If your salary is ₹25 LPA and you are trying to figure out how much tax you will pay — the honest answer is: it depends. The tax on 25 LPA salary is not a single fixed number. It changes based on whether you choose the new tax regime or the old one, what deductions and exemptions you can claim, how your employer has structured the package, and whether your variable pay, bonus, or PF has been accounted for correctly.

For Financial Year 2025-26 (Assessment Year 2026-27), most salaried employees at this income level are defaulted to the new tax regime — but that may or may not be the right choice for you. This article walks through the calculation step by step for both regimes, connects it to your actual monthly in-hand salary, and shows you where to verify the numbers before filing your ITR. Tax rules apply based on the relevant assessment year, so always confirm current figures from the Income Tax Department at incometax.gov.in.

Quick Answer: Tax on 25 LPA Salary

Tax on 25 LPA salary depends on the regime, deductions and salary structure. Under the FY 2025-26 new regime, a ₹25 lakh salary may have about ₹3.20 lakh tax after standard deduction and cess, while the old regime tax changes significantly based on deductions. Verify all current rates at incometax.gov.in before filing your ITR.

Key Takeaways

- ₹25 LPA CTC is not your taxable income — employer PF, gratuity, and benefits are excluded, and your standard deduction further reduces the taxable figure before any slab rate applies.

- Under the FY 2025-26 new regime, a ₹25 lakh gross salary becomes approximately ₹24,25,000 in taxable income after the ₹75,000 standard deduction.

- Estimated new regime tax on ₹25 LPA is approximately ₹3,19,800 — this includes the 4% health and education cess and assumes salary as the only income source.

- Old regime without additional deductions produces an estimated tax of approximately ₹5,69,400 at this salary — nearly ₹2.5 lakh more than the new regime.

- To make the old regime more tax-efficient than the new regime at ₹25 LPA, you typically need around ₹7–8 lakh or more in total deductions and exemptions — very difficult to achieve for most salaried employees.

- Monthly in-hand salary from ₹25 LPA depends on employer PF, professional tax, variable components, and TDS — not just income tax slab calculation.

- TDS deducted monthly is an advance estimate — your actual final tax is settled only when you file your ITR using Form 16 and AIS data.

Key Facts at a Glance

| Parameter | New Regime (FY 2025-26) | Old Regime (FY 2025-26) |

|---|---|---|

| Gross Annual Salary | ₹25,00,000 | ₹25,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (before other deductions) | ₹24,25,000 | ₹24,50,000 |

| Estimated Tax Before Cess | ₹3,07,500 | ₹5,47,500 |

| Health and Education Cess at 4% | ₹12,300 | ₹21,900 |

| Estimated Total Tax Payable | ₹3,19,800 | ₹5,69,400 |

| Surcharge Applicable | Nil — income below ₹50 lakh | Nil — income below ₹50 lakh |

| Section 87A Rebate | Not applicable — income above ₹12 lakh | Not applicable — income above ₹5 lakh |

All figures assume salary as the only income source and gross salary of ₹25 lakh before employer-level deductions. Verify all rates and limits from incometax.gov.in before filing your ITR.

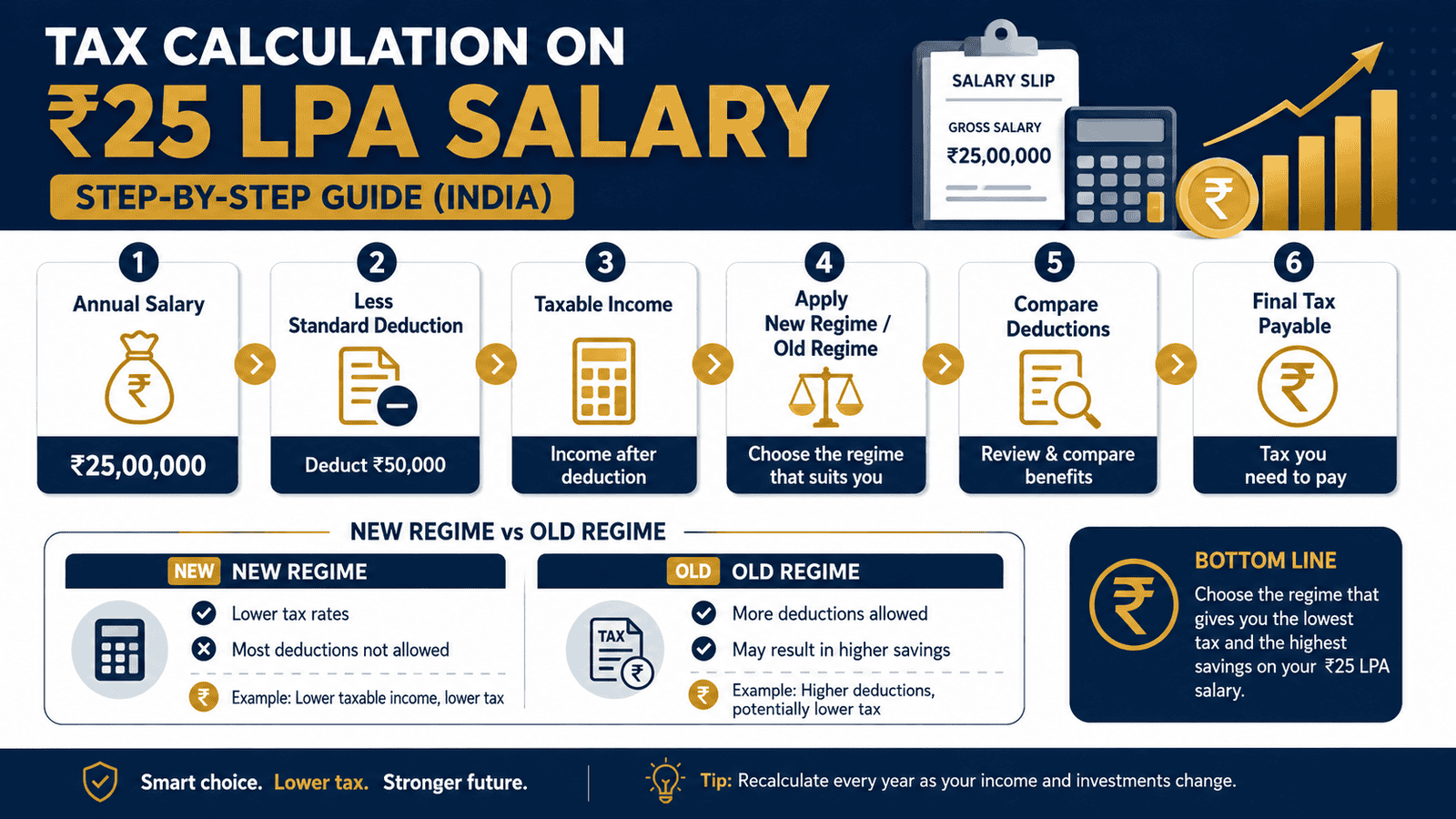

How Tax on 25 LPA Salary Is Actually Calculated

Most salaried employees make one immediate mistake: they assume their ₹25 LPA CTC is what gets taxed. It is not. Your taxable income is your gross salary minus eligible deductions — and the deductions available to you change entirely depending on which tax regime you choose.

Step 1: Start from Gross Salary, Not CTC

Your CTC includes employer’s PF contribution, gratuity accrual, group health insurance premium, and other benefits that never reach your bank account and are not taxable in your hands. For a structured ₹25 LPA package, your gross salary on the salary slip is often ₹23–25 lakh depending on benefits. This article uses ₹25 lakh as gross salary for all examples. The gap between CTC and gross salary matters — and it matters again when you calculate take-home.

Step 2: Subtract the Standard Deduction

Every salaried employee gets a standard deduction automatically — no receipts, no paperwork. Under the FY 2025-26 new regime, this deduction is ₹75,000. Under the old regime, it remains ₹50,000. This directly lowers your taxable salary before any slab rate is applied. Learn how this works in detail: standard deduction meaning.

On a ₹25,00,000 gross salary, your opening taxable income is:

- New regime: ₹25,00,000 − ₹75,000 = ₹24,25,000

- Old regime (before any other deductions): ₹25,00,000 − ₹50,000 = ₹24,50,000

Step 3: Apply Eligible Deductions Under the Old Regime

Under the old regime, you can claim Section 80C investments up to ₹1,50,000 (EPF, PPF, ELSS, LIC, home loan principal), Section 80D health insurance premiums up to ₹25,000 for self and family, HRA exemption if you pay rent, home loan interest under Section 24b up to ₹2,00,000, and NPS contributions under Section 80CCD(1B) up to ₹50,000. Each of these reduces your taxable income — but proof and actual expense are required for every claim.

Under the new regime, most of these deductions are not available. The trade-off is lower slab rates across the board. For a comparison of tax calculations across salary levels, see our guide on 20 LPA salary tax.

Step 4: Apply Tax Slabs to Taxable Income

India’s income tax works on a slab system — each layer of income is taxed at a progressively higher rate. No single flat rate applies to your full taxable income. Under the FY 2025-26 new regime, slabs start at nil for income up to ₹4 lakh, rising through 5%, 10%, 15%, 20%, and 25% bands, and reaching 30% only on income above ₹24 lakh. The old regime reaches the 30% slab much earlier — at income above ₹10 lakh — which is why it produces a much higher tax on ₹25 LPA unless large deductions are in play.

Step 5: Add 4% Health and Education Cess

After calculating income tax on your taxable income, you add 4% health and education cess on the total tax. This is mandatory — not optional and not deductible. On a new regime tax of ₹3,07,500, the cess adds ₹12,300, bringing the final liability to ₹3,19,800. Any calculator that does not show cess separately is giving you an incomplete answer.

Why Your Monthly In-Hand Salary Is Different from What You Expect

Your monthly take-home salary depends on more than income tax. Your employer also deducts employee PF (12% of basic salary — typically ₹1,500–2,500 per month at this salary level), professional tax (varies by state — ₹200 per month in Bengaluru, Hyderabad, and Maharashtra), any group insurance premium contribution, and TDS based on your investment declarations. These cuts happen before you see the salary in your account, and they are why a ₹25 LPA salary rarely translates to ₹2.08 lakh in-hand every month.

Real Example: Rohit’s ₹25 LPA Tax Calculation

Rohit is 32 years old, a senior software engineer at a Bengaluru-based product company earning ₹25 LPA fixed salary with no variable bonus this financial year. His package includes basic pay of ₹12.5 lakh, HRA of ₹5 lakh, special allowance of ₹6 lakh, and employer PF of ₹1.5 lakh. This makes his CTC ₹25 lakh, but his gross taxable salary is approximately ₹23.5 lakh — the employer PF is not taxable in his hands.

For this example, we use ₹25 lakh as gross taxable salary. Rohit opts for the new regime. After the ₹75,000 standard deduction, his taxable income is ₹24,25,000. Applying FY 2025-26 new regime slabs, his estimated tax before cess is ₹3,07,500. After 4% cess (₹12,300), his total estimated income tax is ₹3,19,800 — approximately ₹26,650 per month in TDS.

His actual monthly in-hand would then account for employee PF (approximately ₹1,800/month), professional tax (₹200/month), and group insurance (₹500/month). His estimated monthly take-home sits at roughly ₹1.57–1.62 lakh — not the ₹2.08 lakh that a simple CTC-divided-by-12 calculation would suggest. Understanding this gap is fundamental. CTC versus in hand explains the full breakdown.

How to Calculate Tax on 25 LPA Salary

Income Tax Payable = Tax on Taxable Income as per Applicable Slab Rates + 4% Health and Education Cess

New Regime Calculation — FY 2025-26

Gross salary ₹25,00,000 minus standard deduction ₹75,000 = taxable income ₹24,25,000.

- ₹0 to ₹4,00,000 — Nil = ₹0

- ₹4,00,001 to ₹8,00,000 — 5% on ₹4,00,000 = ₹20,000

- ₹8,00,001 to ₹12,00,000 — 10% on ₹4,00,000 = ₹40,000

- ₹12,00,001 to ₹16,00,000 — 15% on ₹4,00,000 = ₹60,000

- ₹16,00,001 to ₹20,00,000 — 20% on ₹4,00,000 = ₹80,000

- ₹20,00,001 to ₹24,00,000 — 25% on ₹4,00,000 = ₹1,00,000

- ₹24,00,001 to ₹24,25,000 — 30% on ₹25,000 = ₹7,500

Tax before cess: ₹3,07,500. Cess at 4%: ₹12,300. Total new regime tax: ₹3,19,800.

Old Regime Calculation — No Additional Deductions

Gross salary ₹25,00,000 minus standard deduction ₹50,000 = taxable income ₹24,50,000.

- ₹0 to ₹2,50,000 — Nil = ₹0

- ₹2,50,001 to ₹5,00,000 — 5% on ₹2,50,000 = ₹12,500

- ₹5,00,001 to ₹10,00,000 — 20% on ₹5,00,000 = ₹1,00,000

- ₹10,00,001 to ₹24,50,000 — 30% on ₹14,50,000 = ₹4,35,000

Tax before cess: ₹5,47,500. Cess at 4%: ₹21,900. Total old regime tax (no deductions): ₹5,69,400.

| Scenario | Taxable Income | Estimated Total Tax |

|---|---|---|

| New regime — standard deduction only | ₹24,25,000 | ₹3,19,800 |

| Old regime — no additional deductions | ₹24,50,000 | ₹5,69,400 |

| Old regime — with ₹3,00,000 in deductions | ₹21,50,000 | ₹4,75,800 |

For a calculation built around your own salary structure and actual deductions, use our income tax calculator and verify results against incometax.gov.in.

Comparison: New Regime vs Old Regime for ₹25 LPA Salary

| Parameter | New Regime | Old Regime |

|---|---|---|

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (no other deductions) | ₹24,25,000 | ₹24,50,000 |

| Estimated Tax (no other deductions) | ₹3,19,800 | ₹5,69,400 |

| 80C, 80D, HRA, Home Loan Interest | Not available | Available with proof |

| Deductions needed to beat new regime | N/A | ~₹7–8 lakh (very high for most) |

| Complexity of filing | Low | High — all proofs required |

| Best-fit reader at 25 LPA | Employees with limited deductions | HRA claimants with home loan and max 80C |

| When estimate changes | Bonus, ESOP, or other income added | Deductions reduced or disallowed at scrutiny |

Want to see how the tax calculation shifts at the next salary level? Our guide on 30 LPA salary tax shows how crossing ₹30 lakh changes the numbers.

How to Decide What’s Right for You

The new vs old regime decision is a numbers exercise — not a lifestyle preference. Here is how to think through it at ₹25 LPA:

Your total deductions and exemptions under the old regime — 80C, 80D, HRA, home loan interest, NPS — add up to less than ₹5 lakh in a year, the new regime will almost certainly result in lower tax at this salary level.

You are a renter claiming HRA in a metro city, have ₹1.5 lakh in 80C investments, and also pay home loan EMIs — run the actual numbers rather than guessing. With ₹5–6 lakh in total deductions, old regime still produces higher tax, but the gap narrows significantly.

Your employer has defaulted you to the new regime and you have not submitted investment declarations — verify your TDS deductions with HR before March. Switching regimes is allowed at ITR filing time for salaried employees without business income.

You changed jobs mid-year — disclose your previous employer’s income to your current employer, or carry it forward to your ITR. Not doing so leads to shortfall in TDS and interest under Sections 234B and 234C at filing time.

Your salary includes a large joining bonus or ESOP perquisite — this is added to your taxable salary income and may push your total tax significantly higher. Recalculate on the actual gross income, not just fixed CTC.

You have actual receipts and proof for every deduction you plan to claim — do not claim them in your ITR. Unverified deductions attract scrutiny notices, and disallowed claims mean you owe the full tax plus interest.

For a deeper walkthrough comparing both regimes across different salary structures and deduction profiles, read our full guide: new versus old regime.

Common Mistakes to Avoid

Treating CTC as Taxable Income

Many salaried employees open their offer letter and assume the full ₹25 LPA figure is what gets taxed. It is not.

Your CTC includes employer PF (typically ₹1.5–1.8 lakh at this salary), gratuity accrual, group insurance premium, and other benefits that are excluded from your taxable salary. Treating ₹25 lakh as taxable income can inflate your estimated tax by ₹45,000–₹60,000 and cause unnecessary alarm when your actual liability is lower.

Start from your gross salary on your monthly salary slip — not the figure on your appointment letter.

Forgetting the Standard Deduction

Some employees run a back-of-envelope tax calculation directly on gross salary, skipping the standard deduction entirely.

Under the new regime, missing the ₹75,000 standard deduction means calculating tax on ₹75,000 more income than you should. At the 30% slab, that is a ₹22,500 overestimation before cess. Under the old regime, skipping ₹50,000 standard deduction similarly adds ₹15,000 to your estimated tax. The standard deduction is automatic — always apply it first.

If you are using an online tax calculator, confirm it has the standard deduction pre-filled for your chosen regime.

Ignoring the 4% Health and Education Cess

Many quick online calculators display tax before cess as the final figure — this understates your actual liability.

On a new regime tax of ₹3,07,500, the 4% cess adds ₹12,300 — taking total tax to ₹3,19,800. Forgetting cess leads to under-payment of advance tax or TDS shortfall. Always ask whether any calculator output includes cess before using it to verify your payslip TDS deduction.

Look for a line item labelled “health and education cess” — if it is missing from the output, the number is incomplete.

Assuming TDS Equals Your Final Tax

TDS is deducted by your employer based on projections and declarations made at the start of the year — it is an estimate, not a confirmation.

If you received a mid-year bonus, changed jobs, had rental income, or misclaimed a deduction, your actual tax liability at filing time will differ from what was already deducted. This creates either a refund (if TDS was excess) or an additional tax demand with interest (if TDS fell short). Always reconcile TDS with your Form 16 and AIS before filing ITR.

Download Form 26AS from incometax.gov.in and match it against your Form 16 before submitting.

Claiming Deductions Without Actual Proof

Entering deductions in your ITR without supporting documents is a mistake that can cost significantly more than the tax saved.

The Income Tax Department can send scrutiny notices asking for rent receipts, HRA calculation basis, 80C investment statements, insurance premium receipts, and home loan interest certificates. If you cannot produce these, the deduction is disallowed — and you owe the tax you originally avoided, plus interest under Section 234A/B/C and potentially a penalty.

Collect all proofs by March 31 of the financial year and store them for at least six years after the relevant assessment year.

Choosing a Regime Based on General Advice Rather Than Your Own Numbers

Saying “new regime is always better at ₹25 LPA” is broadly true — but not universally so.

A salaried employee with HRA of ₹1.2 lakh, 80C of ₹1.5 lakh, home loan interest of ₹2 lakh, NPS of ₹50,000, and 80D of ₹25,000 has ₹5.45 lakh in deductions. Even this level does not quite flip the regime calculation in favour of old regime — but the gap narrows enough that recalculating every year is worth it.

Use a tax calculator with your actual deductions each April — not last year’s estimate or a blanket recommendation from social media.

When This May Not Be the Right Choice

The tax estimates in this article assume a salaried employee with salary as the sole income source. The numbers here may not reflect your situation if:

- Your income includes capital gains from selling equity, mutual funds, or property — these are taxed at special rates and require a different ITR form entirely.

- Your salary includes large variable pay, an ESOP perquisite, or a joining bonus that pushes total income significantly above ₹25 lakh for the year.

- You have rental income, freelance projects, interest from bonds, or any business income — all of which add to your total taxable income and change the liability.

- You are an NRI, returning NRI, or have foreign income — residential status determines which incomes are taxable in India and under which rules.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax slabs, standard deduction limits, cess rates, surcharge thresholds, Section 87A rebate eligibility, and the rules governing new vs old regime choice are set by the Finance Act and can change with each Union Budget. For FY 2025-26 / AY 2026-27 figures, use only official sources:

- Income Tax Department — incometax.gov.in: Verify current FY 2025-26 tax slabs under both regimes, standard deduction limits, rebate and surcharge rules, and filing requirements. This portal is also where you file your ITR and access Form 26AS and your Annual Information Statement.

- EPFO — epfindia.gov.in: Verify current employer and employee PF contribution rates if you want to calculate your net monthly salary after PF deductions.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Run the regime comparison every April with your actual deductions — not hypothetical ones. Open a tax calculator, enter your real 80C investments, HRA amount, insurance premiums, and home loan interest paid, and compare the final tax under both regimes. The new regime wins at ₹25 LPA for most, but your salary structure may tell a different story.

- If you switched employers during FY 2025-26, inform your new employer of the income earned from your previous employer. Failure to disclose results in under-deduction of TDS, and you will owe the shortfall as self-assessment tax — plus interest under Sections 234B and 234C — when you file.

- Start tax planning in April, not March. If old regime works better for you and you need to build 80C investments, waiting until February compresses your options and forces rushed decisions. NPS contributions, ELSS SIPs, and term insurance can all be set up in April with full-year impact.

- Read your salary slip every month. Identify basic pay, HRA, PF deduction, professional tax, and TDS as separate line items. This gives you a real-time view of in-hand salary and helps you spot any discrepancy in TDS deduction before the financial year ends.

- Download your AIS (Annual Information Statement) from incometax.gov.in at least once before filing. It shows all income, TDS, interest, and other financial transactions linked to your PAN — including data your employer, bank, and broker have reported. Mismatches between your Form 16 and AIS must be resolved before or during filing.

- Keep all deduction proofs — rent receipts, investment account statements, health insurance premium certificates, and home loan interest certificates — for at least six years after the assessment year. The Income Tax Department’s lookback window covers several prior years.

Frequently Asked Questions

How much income tax do I pay on a 25 lakh salary in India?

For FY 2025-26, estimated income tax on a ₹25 lakh salary under the new regime is approximately ₹3,19,800, including 4% health and education cess. Under the old regime without additional deductions, estimated tax is approximately ₹5,69,400. Both figures assume salary income only. Verify current slab rates from incometax.gov.in before filing your ITR.

What is the tax on 25 LPA salary under the new tax regime for FY 2025-26?

Under the FY 2025-26 new regime, ₹25 lakh gross salary minus ₹75,000 standard deduction gives taxable income of ₹24,25,000. Applying current slab rates — including the 30% band for income above ₹24 lakh — the estimated tax before cess is ₹3,07,500. After 4% cess (₹12,300), total estimated tax is ₹3,19,800. No surcharge applies since income is below ₹50 lakh. Verify at incometax.gov.in.

Is the old tax regime better for a 25 LPA salary?

For most salaried employees at ₹25 LPA, the new regime produces lower tax. To make the old regime more tax-efficient, you typically need total deductions of approximately ₹7–8 lakh. Even with maximum 80C (₹1.5L), 80D (₹25K), NPS (₹50K), HRA (₹1.2L), and home loan interest (₹2L), total deductions reach approximately ₹5.45 lakh — still not enough to beat the new regime at this salary. Run actual numbers with your own figures before deciding.

What is my monthly in-hand salary for a 25 LPA package?

Monthly in-hand salary depends on salary structure, TDS, employee PF, professional tax, and variable components. As a rough estimate under the new regime: after TDS (approx ₹26,650/month), employee PF (approx ₹1,800/month), and professional tax (approx ₹200/month), monthly take-home from a ₹25 LPA fixed salary may be approximately ₹1.55–1.65 lakh. This is an estimate — your actual in-hand depends on your specific package and state.

Does Section 87A rebate apply to a 25 LPA salary?

No. Under the FY 2025-26 new regime, the Section 87A rebate applies only if total income is ₹12,00,000 or below. A ₹25 lakh salary is well above this limit. Under the old regime, the rebate applies only up to ₹5,00,000 — also not applicable here. No rebate is available at ₹25 LPA under either regime. Verify current rebate rules at incometax.gov.in.

How much total deduction do I need to make the old regime better than the new regime at 25 LPA?

At ₹25 LPA, the new regime tax is approximately ₹3,19,800. For the old regime tax to match this, your taxable income under the old regime would need to fall to approximately ₹16.5 lakh. After the ₹50,000 standard deduction, that means you need roughly ₹8 lakh in additional deductions from gross salary — which is very difficult for most salaried employees to achieve. The new regime wins at this income level for the majority of readers.

Can I switch from old regime to new regime after submitting investment declarations to my employer?

Yes, but only at the time of filing your ITR. Salaried employees without business income can switch between regimes every year when filing — regardless of what regime was used for TDS deduction during the year. If you switch regime at ITR time, any excess TDS becomes a refund and any shortfall must be paid as self-assessment tax. The switch must happen before the ITR filing deadline.

What happens if my employer deducts less TDS than my actual tax liability at 25 LPA?

If TDS is lower than your actual tax — due to a mid-year job change, undisclosed bonus, or incorrect declarations — you are responsible for the shortfall. Pay the balance as self-assessment tax before filing your ITR. If the shortfall is large, interest under Section 234B (for non-payment of advance tax) may also apply. Always reconcile your Form 16 data with your AIS before finalising your return.

Is Form 16 enough to file ITR for a 25 LPA salary?

Form 16 is your primary document — it gives employer-certified income details and TDS figures. But before filing, also download your AIS and Form 26AS from incometax.gov.in to check if any income, interest, or other TDS has been reported against your PAN from sources beyond your employer. Discrepancies between Form 16 and AIS must be resolved before filing to avoid notices.

How much of my 25 LPA salary is actually exempt from tax?

Under the new regime, only the ₹75,000 standard deduction is automatically exempt — there are no other exemptions. Under the old regime, exemptions depend on your salary structure: HRA exemption (calculated based on rent paid, basic salary, and city), leave travel allowance, and other components may be partially exempt. Your employer typically calculates these at source — check Part B of your Form 16 for the exact exempt amounts applied to your salary.

Final Verdict

For most salaried employees at ₹25 LPA with typical deductions, the tax on 25 LPA salary under the new regime — estimated at ₹3,19,800 for FY 2025-26 — is significantly lower than under the old regime. Unless you have approximately ₹7–8 lakh or more in total eligible deductions and exemptions, the new regime is likely to be more tax-efficient at this salary. The old regime only makes sense for a small subset of ₹25 LPA earners: those with high HRA, home loan interest, maximum 80C usage, NPS contributions, and strong documentation behind every claim.

Before filing, verify all figures with your Form 16 and AIS, use a tax calculator with your actual numbers, and confirm current slab rates and deduction limits directly from incometax.gov.in. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.