Your credit card statement says you earned 3,200 reward points last month. That sounds like a good deal — until you do the actual math. If each point is worth ₹0.25, that is ₹800 gross. Subtract a ₹99 redemption fee, add 18% GST on that fee, factor in your card’s ₹999 annual fee spread across 12 months, and your real monthly reward falls to around ₹600. And that is before checking whether fuel, rent or wallet loads were excluded from earning points at all.

Points, miles and cashback are not equally valuable. The real ₹ return depends on your card’s terms, your spending categories, the redemption option you choose, and any caps or exclusions that quietly reduce what you actually receive. Card features and reward rates can change without notice, according to RBI guidelines.

This article gives you the four-formula calculator model to find the true ₹ value of any credit card reward — and shows you exactly when chasing rewards creates more harm than benefit.

Quick Answer: Credit Card Rewards Points Calculator

A credit card rewards points calculator helps you convert points, miles or cashback into real ₹ value. Enter your spend, points earned, redemption value, fees and annual charges to find the effective reward rate. A card giving 2,000 points may be worth only ₹500 if each point equals ₹0.25.

How to Calculate Credit Card Rewards Value

Use these four formulas in sequence. All figures below are illustrative examples — verify actual rates, fees and values from your card’s MITC or official rewards portal before running your own calculation.

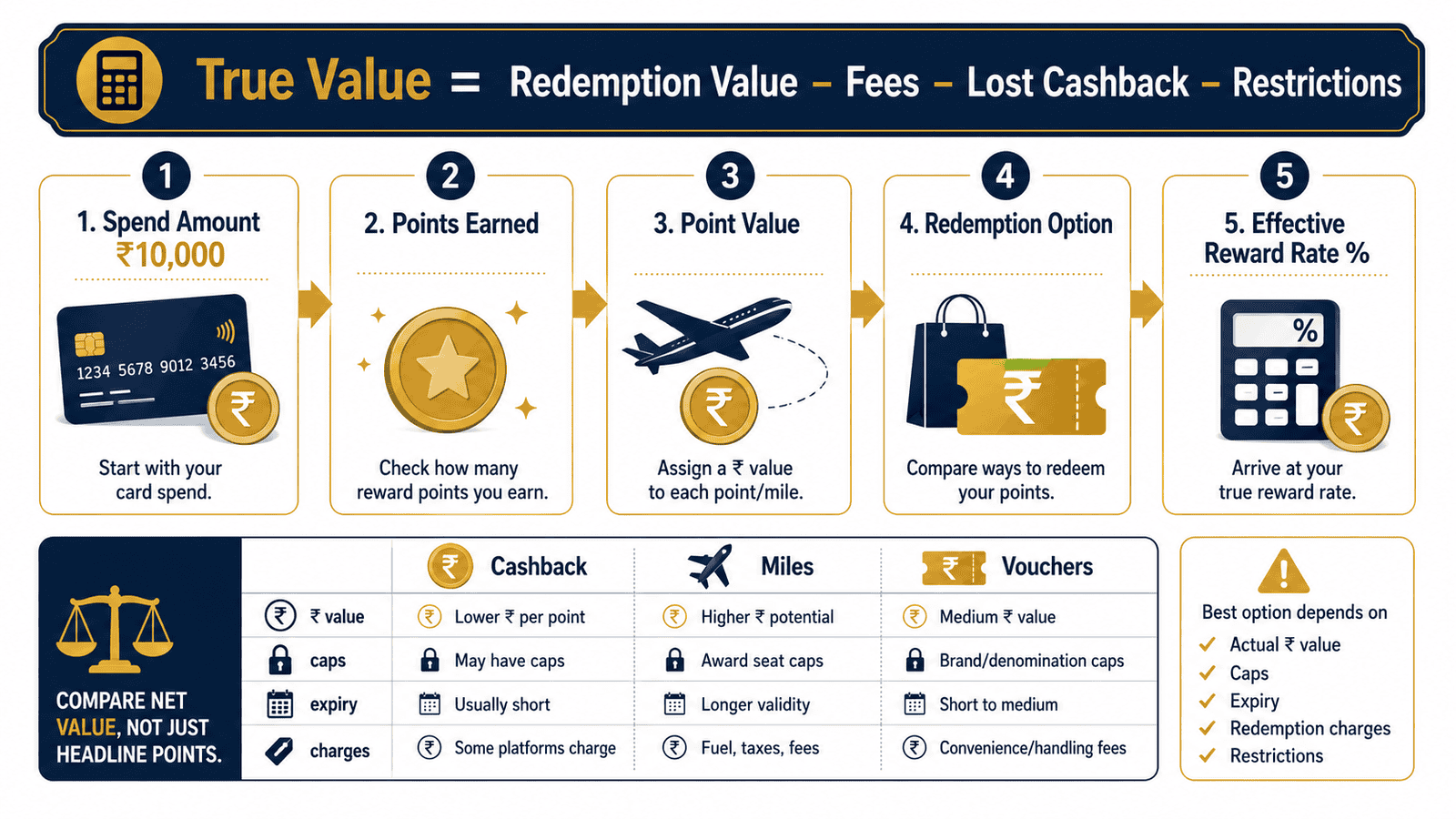

Formula 1 — Points Earned = (Eligible Monthly Spend ÷ Spend Block) × Points Per Block

Example: ₹30,000 eligible spend ÷ ₹100 spend block × 2 points = 600 points. “Eligible spend” excludes fuel, rent payments via apps, wallet loads, government payments and EMI transactions on most cards — always confirm your card’s excluded categories from the MITC.

Formula 2 — Gross Reward Value (₹) = Points Earned × Point Value (₹ per point)

600 points × ₹0.25 per point = ₹150 gross reward value. Point value varies by redemption type — cashback may give ₹0.25 per point while travel redemptions may give ₹0.50 or more on some cards. Verify your card’s redemption catalogue for exact values.

Formula 3 — Net Reward Value = Gross Reward Value − Redemption Fee (incl. GST) − Monthly Annual Fee Share

₹150 − ₹35 (redemption fee including GST) − ₹83 (₹999 annual fee ÷ 12 months) = ₹32 net reward. If your annual fee is waived based on annual spend, skip that deduction — check annual fee waiver eligibility from your card issuer.

Formula 4 — Effective Reward Rate (%) = Net Reward Value ÷ Eligible Spend × 100

₹32 ÷ ₹30,000 × 100 = 0.11%. This is your real reward rate after all deductions — not the headline “2X” or “5X” the card advertises. Most cardholders are surprised how much lower this number is than expected.

Three Calculator Modes

Points mode: Use Formulas 1–4 as shown. Confirm the ₹ value per point at your chosen redemption type before calculating.

Cashback mode: Skip Formulas 1 and 2. Use cashback earned directly as gross reward value — cashback is expressed in ₹ already. Then subtract the monthly annual fee share and any cashback cap applied that cycle.

Miles mode: Use Formula 1 to calculate miles earned. Replace point value with “mile value in ₹,” which depends on the airline, route, cabin class and booking availability. Mile values vary significantly and must be verified directly with the airline or card travel portal before using any conversion rate in your calculation.

Key Takeaways

- 1 reward point does not equal ₹1 on most Indian credit cards — actual point value typically ranges from ₹0.25 to ₹0.50 per point for cashback redemption, depending on the card.

- Cashback is the simplest reward to value, but many cards apply a monthly or annual cap — check your card’s MITC for the exact limit.

- Air miles can offer high per-unit value, but only if you travel enough to use them before expiry — unused miles are worth exactly ₹0.

- After deducting annual fees, redemption fees and GST on those fees, your effective reward rate can fall well below 1% of eligible spend.

- Paying even ₹500 in credit card interest in one month wipes out several months of reward value — billing discipline matters more than reward optimisation.

- Fuel, rent, wallet loads, EMI conversions and government payments are commonly excluded from earning rewards — counting them overstates your effective reward rate.

- Run Formula 4 on your current card before comparing alternatives — the headline multiplier and the real effective rate are rarely the same number.

Key Facts at a Glance

| Calculator Input / Output | What It Means | Example Value |

|---|---|---|

| Monthly eligible spend | Total card spend minus excluded categories | ₹30,000 (example only) |

| Spend block | The ₹ amount per points unit — e.g. ₹100, ₹150 or ₹200 | ₹100 (example only) |

| Points per block | Number of points earned per spend block | 2 points (example only) |

| Point or mile value (₹) | ₹ per point at chosen redemption type | ₹0.25 cashback (example only) |

| Annual fee monthly share | Annual fee ÷ 12 — the monthly cost of holding the card | ₹83 for ₹999 annual fee (example) |

| Redemption fee + GST | Charged by some cards at the time of redemption | ₹35 (example only) |

| Reward cap | Maximum points or cashback per billing cycle | Varies by card — check MITC |

| Net reward value | Gross reward − fees − annual fee monthly share | ₹32 (using above examples) |

| Effective reward rate | Net reward ÷ eligible spend × 100 | 0.11% (using above examples) |

How Credit Card Reward Systems Work

Before using the credit card rewards points calculator accurately, you need to understand what each reward type actually is — and why the same card delivers very different ₹ values depending on how you redeem.

The Four Reward Types

Reward points are the most common format on Indian cards. Your card earns a fixed number of points per ₹ spent, which you accumulate and redeem through a portal. The critical variable is point value — which changes depending on whether you redeem for cashback, vouchers, products or flight bookings.

Cashback is credited directly to your statement or as a separate payment. It is the easiest reward to value — ₹50 cashback is exactly ₹50, no conversion needed. However, cashback cards frequently apply monthly or annual caps that limit how much you can earn regardless of spend.

Air miles are earned on co-branded airline cards or through programmes that convert points to miles. The ₹ value of a mile depends entirely on the airline, route, fare class and seat availability at redemption. Unused miles expire and become worthless — this makes miles a high-risk, high-reward option that only suits frequent flyers.

Vouchers and statement credit are redemption options, not separate reward formats. Vouchers may carry a higher apparent point value than cashback, but they restrict you to specific brands, which can push unnecessary spending.

Base Rewards, Accelerated Rewards and Milestone Benefits

Most cards operate in tiers. Base rewards apply to all eligible spend — typically 1 to 2 points per ₹100. Accelerated rewards (3X, 5X, 10X) apply to specific categories like dining or travel, but almost always come with category caps. Milestone benefits — such as a flight voucher at ₹2 lakh annual spend — only deliver value if your natural spending reaches the threshold without forcing additional expenditure.

If you are new to credit cards, selecting the right card for your spending pattern matters far more than optimising reward multipliers. Read our first credit card guide before deciding which reward structure to focus on.

Excluded Spend Categories

Common exclusions across most Indian cards include fuel purchases, rental payments through apps, digital wallet loads, EMI conversions, insurance premiums, education fees and government payments. If you include excluded spend in your Formula 1 calculation, your estimated effective reward rate will be overstated. Always verify which categories are excluded in your specific card’s MITC before running the calculator.

Why Redemption Value Is As Important As Earn Rate

A card may advertise ₹1 per point for flight redemptions but only ₹0.25 per point for cashback. If you redeem for cashback after assuming the flight rate, your actual reward is 75% lower than you expected. This single misunderstanding accounts for most reward disappointment among Indian cardholders.

Effective reward rate also falls when points expire. Many cards carry expiry windows of 1 to 3 years. Expired points have zero value regardless of the nominal ₹ amount they represented.

Rewards only deliver net value if you pay your full outstanding balance every billing cycle. Understanding your billing cycle basics — including how the grace period works — is essential. According to RBI guidelines on credit card charges, banks must clearly disclose interest rates and minimum amounts due; credit card interest rates are among the highest of any consumer credit product in India.

Real Example: Aarav’s Monthly Reward Calculation

Aarav, 29, is a software engineer in Pune earning ₹18 lakh per year. He puts roughly ₹40,000 of monthly expenses on his credit card — groceries, dining, travel bookings and online shopping.

After checking his card’s MITC, Aarav confirms that fuel spend (₹3,500) and rent payments via a digital wallet (₹8,000) are excluded categories. His eligible monthly spend is ₹28,500.

His card earns 2 points per ₹100 spend. Points earned: ₹28,500 ÷ ₹100 × 2 = 570 points. He redeems for statement credit at ₹0.25 per point. Gross reward value: 570 × ₹0.25 = ₹142.50.

His card carries a ₹999 annual fee (monthly share: ₹83). Redemption attracts a fee of ₹29.50 including GST. Net monthly reward: ₹142.50 − ₹29.50 − ₹83 = ₹30. Effective reward rate: ₹30 ÷ ₹28,500 × 100 = 0.11%.

The headline “2X points” delivered ₹30 of usable monthly value. All figures above are illustrative examples only and do not represent any specific card’s actual rates or terms.

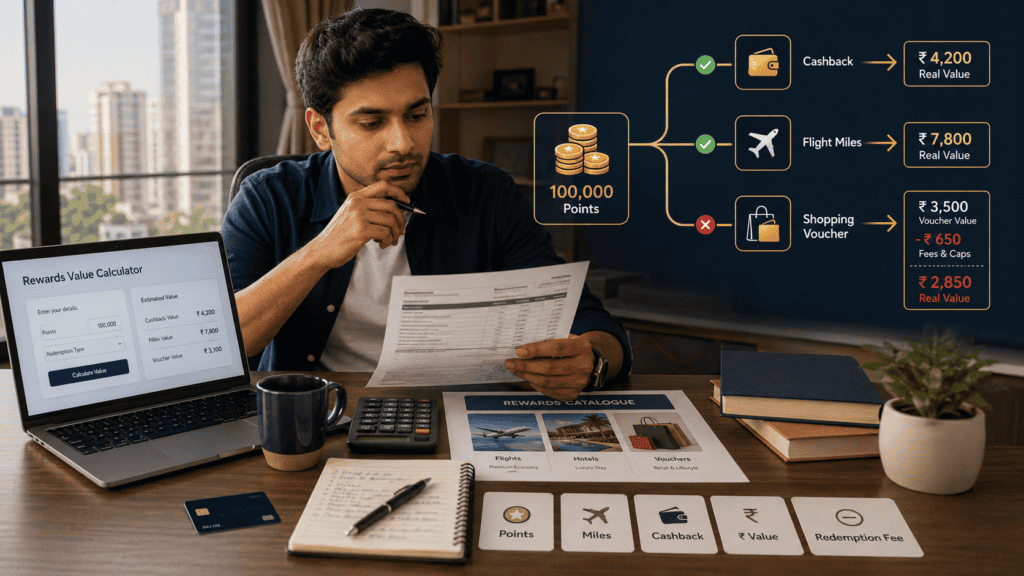

Comparison: Points, Miles, Cashback and Vouchers

Before choosing a redemption type, compare them by effective usable ₹ value for your specific situation. Our full guide on reward versus cashback covers this comparison in depth.

| Reward Type | Best For | Watch Out For |

|---|---|---|

| Cashback | Beginners and salaried earners who want simple, predictable ₹ value | Monthly or annual caps; some cards restrict which spend categories earn cashback |

| Reward Points (cashback redemption) | Cardholders who want flexibility but prefer liquid value over products | Point value for cashback is often lower than for travel — check the redemption catalogue |

| Reward Points (travel / flight) | Frequent travellers who can book award seats on preferred airlines | Blackout dates, minimum point thresholds, and expiry can reduce effective value sharply |

| Air Miles | High-frequency flyers holding a co-branded airline card | Miles expire; value exists only when you actually fly — unused miles are worth ₹0 |

| Vouchers | Shoppers with planned purchases at supported brands | Can push unnecessary spending; no value if you would not visit that brand otherwise |

| Statement Credit | Anyone wanting a direct reduction in their card outstanding | Often the lowest point value in the catalogue — compare before choosing this option |

How to Decide What’s Right for You

you want the simplest reward to calculate and use — THEN choose a cashback card and confirm the monthly cap before applying.

you spend heavily on one or two categories like dining or online shopping — THEN look for accelerated rewards on those specific categories, then verify the category cap and point value at your preferred redemption type using Formula 4.

you fly at least 4–6 times per year on the same airline — THEN a co-branded miles card may deliver the highest reward value, but only after confirming the mile-to-₹ conversion for the routes you actually book.

your Formula 4 effective reward rate is below 0.5% after all fees — THEN check whether an annual fee waiver applies at your annual spend level, or consider switching to a card with a lower fee structure.

your monthly eligible spend is under ₹10,000 — THEN a premium rewards card with a high annual fee is unlikely to recover its cost in reward value at typical card earn rates.

milestone benefits are the main reason you want a card — THEN verify that your natural monthly spend will reach the threshold without additional purchases before factoring those benefits into your decision.

you can pay your full outstanding balance every billing cycle — THEN do not optimise for rewards at all. Interest charges will consistently exceed any reward earned.

Common Mistakes to Avoid

Assuming 1 Point Equals ₹1

Most Indian credit card reward points are worth ₹0.25 to ₹0.50 for cashback redemption — not ₹1.

This assumption leads cardholders to overestimate accumulated value and make redemption decisions based on inflated numbers.

Check the redemption catalogue or rewards portal to confirm exact point value before deciding when or how to redeem.

Ignoring Redemption Fees and GST

Some cards charge a flat fee at the time of redemption, with GST applied on top.

On small redemptions, this fee can consume 20–30% of gross reward value — for example, a ₹99 redemption fee on ₹300 gross reward reduces your net gain to ₹201 before GST is added.

Always calculate net reward value using Formula 3, and check your statement for redemption charges. Our guide on how to read your statement explains exactly where these charges appear.

Including Excluded Spend in Formula 1

Fuel, rent, wallet loads and government payments do not earn reward points on most cards.

Including them in your eligible spend figure inflates your estimated points earned and makes your effective reward rate appear higher than it actually is.

Use only confirmed eligible spend in Formula 1. Verify exclusions in your card’s MITC.

Redeeming for Merchandise Without Checking Cashback Value

Merchandise redemptions typically carry the lowest point value in the catalogue.

A product listed in the rewards store for 8,000 points may deliver ₹0.20 per point, while the same 8,000 points could give ₹0.25 per point as cashback — a ₹400 difference for the same accumulated balance.

Compare point value across all available redemption options before confirming any redemption.

Letting Points Expire

Many cards impose an expiry window of 1 to 3 years from the date of earning.

Expired points have zero ₹ value regardless of how many you accumulated. Set a calendar reminder before the expiry date and redeem proactively rather than waiting to build a larger balance.

Counting Milestone Benefits Before Reaching the Threshold

Premium cards often advertise attractive milestone rewards at high annual spend levels — but these only apply if your natural spending reaches that threshold.

Spending more than you need to in order to unlock a milestone reward typically costs more than the reward is worth. Calculate whether your normal spend pattern reaches the threshold before including milestone benefits in your reward estimate.

When This May Not Be the Right Choice

You carry an unpaid balance and pay interest. Credit card interest rates are among the highest of any consumer loan in India, as referenced in RBI’s credit card guidelines. Even one month of unpaid balance generates interest that can wipe out several months of reward accumulation. Read our guide on card interest charges before focusing on reward optimisation.

Your annual fee exceeds realistic annual reward value. If your card charges ₹2,000 per year and your effective reward rate on typical monthly spend is 0.2%, you need to charge over ₹83,000 per month just to break even — which most salaried cardholders cannot do.

Rewards are changing your spending behaviour. If you are buying things you do not need or eating at more expensive restaurants in order to earn points, rewards are costing you money, not saving it.

You cannot reliably track expiry dates, caps and category exclusions. Rewards programmes are deliberately complex. If managing them adds confusion rather than value, a simpler financial product or a plain lifetime-free card may serve you better.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card reward rates, point values, redemption fees, caps, exclusions and annual fee waiver conditions are set by individual card issuers and can change with each product revision or RBI regulatory update. There is no single government-published table of credit card reward rates.

- Your card’s MITC (Most Important Terms and Conditions) — available on your bank or NBFC’s official website. This document governs all reward rules for your specific card.

- Your card’s rewards portal or mobile app — for current point balance, expiry dates, redemption value per option and any applicable fees.

- Your monthly credit card statement — to confirm reward credits, redemption charges and any fee adjustments applied in a given billing cycle.

- RBI (Reserve Bank of India) — rbi.org.in — for credit card regulatory directions, customer protection guidelines and billing grievance procedures.

- NPCI — npci.org.in — for guidelines relevant to card network transactions and UPI-linked card products.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Compare effective reward rate, not headline multiplier. A “10X points” card may deliver a 0.4% effective reward rate while a plain “1% cashback” card delivers exactly 1% — run Formula 4 on both before deciding which card is actually better for your spend pattern.

- Redeem before expiry, not when you have “enough.” There is no advantage in holding a large unredeemed balance. A redemption worth ₹200 this month is worth more than ₹0 after expiry next quarter.

- Use the right card per category without increasing spend. If one card earns higher points on dining and another on groceries, use each card only for its strong category. Do not spend more on dining just to earn more points.

- Track annual fee recovery as a separate line item. Run Formula 4 twice — once including the annual fee share and once without it. If rewards do not recover the fee even in a good month, pursue a fee waiver or switch to a card with a lower fee.

- Recheck your card’s reward terms every few months. Banks can and do reduce point values, lower category caps or add exclusions mid-year without prominent communication. A card that was excellent for dining last year may now be average for the same spend.

- Never split redemptions into small transactions to avoid minimum thresholds. Repeated redemption fees on small amounts will cost more in aggregate than a single well-timed larger redemption.

Frequently Asked Questions

How do I calculate the ₹ value of my credit card reward points?

Multiply your points balance by the point value for your chosen redemption type. For example, 1,000 points at ₹0.25 per point = ₹250 gross value. Then subtract any redemption fee and GST charged by your card. Use the four-formula model in this article — including annual fee monthly share — to find the true net ₹ value and your effective reward rate.

Are air miles better than cashback for Indian credit cardholders?

Miles can deliver higher per-unit ₹ value than cashback, but only if you fly frequently enough to use them before they expire. If you travel on a specific airline at least 4–6 times per year, a co-branded miles card can outperform a cashback card. If your travel is infrequent or unpredictable, cashback is more reliable — it has no blackout dates, no minimum booking requirements and no expiry risk.

What is a good effective reward rate for a credit card in India?

An effective reward rate of 1% or more — after annual fees, redemption fees and GST — is considered reasonable for a standard rewards card. Rates below 0.5% after all deductions suggest the card’s fee structure may not justify its rewards for your spending level. These are examples only — verify current rates with individual card issuers, as reward structures change regularly.

Do credit card reward points expire in India?

Yes — most cards impose an expiry on accumulated points, typically 1 to 3 years from the date of earning. Some premium cards offer non-expiring points, but this is less common. Check your card’s MITC or the rewards portal for your exact expiry policy. Expired points cannot be reinstated and carry zero ₹ value.

Are credit card reward points taxable in India?

For personal use, cashback and reward redemptions are generally not treated as taxable income under typical consumer scenarios. However, if rewards are linked to business expenses or reimbursements, the tax treatment may differ. This is a nuanced area — consult a qualified tax professional or verify with the Income Tax Department at incometax.gov.in for your specific situation.

Should I pay an annual fee for a rewards credit card?

Only if your realistic annual net reward value — calculated using Formula 4 multiplied by 12 — exceeds the annual fee. If rewards do not recover the fee at your natural spending level, look for an annual fee waiver based on your annual spend threshold, or consider a lifetime-free card that earns lower but consistent rewards without a fee to recover.

Can I calculate rewards on EMI transactions?

Not always. Many cards exclude transactions that have been converted to EMI from earning reward points — either the original transaction earns no points once converted, or subsequent EMI instalments do not accumulate points. Check your card’s MITC for the exact rule, as it varies by bank and card type.

Is there a universal credit card rewards calculator that covers all Indian cards?

No — each card has its own spend blocks, point values, caps, exclusions and fees, so no single calculator can cover all products accurately. The four-formula model in this article gives you a universal structure that you apply to any card by substituting your card’s specific inputs from the official MITC and rewards portal. That is the most reliable approach available.

Final Verdict

A credit card rewards points calculator is not about finding the “best” card — it is about finding the honest ₹ value of the card you hold or are comparing. Cashback is the easiest reward to value and the most reliable option for beginners. Reward points and miles can deliver higher value, but only after accounting for redemption type, fees, GST, caps, exclusions and expiry risk.

The four-formula model in this article gives you a consistent way to calculate your effective reward rate on any card. Run it on your current card before assuming the headline multiplier reflects your actual return. And remember: no reward structure makes financial sense if you are paying credit card interest on an unpaid balance. Billing discipline comes before reward optimisation — always.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.