Rohit in Pune wants his wife to handle household expenses and his son to manage college costs — without handing over cash or juggling multiple bank transfers. An add-on credit card sounds like the easy answer. And it often is. But before Rohit applies, he needs to understand one thing clearly: his wife’s ₹35,000 grocery run and his son’s ₹12,000 online orders both land on his bill, reduce his credit limit, and affect his credit score. This article explains add-on credit card meaning, the rules that govern it, how limits and charges work, what the tax angle looks like, and when a separate card might actually serve the family better.

Quick Answer: Add-On Credit Card Meaning

Add-on credit card meaning is simple: it is a supplementary card issued to a family member under the primary cardholder’s credit card account. The add-on user can spend, but the primary cardholder usually remains responsible for the bill, shared credit limit, charges, and repayment record. A ₹50,000 family spend should be tracked carefully.

Key Takeaways

- An add-on card is a supplementary card linked to the primary cardholder’s account — not a separate credit line with its own independent limit.

- All add-on card spending typically draws from the same credit limit as the primary card; a ₹2,00,000 limit shared across two cards shrinks with every swipe by either user.

- The primary cardholder is generally responsible for the full consolidated bill — including every rupee spent by the add-on cardholder.

- Fees, rewards, per-card spending caps, eligibility rules, and available controls vary significantly by bank and card type — always check the issuer’s MITC before applying.

- Large or unexplained family card spending can raise documentation questions if tax scrutiny arises; keep records for high-value purchases.

- A missed payment or high utilisation on the shared account can affect the primary cardholder’s CIBIL score — even if the overspend was entirely by the add-on user.

- If a family member needs to build their own independent credit history, a separate credit card is usually more effective than an add-on card.

Key Facts at a Glance

| Parameter | What You Need to Know |

|---|---|

| What it is | Supplementary card issued under the primary cardholder’s account |

| Who can get one | Usually spouse, parents, children, or eligible family members — depends on issuer rules |

| Credit limit | Usually shared with the primary card; some issuers allow a separate sub-limit per add-on card |

| Bill responsibility | Consolidated under the primary cardholder’s account; primary cardholder pays |

| CIBIL impact | Repayment behaviour and utilisation on the shared account reflects on the primary cardholder’s credit report |

| Annual fee | May be charged separately for each add-on card — varies by issuer and card tier |

| Tax angle | Spending itself is not automatically taxable; source-of-funds documentation may matter for large or unexplained amounts |

| RBI oversight | Credit card directions issued by RBI govern issuer obligations and customer protections — rbi.org.in |

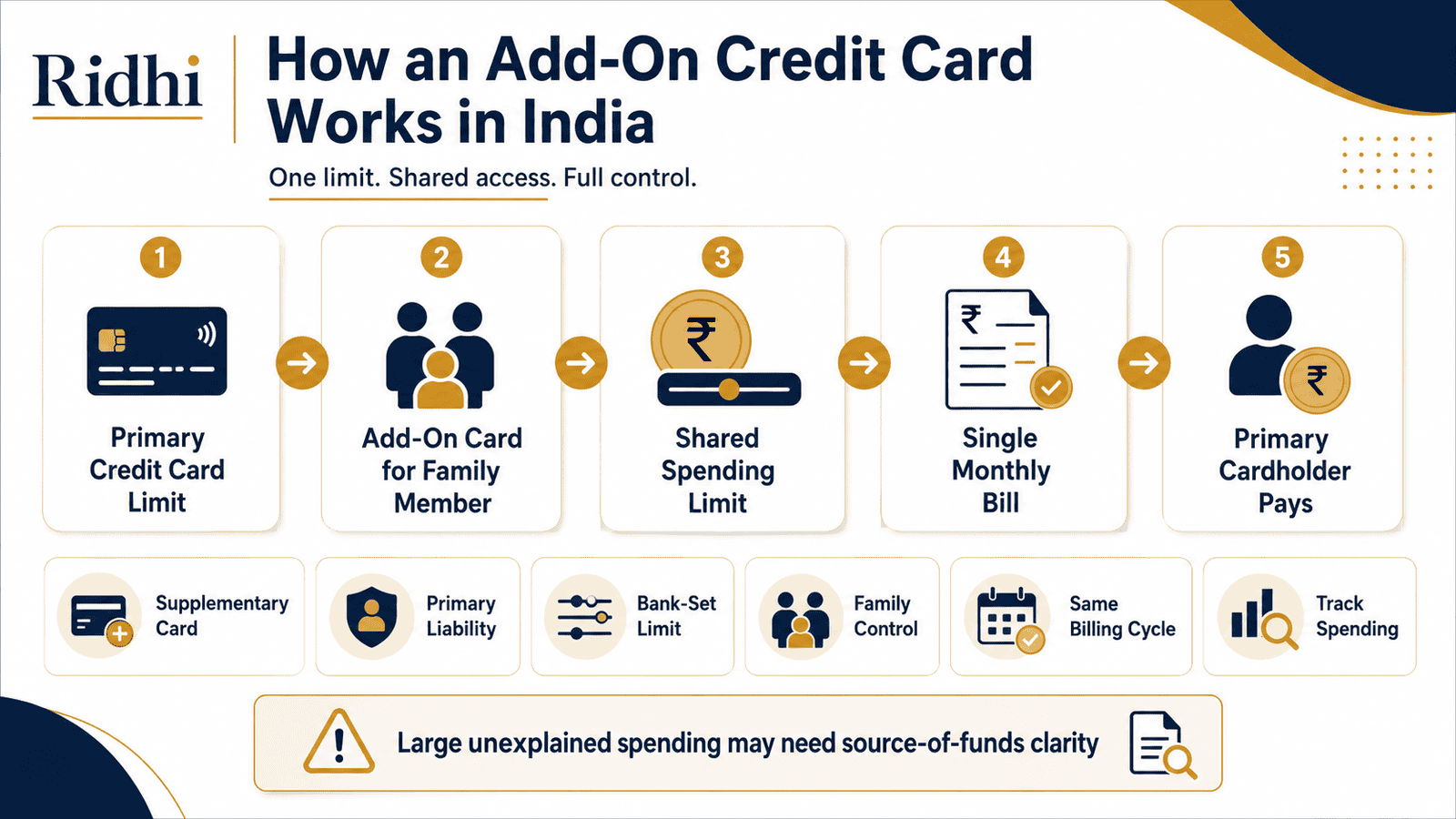

How Add-On Credit Cards Work in India

What the Bank Issues and How It Links to Your Account

When you apply for an add-on card, the bank issues a separate physical or virtual card with a different card number but ties it to your existing primary credit card account. The add-on cardholder gets a card they can swipe, tap, or use online — but there is no separate credit account behind it. Every transaction flows into the same account the primary cardholder holds.

According to RBI’s credit card directions, banks must clearly disclose the terms and conditions governing add-on cards in the Most Important Terms and Conditions (MITC) document. Before you hand a card to a family member, read that document — it tells you whether there is a sub-limit, what charges apply, and what controls are available.

Primary Cardholder vs Add-On Cardholder: Who Is Responsible?

The distinction matters more than most families realise. The primary cardholder signed the credit agreement and is legally responsible for the account. The add-on cardholder is a user — not an account holder. This means:

- The bill comes to the primary cardholder.

- If the add-on user overspends, the primary cardholder must still pay the full amount by the due date.

- Late payment fees, interest charges, and credit score damage — all fall on the primary cardholder’s account.

Shared Credit Limit and How It Gets Used

Most issuers in India operate on a shared credit limit model. If your card limit is ₹2,00,000, every purchase by every cardholder on that account eats into the same pool. Some banks allow primary cardholders to set a lower sub-limit for each add-on card — for example, capping a child’s card at ₹10,000 a month. Whether this option is available depends entirely on the issuer and card product. Check your MITC or call the bank’s customer care before assuming this control exists.

If you are new to how credit card billing cycles work and how all spending rolls up into a single monthly statement, the guide on billing cycle basics explains exactly how all transactions — primary and add-on — appear together and when the due date falls.

Add-On Card vs Getting a Separate First Card

There is an important difference between giving a family member an add-on card and helping them apply for their own first credit card. An add-on card is faster, requires no separate credit check on the add-on user, and gives the primary cardholder consolidated visibility. A separate card, however, lets the family member build their own credit profile. If your spouse or young adult child eventually wants a home loan or car loan in their own name, having their own credit history will matter. If they are starting from scratch and want to understand whether an independent card suits them, the first card selection guide covers what to look for before applying.

Charges That Come With Add-On Cards

Add-on cards are not always free. Common charges to check with your issuer include:

- Add-on card annual fee: Some banks charge ₹500–₹1,000 or more per add-on card per year; others offer the first one free depending on the card tier.

- Cash advance charges: If the add-on cardholder withdraws cash from an ATM, the usual cash advance fee and interest apply from day one — just as they would on the primary card.

- Interest on revolving balances: If the primary cardholder does not pay the full bill by the due date, interest accrues on the combined balance at the card’s standard rate.

All of these flow to the primary cardholder’s account. There is no separate billing for the add-on user.

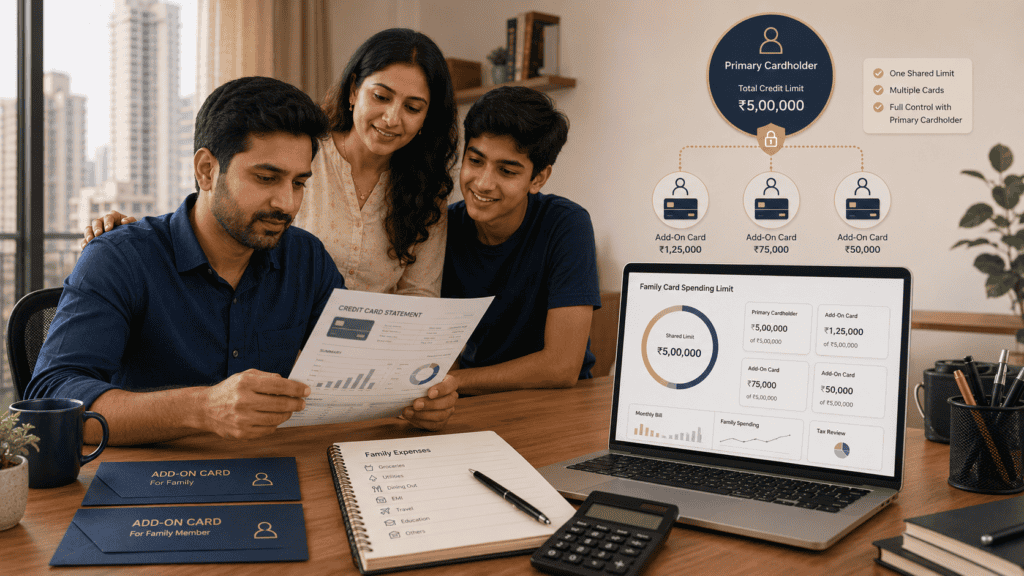

Real Example: The Mehta Family in Pune

Rohit Mehta, 38, is an IT project manager in Pune earning ₹18 lakh a year. He has a credit card with a ₹2,00,000 limit. He adds his wife Priya as an add-on cardholder.

In August, Priya spends ₹35,000 — ₹18,000 on school fees, ₹11,000 on groceries, and ₹6,000 on a family dinner and travel booking. Rohit spends ₹60,000 on electronics and professional software subscriptions.

Their combined spend for the billing cycle: ₹95,000. The available limit on the account drops to ₹1,05,000. The full ₹95,000 appears on Rohit’s credit card statement — not on Priya’s, because she does not have a separate account.

Rohit’s credit utilisation has now crossed 47% of his total limit. That is a level most lenders view unfavourably when assessing future credit applications. If Rohit pays only the minimum amount due, interest starts accumulating on ₹95,000 at his card’s applicable rate. The add-on card was convenient — but tracking shared spending before the due date matters. Understanding how add-on spending raises the credit utilisation impact on the primary account is one of the most important things families often miss.

How to Calculate Add-On Card Impact on Your Limit and Bill

Available Limit = Total Card Limit − Primary Spending − All Add-On Card Spending

Using the Mehta family numbers as an illustrative example:

| Item | Amount (₹) | Running Available Limit (₹) |

|---|---|---|

| Starting card limit | — | 2,00,000 |

| Rohit’s spending (primary) | 50,000 | 1,50,000 |

| Priya’s spending (add-on) | 30,000 | 1,20,000 |

| Total bill before charges | 80,000 | 1,20,000 |

| If only minimum paid (e.g. ₹4,000) | 4,000 paid | Remaining ₹76,000 attracts interest |

This is an illustrative calculation only — actual minimum due amounts, interest rates, and available limit calculations depend on your specific card terms. The key insight: Rohit’s full repayment obligation is ₹80,000 regardless of who spent what. Priya does not receive a separate bill or a separate payment request from the bank.

Add-On Card vs Separate Credit Card: A Comparison

| Parameter | Add-On Credit Card | Separate Credit Card |

|---|---|---|

| Who is responsible for the bill | Primary cardholder | Card user themselves |

| Credit history built | Only on primary cardholder’s report (typically) | On the card user’s own CIBIL profile |

| Credit limit | Shared with primary card — all users draw from same pool | Separate limit approved for the user independently |

| Eligibility check on user | Usually none — primary cardholder’s profile is assessed | Full credit and income check on the applicant |

| Spending visibility | All transactions visible in one primary account statement | Separate statement — primary cardholder has no visibility |

| Best for | Controlled family spending with shared accountability | Independent financial profile and credit-building |

How to Decide What’s Right for You

You want to give a spouse or parent a card for routine household expenses and you are comfortable tracking the shared bill each month — THEN an add-on card with a spending sub-limit is a practical choice.

Your current credit utilisation is already above 30% of your card limit — THEN adding another user who draws from the same pool will worsen your utilisation ratio; consider the impact before applying.

Your young adult child is in college and starting their financial life — THEN a separate entry-level credit card in their name builds their own CIBIL history, which an add-on card typically does not.

You can set up real-time transaction alerts and review the statement before the due date every month — THEN an add-on card is manageable for most families.

The add-on user has inconsistent spending habits or has previously missed repayment obligations on shared expenses — THEN handing them a card tied to your account carries real financial risk.

You are not in a position to monitor combined spending or pay the full bill if add-on usage unexpectedly spikes — an add-on card is not suitable; the primary cardholder cannot disclaim liability after the fact.

Common Mistakes to Avoid

Handing Over the Card Without Setting a Spending Cap

Many primary cardholders give an add-on card without discussing a monthly limit or without checking if the issuer allows a formal sub-limit.

Without a cap, the add-on user could spend the full available limit in one billing cycle, leaving nothing for the primary cardholder’s own expenses and pushing utilisation to 100%. A single billing cycle of unchecked spending can raise total interest costs by thousands of rupees if the full balance is not cleared.

Before issuing the card, call your bank and ask whether a per-card spending cap can be set. Confirm it in writing via the app or by email.

Not Reading the Monthly Statement for Add-On Transactions

Add-on card purchases appear on the same statement as primary card purchases, but they are usually listed separately by card number.

Families who do not review the full statement before the due date often miss duplicate charges, unfamiliar merchants, or disputed transactions from the add-on card. By the time the error is spotted, the due date may have passed. A good starting point is learning to read every line of a credit card statement before the payment date — this is especially important when multiple users are spending on one account.

Set a calendar reminder 3–4 days before the due date to review all line items.

Paying Only the Minimum Amount Due After a High-Spend Month

If family spending across primary and add-on cards has been high in a month, paying only the minimum amount due is a costly habit.

Interest on credit cards in India typically starts from around 36–42% per annum on the outstanding balance. On a combined unpaid balance of ₹80,000, that works out to roughly ₹2,400–₹2,800 in interest for a single month alone. Understanding exactly how credit card interest is calculated helps families appreciate why paying the minimum is dangerous after a big-spend cycle.

Always aim to pay the full statement balance by the due date.

Forgetting Add-On Card Annual Fees

Add-on cards may carry their own annual fee, billed to the primary account. Many cardholders discover this only when they see an unexplained charge on their statement.

Check the MITC at the time of applying. If an add-on card is rarely used, the annual fee may exceed the card’s utility — consider whether it is worth renewing.

Using the Add-On Card for Cash Withdrawals

A cash withdrawal on a credit card — primary or add-on — attracts a cash advance fee (often 2.5%–3.5% of the amount, subject to a minimum) plus interest from the date of withdrawal, with no interest-free period.

An add-on user who withdraws ₹10,000 at an ATM could generate ₹350–₹500 in charges within days, all billed to the primary cardholder’s account. Instruct add-on users clearly: credit cards are not ATM cards.

No Documentation for Large Family Purchases

If a large purchase is made on an add-on card — say, ₹80,000 for a laptop or ₹1,50,000 for a family holiday — and the spending is ever questioned during an income tax assessment, the primary cardholder needs to show that the funds came from legitimate, accounted income.

Keep purchase receipts, booking confirmation emails, and invoices for all high-value add-on card transactions. This is particularly important if the primary cardholder files ITR and the total annual card spend is significant relative to declared income.

When This May Not Be the Right Choice

An add-on credit card may not be the right solution in these situations:

- The add-on user has poor financial discipline: If the person you are giving the card to has a history of overspending or ignoring repayment schedules, your credit score and finances are at risk — not theirs.

- Your credit utilisation is already high: If you are already using 40%–50% of your card limit regularly, adding another user to the same pool will push utilisation higher and can negatively affect your CIBIL score.

- The family member needs independent credit history: An add-on card typically does not build the add-on user’s own CIBIL profile. If they plan to apply for a personal loan or home loan in their own name in the next 3–5 years, they need their own credit history — which a separate card builds and an add-on card generally does not.

- You cannot track combined transactions: If you rarely check your statement or do not have time to review add-on spending before the due date, the risk of missed payments or undetected disputes is real.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card rules, charges, and features can change without notice. Before applying for or issuing an add-on card, verify the current terms from these official sources:

- RBI (rbi.org.in): Master Directions on Credit Cards and credit card guidelines govern customer rights, disclosure requirements, billing practices, and dispute resolution rules. Check for the latest version of RBI’s Credit Card and Debit Card — Issuance and Conduct Directions.

- Income Tax Department (incometax.gov.in): For understanding how large credit card spending may be viewed in the context of annual income, source of funds, and ITR filing. If combined card spend in a financial year is substantial, it may be worth reviewing how this aligns with your declared income using the income tax calculator to understand your broader tax picture.

- Your card issuer’s official website: The MITC (Most Important Terms and Conditions) and schedule of charges are the definitive source for your specific card’s add-on fees, sub-limit rules, rewards sharing policy, and eligibility criteria.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Set a sub-limit before you hand over the card. Call your bank and ask whether a monthly spending cap can be placed on the add-on card. Not all banks offer this, but those that do allow you to cap a child’s card at ₹5,000–₹10,000 per month — preventing a single month’s overrun from affecting your full limit.

- Turn on real-time SMS and app alerts for every transaction. Most Indian banks allow you to enable per-transaction alerts for all cards on an account. A ₹500 grocery transaction alert is less useful than knowing within seconds when the add-on card is used for a ₹15,000 electronics purchase.

- Review the full statement at least 4 days before the due date. This gives you enough time to dispute any unrecognised charge from the add-on card before the payment deadline. Disputed transactions after payment are harder to process.

- Tell add-on users: no cash withdrawals, no EMI conversions without asking. Both actions carry costs — cash advance fees from day one, and EMI conversions that lock a portion of your limit for months. Establish these as ground rules before handing over the card.

- Keep a simple monthly record of add-on spending. A shared note or spreadsheet with the add-on user’s major purchases that month takes 5 minutes and prevents bill-time surprises. This is especially useful if you are tracking family expenses for tax or budgeting purposes.

- Review whether the add-on card’s annual fee is justified each year. If the add-on user is making very few transactions, the fee may outweigh any benefit. Some banks waive add-on fees on premium cards — check your renewal notice and MITC each year.

Frequently Asked Questions

Is an add-on credit card free in India?

It depends on the card and issuer. Some banks include the first add-on card at no additional charge; others levy a separate annual fee per add-on card, which is billed to the primary cardholder’s account. Check your card’s MITC or schedule of charges before applying — do not assume it is free.

Who pays the add-on credit card bill?

The primary cardholder is responsible for paying the full consolidated bill, which includes all spending by both the primary and add-on cardholders. The bank does not bill the add-on user separately. If the add-on user overspends, the repayment obligation falls entirely on the primary cardholder.

Does an add-on card affect my CIBIL score?

Yes — indirectly but meaningfully. All spending on the shared account affects the credit utilisation ratio on the primary cardholder’s credit report. Late payments or defaults are recorded against the primary account. If the add-on user’s spending pushes utilisation above levels that credit bureaus flag as high, the primary cardholder’s CIBIL score may be affected — even if the primary cardholder’s own spending was perfectly controlled.

Can I give an add-on card to my child?

Most banks in India allow add-on cards for children who are 18 years or older, and some allow it for children above a specified age with parental consent — the minimum age varies by issuer. A child below the minimum age set by the bank would not be eligible. Always check the issuer’s eligibility criteria before applying.

Is add-on card spending taxable?

Credit card spending itself is not automatically a taxable event. However, if total card spending in a financial year is significant and appears disproportionate to declared income, it could attract scrutiny during an income tax assessment. The primary cardholder should ensure that all large add-on card purchases are backed by documented sources of income. Consult a tax professional if your combined annual card spend is high relative to your ITR.

Can I set a separate spending limit for the add-on card?

Some banks allow primary cardholders to define a sub-limit for each add-on card — for example, capping an add-on card at ₹15,000 per month from a total limit of ₹2,00,000. This feature is not universally available. Check with your specific issuer through their app, website, or customer care to confirm whether sub-limits can be set and what the minimum/maximum values are.

What happens if the add-on cardholder makes a fraudulent transaction?

Any transaction on the add-on card — including a disputed or fraudulent one — will initially appear on the primary cardholder’s account. The primary cardholder must report the dispute to the bank following RBI’s prescribed timelines for disputed transactions. The primary cardholder bears the repayment risk until the dispute is resolved. Enable real-time alerts on all cards to catch fraudulent usage immediately.

Does the add-on cardholder build their own credit score?

Generally no. In most cases, the add-on card’s payment history and credit utilisation are reported to credit bureaus under the primary cardholder’s profile — not under the add-on user’s name. If a family member wants to build their own independent CIBIL score, they need to apply for a credit card in their own name.

Can I get an add-on card for my parents who are retired?

Yes, most banks allow add-on cards for parents regardless of their employment status, since the credit assessment is based on the primary cardholder’s income and credit profile — not the add-on user’s. The primary cardholder remains fully responsible for the bill. Confirm age limits and documentation requirements with your specific issuer, as these vary.

What is the difference between an add-on card and a supplementary card?

There is no meaningful difference — the two terms refer to the same product. “Add-on card” and “supplementary card” are used interchangeably by Indian banks to describe a card issued to a family member under the primary cardholder’s account. Some issuers use one term in their marketing and the other in their MITC; both describe the same structure and liability framework.

Final Verdict

An add-on credit card is a genuinely useful tool for Indian families who want to consolidate household expenses, give trusted family members spending access, and keep all transactions in one place. For a family like Rohit’s — where spending is predictable, the add-on user is financially responsible, and the primary cardholder reviews the statement before every due date — the convenience is real and the risks are manageable.

But the add-on credit card meaning comes with a liability clause that too many families overlook: the primary cardholder pays for everything. An add-on user’s overspend, missed alert, or impulsive cash withdrawal becomes the primary cardholder’s financial problem. For family members who need to build their own financial identity, a separate credit card is the better long-term path.

Use an add-on card for control and convenience. Use a separate card for independence and credit-building. Understand which one serves your family’s actual goal before you apply. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.