Comparing joining bonus vs retention bonus feels straightforward until the offer letter is in front of you. The numbers look identical — ₹2,00,000 from a new company to join, ₹2,00,000 from your current employer to stay. They are not the same thing.

A bonus of ₹2,00,000 on paper can arrive in your bank account as ₹1,40,000 or less — depending on your income tax slab, how your employer handles TDS under Section 192, and whether a clawback clause kicks in if you leave early. Bonus timing matters. Recovery clauses matter. The month TDS is deducted matters.

This article explains how each bonus works in India, how they are taxed under the Income Tax Act, what they mean for your salary slip and Form 16, and what to check before you say yes to either.

Quick Answer: Joining Bonus vs Retention Bonus

A joining bonus is one-time money paid by a new employer for joining their company. A retention bonus is paid by your current employer for staying till a future date. In India, both are typically treated as taxable salary income when paid. A ₹2,00,000 bonus can face TDS based on your tax slab and employer payroll rules.

Key Takeaways

- Both joining bonus and retention bonus are treated as taxable salary income in India — TDS is deducted by the employer under Section 192 of the Income Tax Act in the month the bonus is paid.

- A ₹2,00,000 bonus paid to someone in the 30% tax bracket can result in TDS of approximately ₹60,000 — reducing the in-hand payout to around ₹1,40,000 in the payment month.

- Joining bonuses typically carry a clawback clause: if you leave within 6 to 12 months, the employer may recover the full gross amount — even though you already paid tax on it.

- Retention bonuses are conditional — if you leave before the specified payout date, the bonus may be partially or fully forfeited, and you may receive nothing at all.

- A bonus shown in your CTC is often a one-time payment made on a specific date — not extra monthly salary. It does not increase your regular monthly in-hand pay across 12 months.

- The correct figure to compare is your estimated net in-hand bonus after TDS, not the gross amount shown in the offer letter or retention agreement.

- Tax treatment, TDS calculation method, and recovery terms vary by employer — always get the full details in writing before accepting either bonus.

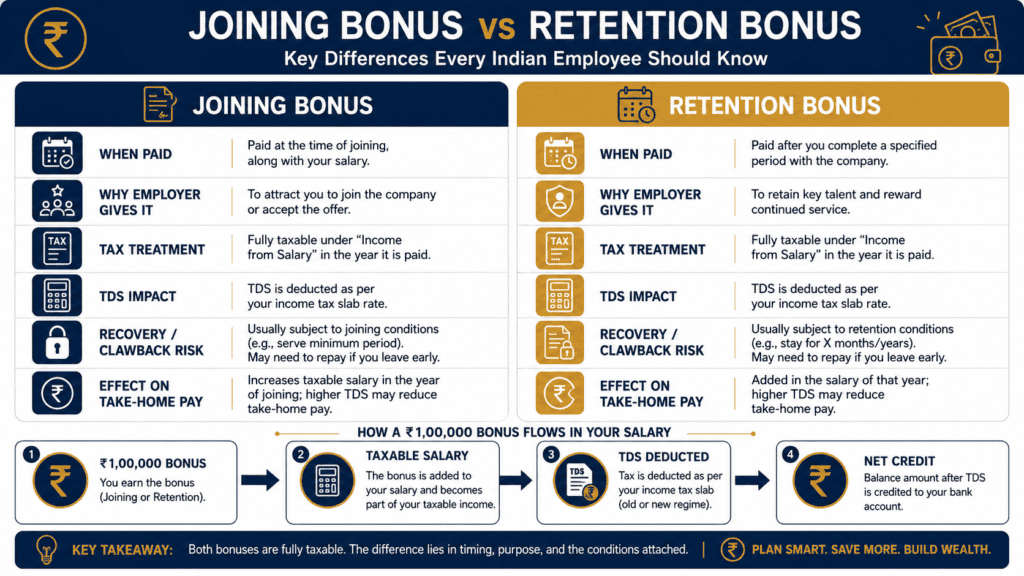

Joining Bonus vs Retention Bonus: Full Comparison

| Parameter | Joining Bonus | Retention Bonus |

|---|---|---|

| Purpose | Incentive to join the new company | Incentive to stay with the current employer |

| Who Pays It | New employer | Current employer |

| Typical Timing | On joining date or first payroll cycle | After completing a minimum service period — usually 1 to 3 years |

| Tax Treatment | Taxable as salary income in the year received | Taxable as salary income in the year received |

| TDS Deduction | Yes — deducted under Section 192 based on annualised income estimate | Yes — deducted under Section 192 based on annualised income estimate |

| Recovery or Forfeiture Risk | Clawback — gross amount may be recovered if you leave early | Forfeiture — bonus not paid if service period is not completed |

| CTC Inclusion | Often included as a separate one-time CTC component | May or may not be included in CTC — varies by employer |

| Best For | Job switchers who need immediate cash support | Existing employees committed to staying for the required period |

To understand how conditional pay components like bonus sit within your overall salary structure, read about variable pay in CTC.

Key Facts at a Glance

| Detail | Joining Bonus | Retention Bonus |

|---|---|---|

| Also Called | Sign-on bonus, onboarding bonus | Loyalty bonus, stay bonus |

| Tax Category | Salary income under Income Tax Act | Salary income under Income Tax Act |

| TDS Section | Section 192 | Section 192 |

| Reported In | Salary slip and Form 16 (Part B) | Salary slip and Form 16 (Part B) |

| Recovery or Forfeiture Clause | Yes — typically a 6 to 24 month minimum service condition | Yes — forfeited if minimum period is not completed before payout date |

| Effect on Monthly In-Hand | One-time credit in the payment month only — not a recurring increase | One-time credit in the payment month only — not a recurring increase |

What Is a Joining Bonus and How Does It Work in India?

A joining bonus — also called a sign-on bonus — is a one-time payment made by a new employer when you accept their offer and join the company. It is most common in technology, consulting, BFSI, and e-commerce, where employers compete for specific skill sets and need to attract candidates quickly.

The primary purpose is to compensate you for what you leave behind at your previous company — unvested ESOPs, a deferred annual bonus that you will not receive because you are leaving before the payout cycle, or other conditional pay you are forgoing by switching jobs. The new company is, in effect, writing a cheque to cover that loss.

Joining bonuses almost always come with a clawback clause. If you leave before the minimum service period — typically 6 months to 12 months, sometimes longer — your employer is contractually entitled to recover the full gross amount. This is a detail that many employees notice only when they decide to resign and discover the deduction in their full and final settlement.

Your salary slip for the joining month will reflect the bonus as a separate line item. The TDS deducted in that month may be substantially higher than your regular months because of how Section 192 works. See where a joining bonus and TDS appear on a typical Indian payslip: salary slip components.

What Is a Retention Bonus and How Is It Different?

A retention bonus — also called a loyalty bonus or stay bonus — is paid by your current employer to keep you from leaving. It is typically offered during periods of organisational uncertainty, before a merger or acquisition, during a restructuring, or when an employer knows a high-value employee has received competing offers.

Unlike a joining bonus, a retention bonus is almost always conditional on a future date. You must complete a defined service period — often 1 to 3 years — before the payment is made. If you leave before that date, the bonus is forfeited entirely in most cases. Some employers structure phased payouts: 50% after 12 months and 50% after 24 months, which reduces the risk of losing everything if your plans change. Either way, the money does not arrive until the condition is met.

A retention bonus is not a salary hike. It is a one-time payment. It does not increase your monthly fixed pay, your PF contribution base, or your gratuity eligibility. Employees who accept a retention bonus in place of an overdue salary revision often find themselves underpaid for the next two years — with a one-time payment that provides temporary relief but no structural improvement.

Bonus in CTC vs What You Actually Receive

This is where most confusion begins. Many employees see a bonus in their CTC and assume it means extra monthly salary. It does not. CTC — Cost to Company — is your employer’s total annual cost of employing you. It includes basic salary, allowances, employer PF contributions, and any one-time components like a joining or retention bonus.

When a ₹2,00,000 bonus appears in your CTC, it means a single lump-sum payment of ₹2,00,000 on a specific date — not ₹16,667 added to your monthly account every month. Your gross bonus, your taxable bonus, and your net in-hand payout are three different numbers. Understanding the difference matters before comparing any two offers side by side. Learn more about why salary structures can look larger than what actually reaches your account: gross and net salary.

How the Income Tax Act Treats Bonus Income

Both joining bonus and retention bonus are treated as salary income under the Income Tax Act. According to the Income Tax Department (incometax.gov.in), salary income includes wages, fees, commissions, perquisites, and any other payment received from an employer in the course of employment. A one-time bonus received under an employment contract falls squarely within this definition.

TDS is deducted under Section 192 of the Income Tax Act. When a bonus is paid, your employer typically annualises the total income for the year — that is, they add the bonus to your projected annual salary and calculate the estimated total tax. They then subtract whatever TDS has already been collected in earlier months and deduct the balance in the bonus month. This is why your in-hand pay can appear sharply lower in the bonus month even though your total annual tax has not changed — it has simply been collected earlier.

The bonus amount and TDS deducted will appear in your Form 16 Part B for the financial year. Both are part of your total taxable salary income when you file your Income Tax Return.

Real Example: Rohit Weighs Two Identical Numbers

Rohit, 29, works as a software engineer in Bengaluru with a current CTC of ₹18 LPA. He has received a new offer from a product company that includes a ₹2,00,000 joining bonus — payable with his first salary. His current employer has countered with a ₹2,00,000 retention bonus, payable after 18 months of continued service.

On paper, the numbers are identical. In practice, they are not.

The joining bonus from the new company arrives in Month 1. His employer will annualise his total projected income — approximately ₹20,00,000 including the bonus — and collect a higher TDS in that month to account for the bump. Depending on regime and deductions, the net credit to his account after TDS could be significantly lower than ₹2,00,000.

The retention bonus from his current employer will only be paid if Rohit stays for the full 18 months. If he resigns on Month 15, he forfeits the entire ₹2,00,000. Meanwhile, the joining bonus from the new company has a 12-month clawback clause — if Rohit leaves the new company within a year, he must return the full gross amount, regardless of how much tax he has already paid on it.

The real comparison is not ₹2,00,000 vs ₹2,00,000. It is net payout after TDS, weighed against the career risk and recovery exposure of each option over a realistic timeline.

How to Calculate Your Real In-Hand Bonus

You can estimate your net bonus payout with a straightforward calculation once you know your projected annual taxable income for the year.

Net In-Hand Bonus = Gross Bonus − TDS on Bonus

TDS on Bonus ≈ Marginal Tax Rate × Gross Bonus (based on employer’s annualised income calculation)

The employer adds the bonus to your projected annual salary, calculates total estimated tax for the year, subtracts TDS already collected in prior months, and deducts the balance in the bonus month. The result is a larger-than-usual TDS deduction in that single payroll cycle.

| Annual Income Including Bonus | Gross Bonus | Approximate Net In-Hand Bonus |

|---|---|---|

| Up to ₹7,00,000 (new regime) | ₹2,00,000 | Potentially nil TDS if total income stays within rebate limit |

| ₹10,00,000–₹15,00,000 | ₹2,00,000 | Approximately ₹1,60,000–₹1,70,000 after TDS |

| Above ₹15,00,000 | ₹2,00,000 | Approximately ₹1,40,000–₹1,50,000 after TDS |

These figures are approximate estimates for illustration. Actual TDS depends on your total annual income, chosen tax regime, eligible deductions, surcharge, and health and education cess. Use our monthly in-hand pay calculator to estimate your specific net payout based on your actual salary and bonus figures.

How to Decide What’s Right for You

you are switching jobs and need immediate cash to cover relocation expenses, a loan EMI gap, or the loss of your previous employer’s bonus cycle — then a joining bonus gives you that cash upfront and may justify the move even when the base salary increase is modest.

you are stable in your current role and your employer is offering a retention bonus with a written agreement, a clear payout date, and a minimum service period you are genuinely comfortable committing to — then the retention bonus can be financially sound.

the joining bonus carries a clawback clause of 12 months or more and you are not fully certain about the new role, team, or employer stability — then the recovery risk outweighs the immediate gain, particularly in a market where job changes can follow quickly.

the retention bonus requires 2 to 3 years of continued service but the role offers no salary revision, no career growth path, or a work environment you find difficult — then the financial cost of staying may exceed what the bonus is worth.

the bonus in either offer is a large share of the headline CTC but the fixed monthly salary is low — then your regular in-hand pay may not cover day-to-day expenses, and the one-time bonus will only provide temporary relief before the shortfall returns.

you have the clawback or forfeiture clause in writing, the payout date confirmed, and the estimated net payout after TDS in hand — do not accept either bonus on verbal assurances. The figure in the offer letter is never the figure that reaches your account.

Common Mistakes to Avoid

Treating the Gross Bonus as In-Hand Pay

Many employees compare offers using the gross bonus figure and assume that is what will be credited to their account.

At a marginal rate of 30%, TDS alone can reduce a ₹2,00,000 bonus to approximately ₹1,40,000 in hand. If you have planned a large expense — a loan repayment, a home deposit, travel — around the bonus amount, you may find yourself short in the payment month.

Always ask your HR or payroll team for an illustration of the estimated net payout after TDS before finalising your decision.

Ignoring the Clawback or Lock-In Clause

A clawback clause allows your employer to recover the full gross joining bonus if you resign before the specified period — often 6 to 12 months, sometimes longer.

If you leave at Month 8 on a 12-month clawback agreement, you may be asked to return ₹2,00,000 in full — even though you received only ₹1,40,000 after TDS. The tax you paid does not reduce the amount you owe. The employer recovers the gross sum, not the net amount.

Read the clause carefully. If the wording is vague — “amount recoverable at management’s discretion” — ask for written clarification before signing the offer letter.

Not Accounting for the TDS Spike in the Bonus Month

When a bonus is paid, the employer annualises total income and deducts the proportionate tax in a single month. This means the TDS deduction in the bonus month can be two to three times higher than your regular monthly TDS.

This is how Section 192 operates — it is not an error by your payroll team. However, if your employer uses an overstated income projection, excess TDS may be deducted. You can recover this as a refund when you file your ITR. Verify the TDS amount reported in your Form 26AS or Annual Information Statement after filing.

Overlooking the Full and Final Settlement Impact

If you resign while a joining bonus recovery clause is active, your employer can deduct the recoverable amount from your full and final settlement. This can reduce or eliminate your last month’s salary, any outstanding leave encashment, and other payables due to you at the time of exit.

Understanding what happens to payouts and deductions when you leave a job mid-year is important: notice period buyout.

Comparing CTC Instead of Average Monthly Net Cash Flow

A company offering ₹18 LPA with a ₹2,00,000 joining bonus does not give you a higher effective monthly income than a company offering ₹20 LPA with no bonus. The bonus is one-time. The ₹2 LPA salary difference is recurring — every month, for as long as you stay.

Calculate your average monthly in-hand over 12 months for each offer — including the bonus month and the eleven months without it — before drawing a comparison.

Accepting a Retention Bonus Without a Written Agreement

Some employers communicate a retention bonus verbally — in a meeting, over a call — without issuing a written retention letter. Without a signed document confirming the amount, payout date, and service condition, you have no enforceable claim to the payment.

If your employer is serious about retaining you, they will commit it in writing. Insist on a signed retention letter before adjusting any career decision around the promised amount.

When This May Not Be the Right Choice

A joining bonus may not be worth accepting if the clawback period is longer than 18 months and you are not fully certain about the new role or employer. Leaving before the clawback period ends can mean returning an amount larger than you actually received after tax.

A retention bonus may not be the right choice if it is being offered in place of a salary revision that is clearly overdue. A one-time payment that keeps you locked in at below-market pay for the next two years does not improve your financial position — it delays the problem.

Either bonus is a weak trade-off if the fixed monthly salary is structurally low. One-time bonuses do not increase your PF contribution base, gratuity eligibility, or monthly cash flow for the months when no bonus is paid.

If the retention letter uses vague language — “subject to management discretion” or “performance-linked” — without specific amounts and dates, the payout may not materialise even if you complete the service period. If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Bonus income from employment — whether a joining bonus or a retention bonus — is classified as salary income under the Income Tax Act. TDS on salary is governed by Section 192 and administered by the Income Tax Department.

- Income Tax Department (incometax.gov.in): For salary income classification, TDS rules under Section 192, Form 16 format, ITR filing procedures, and current income tax slabs and regimes applicable for the relevant assessment year.

- EPFO (epfindia.gov.in): If your employer includes any bonus component within your PF-eligible salary under their payroll policy, verify applicable PF contribution rules. Joining and retention bonuses are generally not part of the PF-eligible basic salary unless specifically structured that way by the employer.

- Your Employer’s HR or Payroll Team: For your specific TDS calculation method, the month your bonus will be paid, and the exact terms of the clawback or retention agreement.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before accepting a joining bonus, ask the company’s HR or payroll team to share an illustrative net payout — the estimated amount after TDS — so you know exactly what will be credited to your account. Do not rely on the gross figure in the offer letter to plan your finances.

- Ask your new employer explicitly: “Is this bonus recoverable, for how long, and under what conditions?” Get the answer in writing. A 12-month clawback on a new company means you are financially locked in even if the role turns out to be a poor fit.

- Check how the bonus will appear in your Form 16 at the end of the year. This matters for your ITR filing — especially if you join mid-year and have two employers in the same financial year, which affects how total salary and TDS are reported.

- If you are deciding between the old and new tax regime, factor in the bonus before calculating. A large one-time bonus can push your total annual income into a higher slab and change which regime saves you more tax. Use our income tax calculator to compare both regimes using your actual salary and bonus numbers before accepting any offer.

- Keep a copy of your offer letter, joining bonus clause, salary slip for the bonus month, and the signed retention agreement — even after the clawback or lock-in period ends. These documents are critical if any dispute arises during full and final settlement.

- If your employer deducts excess TDS in the bonus month, do not panic — it is not a loss. You can claim the overpaid amount as a refund when you file your ITR. Cross-check the TDS reported in your Form 26AS or Annual Information Statement on incometax.gov.in after the financial year ends to confirm it matches what was deducted.

Frequently Asked Questions

Is a joining bonus taxable in India?

Yes. A joining bonus is treated as salary income under the Income Tax Act and is fully taxable in the financial year it is received. Your employer deducts TDS under Section 192 in the payment month, and the amount appears in Form 16 Part B for that year. It is included in your total taxable salary when you file your ITR.

Is a retention bonus taxable in India?

Yes. A retention bonus is also treated as salary income and taxed in the year it is received. The tax treatment is identical to a joining bonus — TDS is deducted by the employer under Section 192 when the payment is made, and the amount is reported in Form 16.

Is TDS deducted on a bonus?

Yes. Both joining and retention bonuses attract TDS under Section 192 of the Income Tax Act. When the bonus is paid, the employer typically annualises your total income for the year — adding the bonus to your projected annual salary — and collects the proportionate estimated tax in that single month. This is why TDS can appear higher than usual in the bonus month.

What happens if a joining bonus is recovered by the employer?

If you leave before the clawback period ends, the employer can recover the full gross joining bonus — not the net amount you received after TDS. You may be able to claim tax relief on the repaid amount in the year of repayment under specific Income Tax provisions, but the treatment depends on how the repayment is structured and the applicable rules for that assessment year. Consult a qualified tax professional for guidance specific to your situation.

Is a bonus part of CTC?

It depends on how the employer structures the offer. Joining bonuses and retention bonuses are sometimes included within the CTC figure and sometimes offered separately. When included in CTC, they inflate the headline annual number without increasing your fixed monthly salary. Always confirm whether any bonus in your CTC is a one-time payment on a specific date or a recurring component, before comparing two offers.

What happens if a retention bonus is forfeited?

If you leave before the required service period ends, the bonus is forfeited — you simply do not receive it. Unlike a clawback (where money is taken back after it is paid), forfeiture means the payment never happens. There are no tax implications for an amount you never received.

Is a joining bonus the same as a sign-on bonus?

Yes. Joining bonus and sign-on bonus refer to the same type of payment — a one-time amount paid by a new employer when you join the company. Both terms are used interchangeably in India, particularly in the technology, consulting, and financial services sectors.

Can I get a refund if my employer deducted excess TDS on my bonus?

Yes. If the TDS deducted in the bonus month exceeds your actual tax liability for the full year — which can happen when the employer uses a higher income estimate for annualisation — you can claim the excess as an income tax refund when you file your ITR. Check your Form 26AS or Annual Information Statement on incometax.gov.in after the year ends to verify the TDS figure reported matches what was actually deducted from your salary.

Which is better — a joining bonus or a retention bonus?

Neither is universally better. A joining bonus suits someone switching jobs who needs immediate cash support and is confident about the new role. A retention bonus suits someone who genuinely plans to stay, where the payout terms are clear, written, and the service condition is realistic. The deciding factors are net payout after TDS, recovery or forfeiture risk, and whether the bonus compensates for a real financial need or career trade-off — not the gross number in the letter.

Final Verdict

Joining bonus vs retention bonus is not a question of which number is larger — it is a question of which option makes more financial sense for your actual situation. A joining bonus delivers cash immediately but ties you to a clawback clause and carries the risk of owing money back if the new role does not work out. A retention bonus rewards loyalty but only pays out if you complete the service period — and only if the terms were agreed in writing from the beginning.

In India, both are taxable salary income. Both attract TDS under Section 192. The net amount that reaches your account is always lower than the gross figure in any offer letter or retention agreement. Compare net payouts, not headlines — and factor in the recovery or forfeiture risk before committing to either.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.