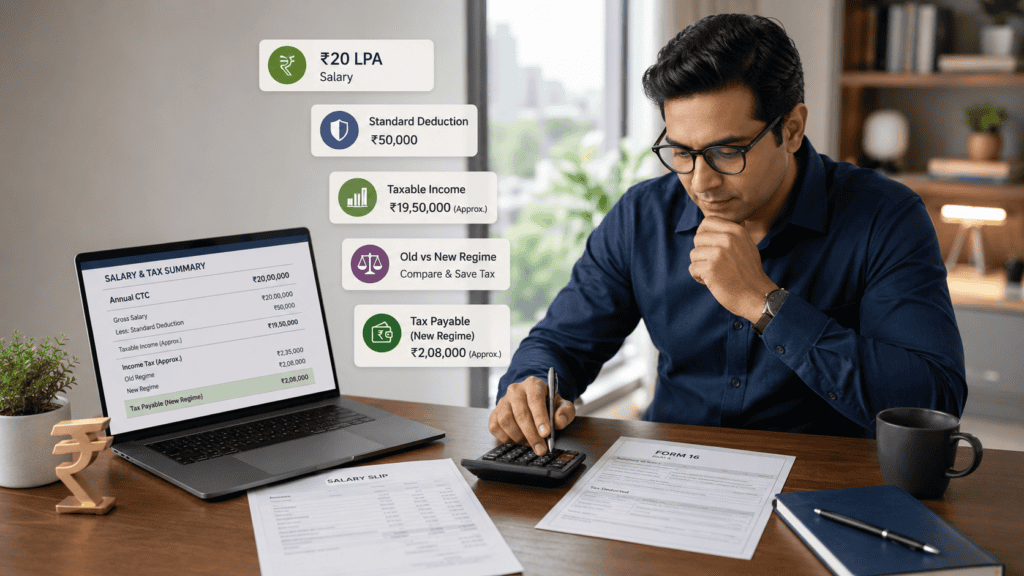

If you just received an offer letter at ₹20 LPA or recently cleared a promotion into this bracket, the first practical question is not about equity or gratuity. It is: how much tax will I actually pay on this salary?

Tax on 20 LPA salary is not a single fixed number. It changes based on which tax regime you choose, how your employer structures your pay, which deductions you declare, and whether variable pay or a joining bonus lands in the same financial year. Two colleagues drawing exactly ₹20 LPA can end up with tax bills that differ by more than ₹1 lakh.

This article gives you a step-by-step calculation for both the old and new tax regimes for Assessment Year 2026-27 (Financial Year 2025-26) — with slab-wise breakdowns, cess, standard deduction, and a clear old-versus-new comparison — so you can make an informed decision before your employer asks you to declare your regime or before you file your ITR.

Quick Answer: Tax on 20 LPA Salary

Tax on 20 LPA salary depends on taxable income after standard deduction, deductions, regime choice and cess. For a ₹20,00,000 salary, compare new regime slabs with old regime deductions before deciding. The final payable tax can change if HRA, 80C, 80D, NPS or home loan benefits apply.

Key Takeaways

- A ₹20,00,000 gross salary is not the same as taxable income — standard deduction, exempt allowances, and declared deductions all reduce it before slabs are applied.

- Under the new tax regime for FY 2025-26, a ₹75,000 standard deduction brings taxable income to approximately ₹19,25,000 — total tax payable works out to roughly ₹1,92,400 including 4% Health and Education Cess.

- Section 87A rebate does not apply at ₹20 LPA in either regime — the rebate threshold is well below the taxable income a ₹20 LPA salary produces, even after standard deduction.

- The old regime beats the new regime at ₹20 LPA only if your total deductions and exemptions exceed approximately ₹7.5 lakh — a threshold most salaried employees without an active home loan will not reach.

- TDS deducted by your employer through the year may not match your final tax liability if you received a bonus, changed employers, or declared a regime that did not reflect your actual deductions.

- Always run both regimes through the official income tax calculator and cross-check with your Form 16 before filing your ITR.

Key Facts at a Glance

| Item | New Tax Regime (FY 2025-26) | Old Tax Regime (FY 2025-26) |

|---|---|---|

| Gross Salary Assumed | ₹20,00,000 | ₹20,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (no other deductions) | ₹19,25,000 | ₹19,50,000 |

| Section 87A Rebate Applicable? | No — income above rebate threshold | No — income above rebate threshold |

| Surcharge Applicable? | No — income below ₹50L threshold | No — income below ₹50L threshold |

| Health and Education Cess | 4% on total tax payable | 4% on total tax payable |

| Assessment Year | AY 2026-27 (FY 2025-26) | AY 2026-27 (FY 2025-26) |

All figures are illustrative and assume salary is entirely gross salary with no exempt allowances. Actual taxable income varies by employer pay structure, exemptions claimed, and deductions declared. Verify current slabs and limits at incometax.gov.in before filing.

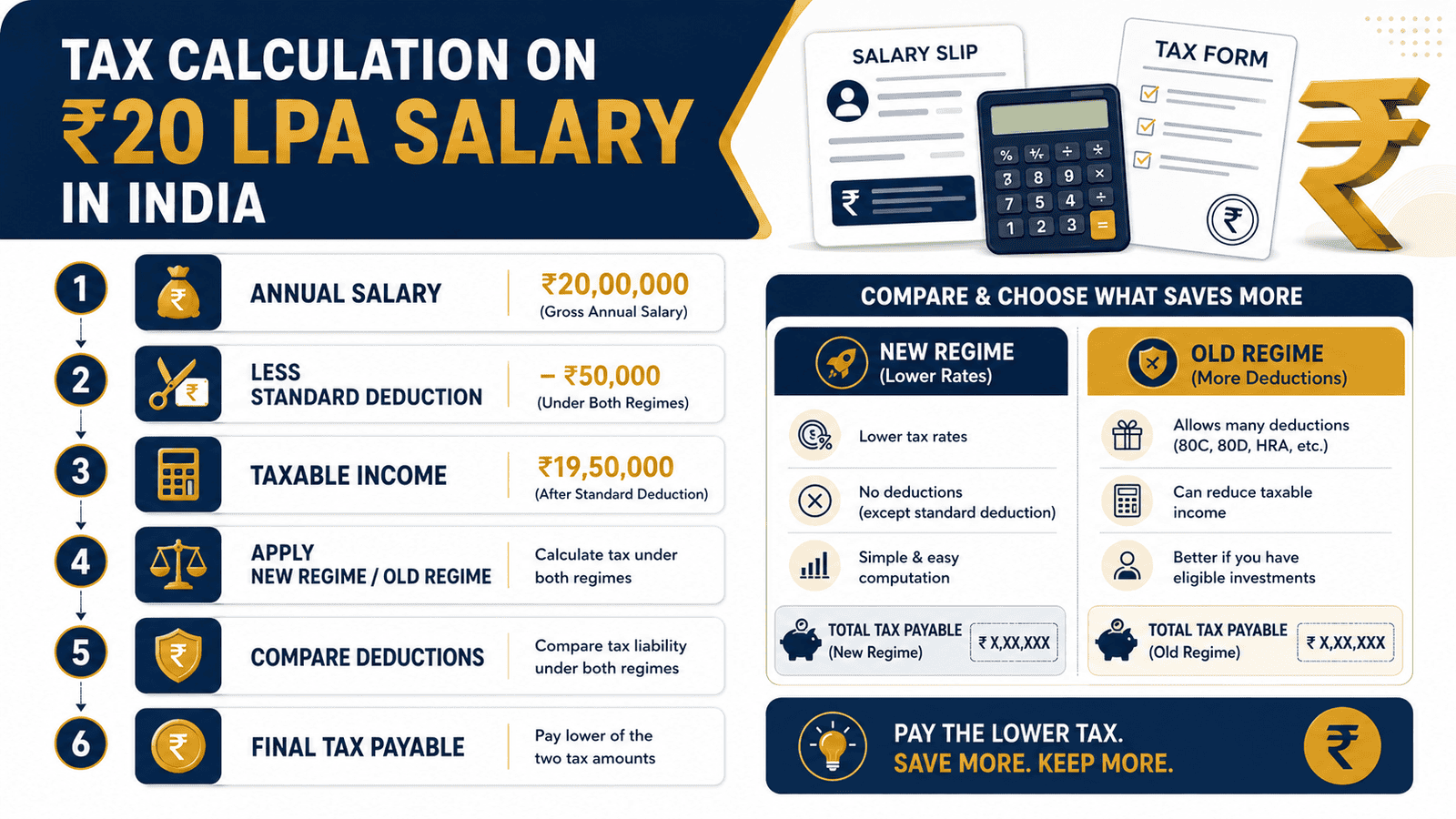

How Tax on 20 LPA Salary Is Actually Calculated

CTC, Gross Salary, Net Salary, and Taxable Income Are Four Different Numbers

Most salary confusion starts here, and it costs people real money at ITR time. Your Cost to Company is everything the employer spends on you — including their share of Provident Fund contributions (typically 12% of your basic pay), gratuity provisions, and sometimes group insurance premiums. Your gross salary is the figure on your payslip before any deductions. Your net or take-home salary is what actually reaches your bank account each month. And your taxable salary income — the number the Income Tax Department applies slabs to — is different from all three.

For a ₹20 LPA CTC package, the gross salary receivable by the employee after excluding employer PF is often closer to ₹19,04,000 or lower, depending on how the employer structures the pay. A ₹20 LPA CTC package where employer PF is ₹96,000 per year (12% of ₹8,00,000 basic) means the employee actually receives ₹19,04,000 as gross salary — the rest goes into the EPF account as employer contribution. This article uses ₹20,00,000 as the gross salary figure for simplicity. Your taxable income may start lower than this.

How the Standard Deduction Reduces Your Taxable Salary Income

Before any slab calculation begins, every salaried employee in India gets a flat deduction from their salary income — no proof, no investment, no paperwork required. For FY 2025-26, this standard deduction is ₹75,000 under the new tax regime and ₹50,000 under the old regime. It applies automatically the moment you report salary income.

After the standard deduction, taxable income from a ₹20,00,000 gross salary starts at:

- New regime: ₹20,00,000 − ₹75,000 = ₹19,25,000

- Old regime (before other deductions): ₹20,00,000 − ₹50,000 = ₹19,50,000

To understand exactly how this deduction works and why it matters, read the full guide on understanding standard deduction and how it reduces your taxable salary.

Why the New Regime Has Fewer Deductions but Lower Slabs

The new tax regime under Section 115BAC replaces most deductions and exemptions with lower slab rates across every income bracket. HRA exemption, Leave Travel Allowance, and most Chapter VI-A deductions — including Section 80C, Section 80D, and Section 80CCD(1B) for NPS — are not available. What you retain is the standard deduction and deductions for employer NPS contributions under Section 80CCD(2).

In exchange, the slab rates are genuinely lower — especially in the ₹4 lakh to ₹16 lakh band. For employees without large deductions, this usually means paying significantly less tax under the new regime. That is why the government made the new regime the default from FY 2024-25 onwards, shifting the burden of proof to the employee who wants to opt for the old regime instead.

Why the Old Regime Requires Proof, Planning, and High Deductions at ₹20 LPA

Under the old regime, you can reduce taxable income through Chapter VI-A deductions: Section 80C allows up to ₹1,50,000 for EPF, ELSS, PPF, life insurance premiums, and home loan principal repayment. Section 80D allows deductions for health insurance premiums. Section 80CCD(1B) permits an additional ₹50,000 for NPS contributions over and above the 80C limit. HRA exemption is available if you pay rent. Home loan interest under Section 24b allows up to ₹2,00,000 deduction on a self-occupied property.

The catch: at ₹20 LPA, the new regime’s lower slabs already produce a much lower tax than the old regime’s higher slabs applied to ₹19,50,000 taxable income. To close this gap, your old regime deductions must be large enough — approximately ₹7.5 lakh in total — to bring your old-regime taxable income down to a level where the old regime’s tax equals or beats the new regime’s ₹1,92,400. That is a bar most salaried employees without an active home loan will not clear.

A Note on Rebate and Cess at This Salary Level

Section 87A rebate is frequently searched alongside ₹20 LPA — but it does not apply here. The rebate reduces tax to nil only for taxpayers whose taxable income falls within a threshold significantly below what a ₹20 LPA salary produces after standard deduction. At ₹19,25,000 (new regime) or ₹19,50,000 (old regime without deductions), no rebate applies.

What does apply is the Health and Education Cess of 4% on the total tax computed. There is no surcharge at this income level — surcharge is levied only when total income exceeds ₹50,00,000. Taxable salary income from salary ₹20 LPA is well below that threshold.

Real Example: Rohan, Software Engineer, Bengaluru

Rohan is 31 years old, works as a senior software engineer at a product company in Bengaluru, and draws a gross salary of ₹20,00,000 per year in FY 2025-26. His pay structure includes a ₹8,00,000 basic, ₹4,00,000 HRA, and ₹8,00,000 in special allowances. He rents an apartment at ₹20,000 per month and has made ₹1,50,000 in Section 80C investments (including his employee EPF contributions). He pays ₹20,000 per year in health insurance premiums for himself and his spouse.

New regime: Taxable income = ₹20,00,000 − ₹75,000 standard deduction = ₹19,25,000. Total tax with cess = ₹1,92,400. No investment proofs needed.

Old regime: Rohan’s available deductions are ₹50,000 (standard deduction) + ₹1,50,000 (80C) + ₹20,000 (80D) + approximately ₹1,60,000 in HRA exemption (based on rent paid, basic salary, and metro location). Total deductions: ₹3,80,000. Taxable income: ₹16,20,000. Tax payable including cess: approximately ₹3,10,440. The new regime saves Rohan approximately ₹1,18,000 in tax compared to his old regime with current deductions.

To see how this compares at a lower salary level, read the compare nearby salary levels guide.

How to Calculate Tax on 20 LPA Salary

Tax Payable = Slab-wise Tax on Taxable Income + 4% Health and Education Cess − Section 87A Rebate (if applicable)

Step-by-Step: New Regime (FY 2025-26)

Step 1 — Annual gross salary: ₹20,00,000

Total tax payable (new regime, no extra deductions): ₹1,92,400

For a personalised calculation using your exact salary structure and deductions, use the use the tax calculator for FY 2025-26 old vs new regime comparison.

| Scenario | Taxable Income | Tax Payable (incl. 4% cess) |

|---|---|---|

| New regime — standard deduction only | ₹19,25,000 | ₹1,92,400 |

| Old regime — standard deduction only | ₹19,50,000 | ₹4,13,400 |

| Old regime — Rohan’s case (₹3.80L deductions) | ₹16,20,000 | ~₹3,10,440 |

| Old regime — break-even (approx. ₹7.58L deductions) | ~₹12,42,000 | ~₹1,92,400 |

Illustrative calculations for FY 2025-26. Verify current slab rates, cess, and deduction limits at incometax.gov.in before using these figures for filing.

Comparison: New Tax Regime vs Old Tax Regime at ₹20 LPA

| Parameter | New Tax Regime | Old Tax Regime |

|---|---|---|

| Standard Deduction | ₹75,000 | ₹50,000 |

| HRA Exemption | Not available | Available with proof |

| Section 80C (up to ₹1.5L) | Not available | Available |

| Section 80D (health insurance) | Not available | Available |

| NPS via 80CCD(1B) — up to ₹50,000 | Not available | Available |

| Employer NPS via 80CCD(2) | Available | Available |

| Section 24b — home loan interest | Not available | Up to ₹2L |

| Tax (no deductions beyond standard) | ₹1,92,400 | ₹4,13,400 |

If you are evaluating a hike or promotion, see how the tax picture shifts at the next bracket: check higher salary tax at ₹25 LPA.

How to Decide What’s Right for You

your total deductions — including HRA, 80C investments, 80D premiums, home loan interest, and NPS — add up to less than ₹4 lakh per year, the new regime will result in significantly lower tax at ₹20 LPA. No further analysis is necessary.

you have an active home loan and claim the full ₹2,00,000 interest deduction under Section 24b, plus full 80C, HRA, health insurance, and NPS — run the old regime numbers carefully. At ₹20 LPA, a combined deduction of ₹7+ lakh can bring old regime tax close to or below the new regime figure.

you joined a new employer this year, received a salary hike, or are in your first year of employment at this CTC — default to the new regime unless you have a complete deduction calculation ready. TDS calibration is simpler and the default is already new regime from FY 2024-25 onwards.

your employer offers NPS contribution under Section 80CCD(2), do not overlook it — this deduction is available in both regimes and directly reduces your taxable income without eating into the ₹1.5 lakh 80C limit.

your variable pay, performance bonus, or joining bonus makes your actual annual income meaningfully higher than your fixed gross salary, your employer’s TDS projection may fall short. Check your tax liability in October or February and top up through advance tax if there is a shortfall.

you do not have rent receipts, insurance premium certificates, and investment proofs ready — the old regime’s deductions cannot be claimed in practice. Do not declare old regime expecting deductions you cannot substantiate at assessment time.

For a detailed walkthrough of how to pick your regime at different income and deduction combinations, read the guide to compare both regimes for salaried employees.

Common Mistakes to Avoid

Treating CTC as Taxable Income

Your CTC of ₹20 LPA includes employer PF contributions, gratuity provisions, and non-cash benefits that never appear in your taxable salary.

Treating CTC as taxable income overstates your liability by ₹50,000–₹1,00,000 in a typical pay structure — and can lead you to make wrong regime decisions or panic unnecessarily about your tax burden.

Always start with your gross salary from the payslip, not the CTC from your offer letter.

Assuming Section 87A Rebate Applies at ₹20 LPA

The Section 87A rebate is one of the most searched terms alongside salary tax questions — and one of the most misapplied. The rebate reduces tax to nil only for taxpayers whose taxable income falls below a threshold well below what a ₹20 LPA salary produces.

Expecting a rebate that does not apply will cause you to underestimate your tax liability, leading to a demand at ITR filing — plus potential interest under Sections 234B and 234C.

Verify the current rebate threshold at incometax.gov.in before assuming it applies to your income level.

Ignoring Variable Pay and Joining Bonus Tax Impact

A ₹1,50,000 performance bonus received in October is fully taxable as salary income in the same financial year. If your employer calibrated your TDS projection on fixed salary alone, this bonus pushes actual liability higher than what was deducted.

The result is a balance tax payable at ITR filing — or worse, an interest charge if you missed the advance tax date. Request your employer to recalculate TDS immediately after any bonus payout by submitting a revised income declaration.

Choosing Old Regime Without Running Both Calculations

Many employees declare old regime in April because they plan to make 80C investments by March 31 — then actually invest less, or do not invest at all. If your real deductions are lower than declared, your employer deducted less TDS than required and you owe the balance at filing.

Only declare old regime if your investments are either already made or locked in — not on the basis of what you intend to do in the months ahead.

Not Accounting for Professional Tax

Professional tax is a small but real deduction — typically ₹2,400 per year in Karnataka, ₹2,500 in Maharashtra, and varying amounts across other states. It is deductible from salary income and shows on your payslip as a monthly deduction.

It does not change the regime decision materially, but omitting it means your take-home estimate is slightly off every month. It is also deductible under the old regime — confirm your state’s applicable amount on your payslip.

Not Cross-Checking TDS with Form 16, Form 26AS, and AIS

TDS deducted at source must match what appears in your Form 16 Part A, Form 26AS, and Annual Information Statement. Mismatches — common when switching employers, receiving freelance income, or having TDS credited to a wrong PAN — delay refunds and create tax demands.

Reconcile all three documents well before the ITR filing deadline. Do not click submit until the numbers match.

When This May Not Be the Right Choice

This article covers a straightforward salary-only tax calculation. The figures and regime comparison may not apply fully if:

- You have freelance, consultancy, or business income alongside salary — this changes your applicable ITR form, presumptive taxation rules, and regime-switching rules significantly.

- You have capital gains from equity mutual funds, shares, ESOPs, or property sales — these are taxed separately and at rates independent of your slab.

- You received salary from two employers in the same year — each employer calculates TDS independently and you must consolidate total income and TDS at filing time.

- You are a non-resident Indian or have foreign income, foreign assets, or treaty-based tax relief — the applicable calculation differs materially from the resident salaried scenario shown here.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

The calculations in this article reflect provisions as understood for FY 2025-26. Income tax slabs, standard deduction amounts, rebate thresholds, cess rates, and deduction limits can change with each Union Budget or subsequent notification. Always verify current figures before filing.

- Income Tax Department — incometax.gov.in — official source for current slab tables, regime comparison, ITR filing, and tax payment.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Your Form 16 is also an essential verification document — it contains your employer’s salary breakdown, the regime applied, TDS deducted, and any deductions your employer accounted for. To understand every line in it before you file, read the guide to read your Form 16 before filing your ITR.

Expert Tips

- Run both regimes before your employer’s investment declaration window — typically January for mid-year and April for full-year declaration. Once you declare, switching regimes through the employer mid-year is generally not permitted. The official ITR filing at year-end gives you one more opportunity to choose.

- If your employer contributes to NPS on your behalf under Section 80CCD(2), that deduction is available in the new regime too — unlike most other Chapter VI-A deductions. Factor it in before concluding the new regime “has no deductions.”

- At ₹20 LPA, the new regime is almost always better unless total old-regime deductions exceed approximately ₹7.5 lakh. Do a ten-minute calculation on paper or the official calculator before committing to old regime simply because you “have 80C investments.”

- Check your year-to-date TDS in October and again in February using your payslip or Form 26AS. If your TDS balance is tracking lower than your estimated liability — due to bonus, hike, or regime mismatch — request your employer to recalibrate TDS for the remaining months.

- If you received ESOP income, a joining bonus, or a mid-year salary revision that pushed your total earnings significantly higher than projected, calculate and pay advance tax by March 15 to avoid interest under Sections 234B and 234C. The threshold for mandatory advance tax is ₹10,000 in balance liability.

- Do not confuse your monthly in-hand salary with your tax payable divided by twelve. TDS is usually higher in January–March when employers true-up the full year’s liability. Expect lower in-hand in those months even if your gross salary did not change.

Frequently Asked Questions

How much tax do I pay on a ₹20 lakh salary?

Under the new tax regime for FY 2025-26, a ₹20,00,000 gross salary produces a taxable income of approximately ₹19,25,000 after the standard deduction of ₹75,000. Tax on this income — applying the new regime slabs and adding 4% Health and Education Cess — works out to approximately ₹1,92,400. Under the old regime with only the standard deduction and no other investments, the tax is significantly higher. Verify current slab rates at incometax.gov.in before using any estimate for ITR filing.

Is the Section 87A rebate available for ₹20 LPA salary?

No. Section 87A rebate applies only if taxable income falls within a threshold that is well below the taxable income of a ₹20 LPA gross salary — even after standard deduction and typical deductions. At ₹19,25,000 (new regime) or above, no rebate applies under either regime. Do not factor a rebate into your tax estimate at this salary level. Verify the current rebate threshold at incometax.gov.in.

Is the new regime better for a ₹20 LPA salary?

For most salaried employees, yes — but it depends on total deductions. The new regime results in lower tax unless your combined old-regime deductions (HRA, 80C, 80D, home loan interest, NPS) exceed approximately ₹7.5 lakh. Most employees without an active home loan and high metropolitan rent will not reach that threshold, making the new regime the better choice. Run both calculations using the same income figures before deciding.

How much is ₹20 LPA in-hand salary per month?

In-hand salary depends on your employer’s pay structure, TDS rate, employee EPF deduction, and professional tax. A rough illustration: annual tax of approximately ₹1,92,400 divided over 12 months is around ₹16,033 per month in TDS. After employee PF (around ₹96,000/year or ₹8,000/month on ₹8L basic) and professional tax (approximately ₹200/month in most states), a typical in-hand could range from ₹1,28,000 to ₹1,48,000 per month depending on pay structure and any reimbursements. Use a dedicated take-home salary calculator for an accurate monthly estimate based on your exact payslip.

Does the standard deduction apply to a ₹20 LPA salary?

Yes — and it applies automatically without any proof or investment required. For FY 2025-26, the standard deduction is ₹75,000 under the new regime and ₹50,000 under the old regime. It applies to every salaried employee regardless of income level. Verify the current amount at incometax.gov.in, as the figure can change with each Budget.

How does HRA exemption affect old regime tax for a ₹20 LPA employee?

HRA exemption under the old regime is the minimum of three values: actual HRA received from employer, rent paid minus 10% of basic salary, and 50% of basic salary for metro cities or 40% for non-metro. For a ₹20 LPA employee in Bengaluru with ₹8L annual basic paying ₹20,000/month rent, the exempt HRA typically works out to approximately ₹1,60,000 per year. This is a meaningful deduction but, on its own, does not make the old regime competitive against the new regime at this salary — it must combine with home loan interest, full 80C, NPS, and other deductions to close the gap.

Can I switch from the new regime to the old regime at ITR filing?

Salaried employees who have no business income can switch regimes at the time of filing their ITR each year — regardless of what regime they declared to their employer for TDS purposes. However, mid-year switching through the employer is generally not permitted once you have declared. At ITR filing time, choose the regime that results in lower tax based on your actual annual income and deductions. Verify the current switching provisions at incometax.gov.in before filing.

What happens if my TDS is lower than my actual tax liability?

If your TDS for the year falls short of your actual tax payable — due to bonus income, employer underestimation, or regime declaration mismatch — you will have a balance tax payable at ITR filing. If this balance exceeds ₹10,000 and advance tax was not paid on time during the year, interest under Sections 234B and 234C applies. To avoid this, check your projected annual tax in advance — especially after any bonus payout — and pay advance tax by the March 15 deadline.

What assessment year applies to salary earned in FY 2025-26?

Salary earned from April 1, 2025 to March 31, 2026 falls under Financial Year 2025-26 and is assessed in Assessment Year 2026-27. The ITR for AY 2026-27 is typically due by July 31, 2026 for salaried individuals without audit requirements. Verify current due dates at incometax.gov.in — extensions are sometimes announced close to the deadline.

Is surcharge applicable on ₹20 LPA salary income?

No. Surcharge is levied only when total income exceeds ₹50,00,000. At ₹20 LPA, total income is well below this threshold and no surcharge applies in either regime. Only the 4% Health and Education Cess on the computed tax liability applies. Verify the current surcharge slabs and thresholds at incometax.gov.in if your income is approaching higher levels.

Final Verdict

For most salaried employees earning ₹20 LPA, the new tax regime is the lower-tax and simpler choice for FY 2025-26. The standard deduction of ₹75,000 reduces taxable income to ₹19,25,000, and the total tax on 20 LPA salary under the new regime works out to approximately ₹1,92,400 including cess — with no investment declarations or supporting documents required.

The old regime deserves a closer look only if your genuine, provable deductions — home loan interest, HRA, full 80C utilisation, NPS, and health insurance — collectively exceed approximately ₹7.5 lakh. That level of deduction typically requires an active home loan in addition to everything else. Without one, the new regime almost always wins at ₹20 LPA.

Run your own numbers before your employer’s declaration window closes. Use the use the tax calculator for a personalised old vs new regime comparison. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.