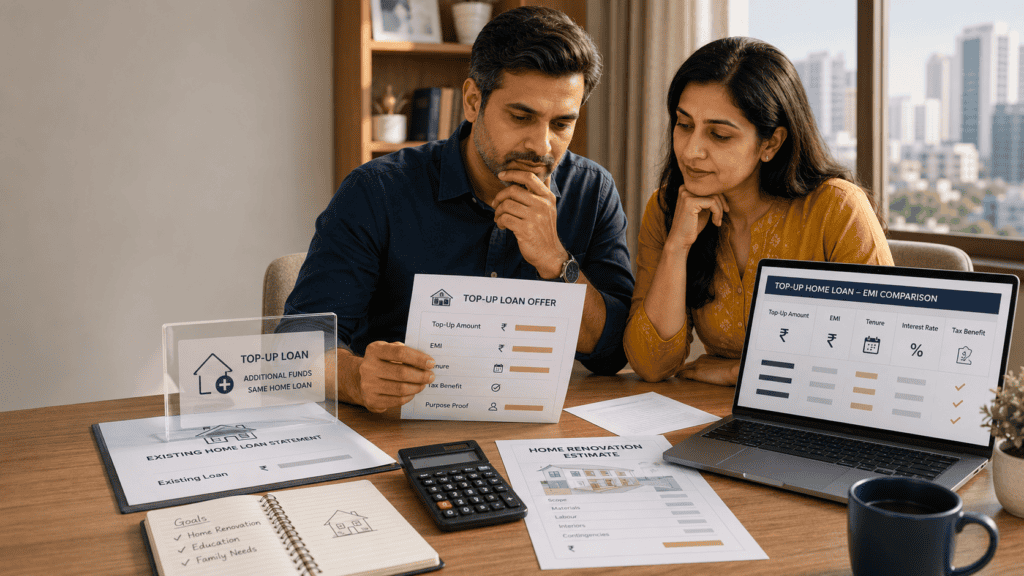

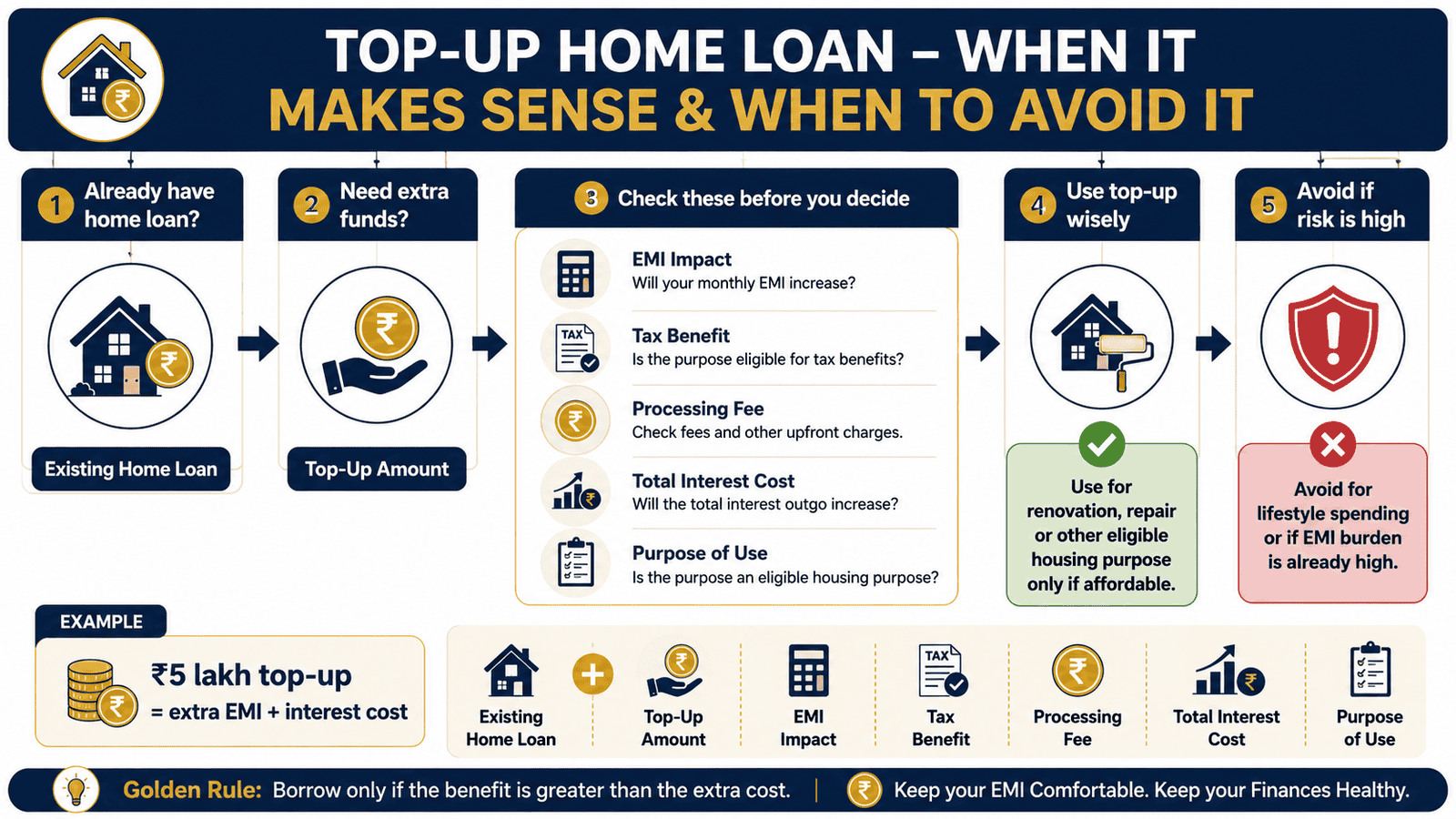

If you already have a home loan and suddenly need extra money — for a kitchen renovation, your child’s school admission, or a medical bill — you are probably wondering whether you need an entirely new loan or whether your existing lender can simply add to what you already owe. That option exists. It is called a top-up home loan, and for many borrowers it is cheaper than a personal loan — but not automatically, and not without conditions.

The lower interest rate sounds attractive on paper. But a top-up home loan stretches your repayment timeline, increases your total debt, and only delivers a tax benefit when you use the money for specific housing-related purposes and keep the paperwork to prove it. This article covers top-up home loan meaning, rules, eligibility, tax treatment, EMI impact, and a practical comparison with alternatives — so you can decide whether borrowing more actually makes sense for your situation.

Quick Answer: Top-Up Home Loan Meaning

Top-up home loan meaning is an additional loan taken over an existing home loan, usually from the same lender. For example, a borrower may take a ₹5 lakh top-up for renovation, education or debt consolidation, but should compare EMI, total interest, processing fee and tax-use proof before applying.

Key Takeaways

- A top-up home loan is an additional amount borrowed against an existing home loan — not a separate product — and can be offered by the same lender or through a balance transfer to a new lender.

- Interest rates on top-up home loans are generally lower than personal loan rates, but adding ₹5 lakh for ten years can cost more in total interest than a shorter-tenure personal loan — always compare total cost, not just the monthly EMI.

- Tax deduction under Section 24(b) is available on the interest component only if the top-up amount is used for purchase, construction, repair, renewal, or reconstruction of a residential property — and you must keep invoices and bank records to prove the end use.

- Eligibility depends on your repayment track record, income stability, outstanding loan balance, property valuation, and credit score — not simply on your original loan approval.

- A longer tenure reduces your monthly EMI but significantly increases the total interest you pay — a ₹5 lakh top-up over 10 years can cost more than double the interest of the same loan over 5 years.

- If you use the top-up for non-housing purposes such as education, medical expenses, or debt consolidation, the Section 24(b) interest deduction does not apply to that portion.

- Processing fees, valuation charges, and legal costs add to total borrowing cost — compare the all-in cost, not only the quoted interest rate.

Key Facts at a Glance

| Parameter | What to Know | Watch Out For |

|---|---|---|

| Product type | Additional loan on top of an existing home loan, with the same lender or a new lender via balance transfer | Treated as a secured loan; the same property remains the collateral |

| Common end uses | Home renovation, repair, education fees, medical emergencies, debt consolidation | Tax benefit is only available for housing-related use; personal or consumption use disqualifies the deduction |

| Processing fee | Charged by lenders on the top-up amount; varies by lender, loan size, and borrower profile | Check loan processing charges carefully — these add to the effective all-in cost of borrowing |

| Tax treatment | Interest deductible under Section 24(b) for housing use; principal generally not eligible under Section 80C for renovation or non-purchase top-ups | End-use proof — invoices, contractor agreements, bank statements — is mandatory to support any tax claim |

| Tenure | Typically up to the remaining tenure of the original home loan, subject to lender policy | Longer tenure means lower EMI but significantly higher total interest outgo |

| Approval dependency | Based on repayment history, income, LTV ratio, and current property valuation | Approval is not guaranteed just because the original home loan was sanctioned years ago |

How a Top-Up Home Loan Works: The Complete Picture

A top-up home loan is an additional credit facility extended to an existing home loan borrower. Instead of applying for a new unsecured loan — with a higher interest rate and a separate repayment schedule — you approach your current home loan lender for extra funds, using the same underlying property as security.

The lender does not simply hand over money because you already have a relationship. A fresh eligibility assessment happens every time. The lender looks at your outstanding principal on the original loan, the current market value of your property, and whether the combined loan-to-value ratio stays within their approved limit. Beyond that, your income stability, recent repayment track record, and credit profile all influence both the approval decision and the interest rate you receive.

Existing Lender vs. the Balance Transfer Route

Most borrowers take a top-up from their existing lender because it involves less paperwork and a familiar process. However, you can also access a top-up when switching your home loan to a different lender through a balance transfer. In that case, the new lender pays off your original loan and simultaneously extends the top-up amount. This route can make sense if your existing loan rate is high — but you must factor in balance transfer fees and processing charges before concluding it actually saves money.

Why Your Credit Profile Still Matters

Your lender will check your credit file before approving the top-up. A strong repayment history on the original home loan helps considerably, but your overall credit utilisation and any late payments on other obligations also factor in. Understanding what constitutes a good CIBIL score before applying will help you know whether to proceed now or wait until your credit profile is in better shape.

Why Tenure and Total Interest Matter More Than EMI

The most common trap with top-up home loans is focusing only on the monthly EMI. Because the interest rate is typically lower than a personal loan and the tenure can stretch over several years, the EMI looks modest. But a longer tenure means a significantly higher total interest outgo. A ₹5 lakh borrowing at an assumed 9% per annum over 10 years costs roughly ₹2.6 lakh in interest. The same amount over 5 years costs under ₹1.25 lakh. The difference is not trivial — you are paying more than double for the comfort of a lower monthly number.

As per RBI’s fair lending guidelines, borrowers are entitled to a clear breakdown of total repayment cost before signing any loan agreement. Ask your lender for the total interest payable across the full tenure, not just the EMI figure quoted in the offer sheet.

How Top-Up Loan Tax Benefit Actually Works

The tax treatment of a top-up home loan depends entirely on what you do with the money — not on the fact that it is linked to a home loan. The Income Tax Act allows deduction of interest paid under Section 24(b) if the funds are used for purchase, construction, repair, renewal, or reconstruction of a residential property. For a self-occupied property, the annual interest deduction limit under Section 24(b) is ₹2 lakh. For a let-out property, there is no upper ceiling on the interest deduction, subject to overall set-off rules — but verify the current provisions for your assessment year at incometax.gov.in.

If you use the top-up for education fees, a family medical emergency, or any non-housing purpose, the Section 24(b) deduction does not apply to that borrowing. Your lender does not check your end use — but the Income Tax Department can. You need invoices, contractor agreements, and bank statements showing money flowing directly to the renovation or construction work. Without that paper trail, a deduction claim can be disallowed at scrutiny.

Principal Deduction Under Section 80C

Section 80C allows deduction on the principal component of a home loan — but only when the loan is used for purchase or construction of a residential property. A top-up used for renovation, repair, or any non-purchase purpose does not qualify for Section 80C deduction on the principal. Many borrowers assume that because it is linked to a home loan, all the usual home loan tax benefits apply automatically. They do not. The qualifying end use and the documentation supporting it are what determine the deduction — not the loan type.

Separation of Product Approval from Tax Eligibility

This is the single most important concept to understand. Your lender will approve the top-up based on financial and credit criteria. That approval has no bearing on whether the amount qualifies for a tax deduction. Tax eligibility is determined by the Income Tax Act, assessed by a tax officer, and depends on how you actually use and document the funds. These are two completely separate evaluations.

Real Example: Rohit’s Renovation Top-Up in Bengaluru

Rohit Sharma, 36, is a senior software engineer in Bengaluru earning ₹24 lakh per year. He has an active home loan with an outstanding balance of ₹28 lakh, and his current EMI is ₹26,400 per month. He needs ₹5 lakh — ₹3.5 lakh for a full kitchen renovation and ₹1.5 lakh for his daughter’s school admission fee deposit.

His lender offers a top-up home loan at an assumed rate of 9% per annum. Rohit compares two tenure options:

- 5-year tenure: EMI approximately ₹10,374 per month | Total interest approximately ₹1,22,440

- 10-year tenure: EMI approximately ₹6,333 per month | Total interest approximately ₹2,59,960

His combined EMI at the 5-year option is ₹36,774 — roughly 36% of his monthly take-home. At the 10-year option it is ₹32,733, which feels more comfortable but costs an additional ₹1,37,520 in interest over the loan’s life. Rohit collects all renovation invoices and ensures contractor payments go through his bank account — so the ₹3.5 lakh kitchen renovation portion qualifies for Section 24(b) interest deduction. The ₹1.5 lakh school deposit does not. He separates the fund usage clearly in his records from day one.

Use Ridhi’s tool to check your own EMI impact clearly before finalising the tenure and loan amount for your situation.

Note: All rates and EMI figures above use an assumed 9% p.a. for illustration only. Verify the actual rate with your lender before applying.

How to Calculate Top-Up Home Loan Cost

The EMI formula for a top-up home loan uses the standard reducing-balance method applied to all term loans:

EMI = P × r × (1 + r)ⁿ ÷ [(1 + r)ⁿ − 1]

Where P = Principal amount | r = Monthly interest rate (annual rate ÷ 12 ÷ 100) | n = Tenure in months

Using the ₹5 lakh example at an assumed rate of 9% per annum, here is how the cost changes with tenure:

| Scenario | Key Inputs (assumed 9% p.a.) | Result |

|---|---|---|

| 5-year tenure | ₹5 lakh principal, 60 months, 9% p.a. | EMI ≈ ₹10,374 | Total interest ≈ ₹1,22,440 |

| 10-year tenure | ₹5 lakh principal, 120 months, 9% p.a. | EMI ≈ ₹6,333 | Total interest ≈ ₹2,59,960 |

| Cost of choosing longer tenure | Monthly EMI saving: ₹4,041 | Extra interest paid over full tenure: ₹1,37,520 |

Choosing a 10-year tenure saves you ₹4,041 per month on EMI — but costs you an additional ₹1,37,520 over the loan’s life. If your cash flow can support the higher EMI, the shorter tenure is almost always the better financial choice. All figures above are illustrative. Use Ridhi’s EMI calculator to model your actual scenario with the rate your lender quotes and confirm total interest before signing.

Comparison: Top-Up Home Loan vs Personal Loan vs LAP

| Parameter | Top-Up Home Loan | Personal Loan |

|---|---|---|

| Interest rate | Generally lower than personal loan; varies by lender, credit profile, and tenure | Generally higher; varies significantly by lender, income, and CIBIL score |

| Collateral | Secured — property already under mortgage serves as collateral | Unsecured — no property or asset pledged |

| Approval speed | Moderate — requires property valuation, income check, and LTV assessment | Generally faster — primarily income and credit score verification |

| Tenure available | Up to the remaining tenure of the original home loan | Typically 1–5 years |

| Tax benefit | Available on interest for housing use, with documentation proof | Not available for standard personal use purposes |

| Documentation burden | Higher — property papers, valuation report, income proof required | Lighter — salary slips, bank statements, identity documents |

| Risk on default | Property at risk — secured loan against mortgaged asset | Credit score damage and legal recovery proceedings — no property risk |

| Best suited for | Planned housing-related expenses with sufficient repayment capacity | Urgent, short-tenure needs where speed matters more than rate |

For the balance transfer option with top-up: this route makes sense only when your existing home loan carries a significantly higher rate than the new lender offers, and the combined savings across the remaining tenure outweigh the transfer and processing charges. Do not assume a balance transfer automatically saves money — calculate the all-in cost including fees before deciding.

Loan Against Property (LAP) is a separate product. LAP uses your property as collateral but is not linked to an active home loan — it typically carries a higher interest rate than a home loan top-up and has different documentation requirements. LAP may be relevant when your original home loan balance is very low or fully repaid and you need a large amount.

How to Decide What’s Right for You

You need funds for home renovation, repair, or construction — and you have invoices and a bank payment trail to prove the end use — THEN a top-up home loan may qualify for Section 24(b) tax deduction, reducing the effective interest cost below the stated rate.

Your combined EMI after adding the top-up stays below 40–45% of your net monthly income — THEN the additional debt remains within a manageable range for most salaried borrowers with stable employment.

You need the money urgently and cannot wait for property valuation and lender processing time — THEN a personal loan may be the faster option, even at a higher interest rate, because the total interest on a short 1–2 year tenure may still be competitive.

Your existing home loan carries a meaningfully higher interest rate than current market rates — THEN explore a balance transfer with top-up, but calculate the total cost including transfer fees, processing charges, and legal costs before concluding it saves money.

You have surplus income every month beyond your current EMI — THEN consider whether using that surplus to prepay the existing loan is a better option than borrowing more. More debt is not the only answer when you already have a home loan outstanding.

You cannot comfortably absorb the higher combined EMI, or the purpose is purely lifestyle-driven spending with no productive return — THEN do not take a top-up home loan. Stretching your property’s mortgage for a vacation or discretionary upgrade rarely makes financial sense. It may be worth reviewing whether prepayment versus part payment on your existing loan is a better use of available funds first.

Common Mistakes to Avoid

Assuming the Tax Benefit Is Automatic

Many borrowers believe that any loan linked to a home loan automatically qualifies for housing tax deductions.

It does not. Section 24(b) applies only when the funds are used for purchase, construction, repair, renewal, or reconstruction of a residential property. Using the top-up for education fees or a family medical emergency means no Section 24(b) deduction applies to that interest — even though the loan itself is secured against a home.

Consult your tax advisor before filing, and maintain a complete paper trail of how every rupee was used from the day of disbursement.

Focusing Only on the Monthly EMI

A ₹5 lakh top-up over 10 years looks manageable at roughly ₹6,333 per month. But the total interest outgo over that period is approximately ₹2,59,960. The same loan over 5 years costs only about ₹1,22,440 in interest.

Always compare total cost — principal plus total interest — across the full tenure before accepting any loan offer. The YMYL principle here is simple: the EMI tells you what you pay this month; the total cost tells you what the borrowing actually costs you.

Not Keeping End-Use Documentation

The Income Tax Department can ask for proof of how the borrowed funds were used, especially during scrutiny. Without this, a deduction claimed under Section 24(b) can be disallowed.

Maintain all contractor invoices, material purchase bills, work completion records, and bank statements clearly showing payments from the disbursed top-up amount — stored together and accessible.

Borrowing More Than You Need Because You Are Eligible

Lenders will tell you the maximum top-up you qualify for. That is not a budget recommendation.

If you need ₹5 lakh and the lender approves ₹9 lakh, borrowing the full amount adds ₹4 lakh in unnecessary debt, with its own interest cost running for years. Borrow only what the specific expense requires.

Ignoring All Charges Beyond the Interest Rate

Processing fees, property valuation charges, and legal fees add to the effective cost of a top-up home loan. On a ₹5 lakh loan, a 1% processing fee is ₹5,000 upfront — which materially increases the effective annualised cost if the tenure is short.

Ask your lender for a complete itemised fee list before accepting the sanction, and factor these into your total cost comparison.

Extending Tenure Without a Prepayment Plan

A longer tenure is not inherently wrong — but only if you plan to make part-prepayments when cash flow allows.

Stretching a ₹5 lakh borrowing to 10 years with no intention to prepay commits you to paying roughly ₹1,37,520 more in interest than the 5-year option — for nothing other than a lower monthly number. That is a significant and avoidable cost.

When This May Not Be the Right Choice

A top-up home loan adds secured debt to a property already under mortgage. In some situations, the apparent convenience of easy borrowing can quietly weaken your financial position.

If your existing home loan EMI already consumes more than 45–50% of your net monthly income, adding a top-up puts your cash flow under real stress — particularly in the event of a job change, salary revision delay, or an unplanned family expense.

If your income is variable, commission-based, or dependent on a single employer without a backup income source, increasing secured debt against your home carries meaningful risk. A sustained repayment default can trigger recovery proceedings against the property itself.

If the purpose is purely discretionary — a luxury renovation upgrade, a holiday, or consumer goods — the return on the borrowing is zero while the interest cost is real and continues for years.

If you do not have clear documentation for the proposed housing use, or the funds will be split between housing and non-housing purposes without clear separation, the tax benefit you expect may not materialise — making the effective cost higher than you assumed when you decided to borrow.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax deduction eligibility, applicable limits, and end-use conditions for top-up home loans are governed by the Income Tax Act of India. Verify the current rules, the applicable assessment year provisions, and any changes introduced by the most recent Union Budget directly at incometax.gov.in. Eligibility and limits under the old tax regime differ from those under the new default regime — confirm which applies to your filing before claiming any deduction.

For lender-specific rules — including interest rate, processing fee, tenure policy, LTV cap, foreclosure terms, and prepayment conditions — verify directly with your bank or NBFC’s official website. These vary significantly across institutions and can change at any time.

RBI’s guidelines on fair practice codes, responsible lending, and borrower rights are available at rbi.org.in.

For a detailed explanation of housing loan deductions under Section 24(b) and Section 80C and how they apply to different loan purposes, see home loan deductions.

- Income Tax Department — incometax.gov.in

- Reserve Bank of India — rbi.org.in

- Your bank or NBFC’s official website — for product-specific rates, fees, and terms

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Ask your lender for a full cost sheet before accepting — this must include the total interest across the chosen tenure, processing fee, valuation charge, and any prepayment or foreclosure terms. Compare this all-in figure across at least two lenders before deciding. The difference in total cost between lenders can be ₹30,000–₹50,000 on a ₹5 lakh top-up.

- If you are in the 30% tax bracket and plan to use the top-up for a housing purpose, document every rupee carefully — contractor agreement, GST invoices, and bank payments directly to vendors. A well-documented ₹5 lakh renovation loan can deliver a meaningful saving in annual tax on the interest component, subject to your overall Section 24(b) limit and assessment year rules.

- Do not choose the longest available tenure just to get a lower EMI. Choose the shortest tenure your cash flow can comfortably support, and set up an auto-debit for part-prepayment when annual bonuses or salary increments come through. This approach reduces total interest cost without straining your monthly budget.

- If you are considering a balance transfer to access a top-up at a lower rate, run the full numbers — savings from the rate reduction versus total charges incurred. A 0.5% rate improvement rarely justifies the transfer cost if you are within the last three to four years of the original loan.

- Keep the top-up funds and their usage tracked separately from your regular home loan — either in a dedicated bank account or in a clearly labelled section of your personal finance records. Mixing funds is the most common reason borrowers lose their documentation trail and cannot support a tax deduction claim when they need it.

- Check your credit report at least two months before applying for a top-up. Any errors, unresolved disputes, or outstanding defaults on your CIBIL file can delay approval or result in a higher rate offer. Resolving a credit report error takes time — starting early avoids urgency-driven borrowing decisions at worse terms.

Frequently Asked Questions

What is a top-up home loan in simple terms?

A top-up home loan is an additional loan you take on top of an existing home loan, usually from the same lender. The same property serves as collateral. The lender reassesses your income, repayment history, and property value at the time of application before approving the top-up amount — it is not an automatic extension of your original sanction.

Can a top-up home loan be used for home renovation?

Yes, and home renovation is one of the most common uses. If you use the top-up for repair, renewal, or reconstruction of your residential property, the interest paid may qualify for deduction under Section 24(b) of the Income Tax Act — provided you maintain proper invoices, contractor agreements, and bank payment records showing the money was used for that purpose.

Is a top-up home loan tax deductible?

The interest component is deductible under Section 24(b) only if the funds are used for a housing-related purpose: purchase, construction, repair, renewal, or reconstruction of a residential property. If you use the money for education, medical expenses, or any other non-housing purpose, Section 24(b) does not apply to that borrowing. Principal repayment on a renovation-purpose top-up also does not qualify for deduction under Section 80C.

Is a top-up home loan better than a personal loan?

It depends on your purpose, urgency, tenure, and documentation capability. A top-up home loan may offer a lower interest rate, but requires property valuation and takes longer to process, and it adds to the secured debt against your property. A personal loan is faster, unsecured, and suitable for urgent short-duration needs — though usually at a higher rate. For a very short tenure, the personal loan’s total interest cost can sometimes be competitive. Always compare total interest outgo, not just the rate.

Can I get a top-up home loan during a balance transfer?

Yes. Many lenders offer a top-up when you transfer your home loan to them. This can be useful if your existing loan carries a high interest rate. However, factor in all charges — processing fee, legal fee, valuation costs, and any prepayment penalty from your existing lender — before concluding that the combined route saves money overall.

Does applying for a top-up home loan affect my CIBIL score?

Yes, in two ways. First, a hard inquiry is made on your credit report at the time of application, which may cause a minor temporary dip in your score. Second, once disbursed, the top-up adds to your total outstanding debt, which may affect your credit utilisation ratio. Consistent on-time repayment of both the original home loan and the top-up will help your score recover and strengthen over time.

What documents are typically required for a top-up home loan?

Lender requirements vary, but the standard set includes: recent salary slips, Form 16, bank statements for the last 6–12 months, the original home loan sanction letter, the property’s registered title documents, and a current valuation report. If you intend to claim a tax deduction on the interest, you will additionally need invoices and proof of contractor payments showing the end use of the disbursed funds. Confirm the exact list with your lender before applying.

Can I prepay a top-up home loan before the tenure ends?

Most lenders allow prepayment on top-up home loans. For floating-rate loans, RBI guidelines generally permit prepayment without penalty for individual borrowers. Fixed-rate top-up loans may carry a foreclosure charge. Confirm your lender’s specific prepayment terms in the sanction letter before signing, and factor this into your decision if you plan to close the loan early.

What happens if I claim a tax deduction on a top-up used for non-housing purposes?

This is a compliance risk you should not take. If the Income Tax Department reviews your return and the actual end use does not match the claimed deduction, the deduction can be disallowed. You may also face interest on the tax differential and potential penalties. Always use the top-up funds for the stated qualifying purpose and maintain documentation from the day of disbursement.

Is the interest rate on a top-up the same as my original home loan rate?

Not always. Some lenders match the top-up rate to the original home loan rate; others price it slightly higher based on the nature of the end use and borrower profile. The rate offered depends on your current credit score, income, outstanding balance, and lender policy at the time of your application. Always confirm the actual rate in the written offer — not just from verbal communication or promotional material.

Final Verdict

A top-up home loan can be a practical and cost-efficient option when you have a genuine housing-related need, a stable income, a manageable existing EMI, and the documentation to support a tax claim. For a borrower like Rohit — who needs ₹5 lakh for a clearly defined renovation and keeps his invoices and bank records in order — the top-up home loan meaning translates into real savings compared to an unsecured personal loan over the same tenure.

But the lower rate does not make it free or risk-free. Your property backs this loan. The tenure you choose directly determines your total interest outgo — not just your monthly EMI. The tax benefit is conditional on end-use proof and the provisions applicable to your assessment year. Borrowing more than you need, for longer than necessary, quietly adds up to lakhs in avoidable interest cost.

Use a top-up home loan for planned, essential, and productive purposes — not for convenience or lifestyle spending. Compare total cost, tenure, fees, tax eligibility, and impact on your cash flow carefully before signing. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.