Your credit card statement shows two numbers: ₹50,000 as the total amount due and ₹2,500 as the minimum amount due in credit card. The smaller figure looks manageable — pay ₹2,500 this month and handle the rest later. That decision, made once out of convenience and repeated out of habit, quietly sets off a cycle of finance charges that builds every billing cycle. The minimum amount due is not a discount on your bill. It is the lowest payment your bank will accept before flagging your account as overdue — and the ₹47,500 you leave unpaid does not pause. It carries forward, attracts interest, and grows. This article explains what minimum due actually means, why it is financially dangerous for most beginners, how to estimate the cost, and what safer repayment behaviour looks like.

Quick Answer: Minimum Amount Due in Credit Card

Minimum amount due in credit card is the small part of your bill you must pay by the due date to avoid default. It is dangerous because the unpaid balance rolls over, interest can start on the remaining amount, and a ₹50,000 bill may still leave ₹47,500 unpaid after a ₹2,500 minimum payment.

Key Takeaways

- Minimum amount due is not the same as total amount due — paying it does not close your credit card bill for the cycle.

- Paying only the minimum prevents an immediate late-payment default but does not stop finance charges from accruing on the unpaid balance.

- The unpaid balance rolls over as a revolving credit card balance and attracts finance charges every billing cycle.

- Repeated minimum payments can create a debt trap — your outstanding balance compounds faster than you clear it.

- On a ₹47,500 unpaid balance at typical Indian card finance charge rates, the monthly interest cost alone can run into several hundred to over a thousand rupees per cycle.

- Paying the total amount due before the payment due date is the only action that stops interest on purchases from the previous cycle.

- If you cannot pay the full bill, paying any amount above the minimum reduces the base on which finance charges are calculated.

Key Facts at a Glance

| Term | What It Means | What to Watch |

|---|---|---|

| Minimum Amount Due | The lowest payment the bank accepts to prevent the account being marked overdue | Paying this does not stop finance charges on the unpaid balance |

| Total Amount Due | The full outstanding bill for the current billing cycle | Paying this avoids interest on purchases and retains the interest-free period |

| Outstanding Balance | The balance remaining unpaid after your payment is received | Finance charges are typically calculated on this carry-forward amount |

| Payment Due Date | The last date to pay at least the minimum without triggering a late fee | Even one day late can trigger a late payment charge and affect CIBIL score |

| Finance Charges | The interest applied by the issuer on unpaid revolving balance | Rate varies significantly by card and issuer — verify in your MITC |

What Is Minimum Amount Due in Credit Card and Why It Is Misleading

How the Minimum Amount Due Is Calculated

Every time your credit card billing cycle closes, your bank generates a statement showing two key numbers: the total amount due and the minimum amount due. Most Indian banks set the minimum amount due as a percentage of your outstanding balance — commonly somewhere in the range of 5% to 10% — or a flat floor amount, whichever is higher. Some issuers also include any EMI instalments due, overdue amounts from prior cycles, and overlimit charges in the minimum due calculation. The exact formula differs across banks and card variants.

Paying this amount on or before the payment due date is enough to keep your account from being recorded as overdue for that cycle. It also prevents a late payment fee from being triggered. That is the extent of the protection it offers. Everything above the minimum you paid — in this example, ₹47,500 — does not pause or disappear. It carries forward as an outstanding balance into the next cycle.

What Happens to the Unpaid Balance

The amount you did not pay rolls over as a revolving credit card balance. Your card issuer then applies finance charges to this carry-forward balance — the interest rate specified in your card’s Most Important Terms and Conditions document. These charges are added to your next statement, increasing the total you owe before you even make a single new purchase.

Finance charges on credit cards in India vary widely by issuer and card type. Many issuers charge an annual percentage rate that translates to a meaningful monthly rate — and on a ₹47,500 unpaid balance, even a mid-range monthly rate results in several hundred rupees in charges per cycle. Do that for three consecutive months and the interest alone runs into thousands of rupees, on top of a principal balance you have barely reduced. The exact rate applicable to your card is stated in your MITC — verify it directly with your issuer, since rates vary and can change.

Understanding late payment charges is also important here, because many beginners confuse the two risks. Missing the due date entirely — paying nothing or paying after the deadline — triggers a separate late payment fee on top of finance charges. Paying the minimum on time avoids that specific penalty. It does not, however, avoid the interest that accrues on the unpaid revolving balance.

The Interest-Free Period: What You Lose When You Revolve a Balance

Most credit cards in India offer an interest-free period on new purchases — typically 20 to 50 days depending on your billing cycle date and when a purchase was made. This grace period applies only when the previous month’s total amount due was paid in full. The moment you carry any unpaid balance forward, many banks cancel the interest-free period on fresh purchases in the following cycle.

That means if you pay only the minimum in July, your August purchases — groceries, fuel, subscriptions — can attract finance charges from the transaction date itself, with no grace period at all. This second layer of cost catches beginners completely off guard. You are not just paying interest on the ₹47,500 you rolled over. You are also losing the free credit benefit on every new transaction until the balance is cleared.

How the Balance Builds — The Debt Trap in Practice

This is how revolving credit card debt silently compounds. You begin with ₹50,000 due. You pay ₹2,500. Balance is now ₹47,500. Finance charges are applied. Your next month’s spending adds another ₹15,000. The following statement shows a total close to ₹64,000 or more — the old unpaid balance, plus finance charges on it, plus new spending. Again the minimum due is a small fraction. Again you pay just that amount. The cycle repeats.

Within three to four months, you may have paid ₹8,000 to ₹10,000 in minimum payments but your outstanding balance has barely fallen — because most of what you paid was consumed by finance charges. The balance you owe is now higher than when you started. This is the credit card debt trap: not dramatic, not sudden, but relentless and compounding month after month.

According to RBI guidelines on credit card operations available at rbi.org.in, card issuers are required to disclose the consequences of paying only the minimum amount on cardholder statements. The warnings are there — printed on your statement — for exactly this reason. Most people skip past them.

Minimum Amount Due vs Total Amount Due: The Core Difference

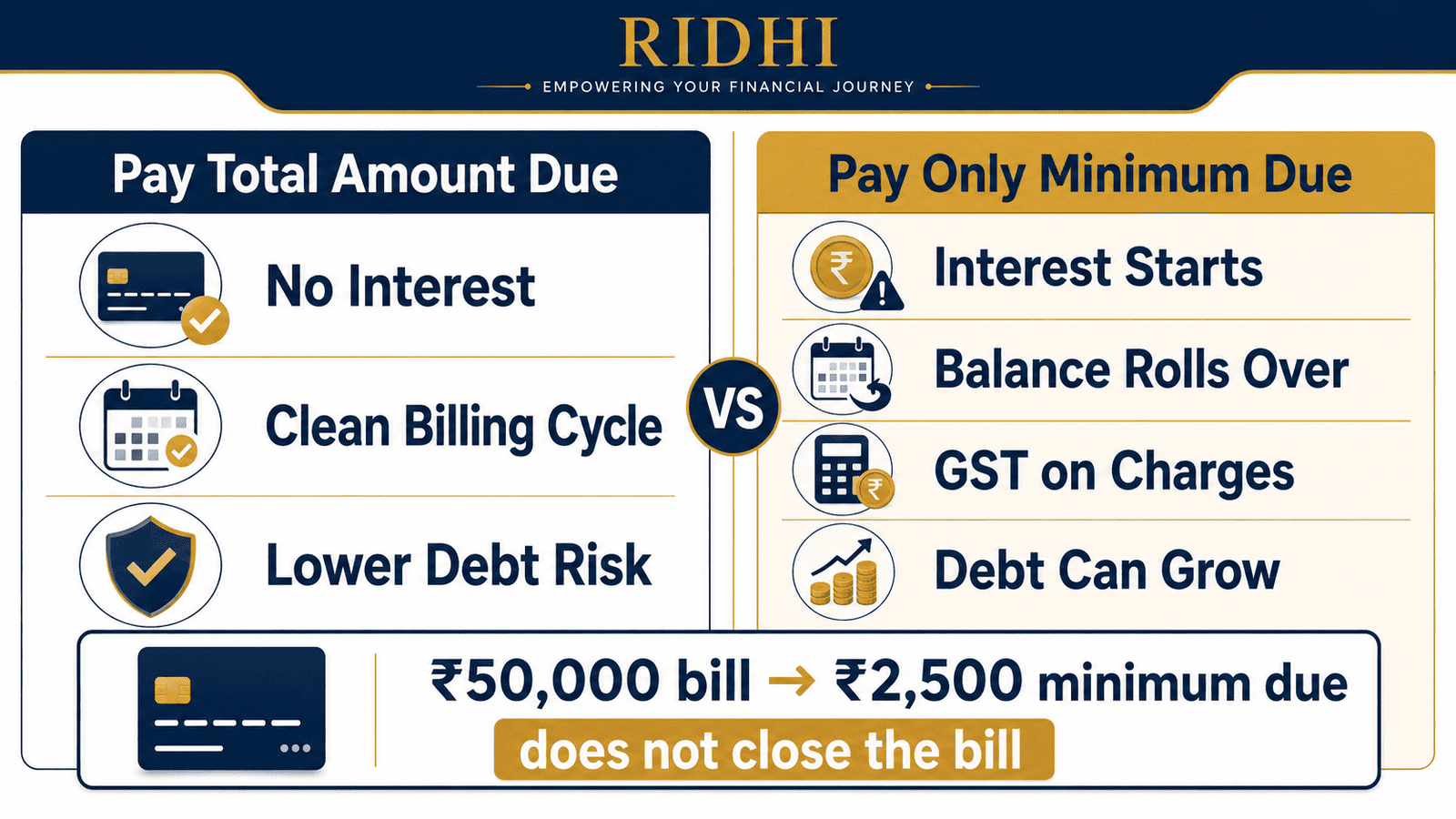

The confusion is partly a design problem. Minimum amount due is displayed prominently because it is the number that determines whether you need to take action immediately. But it is a floor, not a target. Think of it as the absolute lowest your bank will accept before flagging your account. Total amount due is what actually closes the bill for the cycle. Paying the total amount due before the due date means you owe nothing from last cycle, no finance charges are applied to previous purchases, and your credit utilisation resets cleanly for the next billing period.

Real Example: Rohan’s ₹50,000 Credit Card Statement

Rohan, 28, is a software engineer in Pune earning ₹85,000 per month. He used his credit card heavily in June — a laptop, a few weekend trips, and regular daily expenses — and his statement showed a total amount due of ₹50,000. The minimum amount due was ₹2,500. Rohan paid ₹2,500, telling himself he would clear the rest the following month once salary arrived.

His bank applied finance charges on the ₹47,500 unpaid balance as per the card’s terms. Let us say that charge added approximately ₹1,600 for the purpose of this illustration. His next statement now included ₹47,500 in carry-forward balance, plus ₹1,600 in finance charges, plus another ₹15,000 in July purchases — a total approaching ₹64,100 before any other fees. The minimum due on this larger amount was again small. Rohan again paid only the minimum.

By the end of three months, Rohan had paid roughly ₹8,000 in minimum payments. His outstanding balance, however, had not fallen below ₹55,000 — because finance charges kept adding to whatever he did not clear. He was not making progress. He was paying to stay in place.

Note: figures above use a hypothetical monthly rate for illustration only. Actual finance charge calculation depends entirely on your card issuer’s rate, billing method, and applicable terms. Always check your statement and MITC for the figures that apply to you.

How to Calculate the Cost of Paying Only Minimum Due

Unpaid Balance = Total Amount Due − Amount Paid

Finance Charge (one cycle) = Unpaid Balance × Monthly Finance Charge Rate

Next Statement Baseline = Unpaid Balance + Finance Charge + GST on Finance Charge (where applicable)

Applying this to Rohan’s numbers at a hypothetical 3.5% monthly rate:

- Total Amount Due: ₹50,000

- Minimum Payment Made: ₹2,500

- Unpaid Balance: ₹50,000 − ₹2,500 = ₹47,500

- Finance Charge at 3.5% per month: ₹47,500 × 3.5% = approximately ₹1,662

- GST at 18% on finance charge (where applicable): approximately ₹299

- Next statement baseline (before new purchases): approximately ₹49,461

| Scenario | Payment Made | Estimated Next-Cycle Starting Balance |

|---|---|---|

| Pay total amount due | ₹50,000 | ₹0 — clean start, no interest |

| Pay 50% of total due | ₹25,000 | ≈ ₹25,875 plus new purchases |

| Pay minimum due only | ₹2,500 | ≈ ₹49,461 plus new purchases |

The 3.5% monthly rate above is for illustration only. Your card’s actual rate and exact calculation method will differ. Use the credit card interest calculator to estimate how much a revolving balance will cost based on your specific card’s rate — it will give you a far more accurate figure than any generic example can.

Comparison: Paying Total Amount Due vs Paying Only Minimum Due

| Parameter | Pay Total Amount Due | Pay Only Minimum Due |

|---|---|---|

| Late payment penalty | Not triggered | Not triggered (if paid on time) |

| Finance charges on balance | None | Applies to unpaid carry-forward |

| Interest-free period next cycle | Retained on new purchases | May be lost on fresh purchases |

| Outstanding balance | Cleared to zero | Rolls over and can compound |

| Debt-trap risk | None | High if used as a regular habit |

| CIBIL score impact | Positive — low utilisation | Neutral short-term; worsens if balance grows |

| Best use case | Standard repayment behaviour every cycle | One-off cash-flow emergency — not a habit |

How to Decide What’s Right for You

you have the full outstanding amount available before the payment due date — THEN pay the total amount due. No finance charges are applied to the previous cycle’s purchases, and the interest-free period resets for your next cycle.

you cannot pay the full amount — THEN pay as much above the minimum as your cash flow allows. Even clearing ₹20,000 on a ₹50,000 bill significantly reduces the base on which finance charges are calculated next month.

you have paid less than the total due — THEN stop using the same card for discretionary purchases until the balance is fully cleared. Each fresh transaction adds to the revolving balance and compounds the problem in the next billing cycle.

your balance is too large to clear in one or two months — THEN contact your card issuer and ask whether conversion to an EMI plan is available. Confirm the applicable processing fee and interest rate before accepting — it may be lower than revolving card charges, but verify this with your issuer directly.

you have paid only the minimum due for two or more consecutive months — THEN treat this as a serious repayment signal. Review guidance on paying card bills correctly and consider a structured plan to reduce the balance before it becomes unmanageable.

you should not pay only the minimum if you have savings in a savings account earning 3%–4% annually. Using those savings to clear the credit card balance first — and rebuilding savings from subsequent salary credits — is almost always the better financial decision when card finance charges are substantially higher than the interest your savings account earns.

Common Mistakes to Avoid

Thinking Minimum Due Means the Bill Is Settled

Many first-time cardholders assume that paying the minimum amount due closes the statement for the month.

It does not. On a ₹50,000 bill where you paid ₹2,500, you still owe ₹47,500 — and finance charges are applied to that carry-forward amount every cycle. The next statement will reflect both the balance and the charges added to it.

Always check your next month’s statement to confirm exactly what was carried over and what charges were applied.

Continuing to Spend While Carrying a Revolving Balance

Adding fresh purchases to a card that already has an unpaid balance from a prior cycle makes the situation significantly worse.

New transactions may attract finance charges from day one — because the interest-free period is often suspended when a balance is being revolved. Your next total due becomes the unpaid balance, plus finance charges, plus fresh spending. The number grows faster than most people realise.

Stop discretionary card spending on the affected card until the full outstanding balance is cleared.

Ignoring Finance Charges and GST on Your Statement

Finance charges and applicable GST on those charges appear as distinct line items on the credit card statement. Many cardholders look only at the total and minimum due numbers without reading what is driving them.

Ignoring these line items means your mental picture of what you owe is lower than the actual figure. The charges are being added to your balance whether you notice them or not.

Read every line of your monthly credit card statement before deciding how much to pay.

Paying After the Due Date Even When Planning to Pay the Minimum

The minimum amount due protects you from a late-payment penalty only when paid on or before the payment due date.

A payment arriving even one day late can trigger a late fee — which is then added to an already-growing balance. A late payment may also be reported to credit bureaus.

Set a standing bank autopay instruction or a calendar reminder well ahead of the due date, not on the due date itself.

Taking a Cash Advance While Carrying an Outstanding Balance

A credit card cash advance — withdrawing cash from an ATM using your credit card — carries a separate transaction fee and typically attracts finance charges from the very date of withdrawal. There is no interest-free period on cash withdrawals.

Using this feature while you are already carrying an unpaid revolving balance means you are paying high charges on two fronts simultaneously — the existing unpaid balance and the new cash advance.

Avoid cash advances entirely until the outstanding card balance is cleared in full.

Using Minimum Due as a Regular Monthly Repayment Plan

Minimum due was designed as a short-term safety mechanism — a way to avoid immediate default during one difficult month. It was never intended as a sustainable repayment habit.

Paying only the minimum every month means the principal balance never meaningfully reduces. Finance charges keep building on the outstanding amount. Within a few months, the debt can feel impossible to exit.

Set a personal rule: minimum due is a once-in-a-while emergency fallback, used once and then immediately followed by a plan to clear the remaining balance.

When This May Not Be the Right Choice

Paying only the minimum amount due is not appropriate in these situations:

You have savings that could cover the full bill. If your savings account balance is sufficient to pay the total amount due, clearing the card first and rebuilding savings from your next salary credit avoids finance charges — which are typically far higher than the interest a savings account earns.

Your outstanding balance is large relative to your monthly income. If the total amount due exceeds 50% of one month’s take-home pay, minimum payments alone will not reduce the balance at any meaningful pace. Finance charges will compound faster than the minimum payments bring the balance down.

You have already been rolling over dues for two or more consecutive months. One month of minimum-only payment can be a legitimate cash-flow decision. Two or more months is the beginning of a debt cycle that becomes progressively harder to exit without a deliberate change in repayment behaviour.

Your overall debt includes EMIs, personal loans, or BNPL obligations. When multiple repayment commitments are running simultaneously, adding revolving card charges to the load increases the risk of missing a payment across one of those obligations — which has its own cascade of penalties.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Credit card billing rules, minimum due formulas, finance charge rates, late payment fees, and GST treatment on charges are determined by each issuer and can change over time. Always verify current figures directly from your issuer’s official documents.

- RBI (rbi.org.in): The Reserve Bank of India issues guidelines governing credit card operations in India, including disclosure requirements, cardholder protections, and issuer obligations. RBI’s Master Direction on Credit Card and Debit Card — Issuance and Conduct is the primary regulatory reference.

- Your card’s MITC (Most Important Terms and Conditions): This document — available from your bank’s website or on request — specifies the exact finance charge rate, minimum due calculation method, late fee structure, and cash advance charges applicable to your card variant. This is the single most important document to read.

- Your monthly credit card statement: The statement itself shows total amount due, minimum amount due, payment due date, any finance charges from the prior cycle, and late fees if applicable. It reflects the most current position of your account.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Set autopay for the total amount due, not the minimum. Most Indian banks allow you to configure auto-debit for either the minimum amount or the total amount due each cycle. Choosing total amount due means you never accidentally carry a revolving balance and never pay finance charges on purchases you already made.

- Keep credit utilisation below 30% of your credit limit. On a ₹1,00,000 limit, avoid carrying a statement balance above ₹30,000. Lower utilisation reduces both finance charge exposure and the pressure on your CIBIL score from a high utilisation ratio.

- Use one primary card until your repayment habit is stable. Managing two or three credit cards before you have a consistent full-payment discipline multiplies the risk of revolving balances across accounts. Start with one card, clear it fully each month, and then consider a second card only once the habit is solid.

- Read your statement line by line — not just the headline number. Finance charges, GST on those charges, and any carry-forward from the prior cycle are separate line items. Skipping past them gives you an inaccurate picture of what you actually owe and what is driving the balance.

- Treat the minimum due as a once-only emergency option with a recovery plan. If you use it in one month because of a genuine cash crunch, plan the following month’s spending explicitly around clearing the full outstanding — not repeating the minimum payment.

- Check whether your interest-free period was affected after any partial payment. After a month where you did not pay the full bill, confirm from your next statement whether fresh purchases attracted finance charges from day one. This tells you how aggressively you need to reduce the carry-forward balance before spending normally again.

- Build longer-term habits using guidance on using credit cards wisely — consistent full-payment behaviour each month is the most effective long-term protection against revolving credit card debt.

Frequently Asked Questions

Is it okay to pay only the minimum amount due on my credit card?

Paying the minimum amount due on time prevents an immediate late-payment default for that cycle. However, it is not a safe regular habit. The unpaid balance rolls over and attracts finance charges every billing cycle. Used once as an emergency measure, it is acceptable. Used month after month, it leads to a growing balance that becomes increasingly difficult to clear.

Will I be charged interest if I pay the minimum amount due?

Yes, in most cases. When you pay less than the total amount due, the unpaid balance attracts finance charges as per your card’s terms. The exact rate depends on your issuer and card type — check your card’s MITC for the specific annual or monthly rate applicable to your account.

Does paying only the minimum amount due affect my CIBIL score?

Paying the minimum amount on time does not cause an immediate negative entry on your CIBIL report. However, if your outstanding balance keeps growing and your credit utilisation ratio rises significantly, it can hurt your credit score over time. Missing the payment entirely — not even paying the minimum — has a direct and immediate negative impact on your CIBIL score.

What happens if I pay less than the minimum amount due?

If you pay less than the minimum amount due, your account may be recorded as delinquent or past due. This typically triggers a late payment fee, the shortfall is carried over to the next cycle as part of the outstanding balance, and the event may be reported to credit bureaus — which can lower your CIBIL score.

What is the difference between minimum amount due and total amount due?

Total amount due is the complete outstanding bill for the current billing cycle — everything you owe on the card as of the statement date. Minimum amount due is the smallest portion your bank requires by the due date to avoid a late-payment penalty. Paying the minimum does not close the bill. Paying the total amount due does — and avoids finance charges on that cycle’s purchases.

Can I pay more than the minimum due but less than the total amount due?

Yes. You can pay any amount between the minimum and the total amount due. The more you pay above the minimum, the smaller the carry-forward balance and the lower the finance charges in the next cycle. Paying ₹20,000 on a ₹50,000 bill is substantially better than paying ₹2,500, even if you cannot clear the full amount this month.

Can paying only the minimum due for several months lead to a credit card debt trap?

Yes, it can — and this is the most common way revolving credit card debt builds up. When you pay only the minimum each month, the principal balance reduces very little while finance charges are added each cycle. If you continue spending on the card, the balance grows faster than minimum payments bring it down. Within a few months, a manageable ₹50,000 bill can become a ₹70,000 or ₹80,000 balance.

What is a revolving credit card balance?

A revolving credit card balance is the unpaid portion of your bill that carries over from one billing cycle to the next. Unlike a fixed-EMI loan, this balance changes based on how much you pay and how much you spend each month. Finance charges are applied to this balance every cycle, which is why it can grow quickly if not managed actively.

Is the minimum amount due percentage the same across all credit cards in India?

No. Each bank and card issuer sets its own formula. Some base it on a flat percentage of the outstanding balance, others include overdue instalments and overlimit amounts. The percentage itself also varies by card type. Always refer to your specific card’s MITC for the exact calculation method — do not assume your card uses the same formula as someone else’s.

Final Verdict

Minimum amount due in credit card is a safety net — not a repayment strategy. Paying it on time protects your account from an immediate late-payment default. It does not protect you from finance charges on the unpaid balance, and it does not protect your interest-free period on fresh purchases. For Rohan in Pune — and for any cardholder who sees a small minimum due figure and feels reassured — the number that actually matters is the total amount due. Pay it in full every cycle when your cash flow allows. If you cannot, pay as much above the minimum as possible, stop adding fresh purchases to the same card, and treat minimum due as a once-only emergency fallback rather than a monthly routine. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Nikhil Bansal writes about credit cards, billing cycles, card charges, rewards, cashback, credit utilisation, card EMI, BNPL, and responsible credit usage in India. His content is designed for readers who want to use credit cards wisely without falling into expensive repayment mistakes.

He covers topics such as how to choose a first credit card, credit card billing cycle, due date, grace period, minimum amount due, credit utilisation ratio, reward points vs cashback, lifetime free credit cards, annual fee waivers, credit card statement reading, add-on cards, cash advance charges, EMI on credit cards, credit card fraud reporting, BNPL vs credit card, and foreign transaction fees.

Nikhil’s writing is beginner-friendly, direct, and risk-aware. He explains how small mistakes such as paying only the minimum due, withdrawing cash from a credit card, missing due dates, or overusing credit limits can become costly. Since card fees, interest rates, reward rules, waiver conditions, and bank offers change often, readers should verify the latest Most Important Terms and Conditions from the card issuer.