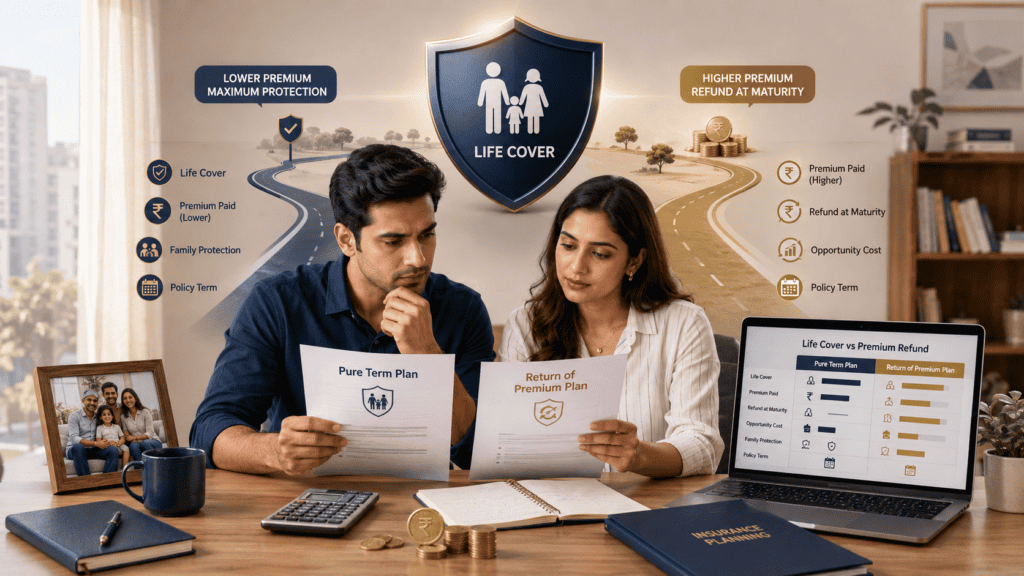

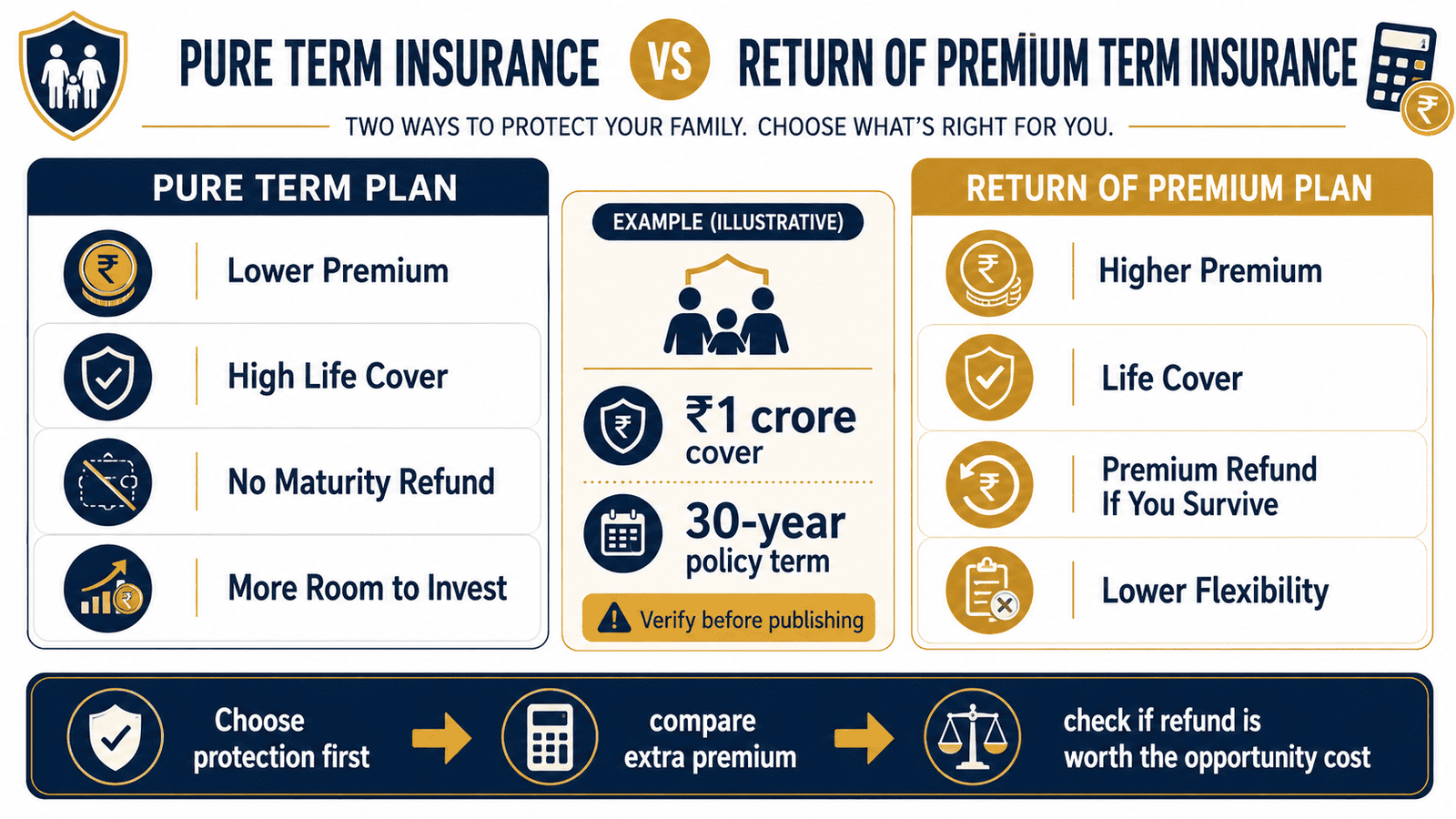

Most Indian salaried families want a term plan where premiums come back — and that is the exact promise of return of premium term insurance. A TROP plan provides standard life cover with one added feature: if you survive the full policy term, the insurer refunds eligible premiums you paid.

The real question is whether that refund justifies the higher annual premium. This article compares TROP with pure term insurance across premium cost, refund value, tax treatment, and opportunity cost. All premium figures in this article are illustrative only. Actual premiums vary by age, health, gender, smoking status, cover amount, policy term, riders chosen, and insurer. Insurance is a subject matter of solicitation. Please read the policy document carefully before purchasing.

Quick Answer: Return of Premium Term Insurance

Return of premium term insurance is a term plan that refunds eligible premiums if you survive the policy term, but it usually costs more than pure term insurance. For a ₹1 crore cover, compare the extra premium, refund value, and opportunity cost before choosing.

Key Takeaways

- TROP provides standard life cover and may refund eligible base premiums if you survive the full term — GST, rider charges, and modal loading are typically excluded from the refund amount.

- Pure term insurance gives the same death benefit at a lower annual premium, with no maturity refund on survival.

- For a 34-year-old buying ₹1 crore cover for 30 years, illustrative TROP premiums can be roughly double the cost of a comparable pure term plan — a difference of approximately ₹13,000 per year.

- That extra ₹13,000/year, if invested separately at 7% p.a. compounded for 30 years, could grow to approximately ₹12.3 lakh — roughly double the illustrative TROP refund amount.

- Section 80C tax deduction on life insurance premiums is subject to current income tax law and individual eligibility — tax benefit alone should not drive an insurance purchase decision.

- Never reduce your sum assured to make TROP premiums affordable — your family’s financial protection must come before the refund feature.

- Policy wording controls what is actually refunded: always obtain and read the benefit illustration before purchasing any TROP plan.

Comparison: Pure Term Insurance vs Return of Premium Term Insurance

The table below sets out the key structural differences. Exact premiums and refund amounts depend on your insurer, age, cover, policy term, and plan wording. According to IRDAI guidelines, insurers must provide a benefit illustration before policy issuance — always request one. For additional context on how term plans compare with savings-linked insurance, see our guide to term versus endowment policies.

| Parameter | Pure Term Insurance | Return of Premium (TROP) |

|---|---|---|

| Annual premium (illustrative — ₹1 cr cover, 30-yr term, age 34, male, non-smoker) | ~₹12,000/year | ~₹25,000/year |

| Death benefit | Full sum assured paid to nominee | Full sum assured paid to nominee |

| Maturity or survival benefit | None | Eligible base premiums refunded on survival (see policy document) |

| GST and rider charges refunded | Not applicable | Typically not refunded |

| Annual cost | Lower premium | Higher premium |

| If you stop paying early | Policy lapses after grace period; no refund | Policy lapses or surrenders; partial or zero refund depending on plan terms |

| Best suited for | Buyers who want maximum life cover at the lowest possible annual cost | Buyers who want a refund on survival, can afford the higher premium without reducing sum assured, and will hold the policy to full term |

Key Facts at a Glance

| Fact | Detail |

|---|---|

| Product type | Term life insurance with maturity or survival benefit |

| Death benefit | Sum assured paid to nominee if policyholder dies during the policy term |

| Maturity benefit | Eligible base premiums may be refunded if policyholder survives the full policy term |

| What is typically not refunded | GST, rider premiums, modal loading charges, underwriting extras — varies by plan |

| Regulator | IRDAI — irdai.gov.in |

| Tax deduction on premium | Possible under Section 80C, subject to current income tax rules and individual eligibility |

| Maturity benefit taxability | Subject to current income tax rules — verify at incometax.gov.in before purchase |

| Key document to request | Insurer’s official benefit illustration showing exact refund amount and exclusions |

How Return of Premium Term Insurance Actually Works

A standard term plan is a pure risk product. You pay premiums for a fixed number of years. If you die during that period, the insurer pays the sum assured to your nominee. If you survive, the policy ends — no payment, no refund. That is the pure risk cover model.

Return of premium term insurance keeps this structure intact and adds one benefit: if you survive the complete policy term, the insurer returns eligible premiums as a maturity benefit. This is sometimes described in policy documents as a “premium refund clause” or “survival benefit.” The operative word is eligible — and what qualifies varies significantly by plan and insurer.

What TROP Is Not

TROP is not an endowment plan. It does not accumulate cash value over time, pay bonuses, or function as an investment. The maturity refund is a return of eligible base premiums — not a return on investment, not a growth product. If you are thinking of it as a way to earn back more than you paid in, that is not how it works.

TROP is also not a ULIP. There is no market-linked fund, no asset allocation, and no possibility of market-linked gains. It is a term plan with a specific contractual refund at maturity — regulated by IRDAI at irdai.gov.in.

How the Death Benefit Works

The death benefit in TROP functions identically to pure term insurance. If a policyholder buying a ₹1 crore TROP plan dies in year 14 of a 30-year term, the nominee receives ₹1 crore. The maturity refund feature is irrelevant in that scenario — it only applies if the policyholder survives all 30 years and the policy remains in force throughout.

Riders and the Refund Calculation

Riders — critical illness cover, accidental death benefit, waiver of premium — add to your annual premium. Most TROP plans exclude rider premiums from the refund calculation. If you add riders without checking the policy document, you may pay a higher annual outgo while the refund only covers the base component. This gap between total premium paid and actual refund received is one of the most common surprises buyers encounter.

Understanding what term insurance basics are designed to do — provide pure financial protection, not savings — is the most important foundation before comparing TROP with pure term insurance.

Real Example: Rahul’s Choice in Pune

Rahul is 34, works as an IT project manager in Pune, and earns ₹18 lakh per year. He has a spouse and a 3-year-old child. He wants ₹1 crore life cover for a 30-year term. He has been quoted two illustrative sets of premiums.

Pure term plan (illustrative): ₹12,000 per year, inclusive of all charges. His family gets ₹1 crore if he dies during the term. He receives nothing if he survives to 64.

TROP plan (illustrative): ₹25,000 per year, inclusive of all charges. His family gets the same ₹1 crore if he dies. If Rahul survives to 64, he receives approximately ₹6,00,000 in eligible base premiums (GST component excluded from refund, illustrative figure only).

Rahul’s first instinct is that ₹6,00,000 back after 30 years sounds very attractive. But when he works out the extra premium — ₹13,000 per year — and multiplies by 30 years, he has paid ₹3,90,000 extra for TROP compared to pure term. The refund of ₹6,00,000 appears to be a ₹2,10,000 gain. But that calculation ignores the opportunity cost of committing ₹13,000 more every year for 30 years.

The key insight: the right comparison is not refund versus extra premium paid — it is refund versus what that extra premium could have grown to if deployed differently over 30 years.

How to Calculate Whether the Refund Is Worth the Extra Premium

Extra Annual Premium = TROP Annual Premium − Pure Term Annual Premium

Total Extra Paid = Extra Annual Premium × Policy Term (years)

Opportunity Cost = Future Value of Extra Premium invested separately at your expected return

Using Rahul’s illustrative figures (all figures are for illustration only — verify current premiums from insurer quotes before deciding):

- Extra premium per year: ₹25,000 − ₹12,000 = ₹13,000

- Total extra paid over 30 years: ₹13,000 × 30 = ₹3,90,000

- Future value of ₹13,000/year at 7% p.a. compounded for 30 years: approximately ₹12,30,000

- Illustrative TROP maturity refund (base premiums only, ex-GST): approximately ₹6,00,000

| Scenario | Key Figures (Illustrative Only) | Result |

|---|---|---|

| TROP maturity refund received on survival | Base premiums only, GST excluded | ~₹6,00,000 |

| Total extra premium paid for TROP vs pure term | ₹13,000/year × 30 years | ₹3,90,000 |

| Same extra premium invested separately at 7% p.a. compounded | ₹13,000/year for 30 years | ~₹12,30,000 |

These numbers are illustrative. Actual premiums, refund amounts, investment returns, and tax treatment will differ based on your plan, insurer, age, and applicable rules at the time of purchase. The framework is what matters: always compare the refund against the opportunity cost of the extra premium, not just against the nominal extra paid.

How to Decide What’s Right for You

your family’s financial protection is the first priority and you are working within a budget — THEN choose pure term insurance and maximise your sum assured. Use our right cover amount guide to calculate the cover your family actually needs before comparing plan types.

you can comfortably afford the higher TROP premium without reducing your sum assured — THEN TROP may provide the refund discipline you value, provided you fully understand what is and is not included in the eligible refund amount.

you are likely to stop or surrender the policy before the full 30-year term ends — THEN TROP is almost certainly unsuitable; most plans pay little or no refund on early surrender, and you will have paid higher premiums throughout the years the policy was active.

your income is stable and you invest surplus money consistently — THEN a pure term plan with the premium difference invested separately may build significantly more wealth than the TROP maturity refund over the same period.

you know from experience that you do not invest surplus money consistently — THEN TROP’s forced-refund structure may work as a useful psychological anchor, even if it is not the most financially efficient option available.

you are buying insurance primarily to claim a Section 80C tax deduction — THEN reconsider the decision entirely. Tax benefit is incidental to insurance; purchasing a more expensive plan to save tax rarely makes financial sense.

you have verified the insurer’s claim settlement record and the policy exclusions are acceptable to you — THEN do not commit to any plan, TROP or pure term, until you have reviewed those details. A refund at maturity is irrelevant if your family cannot successfully claim the death benefit when they need it most.

Common Mistakes to Avoid

Reducing sum assured to make TROP premiums affordable

Choosing ₹50 lakh cover on TROP because ₹1 crore TROP is too expensive defeats the entire purpose of term insurance.

Your family’s financial security depends on an adequate sum assured — not the refund feature. If TROP is unaffordable at the cover level your family needs, pure term is the right answer, not a smaller TROP policy.

Always calculate how much cover your family needs first, then select the plan type — never the other way around.

Assuming all premiums including GST are refunded

Most TROP plans refund eligible base premiums only. GST, rider premiums, modal loading charges, and any underwriting extra are typically excluded.

For a plan where the total annual outgo is ₹25,000 inclusive of 18% GST, the base premium is approximately ₹21,186. Over 30 years, the difference between total paid (₹7,50,000) and eligible refund (approximately ₹6,35,000 on base only) can be ₹1,15,000 or more — a meaningful gap that buyers often do not anticipate.

Request the exact refund amount in writing from the benefit illustration, not an approximate percentage, before signing anything.

Treating the premium refund as investment profit

Receiving ₹6,00,000 after paying premiums for 30 years is not the same as earning a return on that money.

In real terms, the purchasing power of ₹6,00,000 received 30 years from now will be lower than ₹6,00,000 today due to inflation. The TROP maturity benefit is a return of capital — not a return on capital. If investment growth is your objective, evaluate dedicated investment instruments separately.

Conflating insurance refunds with investment returns is one of the most common and costly mental accounting errors in Indian personal finance.

Ignoring claim settlement quality in favour of refund features

Selecting a TROP plan primarily because of the maturity refund while overlooking an insurer’s claim settlement history is a serious misjudgement. The primary purpose of term insurance is a reliable death benefit — that must work when your family needs it most.

Review the insurer’s claim settlement ratio as part of your evaluation — but treat it as one factor among several, not the only filter. Insurer financial strength, claim process transparency, and policy exclusions matter equally.

Buying TROP only for the Section 80C tax deduction

Life insurance premiums may qualify for a Section 80C deduction subject to current income tax law and individual eligibility. But purchasing a more expensive plan to claim a tax deduction is rarely a sound financial decision.

Insurance is for protection. Tax benefit is a secondary consideration. This is especially relevant under the new tax regime, where Section 80C deductions may not apply at all.

Not reading the surrender and lapse conditions before committing

If your financial situation changes and you need to stop paying premiums midway through a 30-year term, TROP may return no refund at all — or only a partial surrender value after a specified minimum premium-paying period.

Understand exactly when refund eligibility kicks in, what the surrender value schedule looks like, and what happens at lapse before signing a long-term premium commitment.

When This May Not Be the Right Choice

TROP may not be suitable if your budget requires you to reduce your sum assured to make the higher premium manageable. A ₹50 lakh TROP policy is weaker financial protection than a ₹1 crore pure term plan — the refund does not compensate for inadequate cover when your family actually needs the death benefit.

It is also less suitable if you are comfortable investing the premium difference yourself. The pure term plan combined with a separate, disciplined investment approach — explored in detail in our term plus mutual fund comparison — has the potential to build significantly more than the TROP maturity refund over the same 30-year period, depending on your investment choices and consistency.

TROP is also a poor fit if there is any realistic chance you will not hold the policy to full term. The refund only activates on survival through the complete policy term with premiums paid throughout. An early exit typically yields little to nothing from the refund feature after paying higher premiums for years.

Finally, if you expect investment-grade returns from the maturity benefit, TROP will disappoint. It returns eligible base premiums — nothing more.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Key sources to check before purchasing any return of premium term insurance plan:

- IRDAI — irdai.gov.in: India’s insurance regulator. Verify registered insurer status, benefit illustration requirements, policy grievance processes, and any regulatory guidelines on TROP product structures.

- Income Tax Department — incometax.gov.in: Current rules on Section 80C deductions for life insurance premiums, maturity benefit taxability, and applicable conditions under the old and new tax regimes.

Before purchasing: obtain the benefit illustration, confirm the exact rupee refund amount, identify which premium components qualify for refund, review exclusions, and read the full policy document including surrender conditions and lapse rules. Verify with your insurer whether GST, rider premiums, and modal loading are included or excluded from the refund.

For an overview of tax saving options available beyond insurance, our 80C deduction guide covers EPF, PPF, ELSS, and home loan principal — so you can evaluate insurance as one part of your overall tax planning, not its foundation.

Expert Tips

- When comparing pure term and TROP, request quotes for identical parameters from the same insurer: same age, same cover amount, same policy term, same riders. This isolates the exact cost of the refund feature and prevents comparison errors caused by different assumptions.

- Ask the insurer for the refund amount in absolute rupees from the benefit illustration — not as “return of total premiums paid” in percentage terms. The rupee figure, net of GST and riders, is the only number that tells you what you will actually receive.

- Before adding any rider to a TROP plan, confirm whether that rider’s premium is included in or excluded from the refund calculation. Riders commonly excluded from refund silently reduce your effective refund-to-premium ratio without appearing on the basic product brochure.

- Keep nominee details current — update after marriage, a child’s birth, or any major family change. The death benefit is only as effective as the nominee information on record at the time of claim.

- Evaluate the insurer’s financial strength and claim settlement track record alongside the refund feature. A maturity refund at age 64 is meaningless if the insurer has difficulty processing death claims when your family needs them in year 10.

- IRDAI at irdai.gov.in maintains a list of registered insurers and publishes annual insurance statistics including claim data. Check these before committing to any insurer, regardless of the plan type.

Frequently Asked Questions

Is return of premium term insurance worth it?

It depends on your priorities and financial situation. TROP provides life cover and returns eligible base premiums on survival — but the annual premium is substantially higher than pure term insurance offering identical cover. If the higher premium forces you to reduce your sum assured, TROP is not worth it. If you can maintain adequate cover at the higher premium and genuinely value the refund structure over 30 years, it can be a reasonable choice — provided you have compared the extra premium against its opportunity cost.

Is TROP better than pure term insurance?

Not categorically. Pure term insurance provides maximum cover at the lowest premium — that is the primary purpose of a term plan. TROP adds a refund feature at a higher price. Whether that trade-off is “better” depends on your budget, your ability to keep the policy to full term, and whether you would systematically invest the premium difference if you chose pure term. There is no universal answer that applies to all buyers.

Do I get all my premiums back in TROP?

No. Most TROP plans refund eligible base premiums only. GST paid on each premium installment is typically not refunded. Rider premiums, modal loading charges applied for monthly or quarterly payment modes, and any underwriting extras are also commonly excluded. Your actual refund will be lower than the sum of all premiums you paid. Always confirm the exact refund amount from the insurer’s benefit illustration — not the product brochure — before purchase.

Is GST refunded in a TROP plan?

Generally, no. The GST component of your insurance premium is typically not included in the TROP maturity refund. The refund usually covers the base premium component only. Verify this specifically in your insurer’s policy document and benefit illustration, as terms vary by plan and insurer.

Does TROP qualify for a Section 80C tax deduction?

Life insurance premiums including TROP premiums may qualify for a deduction under Section 80C of the Income Tax Act, subject to current tax law, applicable conditions, premium-to-sum-assured ratio requirements, and individual eligibility. The deduction limit and conditions also depend on whether you opt for the old or new tax regime. Verify the current position at incometax.gov.in or consult a qualified tax professional before purchasing.

What happens if I stop paying TROP premiums midway?

If you stop paying premiums, the TROP policy typically lapses after the grace period. Many plans offer a paid-up status or a surrender value after a specified number of completed premium years — but this varies significantly by plan. In most cases, stopping premiums before the full term means you partially or fully forfeit the maturity refund while having paid higher premiums throughout the active period. Review the exact surrender value schedule and lapse conditions in the policy document before committing to a long-term premium schedule.

Is TROP better than an endowment plan?

TROP and endowment plans are structurally different. Endowment plans combine life insurance with a savings component and typically offer a maturity benefit plus bonuses, but at premiums significantly higher than either pure term or TROP. TROP only returns eligible base premiums — it does not build a savings corpus or pay bonuses. For buyers whose primary need is affordable life cover, both TROP and endowment plans cost more than pure term insurance. Your choice should depend on the specific policy features, what the benefit illustration shows, and your family’s protection needs.

Can I surrender a TROP plan before the full term?

Most TROP plans allow surrender, but the surrender value before a specified threshold — often three to five completed premium years — may be minimal or zero. Surrendering early typically means no maturity refund benefit and a possible financial loss relative to total premiums paid. If there is any realistic chance you will not hold the policy for the full term, TROP carries a higher financial risk than pure term insurance, which has no such lock-in dependency.

Can I get the TROP death benefit and the premium refund?

No. TROP provides either the death benefit or the maturity refund — not both. If the policyholder dies during the policy term, the nominee receives the sum assured. If the policyholder survives the full term, the eligible premium refund is paid. These are mutually exclusive outcomes, not cumulative benefits.

Is the TROP maturity amount taxable?

The taxability of the TROP maturity benefit depends on current income tax rules and the specific conditions of your policy, including the premium-to-sum-assured ratio. Tax treatment can change with each Budget. Verify the current position at incometax.gov.in or consult a qualified tax advisor before purchasing — do not rely on what applied in a previous financial year.

Final Verdict

Return of premium term insurance can suit buyers who value the refund structure, have a stable long-term income, and can comfortably afford the higher premium without reducing their family’s sum assured. If paying roughly double the pure term premium is manageable and you are confident you will hold the policy for the full 30 years, TROP offers a structured way to combine death benefit protection with a refund at maturity.

For most salaried families, however, pure term insurance at adequate cover remains the more financially practical choice. The extra premium committed to TROP — when compared against its opportunity cost over 30 years — typically outweighs the maturity refund by a significant margin. The refund is a feature, not a reason to compromise on the sum assured your family actually needs. Adequate protection comes first. Before choosing any plan, use the term insurance cover calculator to confirm the cover level your family requires. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Priya Nambiar writes about insurance concepts for Indian families, salaried employees, self-employed professionals, and first-time policy buyers. Her content focuses on helping readers understand coverage, exclusions, claim conditions, premiums, riders, and policy documents before buying or renewing insurance.

She covers topics such as term insurance, health insurance, family floater plans, riders, critical illness cover, employer insurance vs personal insurance, waiting periods, exclusions, deductibles, co-payment, no-claim bonus, claim settlement, premium comparison, renewal rules, and tax benefits linked to insurance.

Priya’s writing is careful, consumer-focused, and policy-document oriented. She explains why insurance should be understood as financial protection, not just a tax-saving tool or investment substitute. Her articles encourage readers to compare coverage, understand limitations, and ask better questions before buying a policy. Premiums, exclusions, claim rules, and benefits vary by insurer, age, health, sum insured, and product type. Insurance is a subject matter of solicitation, and readers should read the official policy document carefully before purchasing.