If you use a credit card for everyday shopping, travel or EMIs, you have probably wondered: am I damaging my CIBIL score every time I swipe? Understanding how credit cards affect CIBIL score is less complicated than most people think — it depends almost entirely on how you use the card, not on the card itself.

A credit card is one of the few financial products that can actively build your credit profile when managed well, or quietly erode it when misused. Repayment history, how much of your available limit you spend each month, how long your account has been open, new card applications and settlement history all feed directly into your credit information report — the document every lender reviews before approving a loan.

This guide breaks down each factor in plain language, with specific Indian salary examples, so you know exactly what helps, what hurts and what to watch.

Quick Answer: How Credit Cards Affect CIBIL Score

how credit cards affect CIBIL score depends mainly on repayment behaviour, credit utilisation, credit age, hard enquiries and settlement history. Paying the full bill on time and keeping ₹25,000 usage on a ₹1,00,000 limit can support your score; missed payments, high usage and settlements can hurt it.

Key Takeaways

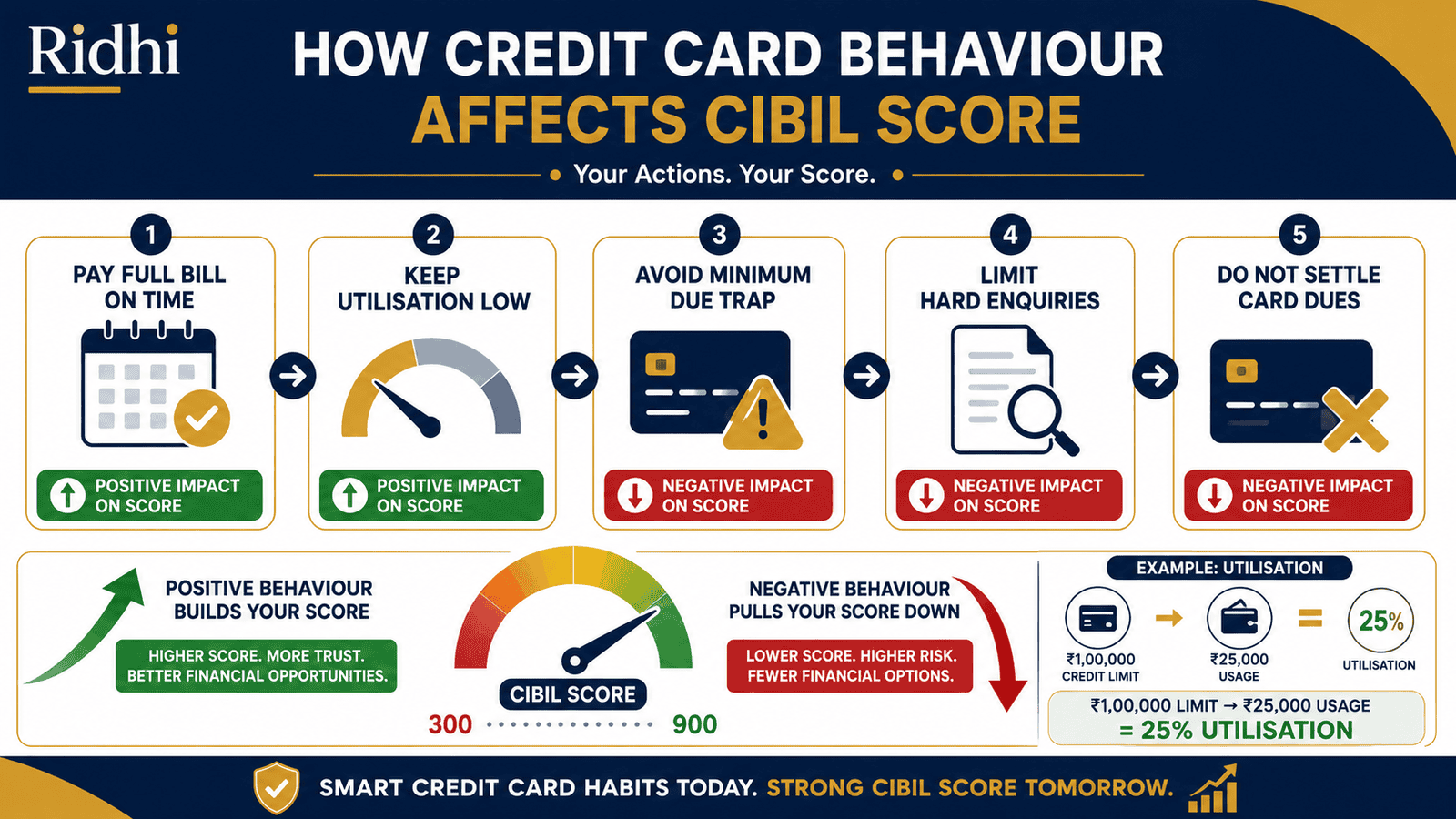

- Paying the full outstanding amount — not just the minimum due — by the due date every month is the single most positive credit card behaviour for your CIBIL score.

- Keeping your credit card usage below 30% of your total available limit (e.g., ₹30,000 on a ₹1,00,000 limit) is generally considered a healthier signal to lenders than consistently high utilisation.

- The minimum amount due is not the same as clearing your bill — paying only the minimum keeps revolving interest compounding and does not protect your credit profile the way full payment does.

- A settlement remark or write-off on your credit report can stay visible to lenders for years and seriously damage your eligibility for home loans and personal loans.

- Every new credit card application triggers a hard enquiry on your report — multiple applications within a few months can signal credit dependency to lenders reviewing your file.

- Closing your oldest well-managed card removes its credit limit from your total available credit, which can raise your utilisation percentage and reduce your account history length over time.

Key Facts at a Glance

| Credit Card Behaviour | Likely CIBIL Impact | What You Should Do |

|---|---|---|

| Full payment on time every month | Positive | Set autopay to total amount due before due date |

| Missed or delayed payment | Negative | Pay before the due date; even one late entry matters |

| Using 25–30% of credit limit | Positive signal | Track spending three to four days before statement date |

| Using 80–100% of credit limit | Negative signal | Reduce spending or request a limit increase from issuer |

| Paying only minimum due repeatedly | Risky | Target total amount due every billing cycle |

| New credit card application | Temporary / Neutral | Apply only when genuinely needed; space applications out |

| Closing an old credit card | Can reduce score | Think before closing your oldest active account |

| Settlement or write-off | Seriously negative | Avoid; clear dues through full payment wherever possible |

Exact score movement is not guaranteed and depends on your overall credit profile and bureau methodology. Source: TransUnion CIBIL — cibil.com

How Credit Cards Affect CIBIL Score: The Key Factors

Payment History — The Biggest Factor

Your payment history is the most heavily weighted element in your credit information report. Every time you pay your credit card bill on time and in full, that behaviour is reported to TransUnion CIBIL and other bureaus by your card issuer. A consistent record of timely full payments builds what lenders call a low days-past-due profile — meaning your accounts rarely, if ever, show overdue balances.

Missing a payment — even by a few days — can trigger a negative entry on your report. The impact is not always immediate in terms of visible score movement, but lenders pulling your report see the entry clearly. Payments that remain unpaid beyond 90 days past due carry a significantly more damaging effect on how lenders perceive your creditworthiness.

Paying the minimum amount due each month keeps your account technically active but does not mean you have cleared your bill. The remaining balance continues to accrue interest, your utilisation stays elevated, and your credit information report reflects a persistent revolving balance. This distinction matters enormously — and is one of the most common misconceptions among first-time card users.

Credit Utilisation — Your Spending Relative to Your Limit

Credit utilisation measures how much of your available credit limit you are using at any point. If your card has a ₹1,00,000 limit and your current outstanding is ₹25,000, your utilisation is 25%. This is generally considered a healthy level. If your outstanding is ₹85,000, your utilisation is 85% — and that can signal financial stress to lenders reviewing your report.

A key point many readers miss: utilisation is calculated across all your credit cards combined, not just on one card. If you hold two cards — one with a ₹50,000 limit and one with a ₹1,00,000 limit — your total available credit is ₹1,50,000. If your combined outstanding is ₹1,10,000, your combined utilisation is approximately 73%, which is high regardless of how it is spread across the two cards. For a detailed breakdown of how this works, read our guide on credit utilisation ratio.

The simplest approach: spend what you can comfortably repay in full, and do not treat your credit limit as a monthly spending budget.

Credit Account Age — Why Older Is Often Better

Your credit history length — how long your accounts have been open and actively managed — contributes to your overall CIBIL profile. A credit card account that has been open, active and well-managed for three or four years carries more positive weight in your credit report than a new account opened six months ago.

This is why closing your oldest card is rarely a straightforward decision. It does not erase historical data immediately, but over time it reduces your active credit age and removes that card’s limit from your total available credit. Understanding what qualifies as a good CIBIL score helps you see why a longer, cleaner history consistently supports a stronger borrowing profile.

Hard Enquiries — Every Application Leaves a Trace

Each time you apply for a new credit card — or any loan — the lender submits a hard enquiry to the credit bureau to review your report. A single enquiry has limited effect. However, applying for three or four cards within a few months creates a cluster of hard enquiries that can signal to lenders that you are actively seeking credit, which raises questions about financial stability.

If you are planning a home loan or large personal loan application within the next six to twelve months, avoid unnecessary credit card applications in that window. The temporary dip from a hard enquiry is minor in isolation; the pattern across multiple enquiries is what lenders notice.

Settlement and Write-Off — The Most Lasting Damage

If you cannot repay your card outstanding in full and negotiate a settlement with the bank — paying less than the full amount owed — the bank reports this as “settled” rather than “closed” on your credit report. A settlement remark stays visible on your report for several years and is one of the first negative signals a lender checks when reviewing a loan application.

A write-off — where the bank classifies your account as a bad debt after extended non-payment — is even more serious. Both outcomes are difficult to recover from quickly and can block access to home loans, personal loans and new credit cards for extended periods. According to TransUnion CIBIL (cibil.com), these entries are standard components of a credit information report reviewed by lenders.

Real Example: Two Colleagues, Two Credit Profiles

Rohan, 29, is an IT professional in Pune earning ₹85,000 per month. He uses his ₹1,00,000-limit credit card for groceries, fuel and annual subscriptions — total monthly spending is usually between ₹22,000 and ₹27,000. He pays the full total amount due every month, three days before the due date. His utilisation stays consistently around 25%. Over two years, his credit information report shows clean payment history and low utilisation — exactly the profile a lender wants to see before approving a home loan.

Vikram, 31, is a software engineer in Bengaluru earning ₹82,000 per month. He also has a ₹1,00,000-limit card but spends ₹88,000 in a busy travel month and pays only the minimum due — roughly ₹4,400. The remaining ₹83,600 revolves at card interest rates. Three months later, he misses a payment entirely because his salary credit was delayed by two days. His credit report now reflects high utilisation, a revolving balance and a missed payment — three separate negative signals stacking against each other in the same report.

Same income bracket. Vastly different credit profiles. Understanding how billing cycle timing and salary dates interact can help you plan payments and avoid exactly this situation.

How to Calculate Your Credit Utilisation

Credit Utilisation (%) = (Total Outstanding Balance ÷ Total Credit Limit) × 100

Using Rohan’s profile: his outstanding is ₹25,000 on a ₹1,00,000 limit.

₹25,000 ÷ ₹1,00,000 × 100 = 25% utilisation — generally considered a healthy level.

Using Vikram’s profile: his outstanding is ₹88,000 on a ₹1,00,000 limit.

₹88,000 ÷ ₹1,00,000 × 100 = 88% utilisation — this can signal heavy credit dependency to a lender.

Now consider a reader with two cards: Card 1 has a ₹75,000 limit with ₹60,000 outstanding. Card 2 has a ₹1,00,000 limit with ₹20,000 outstanding. Total outstanding: ₹80,000. Total limit: ₹1,75,000. Combined utilisation: ₹80,000 ÷ ₹1,75,000 × 100 = approximately 45.7% — higher than it appears when looking at either card in isolation.

| Scenario | Key Figures | Utilisation |

|---|---|---|

| Rohan (controlled spender) | ₹25,000 outstanding on ₹1,00,000 limit | 25% |

| Vikram (high spender) | ₹88,000 outstanding on ₹1,00,000 limit | 88% |

| Two-card reader | ₹80,000 outstanding on ₹1,75,000 total limit | ~45.7% |

These figures are illustrative. To see how unpaid card balances grow with interest over time, use our credit card interest calculator. For a deeper look at what utilisation percentage means for your borrowing profile, read our guide on credit utilisation ratio.

Comparison: Helpful, Risky and Damaging Credit Card Behaviours

| Behaviour | Impact | What to Do Instead |

|---|---|---|

| Full on-time payment, moderate utilisation (under 30%), long well-managed account history | Helpful | Continue this pattern consistently across billing cycles |

| High utilisation (60%+), frequent EMI conversions increasing revolving balance, multiple card applications within a few months | Risky | Reduce spending, space applications at least six months apart |

| Missed payment, settled account, written-off balance, account referred to collections | Damaging | Pay dues in full; contact lender before defaulting if in financial distress |

How to Decide What’s Right for You

you can pay your full card outstanding every month without stretching your budget — THEN use your card freely for planned expenses and let the consistent payment history work in your favour.

your monthly card spending regularly exceeds 50% of your total credit limit — THEN consider requesting a limit increase from your issuer, or splitting spending across two cards to keep combined utilisation at a healthier level.

you are planning a home loan or large personal loan application within the next 6–12 months — THEN avoid applying for any new credit cards in that window, since each application adds a hard enquiry that lenders will see.

you are unsure whether you are paying the total amount due or just the minimum — THEN read your card statement carefully before making each payment. Our guide on how to read a credit card statement walks you through every line, including where total due and minimum due are shown.

you are considering closing a credit card account — THEN check first whether it is your oldest card and whether closure will meaningfully raise your combined utilisation before deciding.

your income is stable enough to guarantee full payment each month — do not rely on minimum due payments to manage your card bills. The revolving interest compounds quickly and the outstanding balance can grow faster than most people expect.

Common Mistakes to Avoid

Paying Only the Minimum Amount Due Month After Month

Many cardholders see the minimum due — often a small percentage of the outstanding balance — and assume paying it keeps everything in order.

Technically, it prevents a missed-payment entry for that cycle. But the remaining balance continues to accrue interest at card rates, your utilisation stays elevated, and your credit information report reflects a persistent revolving balance that lenders notice. Read more about why the minimum due trap is a real financial risk before treating minimum payment as a habit.

Always target the total amount due wherever your cash flow allows.

Treating Your Credit Limit as a Monthly Income

A ₹1,00,000 credit limit does not mean you should spend ₹1,00,000 every month.

Consistently maxing out your card — even if you pay it back in full — tells lenders that you are heavily dependent on credit. This can affect your credit profile over time and reduce your perceived repayment capacity when applying for a home loan or personal loan.

Keep usage well below your available limit. The lower your utilisation, the better the signal.

Missing the Due Date by Even a Few Days

A payment that arrives three or five days late still creates a days-past-due entry visible on your credit report.

According to RBI guidelines, card issuers are required to report payment status to credit bureaus. So delays — even short ones — do get recorded. Set autopay for the total amount due, or a phone reminder at least five days before the due date. Verify current reporting requirements and card terms at rbi.org.in and your issuer’s Most Important Terms and Conditions (MITC) document.

Card charges, interest rates and minimum due calculation methods vary by issuer and can change — always check your MITC for your specific card.

Taking Cash Advances Without Understanding the Cost

Credit card cash advances attract fees and interest from the day of withdrawal — there is no interest-free period as with regular purchases.

Beyond the direct financial cost, heavy cash advance usage can indicate cash-flow stress on your credit report. Use cash advances only in genuine emergencies and repay as quickly as possible.

Closing Your Oldest Card Without Checking the Impact

If your oldest credit card carries no annual fee — or a fee you can get waived — keeping it open and lightly used often makes more financial sense than closing it.

Closure removes that card’s limit from your total available credit, raising your combined utilisation instantly. Over time, it also reduces the average age of your credit accounts. If the card carries a fee you want to avoid, ask the issuer about a downgrade to a no-fee variant before closing outright.

Applying for Multiple New Cards in a Short Period

Each new card application triggers a hard enquiry on your credit report. Two or three applications within two months create a cluster of enquiries that is clearly visible to any lender reviewing your file.

It can look like you are seeking credit urgently — which raises questions about financial stability. Space applications at least six months apart, and apply only when a card genuinely adds value to your regular spending or travel pattern.

When This May Not Be the Right Choice

Credit card use carries real risk when your income is irregular or project-based. Missing a payment during a lean month creates a negative entry that can outlast the cash-flow gap itself by years.

If you are already carrying high-interest personal loan debt or an existing revolving card balance, adding another credit line may worsen your debt-to-income position rather than build your credit profile.

If you are planning a major loan application — home loan, car loan — within the next three to six months, applying for new cards or increasing card activity in that window can add hard enquiries and raise utilisation at exactly the wrong time.

If a previous card account on your credit report shows a settlement or write-off remark, focus on clearing all current dues and reviewing your full credit report before taking on new credit.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card terms, interest rates, fee structures and payment reporting practices are set by individual card issuers and governed by RBI guidelines. These can and do change — sometimes without prominent notice to existing cardholders. Verify current rules from the following official sources before acting on any figure or claim:

- Reserve Bank of India — rbi.org.in (credit card regulations, customer protection guidelines, digital lending rules, complaint escalation)

- TransUnion CIBIL — cibil.com (credit report access, score methodology overview, dispute and correction process)

- Your card issuer’s official website — locate the Most Important Terms and Conditions (MITC) document for your specific card to check fees, interest rates and payment reporting practices

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Set autopay to the total amount due — not the minimum — before your very first billing cycle closes on any new card. Changing this default later is harder once the minimum-due habit has formed.

- Check your total card outstanding three to four days before the statement date, not just on the payment due date. If your balance is unusually high that month, a part-payment before statement generation can reduce the utilisation figure your issuer reports to the bureau for that cycle.

- If your oldest credit card carries no annual fee or one that can be waived, keep it open and active. Even one small transaction every few months — a utility bill or a subscription — keeps the account from going dormant.

- Space new credit card applications at least six months apart. A cluster of hard enquiries in a short window is a visible flag to any lender reviewing your credit information report, even if each individual application seemed justified at the time.

- Request a free credit report from TransUnion CIBIL (cibil.com) at least once a year and check for wrong entries, accounts you did not open, or dues that were cleared but still show as outstanding.

- If your score has already taken damage from missed payments, high utilisation or a settlement, read our practical guide on how to improve your score — it covers the recovery steps that can support gradual improvement over six to twelve months of consistent behaviour.

Frequently Asked Questions

Does using a credit card reduce my CIBIL score?

Not automatically. Using a credit card responsibly — staying within a moderate utilisation range and paying the full bill on time — can have a positive effect on your credit profile over time. The card itself does not reduce your score; your repayment behaviour and utilisation pattern determine the direction of the impact.

Does paying the full credit card bill every month improve my CIBIL score?

Consistent full and timely payment is one of the strongest positive signals in a credit report. Over time, a clean payment record with no days-past-due entries is what lenders and credit bureaus treat as evidence of responsible credit management. The improvement is gradual — typically visible over six to twelve months of clean behaviour.

Does paying only the minimum due affect my CIBIL score?

Paying the minimum due prevents a missed-payment entry for that cycle, but it does not clear your balance. The remaining outstanding continues to accrue interest at card rates, your utilisation remains elevated, and your credit information report reflects an ongoing revolving balance. Lenders reviewing your report can see this pattern over multiple cycles.

Does closing a credit card reduce my CIBIL score?

It can. Closing a card removes its limit from your total available credit, which raises your utilisation percentage immediately. If the card being closed is your oldest account, you also remove its contribution to your credit history length over time. The effect varies depending on your overall profile, but closing your oldest card without thinking through these consequences is generally not advisable.

How many credit cards are safe for CIBIL score purposes?

There is no single safe number. Two or three cards managed well — moderate utilisation, full on-time payments — is typically better than one poorly managed card. The risk with multiple cards is behavioural: more available credit can lead to higher combined spending and higher combined utilisation if not tracked carefully across all cards together.

Does credit card settlement affect future loans?

Yes, significantly. A settlement remark on your credit report — meaning you paid less than the full outstanding amount and the lender agreed to close the account — is visible to all future lenders pulling your report. It is one of the more serious negative signals and can affect eligibility for home loans, personal loans and new credit cards for several years following the settlement.

What is a hard enquiry and how does it affect my credit score?

A hard enquiry is a formal credit check initiated when you apply for a credit card or loan. Each enquiry is recorded on your credit report. One enquiry in isolation has a limited effect. Multiple enquiries within a short window — three applications over two months, for example — can be read as a sign of financial stress or aggressive credit-seeking by lenders reviewing your file.

Can I build my CIBIL score using a credit card?

Yes, over time. A credit card with consistent full payment, low utilisation and no missed payments contributes to a healthier credit profile. The improvement is gradual and depends on your broader credit mix and existing history. There is no shortcut — the score reflects behaviour sustained over several months, not a single billing cycle.

What happens if I miss one credit card payment?

One missed payment creates a days-past-due entry on your credit report that lenders can see when reviewing your file. The impact on your visible score varies by bureau methodology and your overall profile, but the entry itself is recorded. If the payment remains unpaid beyond 90 days, the negative effect becomes significantly more serious and the lender may classify the account differently in your report.

Final Verdict

A credit card is not a threat to your CIBIL score by default. It is one of the most effective tools available for building a strong credit profile — when used with consistent payment discipline. Pay the full outstanding amount on time each month, keep your combined utilisation well below your total available limit, and treat settlement as a last resort rather than a convenient exit from debt.

The damage comes from treating the credit limit as income, paying only the minimum due month after month, missing payment dates and applying for cards repeatedly without clear purpose. None of these outcomes are inevitable — they are all behavioural patterns that can be corrected with the right habits in place.

How credit cards affect CIBIL score ultimately comes down to one question: are you in control of the card, or is the card controlling your cash flow? Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.