Hospital bills in India are no longer small numbers. A week-long admission at a private hospital in Bengaluru or Pune can easily cross ₹6–8 lakh — and most salaried employees carry a base health policy with a sum insured of ₹3–5 lakh. That gap is exactly where top-up health insurance meaning becomes critical. Top-up health insurance is a second layer of medical cover that activates only after your bill crosses a fixed threshold, giving you far more protection at a fraction of what a larger base policy would cost. This article explains how the deductible works, the key difference between a top-up and super top-up plan, and how Indian families should think about layering their health cover — without paying for more than they need. Start with our insurance planning guide if you want the full picture first.

Quick Answer: Top-Up Health Insurance Meaning

Top-up health insurance meaning refers to extra medical cover that starts paying only after your base policy or chosen deductible is crossed. For example, if a hospital bill is ₹8 lakh and the deductible is ₹5 lakh, the top-up may cover eligible costs above that limit, subject to policy terms.

Key Takeaways

- A top-up plan only pays after a single hospital bill crosses your chosen deductible — if your bill stays below that threshold, the top-up pays nothing.

- A super top-up plan adds up all your eligible hospitalisation bills across the year — once the cumulative total crosses the deductible, every claim above it is covered.

- Matching your deductible to your base policy’s sum insured (e.g., ₹5 lakh base + ₹5 lakh deductible top-up) is the most cost-efficient way to expand your cover.

- Top-up premiums qualify for Section 80D deduction — up to ₹25,000 per year for individuals under 60, and ₹50,000 for senior citizens, subject to Income Tax rules in force.

- Top-up plans have their own waiting periods for pre-existing diseases — often 2–4 years — that apply independently from your base policy’s waiting period.

- Employer group health insurance cannot be reliably used as your deductible base: it ends if you leave your job, and claim gaps can leave you personally liable for the deductible amount.

- Super top-up plans are generally better suited to families, especially if multiple members are likely to be hospitalised within the same policy year.

Key Facts at a Glance

| Feature | Top-Up Plan | Super Top-Up Plan |

|---|---|---|

| Deductible trigger | Per single claim | Cumulative annual claims |

| Who it suits | Individuals with one major hospitalisation risk | Families or those with multiple hospitalisations |

| Section 80D benefit | Yes, premium qualifies | Yes, premium qualifies |

| Regulated by | IRDAI | IRDAI |

| Cashless hospitalisation | Available at network hospitals (insurer-specific) | Available at network hospitals (insurer-specific) |

| Pre-existing disease waiting period | Typically 2–4 years (check policy wording) | Typically 2–4 years (check policy wording) |

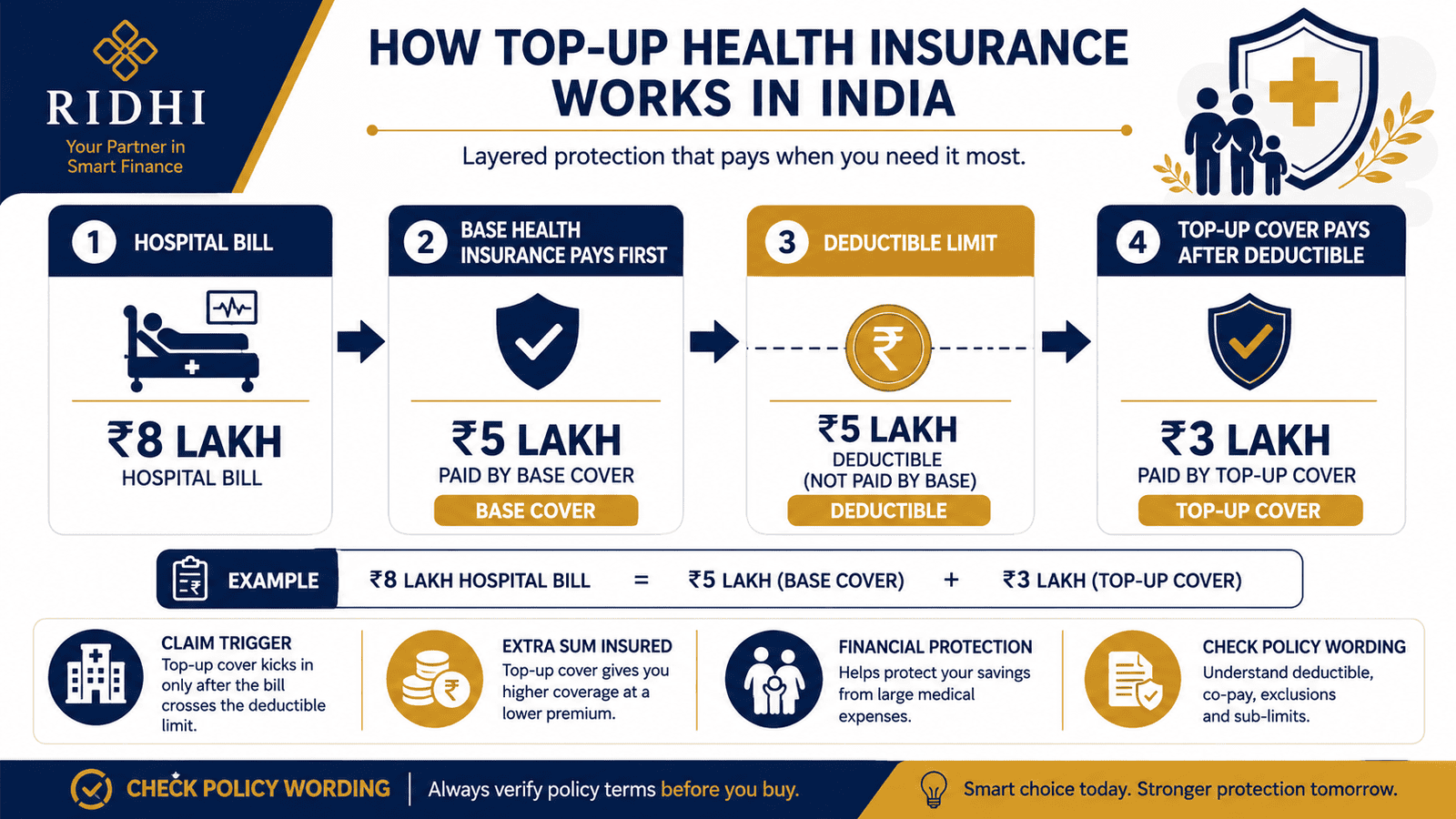

What Is Top-Up Health Insurance — and How Does It Actually Work?

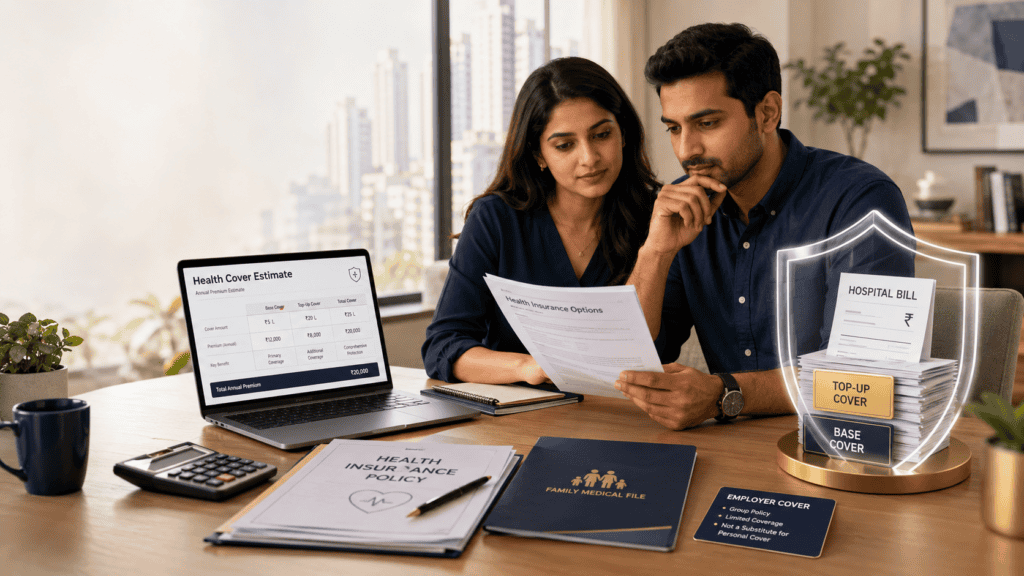

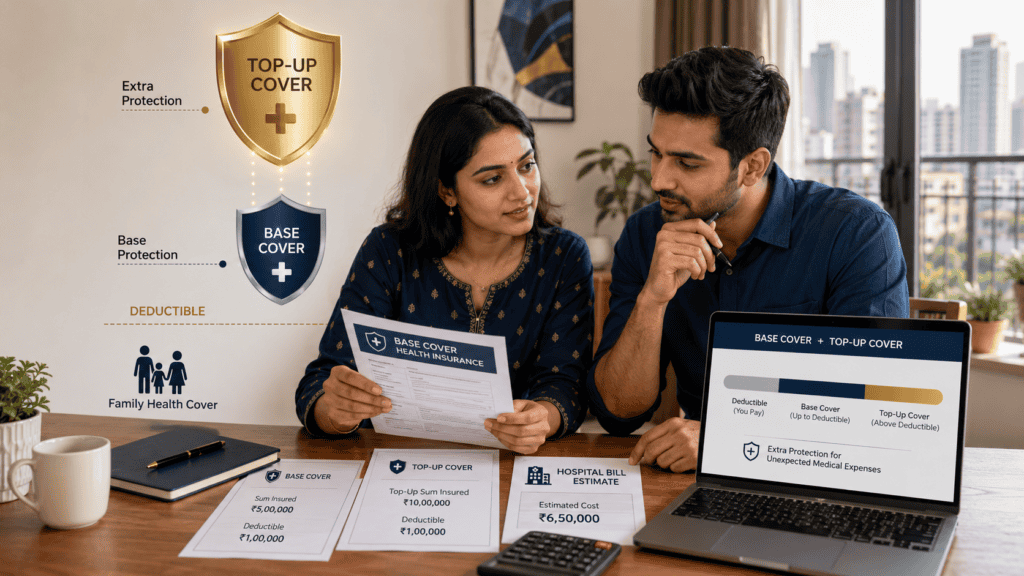

Think of your health cover as a two-bucket system. Your base health policy is the first bucket. When a hospital bill arrives, it fills from that bucket first. A top-up plan is the second, larger bucket — but it only starts filling after the first bucket is empty and the bill crosses a set amount called the deductible.

The deductible in health insurance is the amount you — or your base policy — must pay before the top-up plan pays anything. If your top-up has a deductible of ₹5 lakh and your hospital bill is ₹4.8 lakh, the top-up pays zero. The entire bill falls within the deductible. But if the bill is ₹8 lakh, the top-up covers the remaining ₹3 lakh above the ₹5 lakh threshold — subject to the policy terms and sum insured limit of your top-up plan.

The Deductible Is Not a Penalty — It Is the Activation Point

Many first-time buyers confuse the deductible with an out-of-pocket charge. It is not. The deductible is simply the trigger point below which the top-up is silent. You pay the deductible amount either from your base policy, from your savings, or from an employer group policy. Once that amount is crossed, the top-up takes over.

This design is why top-up plans are so affordable. The insurer knows it will only ever pay for large, catastrophic claims — not every minor hospitalisation. That reduced risk is passed on to you as a lower premium. A top-up plan with a ₹20 lakh sum insured above a ₹5 lakh deductible typically costs a fraction of what a standalone ₹20 lakh base policy would cost.

What Counts as the Deductible Base?

You have three ways to satisfy the deductible before the top-up plan pays:

- Your individual base health policy: The most reliable option. If your base sum insured matches the deductible, every bill that exhausts your base policy automatically triggers the top-up.

- Your employer’s group health policy: Convenient — but risky. If you leave the job mid-year, or if the employer changes the insurer, your group cover disappears. The top-up deductible must still be met from somewhere.

- Out of pocket: Some top-up plans allow the deductible to be paid directly — useful if you have savings set aside as a health emergency fund.

Always read your top-up’s policy wording carefully. Some insurers only allow the deductible to be met by a specific base policy from the same insurer. According to IRDAI health insurance regulations, policy terms must be clearly stated in the document — so never rely on a sales representative’s verbal explanation.

Understand what your basic health cover actually pays for before deciding how to structure your top-up deductible — exclusions in your base policy can create unexpected gaps.

Top-Up vs Super Top-Up: The One Difference That Matters Most

A standard top-up plan applies the deductible to each individual claim separately. So if you are hospitalised twice in a year — once with a ₹3 lakh bill and once with a ₹4 lakh bill — and your deductible is ₹5 lakh, neither bill crosses the threshold alone. The top-up pays nothing for either hospitalisation.

A super top-up plan applies the deductible to the aggregate of all your hospitalisation bills across the policy year. Using the same example: ₹3 lakh + ₹4 lakh = ₹7 lakh in total claims. Once the cumulative amount crosses the ₹5 lakh deductible, the super top-up covers the remaining ₹2 lakh — and any further hospitalisation bills above the already-met deductible for the rest of that policy year.

This makes super top-up plans significantly more practical for families with elderly members, children, or anyone likely to have more than one hospitalisation in a year. The slightly higher premium compared to a standard top-up is almost always worth it in a family floater context.

Sum Insured and How Much Top-Up Cover to Buy

The sum insured of your top-up plan is the maximum amount it will pay above the deductible in a policy year. If you buy a top-up with a ₹20 lakh sum insured and a ₹5 lakh deductible, your total potential cover is ₹25 lakh — assuming your base policy covers the first ₹5 lakh.

A practical rule for most salaried families: match the deductible to your existing base policy’s sum insured, then buy enough top-up sum insured to cover a realistic worst-case hospital bill — typically ₹15–25 lakh for a major surgery or ICU admission at a private hospital in a metro city. This gives you total effective cover of ₹20–30 lakh at a combined premium far lower than buying a ₹25 lakh base policy from scratch.

Real Example: Rahul’s Family Hospitalisation in Pune

Rahul, 36, is a senior software engineer in Pune earning ₹22 lakh per year. He has a family floater base health policy with a ₹5 lakh sum insured, plus a super top-up plan with a ₹20 lakh sum insured and a ₹5 lakh aggregate deductible. His father-in-law, covered under the same family floater, is admitted to a private hospital with a cardiac procedure. The bill comes to ₹9.2 lakh.

Step 1: The base family floater pays ₹5 lakh — the full sum insured — exhausting the base policy for the year.

Step 2: The remaining ₹4.2 lakh exceeds the ₹5 lakh deductible threshold? No — not yet. The aggregate deductible for the super top-up is ₹5 lakh. The base policy paid ₹5 lakh toward the bill. That satisfies the deductible.

Step 3: The super top-up covers ₹4.2 lakh — the portion above the ₹5 lakh deductible.

Rahul’s out-of-pocket cost: ₹0 for this hospitalisation. Without the super top-up, he would have paid ₹4.2 lakh from savings. If Rahul’s wife is also hospitalised later in the same year with a ₹1.5 lakh bill, the super top-up covers that too — the deductible is already met for the year.

Whether to use an individual plan or family floater as the base matters — read our comparison of family floater choice before deciding.

How to Calculate Your Top-Up Payout

Top-Up Payout = Total Eligible Hospital Bill − Deductible Amount (if bill > deductible)

Using Rahul’s example above:

Total bill: ₹9,20,000. Deductible: ₹5,00,000. Payout = ₹9,20,000 − ₹5,00,000 = ₹4,20,000.

If the bill were ₹4,80,000 — below the deductible — the top-up would pay ₹0, and Rahul’s base policy or savings would cover the full amount.

| Scenario | Bill Amount | Top-Up Payout |

|---|---|---|

| Bill below deductible | ₹3,50,000 | ₹0 (base policy or savings cover fully) |

| Bill just above deductible | ₹6,00,000 | ₹1,00,000 |

| Large hospitalisation | ₹9,20,000 | ₹4,20,000 |

| Critical illness or major surgery | ₹18,00,000 | ₹13,00,000 |

All figures assume a ₹5 lakh deductible and sufficient top-up sum insured. Actual payouts depend on eligible expenses under the policy wording and any sub-limits that may apply.

Comparison: Top-Up vs Super Top-Up Health Insurance

| Parameter | Top-Up Plan | Super Top-Up Plan |

|---|---|---|

| Deductible applied | Per single claim | Cumulative across all claims in the policy year |

| Best for | Individuals with one major hospitalisation risk | Families; anyone prone to multiple hospitalisations |

| Multiple small claims | Not covered if each claim is below deductible | Covered once cumulative total exceeds deductible |

| Premium vs top-up | Lower | Slightly higher |

| Complexity | Simpler claim trigger | More tracking required across claims |

| Value for families | Limited | Strong |

How to Decide What’s Right for You

You are a single individual with a solid base policy of ₹5 lakh and want low-cost cover for one catastrophic hospitalisation — THEN a standard top-up with a matching ₹5 lakh deductible is the most affordable route.

You have a family with parents or children on the same floater and any member could be hospitalised more than once in a year — THEN a super top-up is almost always the better choice, even at a slightly higher premium.

Your only health cover is an employer group policy with a ₹3–5 lakh sum insured — THEN buy a personal super top-up with the same deductible amount, but do not rely solely on the employer policy to fund the deductible; it will end when you change jobs.

You are in the 30% tax bracket and are paying top-up premiums — THEN verify your Section 80D deduction eligibility: premium paid for yourself, spouse, and children can reduce taxable income up to ₹25,000 per year (more for senior citizens), subject to rules in force.

Your base policy has significant exclusions — such as no cover for maternity, specific treatments, or certain pre-existing conditions — THEN the top-up plan likely carries similar exclusions; check policy wording before assuming the top-up fills those gaps.

You have no base health policy at all — do not buy only a top-up plan. Without a funded base to meet the deductible, every mid-range hospital bill becomes a direct out-of-pocket expense. Buy a solid base policy first.

Common Mistakes to Avoid

Setting the deductible higher than your base policy sum insured

If your base policy covers ₹3 lakh and your top-up deductible is ₹5 lakh, there is a ₹2 lakh gap that neither policy covers.

A ₹3 lakh bill exhausts your base policy. A ₹4.5 lakh bill still does not trigger the top-up. You pay ₹1.5 lakh from savings — a gap most buyers do not realise exists until the claim arrives.

Always match the deductible to your base sum insured exactly, or keep it lower.

Relying on employer cover to fund the deductible

Group health cover from your employer ends when your employment ends. Mid-year resignations, layoffs, or employer insurer changes leave you without a deductible base.

If you leave your job in August and are hospitalised in September, the top-up deductible is unfunded. You pay the full deductible amount yourself.

Always have a personal base policy that is independent of your employer.

Choosing a top-up instead of a super top-up for a family policy

A standard top-up only pays if a single claim exceeds the deductible. Two ₹3 lakh bills in a year — both under a ₹5 lakh deductible — result in zero top-up payment, even though you paid ₹6 lakh in total.

For families, especially those with elderly parents or young children, the aggregate trigger of a super top-up covers exactly these multi-hospitalisation scenarios. Pay the small additional premium — it is worth it.

Ignoring the top-up plan’s waiting period for pre-existing diseases

Buying a top-up plan does not inherit the waiting period you have already served on your base policy. The top-up has its own waiting period — typically 2–4 years — that starts fresh from the date you buy it.

Check the waiting period rules for your specific top-up policy before assuming that an existing condition is covered on day one.

Buying the cheapest top-up without checking the insurer’s network and claim track record

A ₹200 annual saving on premium is meaningless if the top-up insurer rejects your claim on a technicality or has a poor claim settlement record.

A low-cost plan with limited hospital network coverage may also force reimbursement claims instead of cashless admission — creating significant financial stress during hospitalisation.

Compare insurer reliability before comparing premium alone.

Assuming the top-up will cover all hospital expenses without sub-limits

Some top-up plans have room rent sub-limits — for example, 1% of sum insured per day — that proportionally reduce the entire claim payout if you choose a room above the limit.

A ₹20,000/day room with a ₹2,000/day sub-limit can reduce an ₹8 lakh surgery claim by 90%. Read the policy wording for room rent and ICU caps before buying.

Prefer top-up plans with no room rent sub-limits or with your expected hospital tier explicitly covered.

Not disclosing pre-existing conditions accurately at the time of application

Non-disclosure of pre-existing conditions is the most common reason top-up health insurance claims are rejected. Insurers can void the entire policy — not just deny a single claim — if they discover undisclosed medical history at claim time.

Disclose every condition honestly, even if it means a higher premium or a longer waiting period. It protects your claim when you most need it.

When This May Not Be the Right Choice

A top-up plan is not universally the right move. Consider these scenarios carefully before purchasing:

If you have no stable base health policy to fund the deductible, a top-up plan gives you a false sense of security. You will bear every mid-range hospital bill fully — which is exactly the scenario most people are trying to avoid.

If you are over 60 and have significant pre-existing conditions, the waiting period on a new top-up plan may be 3–4 years. By the time the plan becomes fully active, you may have already incurred the large claim you were planning to use it for.

If your annual hospitalisation risk is low and your existing base cover is adequate for your city and healthcare pattern, the additional premium may not justify the benefit — a well-funded emergency corpus may serve you better.

If you have critical illness risk — cancer, cardiac disease, or stroke — a dedicated critical illness insurance plan may provide broader, lump-sum coverage that a standard top-up cannot replicate.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Top-up and super top-up health insurance plans in India are regulated by the Insurance Regulatory and Development Authority of India (IRDAI). All health insurance product guidelines, standard exclusion lists, and policy wording requirements fall under IRDAI’s mandate.

Premium deductions under Section 80D of the Income Tax Act — including those for top-up premiums — are governed by the Income Tax Department.

- IRDAI — irdai.gov.in

- Income Tax Department — incometax.gov.in

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

For Section 80D deduction rules and worked examples, see our guide on health insurance deduction.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Expert Tips

- Buy your top-up or super top-up plan while you are young and healthy — waiting periods are shorter to serve and premiums are significantly lower. A 30-year-old pays materially less per lakh of cover than a 45-year-old with the same health profile.

- Match your top-up deductible exactly to your base policy sum insured — not higher, not lower. This eliminates the deductible gap and ensures every rupee of coverage works together without an out-of-pocket bridge amount.

- If you have elderly parents on a separate policy, buy a super top-up plan specifically for them. Seniors are more likely to have multiple hospitalisations in a year, making the aggregate deductible trigger far more valuable than a per-claim top-up.

- Check for room rent sub-limits before buying. A top-up plan with no room rent cap gives you genuine cover at any private hospital room of your choice. Sub-limits can quietly reduce a legitimate claim by 50–80% depending on the room chosen during admission.

- When comparing insurers, look at the claim settlement ratio of the insurer for health products specifically — not just their overall settlement rate. High-value top-up claims are more likely to face scrutiny.

- Keep your base policy and your top-up policy with the same insurer if possible. It simplifies coordination of benefits at the time of claim, avoids disputes about deductible documentation, and may make cashless claims smoother.

- Review your top-up coverage every 3 years. Medical inflation in India runs at 10–15% annually — a ₹20 lakh top-up sum insured that was adequate in 2021 may need to be increased by 2025 to cover the same level of care at a private hospital.

Frequently Asked Questions

What is top-up health insurance meaning in simple terms?

A top-up health insurance plan is additional medical cover that only pays when your hospital bill crosses a fixed threshold called the deductible. Below that threshold, your base policy or savings pay. Above it, the top-up pays the excess — up to its sum insured limit.

What is the difference between top-up and super top-up health insurance?

A standard top-up applies the deductible to each individual claim. A super top-up adds all your hospitalisation claims across the policy year — once the cumulative total crosses the deductible, the super top-up covers every subsequent eligible expense for the rest of that year. Super top-up plans are almost always better for families.

Can I buy a top-up plan without an existing base health policy?

Technically, some insurers allow it — but it is not advisable. Without a funded base policy, you must pay the deductible entirely from savings every time you are hospitalised. If a ₹5 lakh deductible sounds manageable to you in savings terms, consider whether you actually need the top-up at all, or whether a standalone base policy is the better first step.

Is the deductible in a top-up plan always the same as my base policy sum insured?

No — it depends on what you choose when buying the top-up. You can choose any available deductible level — common options are ₹2 lakh, ₹3 lakh, ₹5 lakh, or ₹10 lakh. The smartest choice is usually to match the deductible to your base sum insured so there is no gap between the two layers of cover.

What happens if my hospital bill is exactly equal to the deductible?

The top-up pays nothing. The trigger requires the bill to exceed the deductible — not meet it exactly. Your base policy or savings cover the full bill in this case.

Can I claim Section 80D deduction on my top-up health insurance premium?

Yes. Premiums paid for a top-up or super top-up health insurance policy qualify for Section 80D deduction — up to ₹25,000 per year for individuals under 60 (self, spouse, children), and ₹50,000 for senior citizens, subject to the rules in force at the time of filing. Verify current limits at incometax.gov.in before filing.

Does a top-up plan cover pre-existing diseases immediately?

No. Top-up plans have their own waiting period for pre-existing diseases — typically 2 to 4 years from the policy start date. This waiting period is independent of any waiting period you have already served on your base policy. A condition covered by your base policy today may still be excluded by a new top-up plan for several years.

Is it better to increase my base policy sum insured or buy a top-up plan?

For most salaried families, buying a top-up plan is significantly more cost-effective than increasing the base policy sum insured by the same amount. The premium for the top-up layer is lower because the insurer only pays for large, catastrophic claims. However, if your base policy has significant exclusions or sub-limits, those weaknesses are not fixed by a top-up — they need to be resolved at the base level first.

What is an aggregate deductible in health insurance?

An aggregate deductible is the total amount of hospitalisation expenses you must incur across all claims in a policy year before the super top-up plan begins to pay. For example, with a ₹5 lakh aggregate deductible, once your combined claims across the year total more than ₹5 lakh, the super top-up covers all eligible expenses above that cumulative threshold for the rest of the year.

Can a top-up plan be used for cashless hospitalisation?

Yes — most top-up and super top-up plans offer cashless hospitalisation at network hospitals. However, coordination between your base insurer and your top-up insurer at the time of admission can be complex. It is worth confirming the cashless process with your top-up insurer before you are admitted, not during a medical emergency.

Final Verdict

Top-up health insurance meaning, at its core, is simple: it is a cost-efficient way to extend your medical cover far beyond what your base policy alone can provide. For a salaried family with a ₹3–5 lakh base policy in an era of ₹10–20 lakh hospital bills, a super top-up plan is one of the highest-value insurance decisions available. Choose the deductible carefully, match it to your base sum insured, opt for a super top-up over a standard top-up for any family situation, and verify the insurer’s claim track record before committing to a plan. If you are just beginning to build a comprehensive family insurance stack, start with our insurance planning guide to see how every layer fits together. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.