If your salary is ₹6,00,000 a year, the question you are probably asking right now is: will I actually have to pay income tax — or not? Tax on 6 LPA salary is one of the most searched questions by first-job and early-career employees in India, and the confusion is completely understandable.

The answer depends on more than just the number on your offer letter. It changes based on which tax regime your employer uses, whether the standard deduction has been applied, whether Section 87A rebate applies to you, and whether you have any income beyond salary. It also hinges on something many beginners miss entirely: CTC, gross salary, and taxable income are three different numbers — and only one of them determines your actual tax.

This article walks you through the exact calculation path for both the new and old regime, a real worked example with specific ₹ figures, and the conditions under which your final tax at ₹6 LPA could be zero.

Quick Answer: Tax on 6 LPA Salary

Tax on 6 LPA salary may be zero under the new tax regime if your taxable income qualifies for Section 87A rebate after standard deduction. Under the old regime, tax depends on deductions like 80C, HRA, and other exemptions. In both cases, employer TDS may still be deducted if your declarations are missing or the regime is not declared. Verify your specific numbers using a salary tax calculator before filing.

Key Takeaways

- A ₹6 LPA salary does not automatically mean tax is payable — the regime chosen, applicable deductions, and Section 87A rebate eligibility all determine the final amount.

- Under the new tax regime, a standard deduction of ₹75,000 reduces ₹6,00,000 gross salary to ₹5,25,000 taxable income — bringing slab tax to just ₹6,250.

- Section 87A rebate under the new regime can offset that ₹6,250 in full if your total taxable income is within the prescribed threshold — resulting in zero final tax.

- Under the old regime with no additional deductions, tax on ₹5,50,000 taxable income works out to ₹23,400 including 4% cess — because the old regime 87A rebate does not apply above ₹5,00,000.

- Old regime can also produce zero tax if 80C investments, HRA, and other eligible deductions bring taxable income to ₹5,00,000 or below.

- TDS deducted by your employer is not the same as your final tax liability — over-deduction can be reclaimed as a refund when you file your ITR.

- CTC and taxable salary are different numbers — employer PF, gratuity, and perquisites affect what actually gets taxed.

Key Facts at a Glance

| Item | New Tax Regime | Old Tax Regime |

|---|---|---|

| Gross Salary Considered | ₹6,00,000 | ₹6,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income (no extra deductions) | ₹5,25,000 | ₹5,50,000 |

| Slab Tax Before Rebate | ₹6,250 | ₹22,500 |

| Section 87A Rebate Available? | Yes — income within threshold | No — income exceeds ₹5 lakh limit |

| Health & Education Cess (4%) | ₹0 | ₹900 |

| Final Tax Payable | ₹0 | ₹23,400 |

Assumptions: Salary is the only income source. No other deductions or exemptions are claimed in the old regime column. Real results depend on your salary structure, declarations, and total annual income.

How Income Tax Is Calculated on a ₹6 LPA Salary

CTC, Gross Salary, and Taxable Income Are Three Different Figures

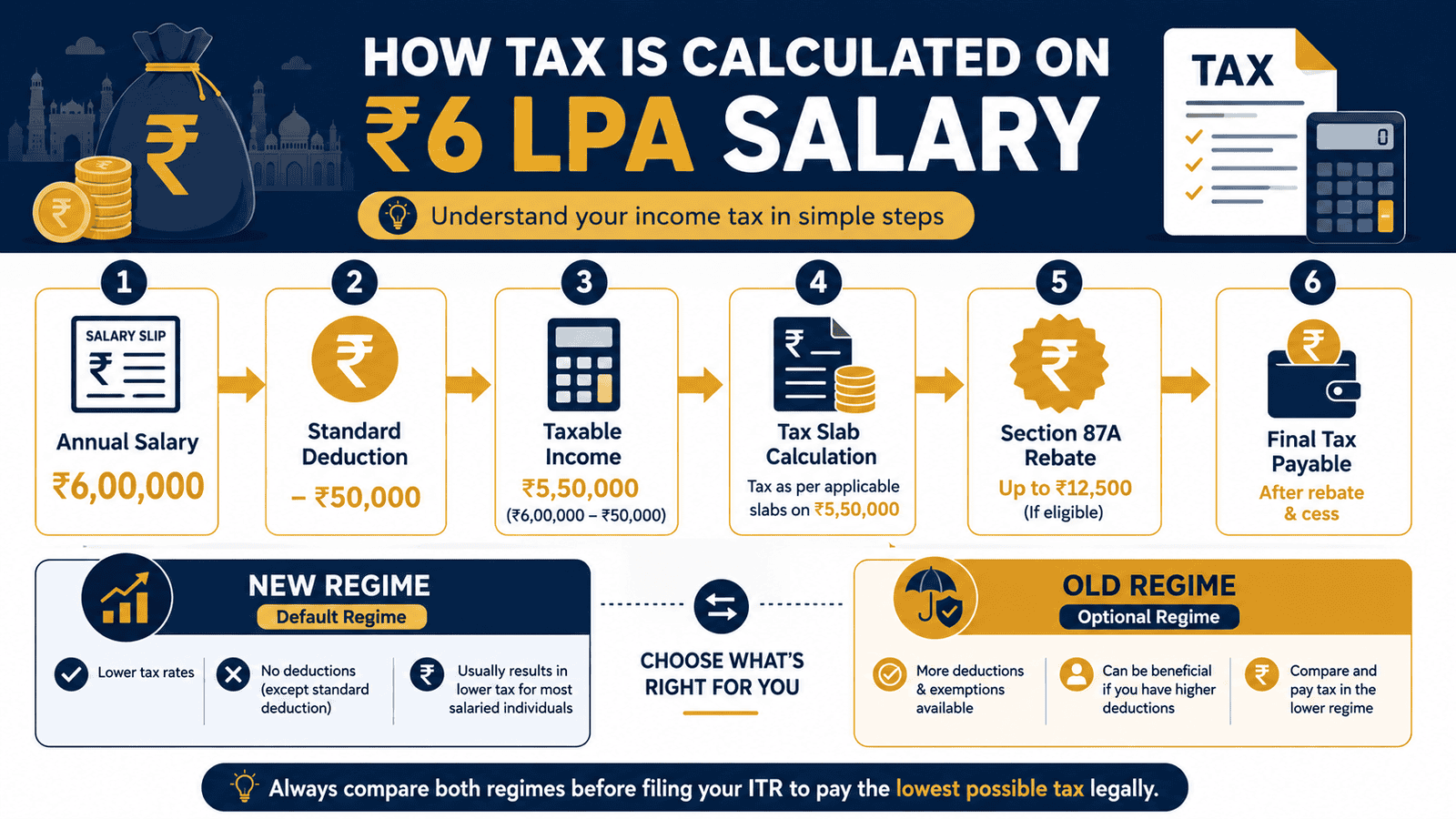

The most common mistake beginners make is assuming the ₹6 LPA number on their offer letter goes directly into the tax calculation. It does not. Your CTC — cost to company — includes employer contributions to PF, gratuity provisions, and other cost items that are not part of your personal taxable income. Gross salary is what appears on your payslip before deductions. Taxable salary is what remains after allowable deductions are applied.

On a ₹6 LPA CTC, your gross salary might actually be ₹5.6–5.8 lakh after accounting for the employer PF portion. The tax is calculated on taxable income — not on the headline package. See the salary and CTC guide for how these numbers connect and where to find each figure in your payslip.

Standard Deduction Reduces Your Taxable Salary Automatically

Every salaried employee gets a flat standard deduction subtracted from salary income before any tax is calculated. You do not need to submit proof or make any investment to claim it — your employer applies it automatically. Under the new tax regime, the standard deduction is ₹75,000 per year. Under the old regime, it is ₹50,000 per year.

On a ₹6,00,000 gross salary, this produces:

- New regime: ₹6,00,000 − ₹75,000 = ₹5,25,000 taxable income

- Old regime: ₹6,00,000 − ₹50,000 = ₹5,50,000 taxable income (before any further deductions)

This one deduction already makes a meaningful difference to the slab calculation. For a deeper explanation of how it works across regimes, read the standard deduction meaning guide.

How Slabs Calculate Tax on Taxable Income

Slabs work progressively. Only the slice of income that falls within each band is taxed at that band’s rate — not the entire income. Under the new regime for FY 2025-26, the first ₹4,00,000 of taxable income is nil. The band from ₹4,00,001 to ₹8,00,000 is taxed at 5%.

On a new-regime taxable income of ₹5,25,000:

- First ₹4,00,000 — nil

- Next ₹1,25,000 (₹4,00,001 to ₹5,25,000) at 5% — ₹6,250

Under the old regime, the bands are narrower and the rates step up faster. Income from ₹2,50,001 to ₹5,00,000 is taxed at 5%, and income from ₹5,00,001 to ₹10,00,000 is taxed at 20%. On ₹5,50,000 taxable income, the slab calculation reaches ₹22,500 — nearly four times the new-regime figure — before cess or rebate.

How Section 87A Rebate Can Bring Final Tax to Zero

Section 87A is a rebate — not an exemption, and not a deduction. The distinction matters. Your income is still computed under slabs and a tax figure is arrived at. Then, if your total taxable income is within the eligibility threshold, the government allows a rebate that reduces the actual tax payable to zero.

Under the new regime, if taxable income is at or below the prescribed threshold, a rebate of up to ₹60,000 applies. Since the slab tax on ₹5,25,000 is only ₹6,250 — well within that cap — the entire ₹6,250 is offset. Final tax: ₹0. Under the old regime, the rebate threshold is ₹5,00,000 and the maximum rebate is ₹12,500. At ₹5,50,000 taxable income (no extra deductions), old-regime income exceeds that threshold and no rebate applies.

This distinction is also important for TDS and ITR: your income is not technically “exempt” — it is computed and then rebated. Form 16 and your ITR should still reflect the full salary income correctly.

Cess Is Calculated Only on Tax After Rebate

Health and Education Cess at 4% is applied to the tax payable after any rebate is deducted — not to taxable income directly. If tax after 87A is ₹0, cess is ₹0. If tax payable is ₹22,500 (old regime, no deductions), cess adds ₹900 — making total liability ₹23,400. This is why the full tax figure always comes last in the calculation chain.

New Regime Under Section 115BAC

The new tax regime under Section 115BAC is now the default option for salaried employees. If you do not declare a preference to your employer, TDS is typically computed under this regime. The old regime remains available but must be actively opted into. For salaried employees filing ITR, the regime can be selected at the time of filing — though it should match the declarations submitted to the employer to avoid TDS discrepancies.

Real Example: Rahul’s First Tax Year on ₹6 LPA

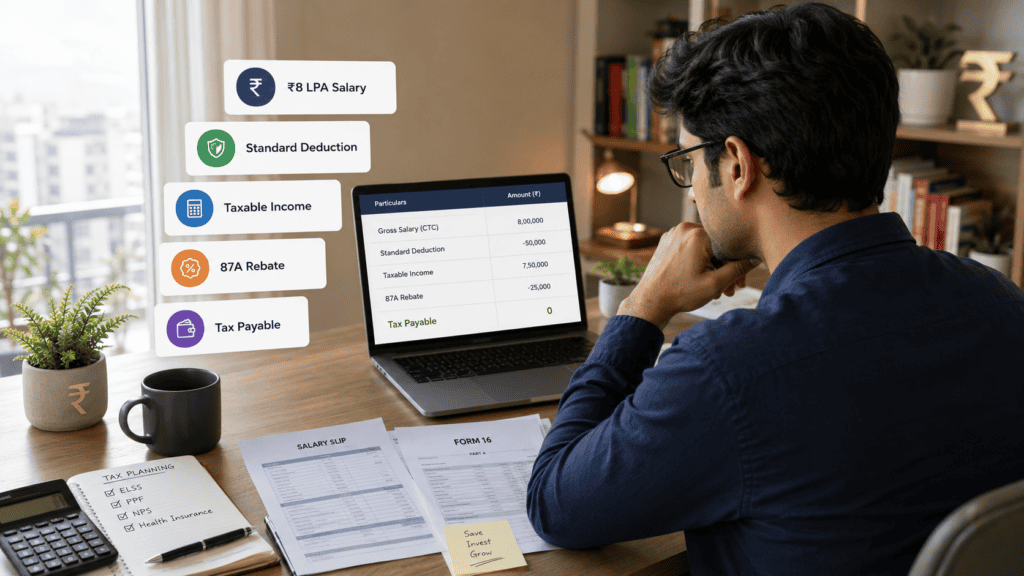

Rahul is 26, a junior software engineer at a mid-size IT firm in Pune. His offer letter shows a ₹6,00,000 annual CTC. After the employer PF contribution is excluded, his gross salary is ₹5,64,000 — but for this illustration we use the full ₹6,00,000 to keep the slab calculation clean.

Rahul is under the new tax regime (the default). His employer applies the standard deduction of ₹75,000, bringing taxable income to ₹5,25,000. Under the new-regime slabs, the slab tax works out to ₹6,250. Rahul’s total income for the year is only his salary — no rental income, no capital gains, no freelance. So his income is within the 87A rebate threshold, and the ₹6,250 is fully offset. Final income tax: ₹0.

His monthly in-hand is still not ₹50,000, because his employer deducts his share of PF (12% of basic), professional tax of ₹200 per month, and a group health insurance premium. To see the exact monthly breakdown for your salary structure, use the take-home salary calculator.

Key insight: Rahul pays zero income tax — but his take-home is still reduced by PF and professional tax, which are entirely separate from the income tax calculation.

How to Calculate Tax on 6 LPA Salary — Both Regimes

Taxable Income = Gross Salary − Standard Deduction − Other Eligible Deductions

Tax Payable = Slab Tax on Taxable Income − Section 87A Rebate

Final Tax = Tax Payable + 4% Health & Education Cess

New Regime — Step by Step

Step 1: Gross Salary = ₹6,00,000

Step 2: Less standard deduction ₹75,000 → Taxable Income = ₹5,25,000

Step 3: Slab tax = 5% × ₹1,25,000 (band from ₹4L to ₹5.25L) = ₹6,250

Step 4: Section 87A rebate = ₹6,250 (income within threshold; rebate offsets tax in full)

Step 5: Cess = 4% × ₹0 = ₹0 → Final Tax Payable = ₹0

Old Regime — Step by Step (No Additional Deductions)

Step 1: Gross Salary = ₹6,00,000

Step 2: Less standard deduction ₹50,000 → Taxable Income = ₹5,50,000

Step 3: Slab tax = (5% × ₹2,50,000) + (20% × ₹50,000) = ₹12,500 + ₹10,000 = ₹22,500

Step 4: Section 87A rebate = Nil (income exceeds ₹5,00,000 threshold under old regime)

Step 5: Cess = 4% × ₹22,500 = ₹900 → Final Tax Payable = ₹23,400

| Scenario | Taxable Income | Final Tax Payable |

|---|---|---|

| New regime, no extra deductions | ₹5,25,000 | ₹0 |

| Old regime, no extra deductions | ₹5,50,000 | ₹23,400 |

| Old regime, ₹50,001+ in 80C/HRA deductions | ₹5,00,000 or below | ₹0 (87A rebate applies) |

For your specific salary, deductions, HRA amount, and other income, verify the final figure using the income tax calculator. And for a full breakdown of rebate conditions, eligibility limits, and what types of income it covers, read the Section 87A rebate guide.

Comparison: New Regime vs Old Regime for ₹6 LPA

| Parameter | New Tax Regime | Old Tax Regime |

|---|---|---|

| Standard Deduction | ₹75,000 | ₹50,000 |

| Taxable Income at ₹6 LPA | ₹5,25,000 | ₹5,50,000 (before extra deductions) |

| Deductions allowed (80C, HRA, NPS etc.) | Not available | Available |

| Section 87A Rebate | Up to ₹60,000 (income within threshold) | Up to ₹12,500 if income ≤ ₹5 lakh |

| Final Tax at ₹6 LPA (no extra deductions) | ₹0 | ₹23,400 |

| Final Tax at ₹6 LPA (old regime with ₹50,001+ deductions) | N/A | ₹0 |

| Best suited for | Low-deduction earners, simplicity | HRA, 80C, NPS, LTA claimants |

Note: Figures are illustrative for a resident individual with salary as the only income source. Tax rules are based on provisions for FY 2025-26. Verify current slabs and thresholds from incometax.gov.in before filing.

How to Decide What’s Right for You

Your gross salary is ₹6,00,000, you have no HRA, no major 80C investments to claim, and no rent receipts to submit — THEN the new regime gives you zero tax with zero paperwork. There is no benefit to switching to the old regime in this case.

You pay rent and receive HRA as a salary component — THEN calculate the HRA exemption under the old regime first. If HRA exemption alone brings your taxable income close to ₹5,00,000, adding even modest 80C deductions can trigger the 87A rebate and give you zero tax under the old regime too.

Your combined 80C investments (EPF, ELSS, PPF, life insurance premiums) total ₹50,001 or more — THEN compare both regimes numerically before April. At ₹6 LPA, this level of deduction under the old regime often delivers zero tax — the same outcome as the new regime, with the added benefit of actual investment growth.

You have interest income from savings, an FD, or any freelance earnings in addition to your salary — THEN your total income may push above the 87A rebate threshold under the new regime. Do not assume zero tax until you include all income sources in the calculation.

You cannot produce rent receipts, investment proofs, or other deduction documents before the employer deadline — THEN the new regime eliminates that admin burden entirely, and at ₹6 LPA you still pay zero tax in most cases.

You are a resident individual for the entire financial year — for example, you are classified as an NRI for FY 2025-26 — THEN Section 87A rebate does not apply to you, and a different tax treatment governs your salary income. Consult a qualified tax professional for NRI salary taxation.

Common Mistakes to Avoid

Treating ₹6 LPA CTC as Your Taxable Income

Many first-job employees assume the package number on their offer letter is directly what gets taxed.

CTC includes employer PF contributions, gratuity provisions, and other costs that do not form part of your personal taxable salary. The actual taxable figure is your gross salary minus standard deduction — and it is often meaningfully lower. Treating CTC as taxable income makes your estimated tax look higher than it actually is, and can cause unnecessary stress.

Check your payslip carefully to identify which components your employer counts as taxable salary. The CTC vs in-hand guide explains each component and where it appears.

Not Knowing Which Regime Your Employer Is Using

Since the new regime became the default, many employees assume their TDS is being calculated correctly without checking.

If you intended to use the old regime and did not declare it to your employer in time, TDS will be computed under the new regime — and you may miss old-regime deductions for the year. Check your salary slip’s TDS line and ask HR which regime is applied to your account.

Declare your regime preference in writing at the start of every financial year — do not assume last year’s preference carries forward automatically.

Assuming Section 87A Rebate Applies to Capital Gains

Section 87A rebate applies to tax on salary and regular income taxed at slab rates — not to tax on special-rate income such as short-term capital gains under Section 111A or long-term capital gains under Section 112A.

If you sold mutual fund units or stocks during the year and earned ₹15,000 in capital gains, that tax remains payable separately — even if your salary income alone qualifies for zero tax. Add all income types before concluding your total tax liability is zero.

Skipping Investment Declarations to the Employer

Under the old regime, failing to submit proof of 80C investments, rent receipts, or NPS contributions to your employer by January-February means your employer computes TDS without those deductions.

The result is excess TDS — money you can only recover by filing ITR and waiting for a refund. Submit declarations on time, in the format your employer requires, with supporting documents ready.

Confusing TDS With Final Tax Payable

TDS is an estimated advance tax deducted month by month throughout the year. It is not your final tax. If excess TDS is deducted, you get a refund. If too little is deducted, you pay the balance at ITR time — along with possible interest under Sections 234B and 234C.

Always reconcile TDS shown in Form 16 against your actual calculated tax before filing. They are not always the same.

Forgetting Bonus and Variable Pay in the Tax Estimate

A ₹50,000 performance bonus on top of ₹6 LPA base takes annual gross salary to ₹6,50,000. Under the new regime, the slab tax on that increases and must be recalculated. Your employer typically adjusts TDS when the bonus is paid, but if they do not, the shortfall falls on you at ITR time.

Include your expected bonus in any annual tax estimate from April onwards — do not calculate only on fixed salary.

When This May Not Be the Right Choice

The zero-tax conclusion for ₹6 LPA depends on specific conditions that may not apply to everyone:

- You have interest income, rental income, or freelance earnings in addition to salary — pushing your total taxable income above the Section 87A rebate threshold.

- Your bonus, arrears, or variable pay took your actual annual income above ₹6,00,000 during the year, changing the slab calculation.

- You have short-term or long-term capital gains from stocks or mutual funds that are taxed at special rates — these are not offset by the salary rebate.

- You are classified as a non-resident individual for the financial year — Section 87A rebate and certain slab structures differ for NRIs.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Income tax slabs, standard deduction amounts, Section 87A rebate thresholds, and cess rates are set by Parliament through the Finance Act each year. They can — and do — change with every Budget. The figures used in this article are based on the provisions applicable for FY 2025-26 (AY 2026-27) as per the information available at the time of writing.

- Income Tax Department — incometax.gov.in (tax slabs, ITR filing, Form 26AS, AIS, refund tracking)

- CBDT (Central Board of Direct Taxes) — incometax.gov.in (Budget notifications, circulars, ITR validation rules)

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Ask your HR or payroll team for a full salary component breakup at the start of April — specifically which components are taxable and which are exempt. This affects your TDS from month one, not just at year-end when it is too late to plan.

- Compare both regimes using a tax calculator before your employer locks in your preference. Many employers ask for regime declaration in April or May — if you miss the window, changing mid-year is complex and the TDS computed may not match your final return.

- If you are in the old regime and pay rent, collect rent receipts every month and note the landlord’s PAN if annual rent to one landlord exceeds ₹1,00,000. Missing the PAN invalidates the HRA claim during processing.

- Check your Form 26AS and AIS (Annual Information Statement) on the e-filing portal before filing ITR. If your employer has reported a different salary figure from what you expect, reconcile it before submitting — mismatches trigger notices.

- Do not rely on social media posts or year-old tax articles for calculations. Slabs and rebate limits change every Budget. A figure that was accurate in February may already be superseded by the time you file in July. Always verify from incometax.gov.in.

- If you have savings account interest, FD interest, or any freelance income in addition to salary — even small amounts — include them in your annual income estimate early. They may affect whether the 87A rebate applies to you in full.

Frequently Asked Questions

Is ₹6 LPA salary tax-free in India?

Under the new tax regime for FY 2025-26, a resident individual salaried employee with no other income typically pays zero final income tax at ₹6 LPA — after applying standard deduction and Section 87A rebate. However, “tax-free” is not a guaranteed or absolute status. The result depends on your total income, regime chosen, and whether you qualify for rebate. Under the old regime without sufficient deductions, ₹6 LPA is not tax-free.

How much tax on ₹6 lakh salary in new regime?

Under the new regime for FY 2025-26, the standard deduction of ₹75,000 brings taxable income to ₹5,25,000. Slab tax on this is ₹6,250. If your total taxable income is within the Section 87A threshold, the ₹6,250 is fully rebated and final tax is ₹0. If you have additional income that pushes you above the threshold, cess of 4% also applies on the tax payable.

How much tax on ₹6 lakh salary in old regime?

Under the old regime with no additional deductions, taxable income after the ₹50,000 standard deduction is ₹5,50,000. Slab tax is ₹22,500, Section 87A rebate does not apply (income exceeds ₹5 lakh), and 4% cess adds ₹900 — giving a final tax of ₹23,400. If deductions like 80C, HRA, or NPS reduce taxable income to ₹5,00,000 or below, the old regime 87A rebate (up to ₹12,500) may bring final tax to zero.

Will my employer deduct TDS on a ₹6 LPA salary?

If you are under the new regime, declared your preference to your employer, and have no additional income, your employer should compute zero tax — meaning no TDS deduction from salary. However, if you have not declared your regime preference, if your employer calculates on a higher estimated income, or if your salary structure includes taxable perquisites, TDS may still be deducted. Always submit your regime declaration and investment information on time at the start of the financial year.

Is 6 LPA before tax or after tax?

The ₹6 LPA figure on your offer letter is always before tax. It is either CTC or gross salary, depending on how the employer presents the package. Your actual monthly in-hand will be lower — reduced by PF contributions, professional tax, health insurance premiums, and income tax TDS if applicable. The term “in-hand salary” refers to what is credited to your bank account after all deductions.

What is the monthly in-hand salary for 6 LPA?

There is no single figure — it depends on your salary structure, employer PF policy, professional tax applicable in your state, and any group insurance deductions. For a ₹6 LPA gross salary with zero income tax liability under the new regime, monthly in-hand typically falls between ₹42,000 and ₹48,000. Use a take-home salary calculator with your actual components for a more accurate number.

Can I get a refund if TDS is deducted on my ₹6 LPA salary?

Yes. If your employer deducted TDS but your final tax liability works out to zero after applying standard deduction and Section 87A rebate, you are entitled to a full refund of the TDS amount. File your ITR, declare all income accurately, and the Income Tax Department will process the refund to your pre-validated bank account. Make sure your bank account is linked and verified on the e-filing portal before filing.

What happens if I choose the wrong tax regime at ₹6 LPA?

If you choose the old regime but cannot provide investment or rent proof to your employer, TDS is calculated without those deductions and you pay more tax upfront than needed — though you can reclaim it as a refund when filing ITR. If you choose the new regime but had significant HRA and 80C that would have saved more in the old regime, you lose that opportunity for that financial year. For salaried employees, the regime declared to the employer early in the year determines TDS — switching at ITR filing is allowed but requires recalculating and possibly paying any shortfall.

Does Section 87A rebate apply to all types of income at ₹6 LPA?

No. Section 87A rebate reduces tax on income taxed at normal slab rates — salary, interest income, business income, and similar. It does not offset tax on special-rate incomes such as short-term capital gains taxed under Section 111A (15%) or long-term capital gains taxed under Section 112A (10% above ₹1,25,000). If you had stock market or mutual fund gains in the year, those are computed and taxed separately even if your salary income qualifies for zero tax under 87A.

Final Verdict

For most salaried employees earning ₹6 LPA with no other income, tax on 6 LPA salary under the new regime works out to zero — after standard deduction and Section 87A rebate offset the ₹6,250 slab calculation entirely. The new regime is simpler, requires no investment proof, and produces the same zero-tax result for low-deduction earners without the admin burden of the old regime.

The old regime can also produce zero tax — but only if 80C, HRA, or other eligible deductions bring taxable income to ₹5,00,000 or below. That takes active planning, document collection, and a proper comparison before the employer’s declaration deadline.

The right starting point is knowing how your salary is structured and what your total annual income looks like across all sources. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.