Most salaried Indians think personal finance meaning is about picking the right mutual fund or timing the market. It is not. Personal finance meaning covers every money decision you make — from how you split a ₹45,000 monthly salary to whether you have a term insurance policy in place if tomorrow does not go to plan.

Without a clear framework, familiar patterns take hold: money runs out before the month ends, no emergency fund exists for a sudden medical bill, and credit card debt quietly charges 36–42% annual interest while an SIP earns 12%. None of these problems require a higher salary to fix. They require decisions made in the right order.

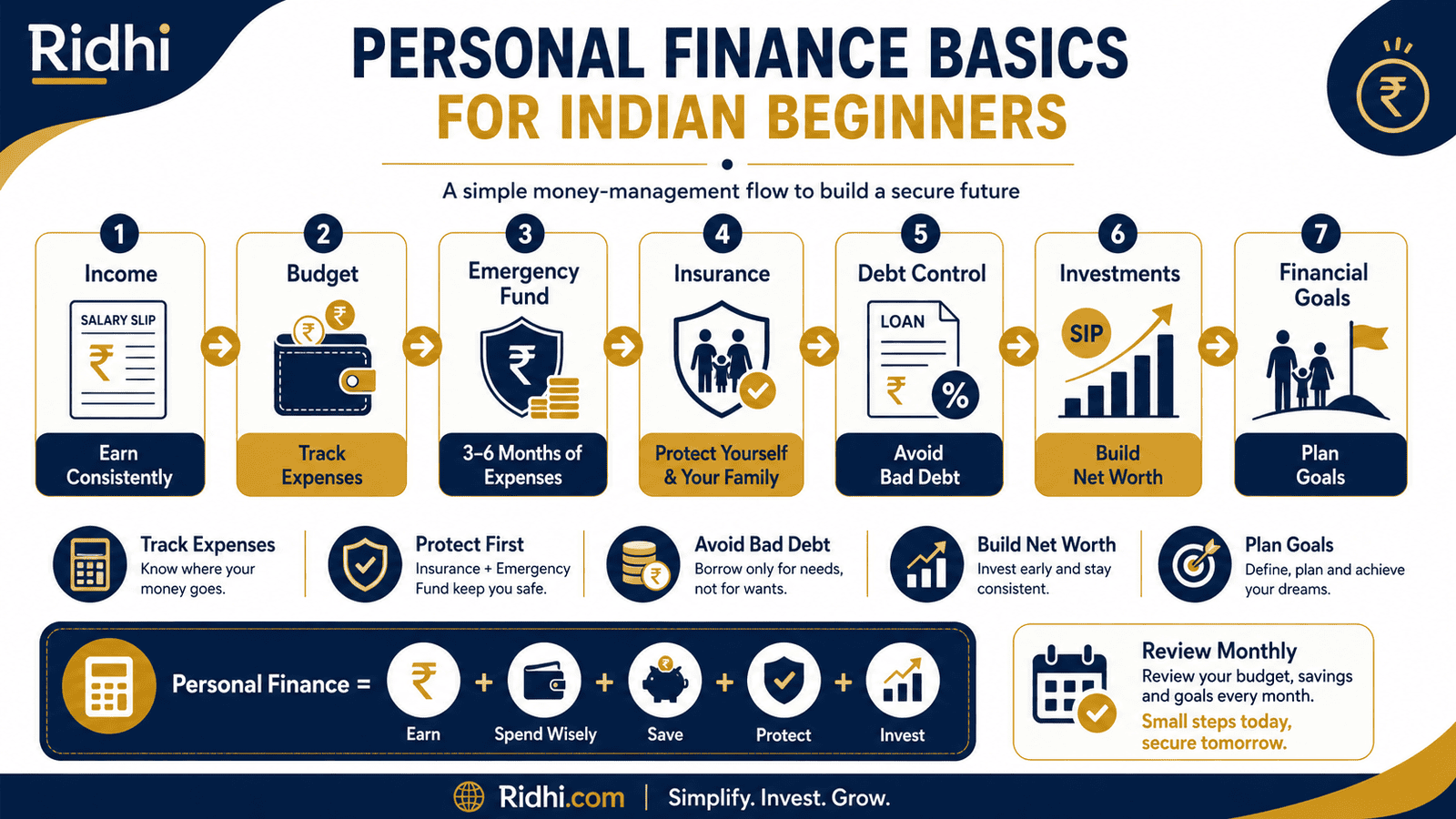

This guide explains what personal finance actually is, how its five core areas work together, and what a beginner in India should tackle first — long before looking at stock prices.

Quick Answer: Personal Finance Meaning

Personal finance meaning is the way you manage your income, spending, savings, debt, insurance and investments to reach money goals. For an Indian beginner, it starts with tracking ₹50,000 monthly income, building an emergency fund, avoiding bad debt and investing only after basic protection is in place.

Key Takeaways

- Personal finance covers five areas in a specific order — budgeting, emergency fund, debt control, insurance and investing — and skipping any step creates financial risk that a larger salary cannot fix.

- A salaried earner bringing home ₹45,000 per month should direct at least ₹9,000 (20%) toward savings and goals before discretionary spending.

- An emergency fund of 3–6 months of essential expenses — typically ₹75,000 to ₹1.5 lakh for a single earner with ₹25,000 in monthly essential costs — must be in place before investing in markets.

- Credit card debt at 36–42% annual interest destroys wealth faster than almost any investment can build it — paying it off first is a mathematical certainty, not a matter of opinion.

- Term insurance of at least 10× annual gross income is the minimum protection floor for any earning member with dependants, and it must come before investing.

- Net worth — total assets minus total liabilities — is the single number that tells you whether your personal finances are genuinely improving year on year.

- Starting to invest at 26 instead of 36 on the same salary can produce a difference of ₹50 lakh or more at retirement in the same fund, because of how compounding works over time.

Key Facts at a Glance

| Personal Finance Area | What It Covers | Starting Point for a Beginner |

|---|---|---|

| Budgeting | Tracking income and allocating it to needs, wants and goals | Record every rupee in and out for one full month |

| Emergency Fund | Liquid cash buffer for job loss, medical bills, urgent repairs | 3–6 months of essential expenses in a savings account or liquid fund |

| Debt Control | Avoiding high-interest debt; clearing existing balances first | Prioritise credit card balance above all other discretionary payments |

| Insurance | Term life cover and health insurance before any market investment | ₹50 lakh term plan; ₹5 lakh family floater health cover minimum |

| Investing | Growing money above inflation for future goals | Start only after steps 1–4 are reasonably in place |

What Personal Finance Meaning Actually Covers

Personal finance is not a product. It is not an app or an investment account. It is a set of decisions — made in the right order — that steadily improve your financial position over years.

Two extremes exist in India. One person earns ₹80,000 a month, invests ₹5,000 in a mutual fund and spends the rest without a budget — and still wonders why they feel financially stretched. Another earns ₹35,000, tracks every rupee, holds six months of expenses in a liquid fund and pays zero credit card interest — and quietly builds net worth. The salary is not the deciding factor. The framework is.

Pillar 1 — Budgeting: Knowing Where Your Money Goes

A budget is not a restriction. It is the act of deciding in advance what your money will do. Without it, spending expands to fill income — a pattern that holds true at every salary level.

For a salaried earner in India, a simple starting structure is three buckets: needs (rent, groceries, utilities, EMIs), wants (dining out, streaming, shopping) and goals (savings, SIPs, loan prepayment). The proportions vary by income and city, but a widely used starting point allocates roughly 50% to needs, 30% to wants and 20% to goals. Learn how to adapt this monthly budget rule to Indian salary and household realities.

Tracking does not require a complicated spreadsheet. Writing down every outflow for 30 days is enough to spot patterns — the ₹2,800 per month on food delivery that nobody mentally counted, the three active subscriptions instead of one, the auto-debit still running for a cancelled gym membership.

Pillar 2 — Emergency Fund: Your Financial Shock Absorber

An emergency fund is liquid money — held in a savings account or a liquid mutual fund — that covers 3 to 6 months of essential monthly expenses. It is not an investment. Its job is to ensure that a sudden medical bill, a job loss or an urgent home repair does not force you into credit card debt or a personal loan at 15–24% annual interest.

For a salaried person with ₹25,000 in monthly essential costs, this means keeping ₹75,000 to ₹1.5 lakh somewhere accessible within 24 hours. This amount sits outside the budget — it is never spent on wants and never invested in equity. Its sole purpose is to prevent one bad event from unravelling everything else.

The most common beginner mistake is investing before this fund is built. A market correction or a job change then forces a withdrawal at the wrong time — or worse, high-interest borrowing — which is the opposite of what personal finance is designed to achieve.

Pillar 3 — Debt Control: Clearing High-Interest Obligations First

Not all debt is harmful. A home loan at 8.5% per annum helps you build a long-term asset. A student loan that funded a useful degree often has returns above its cost. Credit card debt at 36–42% per annum and personal loans at 15–24% are a different matter — they destroy wealth faster than most instruments can build it.

Personal finance for beginners means understanding which debt to address first. The mathematical answer is almost always: highest interest rate first. A ₹60,000 credit card balance generates roughly ₹2,000–₹2,100 in monthly interest charges — ₹24,000 per year leaving the household with nothing in return.

The goal is not to avoid all debt. It is to be free of high-interest debt before deploying serious money into investments.

Pillar 4 — Insurance: Protecting What You Have Already Built

Insurance is not an investment. It is financial protection — ensuring that a single adverse event does not permanently destroy your family’s position.

Two types matter most. Term life insurance is a pure protection product that pays a lump sum to dependants if the policyholder dies during the policy term. According to IRDAI, a healthy 30-year-old non-smoker can obtain ₹1 crore of cover for an approximate monthly premium of ₹700–₹900, depending on insurer and policy term. This is non-negotiable if you have a spouse, children or ageing parents depending on your income. The second is health insurance — a ₹5 lakh family floater policy ensures a hospitalisation does not drain your emergency fund or force a personal loan.

Insurance must precede investing. The logic is direct: if you invest ₹5,000 per month but carry no term cover, a fatal accident leaves your family with a small mutual fund balance and no income. That is not a personal finance plan — it is a gap in one.

Pillar 5 — Investing: Growing Money Above Inflation

Investing means deploying money into assets that grow faster than inflation over time. In India, inflation has historically averaged 5–6% per annum. Money kept only in a savings account earning 3–4% loses purchasing power every year — quietly but consistently.

The correct time to invest is after pillars 1–4 are reasonably in place. At that point, systematic investing — even ₹2,000 per month in a diversified index fund — produces meaningful wealth over 15–20 years because of compounding. SEBI regulates mutual funds in India. EPFO manages the Employee Provident Fund, which is already a forced, employer-matched investment for most salaried employees — and one of the best risk-adjusted savings instruments available to working Indians.

Real Example: Rohit’s Money Snapshot at 26

Rohit, 26, works as a software support executive in Pune earning ₹45,000 per month in hand. He has a ₹3,000 SIP running for six months, a savings account balance of ₹15,000, an EPF balance of approximately ₹40,000 and a two-wheeler with a resale value of around ₹60,000. He also carries a credit card outstanding of ₹1,80,000, built over travel, gadgets and several months of paying only the minimum due.

Rohit believes he is doing something right because he invests. But his personal finance framework has a serious flaw: he is adding to assets on top of high-interest debt, with no health insurance and no term cover in place.

His SIP earns roughly 12% per annum if the fund performs in line with historical averages. His credit card charges approximately 40% per annum. Every ₹3,000 he directs into the SIP instead of the credit card balance costs him around ₹1,200 per year in net interest — money leaving his household permanently.

The fix is not complicated. Pause the SIP, redirect ₹8,000–₹10,000 monthly to the credit card until it is cleared, purchase a basic ₹50 lakh term plan and a ₹3 lakh health cover, then restart investing from a debt-free position. See how to calculate your real net worth — the number that shows whether Rohit’s finances are actually improving.

How to Calculate Your Net Worth

Net worth is the clearest single number in personal finance. It tells you the true state of your finances — not just whether income is coming in, but whether your financial position is improving over time. Use our net worth calculator to run the numbers for your own situation.

Net Worth = Total Assets − Total Liabilities

Using Rohit’s figures from the example above:

Assets: Savings account ₹15,000 + EPF balance ₹40,000 + SIP current value ₹18,000 + Two-wheeler resale value ₹60,000 = ₹1,33,000

Liabilities: Credit card outstanding ₹1,80,000 = ₹1,80,000

Net Worth: ₹1,33,000 − ₹1,80,000 = −₹47,000

Rohit’s net worth is negative. He is running a monthly SIP and still technically insolvent. This is precisely why the order of personal finance decisions matters — a negative net worth getting more negative is not progress, regardless of which app you are using to invest.

| Scenario | Key Inputs | Net Worth |

|---|---|---|

| Rohit today | Assets ₹1.33L, Credit card debt ₹1.80L | −₹47,000 |

| After clearing credit card (approx. 10 months) | Assets ₹1.33L, Debt ₹0 | +₹1,33,000 |

| One year later, investing ₹6,000 per month | Assets ₹2.55L, Debt ₹0 | +₹2,55,000 |

Comparison: Assets vs Liabilities

One of the most practical ways to understand personal finance meaning is to separate what you own from what you owe. The gap between those two numbers is your net worth — and widening that gap over time is the core goal. See assets vs liabilities explained with real Indian examples.

| Parameter | Assets | Liabilities |

|---|---|---|

| Definition | Things you own that hold monetary value | Money you owe to others |

| Indian examples | EPF balance, mutual funds, gold, FDs, savings account, property | Home loan, credit card outstanding, personal loan, car loan EMI |

| Effect on net worth | Increases it | Decreases it |

| Goal in personal finance | Build more of these, systematically, over time | Reduce high-interest ones as the first financial priority |

| Regulated by | SEBI (investments), RBI (bank deposits), EPFO (provident fund) | RBI (lending norms), IRDAI (premium finance products) |

| Key question to ask | “Does this put more money in my pocket over time?” | “Is this interest rate lower than what I can reliably earn by investing?” |

How to Decide What’s Right for You

Personal finance decisions are not identical for everyone, but the priority sequence is consistent for most salaried earners. These if/then guides help you find your starting point.

You have no written budget and genuinely cannot account for where your salary goes each month — THEN spend 30 days tracking every rupee before making any other financial decision. You cannot improve what you cannot measure.

You carry a credit card balance above ₹10,000 or a personal loan above ₹1 lakh at 15%+ interest — THEN direct your monthly surplus toward clearing this before building investments. The interest cost almost certainly exceeds any realistic investment return.

You have no emergency fund — THEN build 3 months of essential expenses in a liquid savings account before opening a mutual fund account. Understand the full case for whether to build your emergency fund or start investing first.

You earn income that a family member depends on and carry no term insurance — THEN buy a term plan this month. It is the cheapest financial protection available for your age and the single most impactful purchase in early personal finance.

You have a working budget, a funded emergency reserve, no high-interest debt and basic insurance coverage — THEN you are ready to invest systematically in line with your goals and time horizon. This is the correct starting position for investing.

You are repaying a home loan at 8–9% per annum and have no other high-interest debt — THEN continue the home loan normally and invest your surplus in equity. At this rate, long-term equity investing is likely to outperform aggressive loan prepayment over 10+ years.

You are not yet tracking spending, carry high-interest debt and have no emergency fund — THEN do not start investing in markets. Investing while financially exposed creates more risk than it resolves. Build the foundation first; the markets will still be there.

Common Mistakes to Avoid

Starting With Investing Before Building a Budget

Many beginners open a mutual fund account before they have ever tracked a month of spending.

Without knowing your actual monthly surplus, you cannot set a sustainable SIP amount. Thousands of investors pause SIPs within six months because cash runs out — and interrupted compounding defeats the purpose of starting early.

Track your expenses for 30 days first, then set an SIP amount you can sustain without interruption for years. Follow this step-by-step guide to building a monthly budget as a salaried Indian.

Paying Only the Minimum Due on Credit Cards

The minimum due payment keeps the remaining balance attracting 36–42% annual interest every month.

A ₹50,000 balance on minimum payments can take over three years to clear and cost more than ₹40,000 in cumulative interest — on top of whatever was originally spent. This quietly destroys significant wealth each year.

Pay the full outstanding each billing cycle. If the balance is already high, treat it as a financial emergency and redirect every rupee of surplus toward it.

Skipping Health Insurance Because “Nothing Has Happened Yet”

A single hospitalisation in a private metro hospital can cost ₹2–₹5 lakh for a moderately serious condition.

Without a policy, this either empties your emergency fund — which then needs to be rebuilt before you can invest again — or forces a personal loan at 15–20% interest. An employer group cover is also insufficient: it disappears when you change jobs or are laid off, precisely when you may need it most.

Buy an individual health policy with at least ₹5 lakh cover, independent of what your employer provides.

Keeping the Emergency Fund in an Equity Mutual Fund

Moving emergency money into equity to “earn better returns” directly undermines the purpose of having an emergency fund.

Equity markets can fall 20–30% in any year. If a job loss or medical emergency coincides with a market downturn, you either withdraw at a loss or borrow at high interest. Both outcomes are worse than earning 6–7% in a liquid fund.

Keep emergency money in a liquid fund or a high-yield savings account. Safety and instant access matter more than return here.

Ignoring the Employer’s PF Contribution

Many salaried employees see PF deductions as money being taken from them.

The employer typically matches the employee contribution — around 12% of basic salary — and adds it to the EPF account. On a basic salary of ₹25,000, that is approximately ₹3,000 per month of additional savings going into a government-backed fund. Opting out voluntarily forfeits this match with no compensating benefit for most salaried earners.

Unless you have a specific and well-reasoned financial purpose, do not opt out of PF. It is one of the few employer-matched, tax-advantaged savings instruments available to salaried Indians.

Setting Goals Without Numbers or Timelines

“I want to save more” is a wish, not a goal. It produces no concrete action.

“I want ₹5 lakh for a car down payment in 24 months — so I need to invest ₹18,000 per month in a recurring deposit” is a goal. Specific amount, specific date, specific monthly action. Every budgeting decision now has a clear purpose behind it.

Write down your top three financial goals with amounts and target dates. Revisit them every six months.

Waiting for the Right Salary to Start

There is no income level at which personal finance basics suddenly become necessary. The fundamentals — budgeting, emergency fund, insurance, then investing — apply at ₹20,000 per month as much as at ₹2,00,000.

A person who builds correct habits at 26 on ₹38,000 per month will almost always be financially stronger at 45 than someone who waits for ₹80,000 salary at 35 — because of the compounding years that cannot be recovered.

Start with what you have. Improve the amounts as income grows.

When This May Not Be the Right Choice

The standard personal finance sequence — budget, emergency fund, debt control, insurance, investing — works for most regular salaried earners. But it may need significant adjustment in certain situations.

If you are self-employed or have highly irregular income, a fixed monthly budget may be impractical. You may need to plan on a quarterly basis and maintain a larger cash reserve — sometimes 9–12 months of expenses — to absorb income gaps between projects or clients.

If you are managing very high debt loads — a personal loan of ₹8–₹10 lakh at 20%+ annual interest — aggressive repayment may need to take priority even before a full emergency fund is in place, with only a minimal cash buffer maintained while the debt is being cleared.

If you are financially supporting two households — your own and ageing parents, for example — income allocation and insurance requirements differ materially from standard frameworks, and professional guidance may be warranted.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Personal finance in India is governed by multiple regulators, each responsible for a different area. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- RBI (rbi.org.in) — savings account rates, bank deposit rules, lending regulations, credit card interest norms.

- SEBI (sebi.gov.in) — mutual funds, stockbrokers, investment advisers, market instruments and investor grievance mechanisms.

- Income Tax Department (incometax.gov.in) — tax slabs, deductions under Section 80C, Section 80D and other provisions affecting personal tax planning.

- IRDAI (irdai.gov.in) — term insurance and health insurance product rules, premium norms and policyholder rights.

- EPFO (epfindia.gov.in) — Employee Provident Fund contribution rates, interest rates, withdrawal rules and UAN management.

- PFRDA (pfrda.org.in) — National Pension System rules, contribution limits and fund manager options.

Expert Tips

- Set your SIP date two days after salary credit. This removes the decision entirely — money moves to investments before it can be spent. You never have to “choose” to invest; it simply happens.

- If your employer offers Voluntary Provident Fund (VPF), consider topping up your PF contribution by ₹1,000–₹2,000 per month. VPF earns the same EPF interest rate, qualifies for Section 80C deduction and carries no market risk — a combination that is difficult to replicate elsewhere.

- Review your term insurance cover every time your income rises by 25% or a major life event occurs — marriage, a new child, a home loan. A ₹50 lakh cover that was sufficient at 25 may be inadequate at 33 once a ₹40 lakh mortgage exists.

- Apply the one-month rule to any purchase above ₹5,000: wait 30 days. If you still want it and the budget permits, buy it. Most impulse purchases do not survive a month of reflection — and the money stays in your account.

- Never place money you will need within two years in an equity mutual fund. Markets can fall 30–40% in a single year. Short-horizon money belongs in FDs, recurring deposits or liquid funds. Understand how compounding makes long-horizon investing so significantly more powerful.

- Check your CIBIL or Experian credit score annually — free from RBI-authorised bureaus. A score above 750 gives you access to lower interest rates on home loans and other credit when you genuinely need it.

- Automate the repetitive parts: SIP auto-debit, insurance premium auto-pay, RD standing instruction. Each automated transfer is one fewer monthly decision that can be delayed, skipped or redirected to spending.

Frequently Asked Questions

What is personal finance in simple words?

Personal finance meaning is the way you manage the money that enters your household — salary, freelance earnings, rental income — to meet daily needs, protect against risk and grow wealth over time. It covers five connected areas: budgeting, emergency fund, debt management, insurance and investing. It is not one subject but five that work together in a specific order.

What are the five areas of personal finance?

The five areas are budgeting (deciding where money goes before it arrives), emergency fund (a liquid cash buffer for genuine surprises), debt management (controlling and eliminating high-interest obligations), insurance (protecting income and assets from large unexpected costs) and investing (growing money above inflation for future goals). All five matter; the sequence matters just as much.

How much should I save from my salary each month?

A practical starting point for most salaried earners is 20% of take-home pay. On a ₹45,000 monthly salary, this means ₹9,000 directed toward savings, SIPs, loan prepayment or goal-linked deposits before discretionary spending. If 20% is not currently achievable, start at 10% and increase it by 1–2% with every salary increment.

What is an emergency fund and how much should I build?

An emergency fund is a ring-fenced pool of liquid money — in a savings account or liquid mutual fund — reserved for genuine emergencies: job loss, hospitalisation, urgent home or vehicle repair. For most salaried earners, the target is 3–6 months of essential monthly expenses. If your essential costs are ₹25,000 per month, aim to accumulate ₹75,000–₹1.5 lakh in this fund before beginning any market investments.

Should I invest before clearing my credit card debt?

In almost every case, no. Credit card interest in India runs at 36–42% per annum. It is extremely difficult for any legitimate investment to consistently return above 36%. Paying off your credit card balance is the highest-return financial action available to you for as long as that balance exists. Clear high-interest debt first, then redirect the freed-up cash into investments.

Is personal finance only relevant for people with high salaries?

No. The framework — budget, emergency fund, debt control, insurance, investing — applies at every income level. The amounts differ; the sequence does not. Someone earning ₹20,000 per month who tracks spending, saves ₹2,000 monthly and carries no credit card debt is in better financial health than someone earning ₹1,00,000 who spends impulsively and carries an unpaid credit card balance.

What is net worth and why does it matter?

Net worth is your total assets — EPF, mutual funds, savings account balance, gold, property — minus your total liabilities — home loan outstanding, car loan, credit card balance, personal loan. It is the single number that tells you whether your financial position is genuinely improving over time. A rising net worth confirms that personal finance is working. A flat or falling net worth signals a problem that a salary increase alone will not solve.

Can I start personal finance on just ₹1,000 per month?

Yes. At ₹1,000 per month, the priority order is: build a small cash buffer first (₹5,000–₹10,000 over a few months), then find the most affordable term insurance plan available for your age and health, then start a ₹500 SIP in a direct-plan index fund. The amount matters less than the habit. Amounts scale naturally as income grows.

What is the single first step in personal finance for a salaried person?

Track every rupee spent for one full month — rent, groceries, EMIs, food delivery, subscriptions, cash withdrawals and everything else. Without this baseline, there is no way to know your actual surplus for saving and investing. Most people who do this for the first time discover ₹2,000–₹5,000 per month in spending they did not consciously realise was happening.

What is the difference between saving and investing?

Saving means keeping money in low-risk, liquid instruments — savings accounts, FDs, recurring deposits — earning 4–7% per annum. It is right for short-term goals under 2–3 years and for the emergency fund. Investing means deploying money into instruments such as mutual funds, equities or NPS that aim to grow above inflation over a longer horizon, typically 7–10+ years. Both are necessary; the question is which goals and which time horizons require which approach.

Final Verdict

Personal finance meaning is not about finding the highest-returning mutual fund. It is about making the right money decisions in the right order — budget before investing, emergency fund before SIP, insurance before wealth building.

For a beginner earning ₹35,000–₹60,000 per month in India, the path is consistent: know where your money goes, build a liquid buffer for emergencies, eliminate high-interest debt, put basic insurance protection in place — and only then start investing with a defined goal and a long time horizon behind it.

The difference between someone who is financially comfortable at 45 and someone who is still stretched is rarely about income. It is almost always about whether they followed a clear framework in their 20s and 30s — and kept following it through pay hikes, lifestyle changes and market cycles.

Start with the five pillars in order. Track your net worth every six months. Let the framework do the rest. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Sanya Malhotra writes about everyday personal finance for Indian individuals and families. Her content focuses on budgeting, saving, emergency funds, debt control, net worth tracking, family money decisions, and practical habits that help readers manage money with more confidence.

She covers topics such as monthly budgeting, expense planning, saving habits, emergency fund behaviour, debt repayment, household financial planning, family discussions about money, financial mistakes, net worth tracking, short-term vs long-term goals, and beginner personal finance concepts.

Sanya’s writing style is warm, simple, and realistic. She avoids making personal finance feel intimidating and instead explains money decisions through relatable Indian examples, ₹ budgets, checklists, and step-by-step frameworks. Her articles are useful for students, freshers, couples, parents, and families who want to improve daily money habits. Her content is educational and does not provide personalised financial advice. Readers should adapt examples to their own income, family responsibilities, city, debt level, risk comfort, and financial goals.