You missed a few credit card payments during a rough patch — a job gap, a medical bill, or just a month where everything went wrong at once. Now the bank is calling, a recovery agent has made contact, and there is a settlement offer on the table. Pay ₹50,000 instead of the ₹80,000 you owe, and it is all over.

Except it may not be over. Not on your CIBIL report.

Settlement and closure are two very different outcomes. One can follow you for years every time a lender pulls your credit report. The other is a clean exit. Before you accept any offer or pay any amount, you need to understand exactly what gets written into your credit history — and what it signals to every future bank, NBFC, or credit card company you approach.

This article explains credit card settlement vs closure in plain language: what each means, how each appears on your CIBIL report, and what to do before you make any payment decision.

Quick Answer: Credit Card Settlement vs Closure

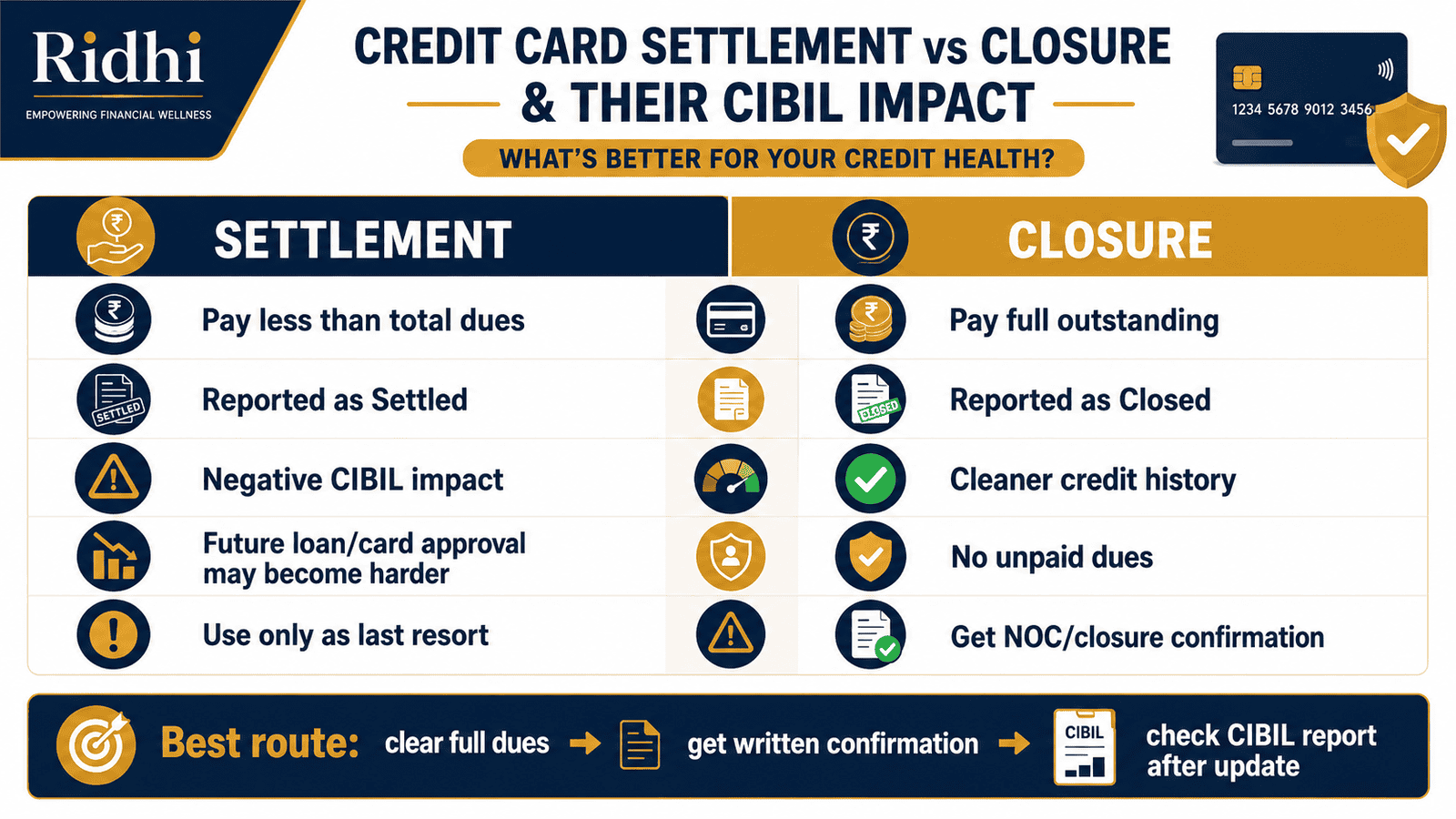

Credit card settlement vs closure means settling pays less than the total dues after default, while closure usually means clearing the full outstanding amount and formally closing the card. Settlement can show as “settled” in your CIBIL report and hurt future approval chances; closure after full payment is usually cleaner.

Key Takeaways

- Credit card settlement usually means the lender accepted less than the total outstanding dues — typically after default — and the difference is written off.

- Closure after full payment means all dues, interest, and charges are paid in full and the card is formally deactivated with no pending balance.

- “Settled” status on a CIBIL report can flag repayment stress to future lenders and reduce loan or card approval chances — sometimes for years.

- “Closed” status after full payment is generally the cleaner credit outcome and signals that you honoured your repayment obligation.

- Always collect written confirmation — a no-dues letter, closure letter, or settlement confirmation — before assuming the matter is resolved.

- Check your CIBIL report 30–45 days after the bank confirms the update to verify the status reported is accurate.

- If the CIBIL status is factually incorrect after a lender update, you have the right to raise a dispute directly with TransUnion CIBIL at cibil.com.

Settlement vs Closure: Side-by-Side Comparison

| Parameter | Credit Card Settlement | Credit Card Closure |

|---|---|---|

| What it means | Lender accepts less than full outstanding after default; balance is written off | All outstanding dues, interest, and charges paid in full; card formally deactivated |

| When it typically happens | After multiple missed payments, usually 90+ days past due or written-off stage | At any point — voluntarily by the cardholder after clearing dues |

| Payment required | Partial — negotiated amount less than total dues | Full — total outstanding including interest and any applicable fees |

| CIBIL report status | Usually reported as “Settled” | Usually reported as “Closed” |

| Future loan / card approval impact | Higher risk flag — lenders may reject or charge more | Cleaner record — no negative repayment remark |

| Best suited for | Genuine financial distress where full payment is not possible | Any cardholder who can repay full dues and wants a clean exit |

| Documents to collect | Written settlement agreement, payment receipt, settlement confirmation letter | Payment receipt, card closure letter, no-dues / NOC letter from issuer |

Key Facts at a Glance

| Fact | Settlement | Closure (Full Payment) |

|---|---|---|

| CIBIL account status reported | Settled | Closed |

| Does negative remark appear? | Yes — “settled” is a derogatory status | No — “closed” is a neutral/positive status |

| How long does it stay on CIBIL? | Up to 7 years from date of default (reporting norms apply) | Account history stays; “closed” status is not a negative mark |

| Do future lenders see it? | Yes — visible to any lender who pulls your report | Yes — but as a closed account, not a negative remark |

| Document to ask for | Settlement letter + payment receipt | No-dues / NOC letter + closure confirmation |

Understanding Credit Card Settlement vs Closure in Detail

What Is Credit Card Settlement?

When a cardholder stops making payments for an extended period — typically 90 days or more past the due date — the account moves into a delinquent or non-performing category. At this stage, the bank or NBFC may initiate a recovery process. As part of that process, the lender might offer to accept a lump-sum amount that is less than the total outstanding dues, including accumulated interest, late fees, and penalties. This negotiated payment is called a settlement or a full and final settlement.

The critical point: the remaining balance that the lender waives off is usually written off internally — but the repayment behaviour leading to that point is reported to credit bureaus. According to TransUnion CIBIL, the account status in your credit report can reflect “Settled” rather than “Closed,” which signals to future lenders that you did not repay the full amount owed.

What Is Credit Card Closure?

Closure, in the proper sense, means you have paid all outstanding dues in full — every rupee of principal, interest, and applicable charges — and formally requested the card issuer to deactivate the card and close the account. A good Good CIBIL score is usually preserved or unharmed by a clean closure, because the account simply moves to “Closed” status, which is neutral in a credit history.

Closure can also be initiated by the bank — for inactivity, for example — but voluntary closure after full payment is the scenario that matters most for credit health.

What Do These Statuses Mean on Your CIBIL Report?

Every credit account you hold is reported to credit bureaus by the lender each month. Each account carries an account status — the most common ones being Active, Closed, Settled, Written-Off, and Delinquent. “Settled” and “Written-Off” are both considered derogatory statuses. They indicate that the original repayment obligation was not met in full.

Future lenders — whether you apply for a home loan, a personal loan, or a new credit card — can see these statuses when they pull your CIBIL report. A settled account can raise questions about repayment capacity and willingness, and some lenders may decline or impose stricter terms even if your overall CIBIL score has recovered partially.

Your credit utilisation ratio and your payment history are both components that affect your CIBIL score — and a settled account can weigh heavily on the payment history factor, which is one of the most significant inputs in score calculation.

Settlement vs Written-Off: Are They the Same?

No. “Written-Off” typically means the lender has written the amount off its books as a loss — often when recovery seems unlikely — without any payment arrangement being made. “Settled” means a payment was made but for less than the full amount. Both are derogatory, but settlement at least shows the borrower engaged with the lender and made a partial payment. The downstream impact on approval decisions can still be significant with either status.

Real Example: Rohit’s ₹80,000 Credit Card Crisis

Rohit, 31, works as a sales executive in Pune and earns ₹65,000 per month. After a job gap of three months in 2023, he missed four consecutive credit card payments. His credit card outstanding — originally ₹45,000 — grew to ₹80,000 after interest charges at approximately 3.5% per month, late payment fees, and over-limit charges. (For a step-by-step breakdown of how credit card interest compounds, see card interest calculation.)

The bank’s recovery team offered Rohit a settlement at ₹50,000 — saving him ₹30,000 immediately. But the settlement agreement stated the account would be marked “Settled” in the credit bureau report.

Rohit considered his options:

- Option A — Accept settlement at ₹50,000: Immediate cash relief of ₹30,000, but “Settled” appears on his CIBIL report. Any home loan or personal loan application in the next 2–3 years could face scrutiny or rejection from lenders who see that remark.

- Option B — Arrange full payment of ₹80,000: No immediate cash saving, but the account closes as “Closed” — a neutral status. His CIBIL history records the missed payments (those are already logged) but not an unresolved outstanding.

Rohit chose to speak with family, arranged ₹80,000, paid in full, and collected a closure letter and no-dues certificate from the bank. The emotional trade-off was real — he had to borrow temporarily — but three years later, he qualified for a home loan without a settlement remark complicating his file. Figures in this example are illustrative; fees, interest rates, and waiver terms vary by issuer.

How to Calculate the Real Cost of Settlement vs Full Payment

Cash Saving from Settlement = Total Outstanding − Settlement Amount Paid

Using Rohit’s numbers:

| Scenario | Amount Paid | CIBIL Status |

|---|---|---|

| Accept settlement | ₹50,000 | Settled (derogatory) |

| Full payment closure | ₹80,000 | Closed (neutral) |

| Immediate cash saving from settlement | ₹30,000 saved now | — |

The ₹30,000 saving looks attractive. But consider the non-numeric cost:

- A home loan of ₹40 lakh at 8.5% over 20 years costs approximately ₹34,800 per month in EMI. If a lender rejects the application — or approves it at 10% instead of 8.5% — the interest cost difference over 20 years can run into lakhs.

- A personal loan application rejected because of a “Settled” remark may force you to approach a higher-cost NBFC instead of a bank.

- A new credit card application may require a secured deposit or higher scrutiny.

Do not decide based on cash saved today alone. The long-term credit access cost of a settled remark can significantly exceed ₹30,000. These numbers are illustrative; actual outcomes depend on your full credit profile at the time of application.

How to Decide What’s Right for You

You can arrange full payment of all outstanding dues, interest, and charges — THEN choose closure after full payment. It is almost always the cleaner credit outcome.

Full payment is genuinely not possible due to job loss, medical emergency, or severe financial distress — THEN settlement may be a last-resort option, but get the terms in writing before paying a single rupee.

A recovery agent is pressuring you to pay immediately without documentation — THEN do not pay without written confirmation from the issuing bank directly. Payments to agents without issuer-confirmed receipts can create disputes later.

You are unsure of the exact outstanding amount including fees and interest — THEN read your latest read card statement or request a written outstanding statement from the bank before deciding on any amount.

The bank confirms a settlement offer in writing AND has clearly stated what CIBIL status will be reported — THEN you have the information needed to make an informed choice for your specific situation.

You have not received written confirmation of what the lender will report to CIBIL after payment — do NOT proceed with any payment under the assumption that the account will close cleanly. Verbal assurances are not enough.

Common Mistakes to Avoid

Assuming Settlement and Closure Mean the Same Thing

Many borrowers believe that once they make a payment and the card stops being used, the matter is resolved. It is not.

Settlement after a default can leave a “Settled” remark on your CIBIL report for years. Closure after full payment leaves “Closed” — a neutral status. Confusing the two is one of the most common — and most expensive — credit mistakes Indian borrowers make.

Before any payment, ask the bank explicitly: “What status will be reported to CIBIL after this payment?”

Paying a Recovery Agent Without Written Issuer Confirmation

Recovery agents work on behalf of the lender but are not the lender. Paying an agent in cash, through an informal transfer, or without a receipt issued by the bank itself can create a disputed record later.

Always insist on an official payment receipt from the issuing bank or NBFC — not just the agent. According to RBI guidelines, lenders are required to follow fair practices in recovery. You have the right to request all communications in writing.

Pay only through official bank channels — net banking, NEFT/RTGS to the card account, or the bank’s official app.

Not Collecting a No-Dues Letter or Closure Confirmation

A payment receipt alone is not enough. The bank’s internal records may not automatically trigger a CIBIL update, or the update may reflect an incorrect status.

Always collect a no-objection certificate (NOC) or no-dues letter explicitly stating that all outstanding amounts have been cleared and the account is closed or settled as agreed. This document is your proof if a dispute arises months later.

Letting Minimum Amount Dues Snowball Before Seeking Help

Many cardholders pay only the minimum amount due month after month, watching interest accumulate at 3–4% per month. A ₹30,000 balance paid minimally can cross ₹60,000–₹80,000 within 18–24 months without new spending.

If repayment is becoming difficult, contact the bank early — before reaching the 90-day default threshold that typically triggers the settlement process. Lenders often have hardship programmes or EMI conversion options that protect your credit record.

Not Verifying Your CIBIL Report After Payment

Even when the bank confirms closure or settlement, the CIBIL report update can take 30–45 days. Some borrowers assume the update is automatic and correct — and then discover a “Settled” or even “Written-Off” status months later when applying for a loan.

Check your CIBIL report directly at cibil.com after the lender confirms the update. If the reported status is factually incorrect, raise a dispute immediately.

Taking New High-Cost Credit Immediately After Settlement

After a settlement, your CIBIL score may be lower and your profile may show a derogatory remark. Applying for new loans or cards immediately — especially from multiple lenders — generates multiple hard enquiries, which can further reduce your score.

Give yourself 6–12 months of on-time repayment behaviour on any remaining accounts before applying for new credit. Patience here directly improves your approval chances.

When This May Not Be the Right Choice

Settlement may not be suitable if you have family, employer advances, or accessible savings that could cover the full outstanding. A temporary borrowing of ₹30,000–₹80,000 from a trusted source is almost always a better trade-off than carrying a “Settled” remark for several years.

Closure of one card may not be enough if other credit card accounts or loans are also overdue. Lenders look at your entire credit profile — clearing one account while others remain delinquent will not meaningfully restore your creditworthiness.

Closing an older credit card — even after full payment — can affect your credit utilisation ratio and reduce your average credit history age, which can have a small negative impact on your CIBIL score. This is worth considering if you have no other active credit accounts.

Borrowers in severe financial distress should contact the bank’s customer service or nodal officer directly and formally, rather than ignoring notices. Ignoring collection communications escalates the situation and reduces the chance of a structured repayment arrangement.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit reporting, recovery practices, and grievance resolution in India are governed by institutions whose official sources you should consult directly before making any decision:

- Reserve Bank of India — rbi.org.in: Guidelines on fair practices in lending, recovery agent conduct, and customer rights in credit card grievances.

- TransUnion CIBIL — cibil.com: Check your CIBIL credit report, understand account statuses, and raise a dispute if any reported information is factually incorrect.

- Your card issuing bank or NBFC — issuer’s official website or app: Closure process, outstanding statement request, settlement policy, and NOC issuance procedure vary by lender. Always verify with the issuer directly.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Before making any payment — settlement or closure — request a written outstanding statement from the bank that lists principal, interest, fees, and any applicable penalties. Do not rely on verbal figures from recovery agents. This also helps you verify whether there are any erroneous charges you can dispute.

- Ask explicitly in writing: “What account status will be reported to CIBIL after this payment?” Get the answer in writing before you pay. Verbal assurances that “it will be marked closed” are not binding and have led to disputes for many borrowers.

- After closure or settlement, follow up with the bank in writing for the no-dues or closure letter. Set a reminder for 45 days after payment to check your CIBIL report at cibil.com and confirm the status update is correct.

- If your CIBIL report shows an incorrect status after the lender has confirmed the correct position, raise a dispute directly with TransUnion CIBIL. The bureau is required to investigate with the lender and update factually incorrect records.

- After any credit setback, focus on rebuilding through on-time payment behaviour. Even one active credit card with zero missed payments and low utilisation can gradually improve your score over 12–24 months of consistent behaviour.

- Avoid applying for multiple loans or cards in quick succession after a settlement. Every hard enquiry is visible on your CIBIL report and signals credit-seeking behaviour, which can further lower your score at a vulnerable time.

- Keep a physical or cloud-based folder with every credit-related document: payment receipts, settlement agreements, NOC letters, closure confirmations, and CIBIL report downloads. These can be essential when disputing an incorrect remark or explaining your credit history to a future lender.

Frequently Asked Questions

Is credit card settlement bad for my CIBIL score?

Yes, credit card settlement is generally considered a derogatory event for your CIBIL profile. When the lender reports the account as “Settled,” it signals to future lenders that you did not repay the full amount owed. This can lower your CIBIL score and make loan or card approvals more difficult. The exact score impact depends on your overall credit history, but the negative remark can remain visible for several years.

Is credit card closure good for CIBIL?

Voluntary closure after full payment is generally a neutral-to-positive outcome. The account status moves to “Closed” — not a derogatory remark. The payment history on that account (including any previously missed payments) remains in your report, but there is no unsettled balance or negative remark added by the closure itself. Lenders viewing a “Closed” account see a completed repayment relationship.

Can “Settled” status be removed from my CIBIL report?

A factually accurate “Settled” status cannot simply be removed on request — it reflects what the lender reported. However, if you later pay the remaining waived amount and the lender agrees to update the status to “Closed” or “No Dues,” they can report a revised status to the bureau. Some borrowers negotiate this with their lender after settlement. The lender’s willingness to update varies and is not guaranteed. If the status is factually incorrect, you can raise a dispute at cibil.com.

How long does CIBIL take to update after card closure?

Lenders typically report to credit bureaus monthly. After the bank processes your closure and confirms the update, the CIBIL report usually reflects the change within 30–45 days. Always verify by checking your report directly at cibil.com after the bank confirms the closure. Do not assume the update has occurred without checking.

Should I settle if I genuinely cannot pay the full dues?

If full payment is truly not possible after exploring all options — including borrowing from trusted sources, converting to an EMI plan with the bank, or a negotiated repayment schedule — then settlement may be a practical last resort. It is better than a written-off account with zero payment. But go into it with clear eyes: the CIBIL remark will be visible to future lenders, and rebuilding your credit profile after settlement takes time and consistent repayment behaviour.

What document proves my credit card is properly closed?

Ask the issuing bank for a no-dues certificate or no-objection certificate (NOC) explicitly stating that all outstanding amounts have been cleared and the card account is closed. Also keep your final payment receipt and the bank’s written confirmation of closure. These documents protect you if a dispute arises later or if an incorrect status appears on your CIBIL report.

Can I get a new credit card after a settlement?

Yes, but it may be more difficult. Lenders can see the “Settled” status on your CIBIL report and may reject new card applications or approve only a secured credit card — one backed by a fixed deposit. The waiting period and likelihood of approval depend on your overall credit profile, income, and how long ago the settlement was. Consistent on-time repayment behaviour over 12–24 months on other active accounts can gradually improve your position.

What happens if I ignore credit card dues and neither settle nor pay in full?

Ignoring dues leads to the account eventually being classified as a Non-Performing Asset (NPA) and possibly marked as “Written-Off” — typically a worse CIBIL status than “Settled.” The lender can continue recovery efforts, and the unpaid amount with accumulated interest remains a legal liability. This also severely limits your future borrowing ability. Engaging with the bank early — before 90 days past due — gives you far more options.

Does closing an old credit card hurt my CIBIL score?

It can, marginally. Closing an old card reduces your total available credit limit, which can increase your credit utilisation ratio — one factor in your CIBIL score. It also removes the account from your active credit mix over time. If it is your oldest card and you have few other accounts, the impact may be slightly larger. In most cases, a well-managed closure after full payment does not cause significant or lasting damage to a healthy credit profile.

Is there a difference between a card settlement and a loan settlement for CIBIL purposes?

The CIBIL reporting logic is similar — both can show as “Settled” if the full amount was not paid. However, the scale of the impact may differ. A settled home loan or large personal loan may have a more significant effect on your profile than a settled credit card, given the higher amounts involved. In both cases, the “Settled” status is derogatory and visible to future lenders.

Final Verdict

Credit card settlement vs closure is not a minor terminology difference — it is the difference between a clean credit history and a remark that follows you for years. Full payment closure is almost always the better option if it is financially possible. It leaves no negative status on your CIBIL report and does not raise red flags with future lenders considering your home loan, car loan, or credit card application.

Settlement is a genuine option in cases of severe financial distress — but it should be a considered, documented decision, not a quick agreement under pressure from a recovery call. Get the terms in writing. Confirm what will be reported to CIBIL. Collect your NOC. Then verify your CIBIL report 30–45 days later.

If you are in the process of rebuilding after a missed payment, settlement, or credit setback, the path forward is consistent — on-time payments, low utilisation, and patience. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.