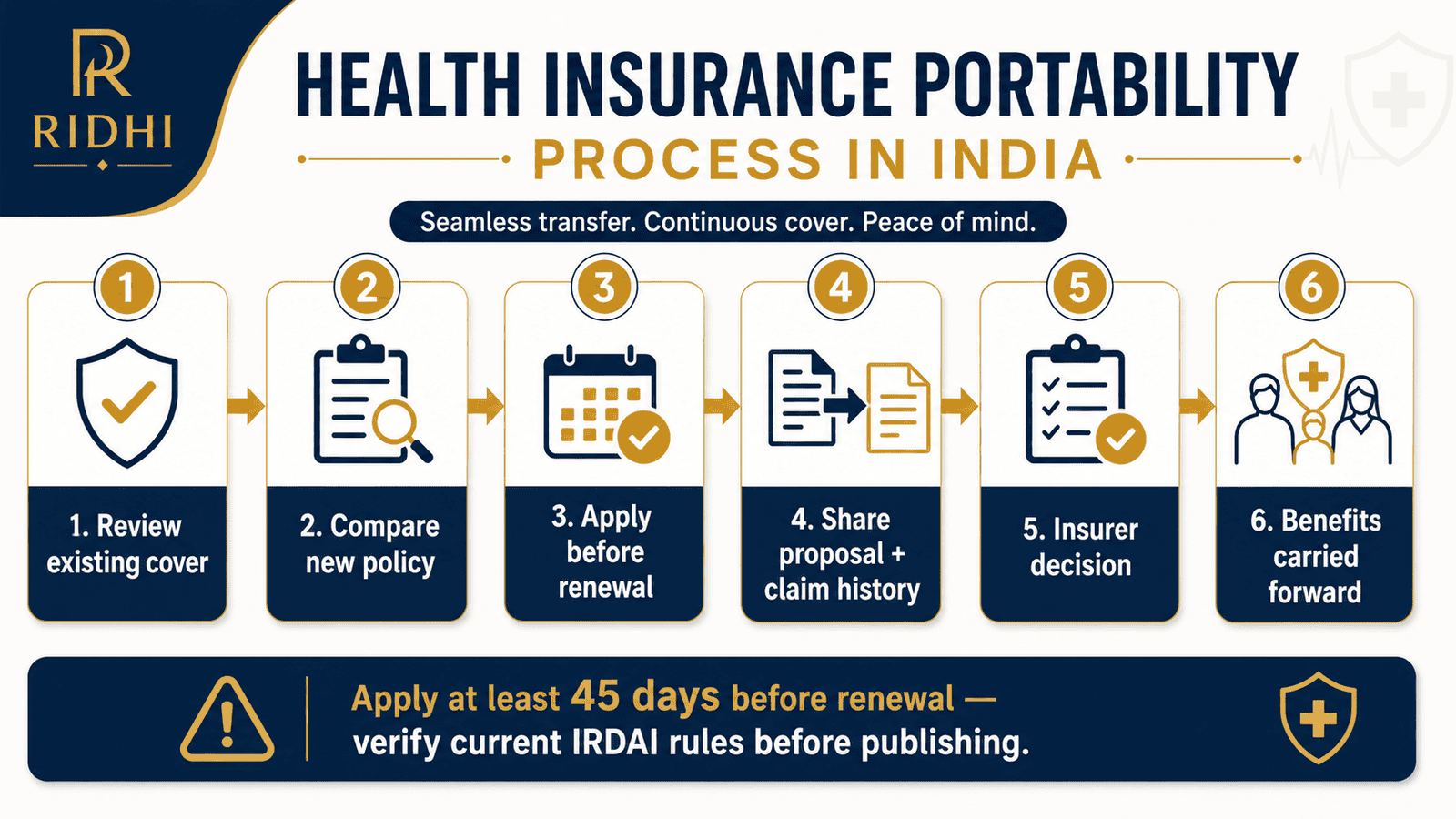

The renewal-only rule and the 45-day window

You can only port at renewal — not during the policy year. Once you decide to switch, you must submit your portability proposal form to the new insurer at least 45 days before your renewal date. This buffer gives the new insurer time to complete medical underwriting before your current policy expires.

If you apply with less lead time, the new insurer may not finish underwriting before your current policy lapses or auto-renews. In that case, your portability request fails for that renewal cycle, and you wait another full year. Timing is not an administrative detail — it is a hard deadline that determines whether your continuity benefits survive the switch.

Waiting period credit and how it works

The most valuable benefit of porting is waiting period credit. Health insurance policies carry several types of waiting periods: an initial waiting period of typically 30 days for most illnesses, and a longer pre-existing disease waiting period — often ranging from one to four years depending on the insurer and the condition declared at inception. When you port, the time already served with your old insurer carries forward.

There is one critical boundary: waiting period credit applies only to the sum insured you are carrying over. If your old policy was ₹5 lakh and you port to a ₹10 lakh policy, the continuity credit applies to ₹5 lakh. The additional ₹5 lakh may attract a fresh waiting period on the new insurer’s terms, particularly for any declared pre-existing conditions. This distinction is one of the most common misunderstandings in the porting process — and one that can cause real problems at claims time.

For a complete breakdown of how different types of waiting periods affect your actual claims, see our guide on waiting period impact.

No claim bonus — never assume, always confirm

If your policy accumulated a no claim bonus over claim-free years — typically as an increase in effective sum insured or a premium discount — do not assume it transfers automatically. IRDAI’s portability framework is clear on waiting period continuity but NCB treatment varies by insurer. Some insurers recognise and carry forward accumulated NCB; others do not. Ask the new insurer for written confirmation of how they will treat your existing NCB before you accept any portability terms.

Premium is not locked or protected

The new insurer sets your premium from scratch — based on your current age, medical history, city, sum insured, and claims record. Portability does not entitle you to the same premium your old insurer charged, or anything close to it. If you had a hospitalisation claim in the last policy year, expect the underwriting assessment to reflect it. The new premium may be lower, higher, or similar; the only accurate picture comes from a formal quote submitted with full medical and claims disclosure.

Real Example: Rohan’s Family Floater Port

Rohan Mehta, 38, is a senior software engineer in Bengaluru earning ₹28 lakh per year. He holds a ₹10 lakh family floater covering himself, his wife, and their young child. His wife has a thyroid condition that was declared at inception, four years ago. Under a standard four-year pre-existing disease waiting period, that condition waiting period is now complete.

At renewal, the premium is rising from ₹26,400 to ₹31,800 — a jump of ₹5,400. The hospital his family uses for consultations has also been delisted from the cashless panel. A competing insurer is offering a comparable ₹10 lakh family floater at ₹28,500 per year, with stronger hospital coverage in his part of Bengaluru.

If Rohan ports, his wife’s thyroid waiting period credit carries forward for the full ₹10 lakh — it will not reset. However, the new plan has a ₹3,500 per day room rent cap. His current policy has no room rent cap. In a city like Bengaluru, where semi-private room costs regularly run ₹7,000–₹10,000 per night, that cap creates proportionate deductions across all hospitalisation items — not just the room charge. The ₹3,300 annual saving may not compensate for that exposure. Rohan needs to model both scenarios before deciding.

For families weighing whether to port a combined floater or split into separate individual policies at the same time, our guide on family floater choice covers that trade-off in detail.

Comparison: What Transfers vs What Can Change After Porting

| Feature | Does it transfer? | What to check before accepting |

|---|---|---|

| Pre-existing disease waiting period credit | Yes — for ported sum insured | Fresh waiting period may apply to any increased sum insured amount |

| Initial waiting period credit | Generally yes | Confirm with the new insurer’s policy wording before accepting |

| No claim bonus (NCB) | Varies by insurer | Request written confirmation of NCB treatment from new insurer |

| Premium | No — fully reassessed | Get formal underwritten quote with complete health and claims disclosure |

| Room rent and sub-limits | No — new policy terms apply | Compare both policy documents specifically on room rent cap and disease-wise limits |

| Network hospitals | No — new insurer’s network | Verify preferred hospitals in your city are on the new cashless panel |

| Restoration benefit | No — product specific | Check whether new plan includes restoration and on what conditions |

How to Decide What’s Right for You

Your current insurer has raised premium significantly and the new insurer offers a comparable or better plan in terms of cover — compare cashless hospital access before committing; our guide on cashless hospital claims explains what to look for in a network before switching.

Your pre-existing disease waiting period has been fully served with your current insurer and the new insurer offers better room rent terms, lower sub-limits, or a restoration benefit — porting preserves your continuity credit while improving your policy quality.

You want to evaluate the new insurer’s claim-handling quality before porting — not just their premium — read our guide on insurer claim record to understand what to look for beyond the headline ratio.

You are mid-policy year and unhappy with your insurer — wait until renewal. Portability does not apply mid-term, and cancelling now means losing continuity credit and any unearned premium you have already paid.

You had a claim in the last 12 months — port only after comparing whether the new insurer’s underwriting accepts you at a reasonable premium without heavy loading or new exclusions, since recent claims will directly affect the assessment.

You have a recently diagnosed serious health condition, a hospitalisation in the last six months, or a complex pre-existing disease — porting may result in the new insurer declining your application, applying heavy premium loading, or adding new policy-level exclusions that did not exist before. Staying with your current insurer, which has already accepted your health history, may be the lower-risk outcome in these circumstances.

Common Mistakes to Avoid

Applying too close to the renewal date

The new insurer needs your application at least 45 days before your renewal date to complete medical underwriting in time.

Apply later than that and the new insurer may not finish the process before your current policy expires. Your old policy may auto-renew, the port lapses, and you wait another full year. This is the single most preventable mistake in the entire process.

Set a calendar reminder at least 60 days before renewal to start comparing, and aim to apply by day 50 at the latest.

Choosing only on premium

A ₹3,000 lower annual premium is attractive until you notice the new plan has a ₹3,000 per day room rent cap with proportionate deductions on all associated charges.

A single five-day hospitalisation in a semi-private room in a metro hospital can generate an out-of-pocket gap of ₹40,000–₹80,000 from room rent restrictions alone — far exceeding years of premium savings. Compare room rent caps, disease-wise sub-limits, co-pay clauses, and exclusions alongside premium.

Use premium as a tiebreaker between otherwise comparable plans, not as the primary filter.

Not disclosing claims or health conditions fully

Portability applications require complete disclosure of claim history and all diagnosed health conditions.

Incomplete disclosure is non-disclosure — and it is grounds for claim rejection when you need the policy most. The new insurer’s underwriting must be based on accurate, complete information to be valid. Declare everything, even if it results in loading or a specific exclusion.

A policy issued with full knowledge of your health history will stand up at claims time. One issued on incomplete information carries real risk.

Assuming all benefits transfer automatically

NCB, restoration benefits, wellness add-ons, and specific riders do not automatically port under IRDAI health insurance portability rules.

Assuming your NCB is preserved without written confirmation could leave you with a lower effective sum insured than you expected. Verify each benefit separately, in writing, before accepting the new policy.

Cancelling the old policy before written approval

Until the new insurer provides written acceptance of your portability request, your old policy is your only active cover.

Cancelling early — even with a verbal assurance from the new insurer — leaves a gap. If the new insurer’s underwriting is delayed or declines to accept you, you must reapply fresh without continuity credit. Never cancel the old policy before written approval is in hand.

Ignoring the network hospital situation in your specific city

A national insurer may list thousands of hospitals but have thin cashless coverage in your city or locality specifically.

Before porting, confirm that your preferred hospital and the nearest major hospital to your home are on the new insurer’s cashless list — not just in the insurer’s overall network count. Cashless access failures convert every hospitalisation into a reimbursement claim, adding paperwork and temporary out-of-pocket costs at an already stressful time.

When This May Not Be the Right Choice

If you have had a hospitalisation for a serious condition in the last 12 months, or have been diagnosed with a new health condition recently, porting may result in the new insurer declining your application, loading your premium significantly, or adding exclusions that your current insurer has not applied. In these cases, staying with your existing insurer — which has already accepted your health record and renewed without restriction — may be the lower-risk path.

If you are currently relying on your employer’s group health insurance and plan to port it when you leave the job, that is not health insurance portability in the IRDAI sense — it is a fresh individual purchase. Your group policy does not create a personal continuity record. The implications of this gap are significant; read our guide on employer health cover to understand what you are and are not protected by.

If your current insurer proactively offers a retention benefit at renewal — premium freeze, enhanced sum insured, removed loading — compare that option against the uncertainty of underwriting at a new insurer before committing to the switch.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Health insurance portability rules in India are governed by IRDAI regulations and circulars. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- IRDAI — irdai.gov.in (primary regulator for all insurance in India; publishes circulars and portability guidelines)

- Policyholder portal — policyholder.gov.in (consumer-facing guidance on portability rights, process, and grievance redressal)

Before initiating a port, verify the current application deadline, the new insurer’s treatment of waiting period credit and NCB in their specific policy wording, and the documents required for the portability proposal form. Keep copies of all correspondence, the proposal acknowledgement, and any written confirmation from the new insurer about continuity benefit treatment.

Expert Tips

- Start comparing insurers at least 60 days before your renewal date — this gives you time to shortlist, request formal quotes, review policy documents, and submit your application well ahead of the 45-day deadline without rushing.

- Rank insurers first by claim settlement behaviour and cashless hospital coverage in your city, then by premium — a ₹2,500 cheaper plan with poor claim service and no network in your locality is not a saving.

- Ask the new insurer to confirm in writing, before you apply, exactly how your pre-existing disease waiting period credit will be treated and whether it applies to the full sum insured or only to the ported amount — do not rely on verbal representations from a sales intermediary.

- Check the room rent clause specifically against hospital costs in your city. A ₹4,000 per day cap in Mumbai or Bengaluru, where semi-private rooms cost ₹7,000–₹12,000 per night, triggers proportionate deductions on surgeons’ fees, nursing charges, and investigations — not just the accommodation line item.

- If you are increasing your sum insured while porting, ask the new insurer to specify in writing which elements of cover carry a fresh waiting period — typically the incremental amount, not the base amount, is affected, but you need this in writing before you sign.

- If you have accumulated NCB over three or more claim-free years, that may represent a 30–50% increase in your effective sum insured with no additional premium. Confirm whether this transfers, and if not, factor the true economic cost into your comparison — the new insurer’s base sum insured at that premium may be worth significantly less than what you currently hold.

- After porting, keep all documentation from your old insurer: the policy schedule, renewal notice, claim history, and any discharge summaries. These are the proof of continuity credit if a dispute ever arises at claims time with the new insurer.

Frequently Asked Questions

Can I port my health insurance policy at any time during the year?

No. IRDAI health insurance portability rules permit porting only at renewal — not mid-policy year. If you are unhappy with your insurer during the policy term, you must wait until the renewal date to initiate a portability request. Mid-term cancellation and fresh purchase with a different insurer is not the same as portability and does not preserve your continuity benefits.

Will my pre-existing disease waiting period reset when I port?

No — the waiting period credit you have already served should carry forward for the sum insured you are porting. If you are four years into a policy and declared a pre-existing condition at inception, that waiting period should be treated as complete by the new insurer. The reset risk applies only to any additional sum insured you add above your current cover, which may attract a fresh waiting period on the incremental amount.

Can the new insurer reject my portability request?

Yes. The new insurer has the right to decline your application after medical underwriting, offer a policy with additional exclusions, or apply a premium loading based on your health history. IRDAI portability rules require the new insurer to process your application, but they do not guarantee acceptance on identical terms. If your request is declined, your existing policy remains in force provided it has not been cancelled.

Will my no claim bonus transfer automatically when I port?

Not necessarily. NCB treatment depends on both the accumulated NCB in your old insurer’s records and the new insurer’s policy wording on portability. Some insurers recognise existing NCB; others do not. Ask the new insurer for a written statement on NCB treatment before initiating the port — and factor this into your comparison if your current NCB represents a meaningful increase in effective sum insured.

Can I port a family floater policy as a whole unit?

Yes. A family floater policy can be ported together to a new insurer, with all members covered under the floater carrying their continuity status. If you are simultaneously considering splitting the floater into separate individual policies while porting, that is a more complex change — individual members may have different health histories and underwriting outcomes, which can complicate the process.

Should I port if my premium increased by only ₹2,000–₹3,000?

Generally not for a small increase alone. The underwriting risk, potential loss of NCB, possible introduction of new sub-limits or co-pay, and the effort involved may not be justified by a ₹2,000–₹3,000 annual saving. Porting makes stronger sense when the premium gap is material, the old insurer’s hospital network is genuinely weak in your city, or the new plan offers a substantially better structure at a comparable price.

What happens if I miss the 45-day application window?

If you apply less than 45 days before your renewal date, the new insurer may not complete underwriting in time. Your current policy may auto-renew with the old insurer, and your portability request lapses for that renewal cycle. You will need to wait until the next renewal to try again. Missing the window by even a few days can cost you a full year.

Is IRDAI health insurance portability available for group policies from my employer?

Group health insurance policies provided by employers are not covered by the same portability framework. Porting from a group policy to an individual policy when you leave employment is treated as a fresh purchase, not a port under IRDAI’s individual portability rules. Your group policy history does not automatically give you continuity credit with a new individual insurer in the same way a personal policy history would.

Can I increase my sum insured when porting?

Yes, but with conditions. Waiting period credit under portability applies to the original sum insured you are carrying over. For any increase in sum insured above your existing cover, the new insurer may apply a fresh waiting period — particularly for declared pre-existing conditions. Ask the new insurer to specify in writing which elements carry fresh waiting conditions before you accept the new policy terms.

What documents do I typically need for a portability request?

Typically: your existing policy document, the renewal notice from your current insurer, a full claims history, and the new insurer’s portability proposal form with complete medical and health disclosure. Specific document requirements vary by insurer. Confirm the full list directly with the new insurer before submitting, and keep copies of every document and communication for your records.

Final Verdict

Health insurance portability rules give you real leverage to switch to a better insurer without resetting years of waiting period credit — but only if you use the process correctly. Port when your current insurer has a genuinely weak hospital network in your city, poor claim service, or a significantly higher premium with no improvement in cover. Do not port solely for a small premium saving, especially if it means accepting stricter room rent terms or losing a well-accumulated no claim bonus.

Start the process at least 60 days before renewal. Compare policy wording on room rent, sub-limits, exclusions, and hospital network — not just premium and sum insured. Get NCB treatment and waiting period credit confirmed in writing. Keep your old policy active until written approval arrives from the new insurer. Insurance premiums vary by age, health condition, and sum insured — the quote shown online is indicative until underwriting is complete. Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.