Knowing your ₹8 LPA salary is straightforward. Working out the actual tax on 8 LPA salary — across the new and old regime, after standard deduction, after Section 87A rebate — is where most salaried employees get completely lost. The answer is not the same for everyone at ₹8 lakh: it depends on your regime choice, your salary structure, and whether a rebate wipes out your tax bill before you even pay a rupee. The difference between choosing the wrong regime and the right one at this income level can be as much as ₹65,000. This article walks you through every step, for FY 2025–26 (AY 2026–27), in plain language.

Quick Answer: Tax on 8 LPA Salary

Tax on 8 LPA salary depends on whether you choose the new or old regime, salary deductions, and rebate eligibility. After standard deduction and Section 87A rebate rules, many salaried taxpayers may pay low or nil tax under the new regime if conditions are met. Under the old regime without significant deductions, tax can be substantially higher. Always use a tax calculator and verify current slabs before filing.

Key Takeaways

- Under the new tax regime for FY 2025–26, a salaried employee earning ₹8,00,000 gross may pay zero income tax after standard deduction of ₹75,000 and Section 87A rebate — if total taxable income stays within the eligible threshold.

- Under the old tax regime with no additional deductions, the same ₹8 LPA salary can attract a tax liability of approximately ₹65,000 including health and education cess — a significant difference from nil.

- The standard deduction is a flat reduction from gross salary before any slab applies — ₹75,000 under the new regime and ₹50,000 under the old regime for FY 2025–26 (verify before filing).

- A deduction reduces your taxable income; a Section 87A rebate reduces the tax you have already calculated — these work at different stages and must not be confused when estimating your liability.

- Under the old regime, if Chapter VI-A deductions — 80C, 80D, NPS — bring your taxable income to ₹5 lakh or below, a separate rebate can also bring your tax to nil, but it requires deliberate investment planning.

- Your employer’s monthly TDS is an estimate. The final tax is settled when you file your ITR — which may produce a refund or a balance due, depending on what actually happened during the year.

Key Facts at a Glance

| Parameter | New Regime — FY 2025–26 | Old Regime — FY 2025–26 |

|---|---|---|

| Assessment Year | AY 2026–27 | AY 2026–27 |

| Annual Gross Salary | ₹8,00,000 | ₹8,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (no extra deductions) | ₹7,25,000 | ₹7,50,000 |

| Tax Before Rebate | ₹16,250 | ₹62,500 |

| Section 87A Rebate | ₹16,250 (full — income within threshold) | Nil (income above old-regime threshold) |

| Health and Education Cess (4%) | ₹0 | ₹2,500 |

| Final Tax Payable | ₹0 | ₹65,000 |

| Official Source | incometax.gov.in | incometax.gov.in |

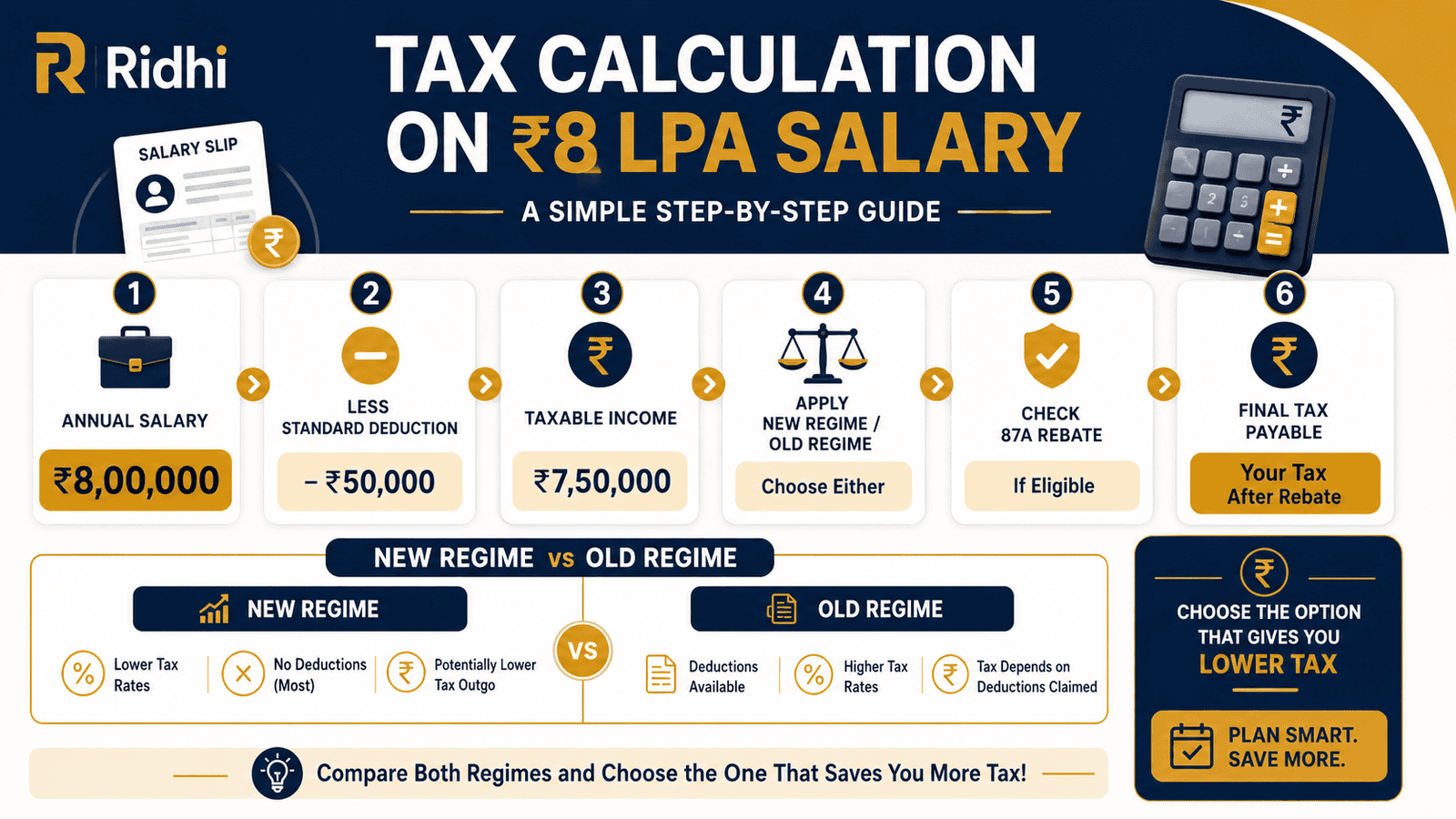

How Tax on 8 LPA Salary Is Actually Calculated

Most people assume income tax is charged directly on the ₹8,00,000 figure. It isn’t. Your gross salary passes through several steps before a slab rate ever touches it — and understanding each step is the difference between correct tax planning and costly guesswork.

Step 1: What Is Your Taxable Salary?

Your gross salary includes basic pay, HRA, special allowances, and other components. Some of these — Leave Travel Allowance under specific conditions, HRA if you pay rent and are in the old regime — are partially or fully exempt. What remains after exemptions is your gross taxable salary. This is not the same as your CTC. Understanding how gross salary becomes taxable income is the foundation of any tax calculation. Our guide on taxable salary meaning explains this conversion in detail with examples.

Step 2: The Standard Deduction Comes Off First

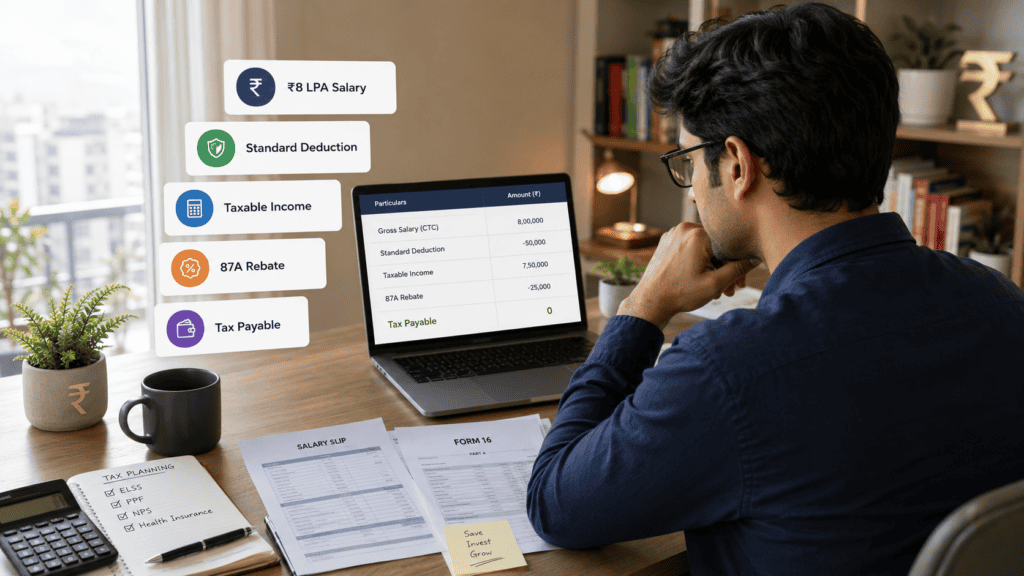

Before any slab rate applies, every salaried employee gets a flat standard deduction. No receipts. No proof. No conditions — it applies automatically. For FY 2025–26, the standard deduction is ₹75,000 under the new tax regime and ₹50,000 under the old tax regime.

For an ₹8,00,000 gross salary: after the new-regime standard deduction, your taxable income drops to ₹7,25,000. Under the old regime, it drops to ₹7,50,000. That ₹25,000 difference sounds small, but it can move you across slab boundaries and change your tax outcome meaningfully. The standard deduction guide covers how this interacts with different salary structures and why it matters more at some income levels than others.

Step 3: Deduction vs. Rebate — They Are Not the Same

This confusion costs people money every year. A deduction reduces your taxable income before the slab tax is calculated. Section 80C contributions, HRA exemption, home loan interest — all of these are deductions. A rebate under Section 87A reduces the tax after it has been calculated on your taxable income.

Why does this matter for ₹8 LPA? Under the new regime for FY 2025–26, the Section 87A rebate threshold is high enough to cover an ₹8 LPA salary after standard deduction. The calculated tax gets wiped out by the rebate — without requiring you to invest in a single 80C product. Under the old regime, the rebate threshold is much lower, so it only helps if deductions bring your taxable income down significantly first.

Step 4: Slab Rates Apply to the Remaining Taxable Income

India’s income tax uses a progressive slab structure. Different portions of your income are taxed at different rates — not your entire income at one flat rate. Under the new tax regime for FY 2025–26, income up to ₹4 lakh attracts nil tax; income between ₹4 lakh and ₹8 lakh is taxed at 5%. For an ₹8 LPA earner with ₹7,25,000 taxable income, only the portion above ₹4 lakh — that is, ₹3,25,000 — is taxed at 5%, giving ₹16,250 in tax before rebate.

Under the old tax regime, slab structure is different. Income up to ₹2.5 lakh is nil; ₹2.5 lakh to ₹5 lakh is 5%; ₹5 lakh to ₹10 lakh is 20%. For ₹7,50,000 taxable income (old regime, no extra deductions), the calculation gives ₹62,500 before cess — and the old-regime 87A rebate does not apply at this income level.

Step 5: Health and Education Cess Is Always Added Last

Once tax payable after rebate is determined, a 4% health and education cess applies. If your tax after rebate is ₹0 — as in the new-regime case for ₹8 LPA — the cess is also ₹0. If your tax is ₹62,500, cess adds ₹2,500. The cess cannot be reduced through any deduction or investment. It applies to all taxpayers, based on the net tax figure after all rebates.

Real Example: Rohan’s ₹8 LPA Tax Calculation

Rohan, 27, is a software analyst at a mid-size IT firm in Pune. His annual CTC is ₹8,00,000, paid as basic salary, HRA, and special allowance. He lives in a rented flat but has not claimed HRA exemption because he chose the new tax regime at his employer’s declaration stage.

Under the new regime for FY 2025–26: Rohan’s gross taxable salary is ₹8,00,000. After the standard deduction of ₹75,000, his net taxable income is ₹7,25,000. Applying the slab rates — nil up to ₹4 lakh, 5% on ₹3,25,000 — gives a tax of ₹16,250. His taxable income of ₹7,25,000 is within the Section 87A rebate threshold, so the full ₹16,250 is rebated. Tax after rebate: ₹0. Cess: ₹0. Final tax payable: nil.

If Rohan had instead chosen the old regime with no additional deductions: taxable income ₹7,50,000, tax ₹62,500, cess ₹2,500, total ₹65,000. The regime choice alone determines whether he keeps or loses ₹65,000. Rohan’s employer may still deduct some TDS monthly depending on the declaration form — he will reconcile this and receive a refund when he files his ITR.

How to Calculate Tax on 8 LPA Salary

Taxable Income = Gross Salary − Standard Deduction − Eligible Deductions (old regime only)

Tax = (Slab-wise tax on Taxable Income) − Section 87A Rebate (if eligible)

Final Tax Payable = Tax After Rebate + 4% Health and Education Cess

Applying the formula to ₹8 LPA for FY 2025–26 across three common scenarios — all figures should be verified before filing:

| Scenario | Key Inputs | Final Tax Payable |

|---|---|---|

| New Regime — No extra deductions | Taxable income ₹7,25,000; rebate applies in full | ₹0 |

| Old Regime — No extra deductions | Taxable income ₹7,50,000; rebate not applicable | ₹65,000 (incl. cess) |

| Old Regime — With ₹2.5L deductions (80C + 80D + NPS) | Taxable income ₹5,00,000; old-regime rebate applies | ₹0 |

For your exact salary structure — including HRA, variable pay, or employer PF contributions — use the salary tax calculator for a precise estimate. Before assuming nil tax, verify your Section 87A rebate eligibility for the current financial year.

Comparison: New Regime vs Old Regime for ₹8 LPA

| Factor | New Regime | Old Regime |

|---|---|---|

| Standard Deduction | ₹75,000 Higher | ₹50,000 |

| 80C, HRA, Home Loan Deductions | Not allowed | Allowed |

| Section 87A Rebate Threshold | Up to ₹12 lakh taxable income Higher | Up to ₹5 lakh taxable income |

| Tax — ₹8L, no extra deductions | ₹0 | ₹65,000 |

| Tax — ₹8L, with ₹2.5L deductions | Not applicable — deductions not allowed | ₹0 (if taxable ≤ ₹5L) |

| Best suited for | Employees with few or no major deductions | Employees with HRA, home loan, and 80C exceeding ₹2.5L |

| Complexity | Low — no proofs needed | Requires investment proof and planning |

The comparison above covers the basic salary-only case. If your salary includes significant variable pay, multiple employers, or rental income, the analysis changes. Read the full breakdown in our old versus new regime guide.

How to Decide What’s Right for You

Your ₹8 LPA salary is straightforward — basic, HRA, and special allowance — with no home loan, no 80C investments, and no major deductions: the new regime will almost certainly result in nil tax. File under the new regime without hesitation.

You have existing 80C investments of ₹1.5 lakh and pay significant rent in a metro city: add up your total eligible deductions before deciding. If they cross ₹2 lakh, compare both regimes using a calculator — the old regime may produce a lower tax or comparable outcome with more planning involved.

You contribute to NPS under Section 80CCD(1B) and have combined deductions — 80C ₹1.5L, 80D ₹25,000, NPS ₹50,000 — exceeding ₹2.25 lakh: the old regime can bring your taxable income close to ₹5 lakh and may result in nil tax under the old-regime 87A rebate as well. Verify current limits before acting.

You received a mid-year increment, joining bonus, or performance payout that raised your total gross earnings above ₹8,75,000: recalculate. A higher total income may push your taxable income above the Section 87A threshold even under the new regime, resulting in some tax payable. Do not assume nil tax on the basis of your base salary alone.

You want maximum monthly take-home and no investment lock-ins: the new regime requires no 80C commitments and keeps your in-hand salary higher through the year. Check how your regime choice affects your monthly in-hand pay before finalising.

You have a home loan with interest of ₹1.5–2 lakh per year under Section 24b — this deduction is not available under the new regime. If home loan interest is your largest deduction, do not switch to the new regime without calculating the full impact first. The old regime may cost less overall in this specific scenario.

Common Mistakes to Avoid

Assuming ₹8 LPA Always Means Zero Tax

Under the new regime for FY 2025–26, nil tax is possible for an ₹8 LPA salary — but only if total taxable income after standard deduction stays within the Section 87A threshold.

A mid-year promotion to ₹9 LPA, a bonus credited in March, or a taxable allowance not captured in standard deduction can all push total taxable income above the threshold and result in unexpected tax due at ITR time.

Calculate your full-year total taxable income — not just base salary — before assuming a nil outcome.

Confusing Deduction with Rebate

Many salaried employees believe Section 87A is something they “invest in” or “claim” alongside 80C. It is not a deduction — it is a rebate on calculated tax and applies only if your taxable income is within the eligible limit.

The practical difference: if your taxable income is ₹7,25,000 and your slab tax is ₹16,250, the rebate eliminates that ₹16,250. No 80C investment was required. Treating the rebate as a deduction and double-counting it leads to serious tax shortfalls at filing time.

Understand which step each mechanism works at — deductions first, slab tax next, rebate last, then cess.

Ignoring Taxable Salary Components

Your CTC says ₹8 lakh, but your actual taxable gross salary may differ. Special allowances, city compensatory allowances beyond permitted limits, and taxable perquisites all add to gross taxable salary.

An employee with a ₹8 LPA CTC but ₹90,000 in fully taxable special allowances effectively has ₹8,90,000 in gross taxable salary — which changes the entire tax calculation. Check your salary slip components carefully, not just the CTC figure.

Your Form 16 from your employer will show the final taxable income figure. That is the number that matters for your ITR.

Not Comparing Both Regimes Before Filing

Your employer defaults to one regime for TDS — often the new regime. That does not mean it is the right choice for your situation. Salaried employees can typically choose their regime when filing the ITR.

Running a quick comparison using both regimes in February or March — when you have your actual investment figures — takes 20 minutes and can save you thousands. The declaration you gave your employer in April last year does not lock in your ITR regime choice.

Always compare before filing, not just at investment declaration time.

Using Last Year’s Tax Slabs

Tax slabs, standard deduction limits, Section 87A rebate thresholds, and cess rates can and do change with each Union Budget. The slabs for FY 2024–25 are not guaranteed to be identical to FY 2025–26.

Using outdated numbers — found in an old article, an office WhatsApp group, or a stale blog post — to plan your tax is one of the most common errors among salaried employees. Before any financial decision, verify current rates at incometax.gov.in.

Bookmark the official portal. Use it every time you see a specific tax figure, not just once a year.

Treating Employer TDS as the Final Word

Monthly TDS is your employer’s best estimate of your annual tax liability — based on your declaration, salary projections, and assumed investments. If your actual income, investments, or deductions differ from the declaration, TDS may be higher or lower than your true liability.

Excess TDS results in a refund — but only if you file your ITR. Missing TDS results in interest on the balance due. The ITR, not the TDS, is the final settlement. File before the deadline every year regardless of whether your net tax appears to be nil.

When This May Not Be the Right Choice

The nil-tax conclusion for ₹8 LPA under the new regime applies only to a straightforward salary with no other income sources. This article may not cover your full situation if:

- You received a joining bonus, performance bonus, or referral incentive that pushes your total annual taxable income above the Section 87A threshold — even one additional ₹75,000 in gross income can shift the outcome.

- You have rental income, short-term or long-term capital gains from mutual funds or equities, or freelance income alongside your salary — each of these requires its own tax treatment and can significantly change your overall liability.

- You changed jobs mid-year and had two employers — both may have calculated TDS independently on an annualised basis, leading to a shortfall in total TDS relative to your combined annual income.

- You have carry-forward losses from previous years, relief claims under Section 89, or deductions under other provisions that require professional assistance to compute and claim correctly.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax slabs, standard deduction limits, Section 87A rebate thresholds, cess rates, and regime rules are all set by the government and can change with each Union Budget or regulatory notification. This article reflects publicly available information for FY 2025–26 (AY 2026–27), but you must confirm all figures directly from official sources before filing.

- Income Tax Department — incometax.gov.in: Current tax slabs for both regimes, standard deduction rules, Section 87A rebate limits, ITR filing portal, Form 26AS and AIS access, TDS credit verification.

- EPFO — epfindia.gov.in: Employee and employer provident fund contribution rules, relevant if your salary structure includes significant employer PF contributions that affect your net taxable income.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Run your tax calculation in February, not April: By February you know your actual investments, full-year salary (including bonuses), and any mid-year changes. A February calculation gives you time to make any last-minute eligible investments under the old regime before March 31 — or confirm you’re better off under the new regime with no additional action required.

- Collect your Form 16 from your employer before filing your ITR: Form 16 is issued by June 15 and shows your gross salary, exemptions, deductions as declared, TDS deducted, and employer PAN. Cross-check it against your own salary slips for the year. If any figure differs from your actual investment or income, resolve the discrepancy with your employer before filing.

- Don’t invest in 80C instruments solely for a tax benefit that may not exist: If your ₹8 LPA salary results in nil tax under the new regime, adding an ELSS or PPF contribution for “tax savings” that do not apply under that regime is a planning error. Invest in these instruments if they suit your financial goals — not because of a tax-saving assumption that doesn’t hold under your chosen regime.

- If you changed jobs during the year, collect Form 16 from both employers: Each employer calculates TDS based on the salary paid by them alone. The combined annual income from two employers may be higher than what each independently factored in, resulting in a tax shortfall. You are responsible for the difference at ITR time — even if neither employer made a calculation error.

- Recalculate your tax whenever your income changes significantly: A promotion, salary hike, or bonus that takes your annual gross above ₹8,75,000 can move your taxable income above nil-tax territory even under the new regime. Treat any income change above ₹50,000 per year as a trigger to rerun your tax estimate.

- File your ITR even if your tax payable is zero: Filing is typically required if your gross income exceeds the basic exemption limit, even if the rebate brings your tax to nil. Not filing means forfeiting any TDS refund owed to you, and it breaks a filing record that is useful for visa applications, loan approvals, and future tax assessments.

Frequently Asked Questions

How much income tax do I pay on an 8 lakh salary?

For FY 2025–26, a salaried employee earning ₹8,00,000 may pay nil income tax under the new regime after standard deduction of ₹75,000 and Section 87A rebate — assuming no other income and that taxable income stays within the rebate threshold. Under the old regime with no additional deductions, the total tax liability is approximately ₹65,000 including health and education cess. Verify current slabs, rebate limits, and cess rates at incometax.gov.in before filing your ITR for AY 2026–27.

Is ₹8 LPA salary completely tax-free under the new tax regime?

Under the new regime for FY 2025–26, after the standard deduction of ₹75,000, the taxable income from ₹8,00,000 gross salary is ₹7,25,000. If this falls within the Section 87A rebate threshold — which for FY 2025–26 covers taxable income up to ₹12 lakh — the full calculated tax of ₹16,250 is rebated, leaving nil tax payable. However, this changes if you have additional income — a bonus, rental income, capital gains — that increases total taxable income above the threshold.

Is the old regime ever better than the new regime for ₹8 LPA?

For most ₹8 LPA employees with few or no major deductions, the new regime results in lower (often nil) tax. The old regime becomes worthwhile only when total Chapter VI-A deductions — 80C, HRA, home loan interest, 80D, NPS — exceed approximately ₹2.5 lakh, potentially bringing taxable income to ₹5 lakh or below for the old-regime rebate to apply. Even then, the planning effort, investment lock-ins, and proof requirements mean the decision is genuinely case-by-case. Run both calculations before committing.

Does the standard deduction apply automatically or do I need to claim it?

The standard deduction applies automatically to all salaried employees and pensioners. You do not need to submit any proof, make any investment, or make any declaration to claim it. Your employer includes it in TDS calculations, and it appears in your Form 16. For FY 2025–26, it is ₹75,000 under the new regime and ₹50,000 under the old regime — verify current amounts before filing.

My employer deducts TDS every month. Does that equal my final tax?

No. Employer TDS is an estimate based on your income declaration at the start of the year — including your declared investments and expected income. If your actual investments, deductions, or income changed during the year, the final tax due may be higher or lower. You reconcile this when you file your ITR. Excess TDS means a refund; insufficient TDS means a balance due with interest. The ITR is the final settlement, not the monthly TDS.

Can I claim Section 87A rebate under the old tax regime at ₹8 LPA?

Not directly at ₹8 LPA under the old regime, because your taxable income of ₹7,50,000 (after ₹50,000 standard deduction) exceeds the old-regime rebate threshold of ₹5 lakh. To become eligible, you would need Chapter VI-A deductions of at least ₹2.5 lakh — for example, 80C ₹1.5L, Section 80CCD(1B) ₹50,000, and Section 80D ₹50,000 — to bring taxable income to ₹5 lakh. Only then does the old-regime rebate of up to ₹12,500 apply. Verify current thresholds before planning.

What is Form 16 and why do I need it to file my ITR?

Form 16 is the official tax certificate issued by your employer by June 15 each year. It contains two parts: Part A shows your TDS details as per TRACES, and Part B shows your salary breakdown — gross income, exemptions, deductions, taxable income, and TDS deducted. For an ₹8 LPA employee, Form 16 is the primary input for your ITR. If you changed jobs, you need Form 16 from every employer you worked with during the year.

What happens if I don’t file my ITR even if my tax is nil?

If your gross income exceeds the basic exemption limit, you are generally required to file an ITR — even if your final tax after rebate is nil. Not filing can attract a late filing fee of ₹1,000 to ₹5,000 depending on when you file and your income level. More immediately, you cannot claim a TDS refund without filing — and if your employer over-deducted TDS, that money sits with the government until you claim it through your ITR. Verify current penalty and filing rules at incometax.gov.in.

Can I switch from the new regime to the old regime when filing my ITR?

Salaried employees without business income can generally switch between regimes at the time of filing their ITR — even if their employer deducted TDS under a different regime during the year. This flexibility allows you to choose whichever regime gives a lower tax based on your actual full-year figures. However, the rules governing this switching option can change. Always verify the current switching conditions from incometax.gov.in or a qualified tax professional before assuming you can change.

How does health and education cess affect my ₹8 LPA tax?

Health and education cess is 4% of your tax payable after rebate. It applies to all taxpayers and cannot be reduced through any deduction, investment, or exemption. If your tax after Section 87A rebate is ₹0 — as in the new-regime case for ₹8 LPA with no extra income — cess is ₹0. If your old-regime tax is ₹62,500, the cess adds ₹2,500, bringing total payable to ₹65,000. Cess is always the final step in the calculation.

Final Verdict

For most salaried employees earning ₹8 LPA in FY 2025–26, the new tax regime is the simpler and more financially rewarding option. After standard deduction and the Section 87A rebate, the tax on 8 LPA salary can be nil — with no investment commitments, no proof submissions, and no planning complexity. If you have significant deductions — a home loan, consistent HRA claims, maximum 80C, and NPS contributions exceeding ₹2.5 lakh combined — the old regime may match or occasionally beat this outcome, but it requires deliberate planning and annual proof maintenance. Start by checking your actual deductions for the year, then run both regimes through a salary tax calculator before deciding.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.