You are browsing online and the checkout page gives you two options: pay with your credit card, or split the purchase into easy instalments with a BNPL service. Both look convenient. Neither feels like real spending in the moment. That is exactly the trap.

BNPL — Buy Now Pay Later — has expanded rapidly across Indian e-commerce, travel, and app-based purchases. At the same time, credit cards remain the go-to short-term credit tool for most salaried employees. Both are credit. Both carry costs. Both can damage your CIBIL score if you miss repayments.

This article compares BNPL vs credit card in India across repayment structure, costs, CIBIL impact, acceptance, and risk — so you can make a clear-headed decision at checkout, not a rushed one.

Quick Answer: BNPL vs Credit Card

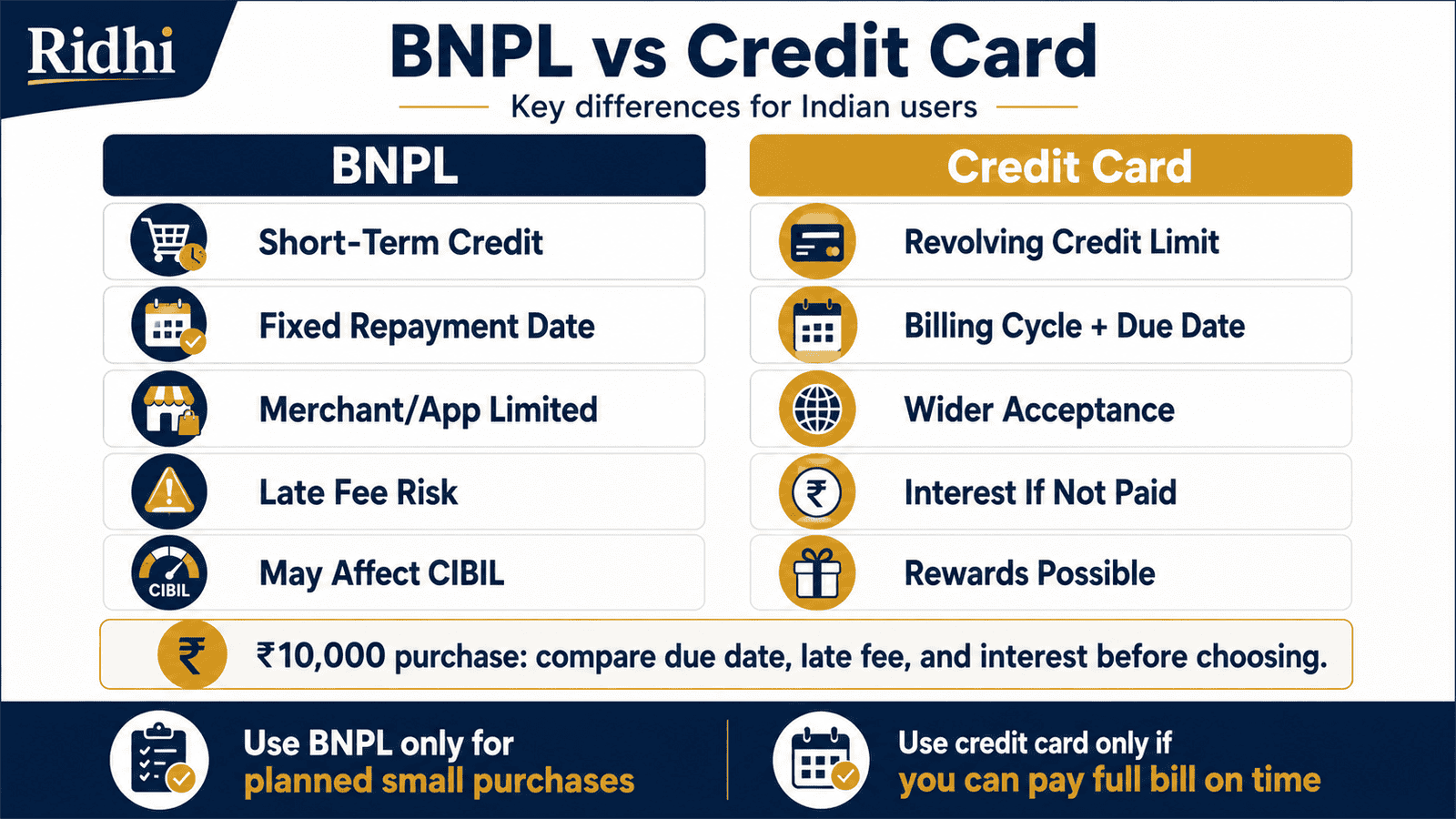

BNPL vs credit card mainly differs in repayment structure, flexibility, acceptance, rewards and penalty risk. BNPL is usually useful for small planned purchases split into short repayments, while a credit card offers wider acceptance, billing-cycle flexibility and rewards. For a ₹10,000 purchase, compare due date, fees, interest and CIBIL impact before choosing.

Key Takeaways

- BNPL works best only when you know exactly when your income will arrive and the repayment date aligns with it — unplanned BNPL use leads to cascading due dates.

- Credit cards offer an interest-free period only when you pay the full outstanding amount before the due date — pay less, and interest typically applies to the entire balance.

- BNPL often lacks rewards, cashback, or lounge access that many credit cards offer — the “convenience” may cost more than you save.

- Missing even one BNPL instalment can trigger a late fee and, if the provider reports to credit bureaus, a negative mark on your CIBIL report.

- Managing five small BNPL dues across different apps is harder than managing one credit card bill — multiple due dates increase miss risk significantly.

- Both BNPL and credit cards are short-term credit, not additional income — using either for lifestyle inflation will compound into debt.

- Provider-specific charges, late fees, interest rates, and credit reporting practices vary and can change without notice — always read the Most Important Terms and Conditions (MITC) before using either product.

BNPL vs Credit Card: Side-by-Side Comparison

| Parameter | BNPL | Credit Card |

|---|---|---|

| Repayment style | Fixed instalments or single due date set by provider | Revolving credit — pay full, minimum, or any amount between |

| Interest-free period | Usually zero-cost if paid on time, but conditions apply per provider | Up to 45–50 days if full bill paid before due date; varies by card and cycle |

| Cost if late | Late fee per provider terms; may also attract interest or processing charge | Late payment fee + interest on full outstanding at 2%–4% per month (varies by issuer) |

| Acceptance | Limited to partner merchants and apps; not widely accepted offline | Widely accepted — online, offline POS, international (subject to card network) |

| Rewards and benefits | Usually none or minimal; provider-specific cashback on select merchants | Reward points, cashback, lounge access, insurance, offers — varies by card |

| CIBIL / credit score impact | Depends on whether provider reports to bureaus; missed payments can hurt score | Reported to credit bureaus — payment history and utilisation both affect CIBIL |

| Credit limit | Usually lower; set by provider based on profile; may reduce if misused | Higher limit possible; based on income, credit history, issuer policy |

| Eligibility | Often easier — some providers approve with limited credit history | Requires income proof, credit history; stricter for first-time applicants |

For a deeper look at how card EMI compares as a borrowing option, see credit card EMI vs personal loan. Note: rates, fees, rewards, and features listed above can change without notice — verify with your specific provider before using either product.

Key Facts at a Glance

| Factor | Detail |

|---|---|

| Product type | Short-term credit facility — not a salary advance or free purchase |

| Common use cases | Online shopping, electronics, travel booking, app-based purchases, emergency buys |

| Main financial risk | Overspending beyond repayment capacity and missing due dates |

| Cost triggers | Late fee, interest/finance charge, processing fee, GST on charges — varies by provider |

| Credit bureau reporting | Credit cards: always reported. BNPL: depends on provider — check MITC |

| Regulatory oversight | Credit cards: RBI-regulated. BNPL: regulated under RBI digital lending guidelines |

| Verification source | RBI (rbi.org.in), bank/card issuer MITC, BNPL provider terms and conditions |

How BNPL and Credit Cards Actually Work in India

Understanding where these two products differ at a structural level will help you see through the marketing and focus on the actual cost and risk.

What BNPL Means in India

Buy Now Pay Later is a short-term credit arrangement where a bank or NBFC (Non-Banking Financial Company) pays the merchant on your behalf. You repay the provider — either in a lump sum on a fixed due date, or in instalments over a set period. Products like LazyPay, ZestMoney (check current availability), Simpl, and credit-line features offered by apps like Amazon Pay Later or Flipkart Pay Later are common examples in India.

BNPL approval can be faster and easier than a credit card because some providers use alternative data to assess creditworthiness. That lower barrier to entry is convenient — but it also makes it easier to take on credit without fully realising it. RBI’s digital lending guidelines, updated in recent years, now require regulated entities offering BNPL-style products to follow clearer disclosure and repayment norms. Always check whether your BNPL provider is RBI-regulated or operates through a regulated partner.

What a Credit Card Actually Is

A credit card gives you access to a revolving credit limit. You spend, a billing cycle closes (typically monthly), and a statement is generated. You then have a grace period — usually around 18–25 days after the statement date — to pay the full outstanding amount without any interest. Understand how your billing cycle and due date work before spending on a card, because if you pay even one rupee less than the full amount, interest typically applies on the entire statement balance — not just the remaining unpaid portion, on most cards.

Revolving Credit vs Fixed Instalment

This is the most important structural difference. BNPL locks you into a fixed repayment schedule — you either meet it or pay a penalty. A credit card offers flexibility: you can pay the full bill, a partial amount, or just the minimum due. That flexibility sounds like freedom. In practice, it is a trap for anyone who does not have the discipline to pay in full every month. The minimum due option keeps the account active but triggers interest charges that compound aggressively over time.

The “Interest-Free” Claim on Both Products

Both BNPL and credit cards market themselves as zero-cost if used correctly. For BNPL, “interest-free” usually means you pay no extra charge if you repay on the fixed due date — but processing fees, convenience charges, or GST may still apply. For a credit card, the interest-free period applies only when the entire statement balance is paid before the due date. Pay less, and the interest clock starts on the full statement amount from the transaction date on most cards, not the due date. Neither product is truly free if you miss the full payment condition.

Real Example: Rohit’s ₹10,000 Purchase in Pune

Rohit, 28, works as a software engineer in Pune earning ₹75,000 per month. He needs to buy a ₹10,000 item — say, a pair of noise-cancelling headphones — and has two options at checkout.

BNPL path: Rohit selects pay-later. The provider approves instantly. He gets a due date 15 days later for ₹10,000, or a 3-instalment option splitting the amount into three monthly payments. If his salary arrives before the due date and he pays on time — total cost is ₹10,000 (or slightly more if a processing or convenience fee applies — verify with your provider). If he misses the due date, a late fee kicks in — the exact amount varies by provider and can change without notice.

Credit card path: Rohit swipes his credit card. The ₹10,000 appears on his next statement. If his billing cycle ends in 10 days and his due date is 20 days after that, he has 30 days total to pay ₹10,000 with zero interest. If he pays in full — total cost is ₹10,000. If he pays only the minimum due — interest at the card’s monthly rate (typically 2%–4% per month, verify with your issuer) applies to the remaining balance, compounding each month. For a full breakdown of how card interest is calculated, see how credit card interest is calculated in India.

Key insight: Both options cost ₹10,000 if Rohit pays in full on time. The difference emerges only at the point of failure — missed or partial payment. BNPL has a hard, fixed penalty. A credit card can spiral if only the minimum due is paid month after month.

How to Calculate Total Repayment Cost

Total Cost = Purchase Amount + Processing / Convenience Fee + Interest / Finance Charge + Late Fee + GST on Charges

Using a ₹10,000 purchase as the base:

| Scenario | Assumption | Approximate Total Cost |

|---|---|---|

| BNPL — paid on time | No processing fee (verify with provider); no late charge | ₹10,000 or slightly more if fees apply |

| BNPL — missed due date | Late fee per provider terms (verify); no interest assumed | ₹10,000 + late fee (provider-specific) |

| Credit card — full payment on time | No interest; within interest-free period | ₹10,000 |

| Credit card — minimum due paid for 3 months | Interest at ~3% per month on outstanding (illustrative; verify with issuer) | ₹10,000 + ~₹900–₹1,000+ in interest (compounding) |

These figures are illustrative. Actual processing fees, late charges, and interest rates vary by provider and card issuer — and can change without notice. Use the credit card interest calculator to model your actual card’s cost for any outstanding amount. For “no-cost EMI” or zero-interest BNPL offers: read the fine print — some schemes involve a processing fee, or the merchant inflates the MRP to cover the cost.

How to Decide What’s Right for You

You are buying something small (under ₹5,000–₹10,000), the BNPL due date falls before your next salary credit, and you have zero outstanding BNPL dues — THEN BNPL may be a convenient, low-risk option for this purchase.

You pay your credit card bill in full every month without fail — THEN a credit card is likely the better option: you get rewards, wider acceptance, and the same zero-cost outcome with more flexibility.

You already have two or more active BNPL dues running simultaneously — THEN adding another BNPL purchase increases your miss risk significantly. Consolidate before adding more.

You have a history of paying only the minimum due on your credit card — THEN the card’s revolving credit feature is actively costing you money. Address this before using the card for new purchases.

You are new to credit and unsure which product to start with — THEN explore a starter credit card with a low limit before taking on BNPL across multiple apps. A single billing cycle is easier to track than multiple BNPL due dates.

The purchase is a want rather than a need and you have no immediate income to repay — THEN neither BNPL nor a credit card is appropriate for this purchase. Use savings instead.

You cannot clearly answer “how will I repay this by the due date?” — do not choose either option. Deferred payment products do not solve a cash flow problem; they delay and worsen it.

If you are deciding between starting with a credit card or BNPL as your first credit product, the guide on how to choose your first credit card in India can help you evaluate your options clearly.

Common Mistakes to Avoid

Treating BNPL as Free Money

BNPL is not a salary advance or a gift — it is credit extended by a bank or NBFC.

Every BNPL transaction creates a repayment obligation with a fixed due date. If you miss it, you pay a late fee and potentially get a negative credit mark. Over time, treating BNPL as a spending supplement rather than a repayment commitment leads to ballooning dues across multiple apps.

Before using BNPL, confirm the exact repayment date and ensure incoming salary or income covers it without disrupting other obligations.

Juggling Multiple BNPL Due Dates Across Apps

Each BNPL app has its own due date, late fee structure, and repayment rules.

A salaried user with active dues on three BNPL apps — say ₹3,000 on one, ₹4,500 on another, and ₹6,000 on a third — faces ₹13,500 in fragmented credit obligations, each with different deadlines. Missing any one creates a fee and credit risk. Most people underestimate how quickly this adds up.

Cap your active BNPL obligations to what you can fully repay in the current month.

Paying Only the Minimum Due on a Credit Card

The minimum due on a credit card statement is typically 5% of the total outstanding or a fixed floor amount — whichever is higher.

Paying only the minimum keeps the account active but triggers interest on the remaining balance at the card’s monthly rate — often 2%–4% per month (verify with your issuer). On a ₹50,000 balance, that is ₹1,000–₹2,000 in interest every month, compounding. Understand why paying only the minimum due is dangerous before treating it as a legitimate repayment strategy.

Always pay the full statement balance. If you cannot, pay as much above the minimum as possible and avoid new purchases until cleared.

Ignoring Your Credit Utilisation Ratio

Your credit utilisation ratio — the percentage of your total available credit limit that you are currently using — is one of the key factors in your CIBIL score.

Using a high proportion of your credit card limit (above 30%–35% as a general guideline) can reduce your score, even if you pay on time. Similarly, if your BNPL provider reports your credit line usage to bureaus, high utilisation on that facility may also affect your score. Learn how credit utilisation ratio affects your CIBIL score before maxing out either product.

Keep total credit usage well below your combined limit at all times.

Assuming BNPL Never Affects Your CIBIL Score

Not all BNPL providers currently report to credit bureaus — but many do, or may do so in the future as RBI’s digital lending guidelines evolve.

A missed BNPL repayment with a reporting provider will appear on your credit report just like a missed credit card payment. Assuming BNPL is invisible to CIBIL and using it carelessly is a mistake that can silently damage your credit profile.

Check your BNPL provider’s MITC or terms to understand their bureau-reporting policy before treating it as a score-free product.

Not Reading BNPL Charges, Processing Fees, and Late Fee Rules

BNPL products are often marketed as “zero-cost” or “no interest” — which can be true under specific conditions.

However, some BNPL products include a processing or convenience fee per transaction, GST on charges, or penalty charges that are significantly higher than a credit card late fee. A ₹500 late fee on a ₹1,500 BNPL purchase is a 33% penalty — far worse than the equivalent credit card charge in many cases. Always read the full charge schedule before activating or using any BNPL facility.

Compare total repayment cost — not just the headline instalment amount — before choosing BNPL.

When This May Not Be the Right Choice

Irregular income or variable salary months: If your income is variable — freelance work, commission-based pay, or seasonal earnings — committing to fixed BNPL due dates or credit card billing deadlines is risky. A month where income is delayed or lower than expected can result in missed payments and penalty charges on top of an already stretched budget.

Existing credit card debt or active loan repayments: If you are already carrying a credit card balance or repaying an EMI-heavy loan, adding BNPL or more credit card spending increases your total debt obligation without increasing your income. The compounding interest on existing debt will cost more than any convenience gain from new credit usage.

Spending on wants, not needs: Both BNPL and credit cards are designed for purchases — not for converting unaffordable wants into “monthly payments.” If a purchase is not necessary and you would not buy it with cash in hand, a deferred payment option does not change the affordability reality. It defers the cost and adds penalty risk.

Using either product to cover recurring cash-flow gaps: Using BNPL or a credit card every month to cover rent, groceries, or utility bills because salary runs short is a structural cash-flow problem — not a credit product use case. Repeated reliance on credit to cover monthly essentials signals that the spending pattern needs correction, not more credit access.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Both credit cards and BNPL products are regulated in India, but the regulatory framework and documentation differ. Before using either, verify current terms from these sources:

- Reserve Bank of India (rbi.org.in): For credit card regulations, digital lending guidelines, and guidelines on regulated lending entities offering BNPL-style products.

- Your bank or credit card issuer’s official website: For the Most Important Terms and Conditions (MITC) document covering interest rates, fees, late payment charges, grace period rules, and credit limit policies — specific to your card.

- Your BNPL provider’s official terms and conditions: For repayment schedule, late fee structure, credit bureau reporting policy, and account restriction rules in case of default.

- Credit bureaus (CIBIL, Experian, CRIF, Equifax): To understand how credit card and BNPL usage appears on your credit report and affects your score.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Use BNPL only against confirmed income: Before activating a BNPL purchase, check that your next salary credit — or another expected, confirmed income — will arrive before the due date. Do not use BNPL against expected or uncertain future income.

- Pay your full credit card bill every month, not just the minimum: The minimum due is not a repayment strategy — it is a debt continuation mechanism. Set a standing instruction or auto-pay for the full outstanding amount if discipline is a challenge.

- Build one repayment calendar for all credit obligations: List every BNPL due date, credit card billing date, and EMI deduction date in one place — a spreadsheet or calendar app. Treat it as a fixed monthly obligation, not a best-effort reminder.

- Compare total cost, not monthly instalment: A ₹10,000 purchase split into three BNPL instalments of ₹3,500 each costs ₹10,500 — 5% more than the purchase price. Always calculate the full repayment amount before choosing any instalment-based option.

- Keep your credit utilisation below 30% across all products: Whether it is your credit card limit or a BNPL credit line, using too much of your available credit at any point can reduce your CIBIL score — even if every payment is made on time. Spread purchases across billing cycles if needed.

- Prefer debit or savings for discretionary purchases when repayment is uncertain: If you are not confident you can repay within the due date, use money you already have. The cost of one missed BNPL fee or one month of credit card interest will always exceed the convenience of deferred payment.

- Check if your BNPL provider reports to credit bureaus: This is often buried in the MITC or FAQs on the provider’s site. Know your provider’s reporting policy before assuming BNPL is invisible to your credit score.

Frequently Asked Questions

Is BNPL better than a credit card in India?

Neither is universally better. BNPL may suit small, planned purchases where you can repay in full on a fixed date. A credit card may be better for users who pay the full bill monthly, need wider acceptance, or want rewards. The better option depends on your repayment discipline, the purchase type, and the specific costs involved. Compare total cost and repayment terms for your specific provider before deciding.

Does BNPL affect your CIBIL score?

It depends on whether your BNPL provider reports to credit bureaus. Some providers in India do report repayment behaviour to CIBIL or other bureaus, especially those operating through a regulated bank or NBFC partner. A missed BNPL repayment with a reporting provider will negatively impact your credit score — similar to a missed credit card payment. Check your provider’s terms to confirm their reporting policy.

Is BNPL interest-free?

BNPL is often marketed as interest-free — meaning no interest is charged if you pay on time. However, “interest-free” does not always mean “cost-free.” Processing fees, convenience charges, or GST on charges may apply depending on the provider and the product. Always read the full charge schedule, not just the headline marketing. And if you miss the due date, late fees or penalty interest can apply.

What happens if I miss a BNPL repayment?

Missing a BNPL repayment typically triggers a late fee, the amount of which varies by provider and can change without notice. Some providers may also restrict your BNPL account — preventing new purchases — until the overdue amount is settled. If the provider reports to credit bureaus, the missed payment will appear on your credit report and can lower your CIBIL score. Check your provider’s specific MITC for exact consequences.

Is credit card EMI better than BNPL EMI?

Credit card EMI converts a large purchase into fixed monthly payments from your existing credit limit. BNPL EMI is a separate credit facility from a bank or NBFC. Credit card EMI may involve a processing fee and typically comes with card-level protections and rewards (subject to the card and issuer). BNPL EMI may have lower eligibility requirements but can lack the same protections. Compare total repayment cost, processing fees, and foreclosure charges on both before choosing. For a detailed comparison of borrowing options, see credit card EMI vs personal loan.

Which is safer for beginners — BNPL or a credit card?

Neither is inherently safer — both carry real financial risk if misused. For beginners, a single credit card with a low limit and one monthly billing cycle is often easier to track than multiple BNPL apps with different due dates. A credit card also builds a credit history systematically. However, if a beginner tends to pay only the minimum or avoids full repayment, BNPL’s fixed due date may impose more natural discipline. The safest start is understanding the product fully before using it.

Can I use BNPL and a credit card together?

You can — but doing so increases your total credit obligations and the number of repayment deadlines you must track. Using both simultaneously without a clear repayment plan multiplies miss risk. If you choose to use both, maintain a single repayment calendar and ensure your monthly income comfortably covers all obligations before the earliest due date.

What is the maximum BNPL credit limit in India?

BNPL credit limits vary widely by provider, your income profile, credit history, and repayment behaviour. Some providers offer limits starting from a few thousand rupees; others may extend higher limits to users with strong profiles. Limits can be revised upward or downward by the provider based on usage and repayment. Check your specific provider’s app or MITC for the applicable limit and revision policy.

Does paying BNPL on time improve my credit score?

If your BNPL provider reports repayment behaviour to credit bureaus, consistent on-time payments can contribute positively to your credit profile — similar to timely EMI or credit card payments. However, not all BNPL providers report to bureaus, so this benefit may not apply universally. Confirm your provider’s reporting policy before treating BNPL as a credit-score-building tool.

Final Verdict

The BNPL vs credit card decision comes down to repayment discipline, purchase size, and how clearly you can see your next repayment. BNPL is simpler for small, planned purchases when you know the money is already in your account — but its fixed due dates, limited acceptance, and potential credit bureau reporting mean it is not a consequence-free option. A credit card offers more flexibility, wider acceptance, and genuine rewards — but that flexibility can become a debt spiral if you carry a balance or pay only the minimum month after month.

Disciplined users who pay the full card bill every month will almost always get more value from a credit card. Beginners or users with inconsistent tracking habits should approach both products with caution, start with lower limits, and build one repayment habit before adding the second product. The safest option is not BNPL or a credit card — it is whichever one you can repay fully and on time, every time. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.