A well-meaning relative suggests LIC Jeevan Anand. Or an LIC agent walks into your office and makes the pitch: “You get life cover and your money back at maturity.” For a salaried family with a home loan, a young child, and a spouse depending on your income, that sounds responsible. But before you sign the proposal form, one question matters more than any premium figure: does this policy actually protect your family if something happens to you tomorrow?

The “money back” argument is emotionally appealing — but it can quietly distract from the real job of life insurance, which is replacing your income. A ₹5 lakh or ₹10 lakh sum assured feels like real cover until you look at your home loan balance, your child’s education timeline, and your monthly household expenses side by side. Before comparing any two products, understanding what your family actually needs is the first step — see our guide to family insurance basics for that foundation.

This article compares LIC Jeevan Anand and term insurance across cover size, premium efficiency, maturity benefit, surrender consequences, and who each product genuinely suits. Product terms and LIC policy versions can and do change — always verify the current document on licindia.in before purchasing.

Quick Answer: LIC Jeevan Anand vs Term Insurance

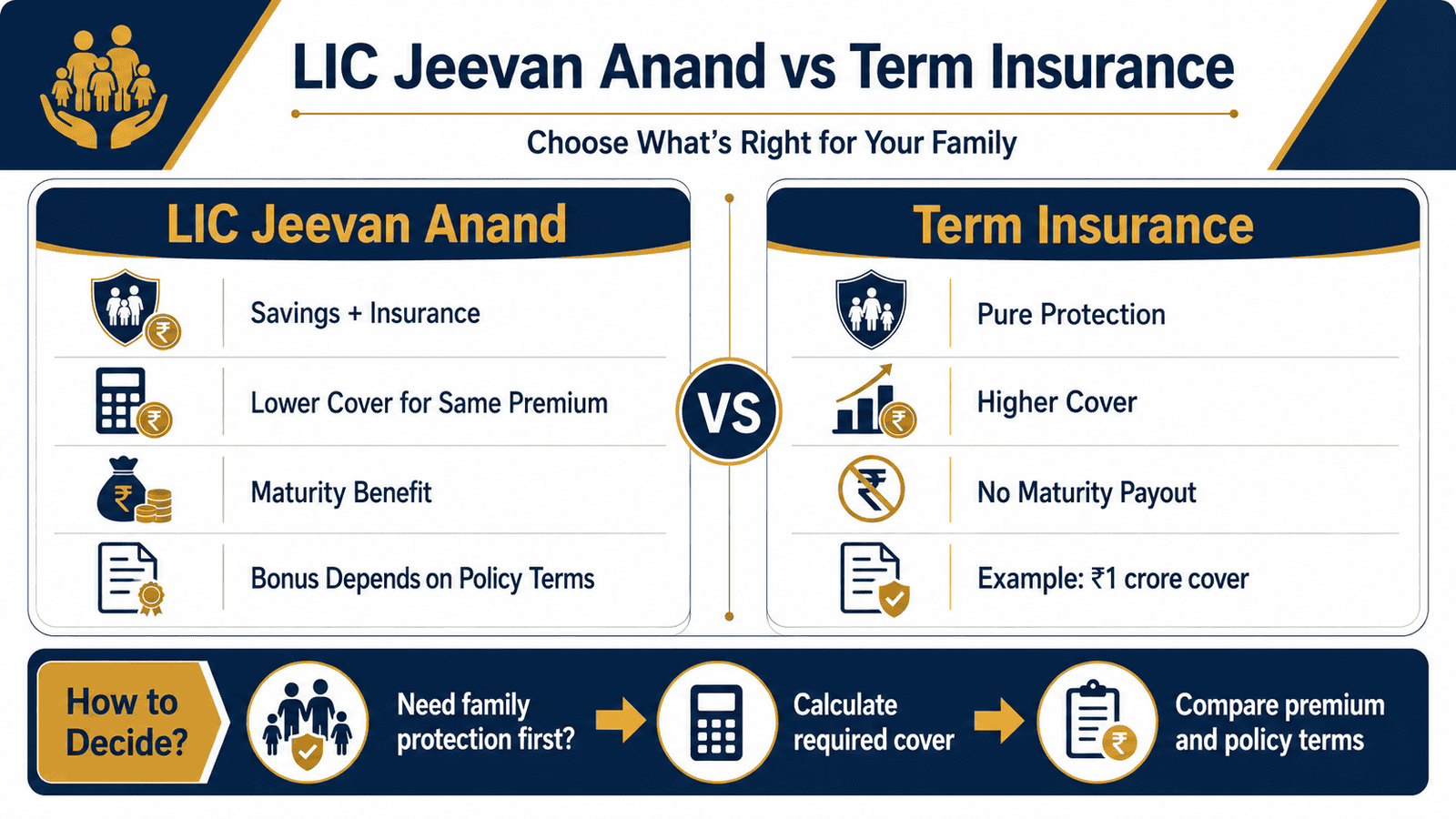

LIC Jeevan Anand vs term insurance is mainly a choice between savings-linked life insurance and pure family protection. Jeevan Anand may offer maturity benefits and lifelong cover terms, while term insurance usually gives much higher cover, such as ₹1 crore, for lower premiums. For most earning families, protection need should be calculated first.

Key Takeaways

- Term insurance is built for pure income replacement — your family receives a large sum assured if you die during the policy term. There is no maturity payout to the policyholder on survival.

- LIC Jeevan Anand is a traditional participating non-linked savings life insurance plan — because the premium funds both a savings component and life cover, the cover amount you get per rupee spent is significantly lower than term insurance.

- The same ₹20,000 annual premium that buys a small traditional sum assured can often secure ₹1 crore or more in term cover for a healthy 34-year-old male non-smoker — the gap in protection is real and material.

- Maturity benefit and bonus projections are not fully guaranteed — only the basic sum assured and already-vested bonuses are relatively secure; future bonuses are declared annually and vary with LIC’s surplus.

- LIC’s older New Jeevan Anand Plan No. 915 (UIN 512N279V02) was withdrawn from sale; verify the currently available plan number, UIN, and policy document on licindia.in before purchasing any version of this policy.

- Do not buy any life insurance policy only for Section 80C tax saving or because a maturity payout exists — calculate the cover your family needs first, then choose the product that meets it.

Comparison: LIC Jeevan Anand vs Term Insurance

| Parameter | LIC Jeevan Anand | Term Insurance |

|---|---|---|

| Primary purpose | Savings-linked life cover: death benefit + maturity benefit | Pure income replacement: death benefit only |

| Life cover for same annual premium | Lower cover per ₹ spent | Much higher cover per ₹ spent |

| Maturity benefit on survival | Sum assured + vested bonuses + final additional bonus (if declared) | Nil — no payout if policyholder survives |

| Death benefit structure | Sum assured on death + vested simple reversionary bonuses | Full sum assured paid to nominee, typically tax-free (conditions apply) |

| Early exit / surrender | Surrender value applies; early exit can mean recovering less than premiums paid | No surrender value; simply stop paying and cover lapses |

| Returns transparency | Bonus declared annually by LIC; non-guaranteed component varies each year | No returns; premium is the pure cost of protection |

| Tax treatment (verify current rules) | 80C deduction on premium; 10(10D) on maturity and death proceeds — conditions apply | 80C deduction on premium; 10(10D) on death proceeds — conditions apply |

| Best suited for | Someone who knowingly wants conservative savings-linked insurance after adequate term cover is already in place | Primary earner with dependents who needs maximum income replacement at lowest annual cost |

Key Facts at a Glance

| Fact | LIC Jeevan Anand | Term Insurance |

|---|---|---|

| Product category | Traditional participating non-linked savings life insurance plan | Pure risk / term life insurance plan |

| Maturity payout | Sum assured + vested simple reversionary bonus + final additional bonus, if declared | None — no survival benefit in standard plans |

| Cover adequacy for earning families | Typically limited by savings component; may not meet ₹1 crore+ income-replacement need | Customisable; ₹1 crore and above cover is widely available |

| Liquidity / early exit | Surrender value available after minimum premium payments; paid-up option available; early exit usually unfavourable | No surrender value; cover lapses on non-payment; no lock-in penalty |

| Policy version to verify before buying | Confirm current plan number, UIN, brochure, and CIS on licindia.in — older Plan No. 915 was withdrawn | Verify policy document, exclusions, waiting periods, and claim process on insurer’s official site |

How LIC Jeevan Anand and Term Insurance Actually Work

What Is LIC Jeevan Anand?

LIC Jeevan Anand is a traditional participating non-linked savings life insurance plan. “Participating” means the policy is eligible for bonuses that LIC declares each year from its actuarial surplus — these bonuses are not guaranteed and vary with each declaration. “Non-linked” means the policy has no exposure to stock market indices or mutual fund unit values. Your premium and maturity benefit are not market-dependent.

When you pay a Jeevan Anand premium, that money is pooled to serve several functions simultaneously: the cost of life risk cover, a savings reserve that supports the maturity payout, LIC’s operating expenses, and the annual bonus accumulation fund. Because one rupee of premium is doing multiple jobs at once, the life cover amount — the sum assured — that you receive per rupee is significantly lower than what a pure term plan would deliver for the same outlay.

At maturity, the policyholder receives the sum assured on maturity plus vested simple reversionary bonuses plus any final additional bonus LIC declares. On death during the policy term, the nominee receives the sum assured on death plus accrued bonuses. LIC’s older New Jeevan Anand Plan No. 915 was withdrawn from sale; verify the currently offered plan number, UIN, and policy document directly on licindia.in before purchasing.

What Is Term Insurance?

A pure protection plan like term insurance does exactly one thing: it pays a large lump sum to your family if you die during the policy term. No savings component. No maturity payout on survival. No bonus accumulation. Because the entire premium is priced around the cost of covering your mortality risk, the same annual premium buys dramatically more life cover than a savings-linked plan. That is not a flaw in traditional plans — it is simply what each product is designed to do.

For a healthy, 34-year-old non-smoking male, ₹1 crore in term cover is available across multiple IRDAI-registered life insurers. The premium cost per lakh of cover is far lower than in a traditional savings plan precisely because no savings corpus is being built alongside.

The Core Trade-off: Savings Plus Cover vs Cover Only

The confusion in this comparison centres on the word “returns.” In a traditional plan, part of your premium goes toward building a maturity corpus. That maturity payout is sometimes described as a return on investment. But this conflates two separate financial functions: insurance protection and savings or investment. When you combine both in one product, the plan must balance both goals rather than optimising for either.

This is why many financial planners recommend keeping insurance and investing separate — a ₹1 crore term plan at a lower annual premium leaves budget for PPF, ELSS, NPS, or other transparent instruments where you can track returns clearly. Whether that separation suits you depends on your goals, discipline, and existing financial setup.

Key Terms Explained: Sum Assured, Bonus, Surrender Value, Paid-Up

Sum assured is the basic cover amount agreed at inception. In traditional plans, the death benefit is typically defined as the higher of: a multiple of annualised premium, or the sum assured on death — verify exact terms in the current policy document. Maturity benefit is sum assured on maturity plus vested simple reversionary bonuses plus final additional bonus. The bonus components are non-guaranteed beyond what has already been declared and vested.

Surrender value becomes available after a minimum number of premium payments — the threshold and the surrender value factor depend on the policy document and premium payment years completed. Surrendering early, especially in the first three to five years, typically means recovering significantly less than total premiums paid. The paid-up option reduces the sum assured proportionally if you stop paying after the minimum premium period — the policy does not lapse, but cover and maturity value reduce.

Real Example: Rahul Sharma, Pune — The Cover Gap

Rahul Sharma is 34, an IT project manager in Pune earning ₹18 lakh per year. His household runs on around ₹75,000 per month. He has a home loan with approximately ₹38 lakh outstanding, a 6-year-old child, and a spouse who currently has no independent income. Rahul’s mother suggested he take a traditional LIC policy — “something safe with money back.”

Under Scenario A, Rahul buys a traditional savings plan with a ₹5 lakh sum assured. His family is covered for ₹5 lakh plus any declared bonuses. His home loan alone is ₹38 lakh. If Rahul dies in year five, the policy payout covers less than 15% of his outstanding loan — before accounting for household expenses or his child’s education.

Under Scenario B, Rahul spends a similar or slightly different annual outlay on a ₹1 crore term plan for 25 years. His nominee receives ₹1 crore tax-free. The home loan is cleared, the family can sustain monthly expenses for over a decade, and the child’s education fund remains intact.

This is not about LIC being unsafe — LIC’s claim-paying record is established. It is about what each product type is designed to deliver. Actual premiums depend on age, health status, smoker or non-smoker classification, policy term, riders selected, insurer, and underwriting outcome. Verify current premium quotes and benefit illustrations from official sources before making any comparison.

How to Calculate If Your Cover Is Enough

Required Cover = (Outstanding Liabilities) + (Annual Household Expenses × 10 to 15) + (Future Financial Goals) − (Existing Liquid Assets)

Using Rahul’s numbers as an illustration only:

| Component | Rahul’s Illustrative Figure | How to Estimate Yours |

|---|---|---|

| Outstanding home loan | ₹38,00,000 | Check latest loan statement |

| 10 years family expenses (₹75,000 × 12 × 10) | ₹90,00,000 | Current monthly spend × 120 |

| Child’s future education goal (illustrative) | ₹20,00,000 | Estimate in today’s rupee value |

| Less existing liquid assets | −₹12,00,000 | FD, savings, liquid funds accessible within a week |

| Estimated required cover | ₹1,36,00,000 | Round up to next ₹25 lakh bracket |

Rahul needs roughly ₹1.25–1.5 crore in life cover. A ₹5 lakh or ₹10 lakh traditional policy sum assured covers less than 8% of that need. Use the term cover calculation tool to run your own numbers before comparing any products.

How to Decide What’s Right for You

Your family depends on your income and you have a home loan, dependent spouse, or young children — calculate your protection need first. If that number is ₹75 lakh or more, a term plan is likely the more direct solution before any savings-linked product is considered.

You already have adequate term cover of ₹1 crore or more and want a conservative savings-linked product as a secondary financial instrument — then LIC Jeevan Anand can be evaluated on its own merits: guaranteed sum assured, bonus accumulation, and a traditional savings structure. Just ensure the protection gap is already closed.

Maturity payout matters to you but you also want transparency in returns — compare term plus investing in PPF, ELSS, or NPS against a traditional plan using the same annual budget. Separating insurance cost from wealth creation often results in a clearer picture of where your money is going.

You are buying any life insurance policy because March 31 is approaching and you need an 80C deduction — stop. Check whether you have adequate protection first. A ₹1 crore term plan also qualifies for 80C, and it gives your family far more cover per rupee of premium than a traditional plan.

You are confident you can sustain premium payments without interruption for 20–25 years — a traditional savings plan becomes less risky. If there is any realistic chance you will stop paying within five to seven years, the surrender value consequences can mean a significant financial loss compared to total premiums paid.

Do not treat LIC Jeevan Anand as your primary or only life cover if your family’s income-replacement need is ₹50 lakh or above and the policy sum assured is a fraction of that. The gap between what is needed and what is covered is real — and it will matter to your family, not to an agent’s commission.

Common Mistakes to Avoid

Buying a Policy Because “LIC Is Safe” Without Checking Cover Size

LIC’s solvency margin and claim-paying track record are a separate question from whether a specific policy provides adequate cover for your family’s needs.

A financially strong insurer with a ₹5 lakh sum assured still leaves a ₹1.3 crore gap if that is what your family actually needs. Brand trust and cover adequacy must be evaluated independently.

First calculate the cover your family requires — then choose the insurer and product that meets it.

Choosing Any Plan Solely Because It Returns Money at Maturity

Maturity value feels like “getting money back.” But the question is: what did that maturity amount cost you in terms of the protection gap it created over 20–25 years?

If you committed ₹20,000/year to a policy with a ₹5 lakh sum assured when you needed ₹1.25 crore in cover, the maturity payout does not compensate for two decades of underinsurance.

Evaluate total cost, protection provided, and opportunity cost together — not maturity amount in isolation.

Comparing Maturity Amounts Without Looking at Cover Size

Many buyers compare “₹12 lakh maturity from Jeevan Anand vs ₹0 back from term insurance” and conclude the traditional plan is better value. This comparison ignores the fact that the term insurance buyer had ₹1 crore of protection throughout the same period for a lower annual outlay. The comparison is only valid if cover sizes are equal — which they rarely are.

Ignoring Surrender Value and Paid-Up Consequences Before Buying

If you stop paying premiums on a traditional plan before the minimum required years, you may receive very little on surrender — often less than total premiums paid. Even after the paid-up period, the sum assured reduces to a paid-up value and the policy’s protection diminishes.

Only commit to a traditional plan if you are confident you can sustain premiums for the full policy term.

Not Verifying the Current LIC Plan Version Before Purchasing

LIC’s older New Jeevan Anand Plan No. 915 was withdrawn from sale. The current plan number, UIN, and policy document must be confirmed directly on licindia.in before purchasing. Relying on an agent’s old brochure, an outdated PDF, or a comparison article from 2022 can lead to incorrect expectations on premiums, benefits, or surrender terms.

Treating Bonus Projections as Guaranteed Returns

A benefit illustration shows low and high bonus scenarios alongside guaranteed elements. The higher projections are non-guaranteed — they depend on LIC’s actual surplus declaration each year, which can vary. Plan your protection needs and financial decisions around the guaranteed minimum, not the optimistic scenario an agent circles in the illustration.

Assuming the Maturity Payout Is Always Tax-Free Without Checking

Section 10(10D) exemption on life insurance maturity proceeds has conditions — including rules on the premium-to-sum-assured ratio — that can affect whether the payout qualifies as tax-free. These conditions have been tightened in recent budgets. Verify current tax treatment from incometax.gov.in or a qualified tax professional before factoring tax-free maturity into your decision.

When This May Not Be the Right Choice

LIC Jeevan Anand may not suit you if your primary need is replacing a large income. A salaried professional earning ₹15–20 lakh in a metro city with a home loan, young children, and a dependent spouse typically needs ₹1 crore or more in life cover. The premium required to build a ₹1 crore sum assured through a traditional savings plan is significantly higher than what a term plan would cost for the same cover — making the traditional plan an inefficient solution for this specific need.

It may also not suit you if there is any realistic chance of discontinuing premiums within five to seven years. Early surrender of a traditional plan is among the most common causes of insurance-related financial loss in India — the surrender value recovered is typically well below total premiums paid in the early years.

Term insurance, conversely, may not suit someone who has a specific, informed preference for savings-linked traditional insurance and has already secured adequate protection through other policies. That is a valid position — but it requires genuinely adequate protection to already exist.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Life insurance products in India are regulated by the Insurance Regulatory and Development Authority of India. Product terms, benefit structures, premium rates, surrender rules, and tax treatment are all subject to change with regulatory updates, budget changes, and product revisions.

- LIC (licindia.in) — Verify the currently available plan version, plan number, UIN, official policy document, Customer Information Sheet, standard benefit illustration, premium table, and surrender value terms before purchasing. LIC’s older New Jeevan Anand Plan No. 915 / UIN 512N279V02 was withdrawn from sale; confirm what is currently offered on the LIC website.

- IRDAI (irdai.gov.in) — Verify insurer registration, consumer protection rights, and grievance escalation procedures. For claim settlement data across insurers, refer to IRDAI’s published annual report — not individual insurer marketing materials.

- Income Tax Department (incometax.gov.in) — Verify current Section 80C deduction limits, Section 10(10D) conditions for maturity and death proceeds, and any budget-year amendments affecting insurance tax treatment.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Do not rely solely on agent WhatsApp forwards, old brochures, or benefit illustrations from a previous policy version. The policy document you sign governs everything.

Expert Tips

- Start with the protection number, not the product brochure. Use the formula: outstanding liabilities + 10–15 years of household expenses + financial goals − liquid assets. For most salaried families in metro India, that figure is ₹75 lakh to ₹2 crore — not ₹5–10 lakh.

- Always ask for the official Benefit Illustration from LIC before purchasing Jeevan Anand. It separates guaranteed components from non-guaranteed bonus projections. If an agent cannot produce the official illustration, that is a warning sign — do not proceed without it.

- Verify the current LIC plan number and UIN on licindia.in before committing. Agents may carry brochures for older withdrawn versions. Only the currently-sold product and its active policy document are legally binding.

- If you want a savings element in your financial plan and you already have adequate term cover, compare the Jeevan Anand maturity projection against PPF or ELSS over the same policy term before deciding. The bonus projections in a benefit illustration are non-guaranteed; the PPF rate is set by the government each quarter and currently better tracked.

- Review your life cover amount after every major life event — marriage, birth of a child, a new home loan, or a significant salary increase. Cover that was adequate at 28 may be seriously insufficient at 35.

- If you already hold a traditional LIC plan and now realise it is underinsured, do not surrender it impulsively. Buy additional term cover first to close the protection gap. Then decide on the traditional plan calmly — not under pressure.

Frequently Asked Questions

Is LIC Jeevan Anand better than term insurance?

For income replacement — the core job of life insurance — term insurance is usually more efficient because it provides significantly higher cover for the same or lower annual premium. LIC Jeevan Anand is a savings-linked traditional policy and is not designed to be a direct substitute for a large-cover term plan. “Better” depends entirely on your protection need, budget, and goals. Calculate required cover first, then choose the product that meets it.

Is LIC New Jeevan Anand still available to buy?

LIC’s New Jeevan Anand Plan No. 915 (UIN 512N279V02) was withdrawn from sale. LIC’s current product pages reference a New Jeevan Anand plan under a newer UIN. The exact currently-offered plan number, availability, and policy terms must be confirmed directly on licindia.in or through a licensed LIC agent before purchasing. Do not rely on older brochures.

What is the main difference between Jeevan Anand and a term plan?

Jeevan Anand combines savings and life cover in one policy — you receive a maturity payout at the end of the term plus a death benefit if you pass away during the term. Term insurance provides only a death benefit; there is no payout to the policyholder on survival. The trade-off is straightforward: maturity value versus the size of protection cover. The same annual premium typically buys much higher life cover in a term plan than in a traditional savings plan.

Does term insurance return money if I survive the policy term?

Standard term insurance does not. If you survive the full policy term, your premiums are not returned — they were the cost of keeping your family protected. Some insurers offer “return of premium” variants at a higher premium, but these significantly increase annual cost. For most buyers, a standard term plan at a lower premium with the difference invested elsewhere is likely to produce better overall outcomes — though you should verify specific product terms and costs before deciding.

Is LIC Jeevan Anand a good investment option?

It is a traditional participating savings-linked plan — not an investment product in the mutual fund or ULIP sense. Bonuses are declared by LIC annually and the non-guaranteed portion varies. Traditional endowment and savings plans have generally produced effective returns lower than PPF or long-term equity over comparable periods, though individual outcomes depend on actual declared bonuses, policy term, and your personal tax situation. Ask for the benefit illustration, check the guaranteed versus non-guaranteed split, and make your own comparison before deciding.

What should a salaried person buy first — term insurance or a traditional plan?

For a salaried person with dependents, a home loan, or a family relying on their income, adequate protection cover typically comes first. The primary financial risk is leaving your family without income. Traditional savings plans and investments are secondary decisions once the protection gap is addressed — not products to buy instead of protection.

How much term insurance cover is actually enough?

A practical starting point: outstanding loans + 10–15 years of household expenses + future financial goals (child’s education, spouse’s retirement) − existing liquid assets. For a salaried professional earning ₹15–18 lakh in a metro city with a home loan and young children, this often works out to ₹1–1.5 crore. Use the term cover calculation tool to work through your own numbers before comparing products.

Can I hold both LIC Jeevan Anand and a term plan at the same time?

Yes, many policyholders hold both. A common approach is to buy sufficient term cover first — ₹1 crore or more — to close the income-replacement gap, and then separately evaluate a traditional plan for conservative savings or legacy goals. The critical point is that the traditional plan should not be your only life cover when your family’s protection need is significantly higher than the policy sum assured.

What should I verify before buying any LIC policy?

Confirm: the current plan number and UIN on licindia.in; the official policy document and Customer Information Sheet; the standard benefit illustration with guaranteed and non-guaranteed components labelled separately; the annual premium including GST; surrender value and paid-up value terms; riders available and their costs; exclusions; and the free-look period. Never sign a proposal based solely on a verbal pitch or a forwarded PDF.

Is the maturity amount from LIC Jeevan Anand tax-free?

Section 10(10D) of the Income Tax Act governs tax treatment of life insurance proceeds. Conditions — including rules around the ratio of annual premium to sum assured — determine whether maturity proceeds qualify for exemption. These conditions have been revised in recent Union Budgets. Verify the current applicable rules with a qualified tax professional or from incometax.gov.in before assuming the payout will be tax-free.

What happens if I stop paying Jeevan Anand premiums midway?

If you stop before completing the minimum premium payment period, the policy typically lapses and surrender value, if any, is minimal. After completing the minimum period, the policy can convert to paid-up status — the sum assured reduces proportionally and the policy continues at lower cover without further premiums. Surrendering a traditional plan early is one of the most common reasons policyholders receive significantly less than total premiums paid. Verify the exact paid-up and surrender terms in the current policy document before purchasing.

Final Verdict

For income replacement — the core job of life insurance — term insurance usually solves the problem more directly. A ₹1 crore term plan typically costs less per year than a traditional savings plan with a ₹10–15 lakh sum assured, and the protection is many times larger. LIC Jeevan Anand vs term insurance is not a question of which is “better” in the abstract — it is a question of what your family actually needs your insurance to do.

If adequate protection is already in place and you want a conservative savings-linked product as a secondary instrument, Jeevan Anand can be evaluated on its own terms: guaranteed savings structure, LIC’s institutional track record, and traditional policy features. If protection is not yet in place, that comes first — before any savings plan, before any tax deadline. Compare cover adequacy, affordability, surrender terms, and opportunity cost, not just maturity amounts.

Connect your insurance decision to a broader financial plan using our basic money planning guide — insurance is one layer, not the whole foundation. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.