₹1 lakh a month sounds comfortable — until you sit down to actually plan it. Rent, groceries, school fees, EMIs, parents’ medical bills, insurance premiums, and the occasional weekend out have a way of consuming a 1 lakh salary budget faster than most people expect. And yet, the professionals who build real financial security on this income are not earning more than you. They are structured differently.

The gap between feeling financially stretched on ₹1 lakh and building genuine wealth on the same salary is almost always about clarity — knowing what goes where before the month slips away. This guide gives you four practical Indian budget templates across different household types, explains the thinking behind each split, and helps you personalise the plan without vague advice or western-style frameworks that ignore rent, EPF, and school fees.

Quick Answer: 1 Lakh Salary Budget

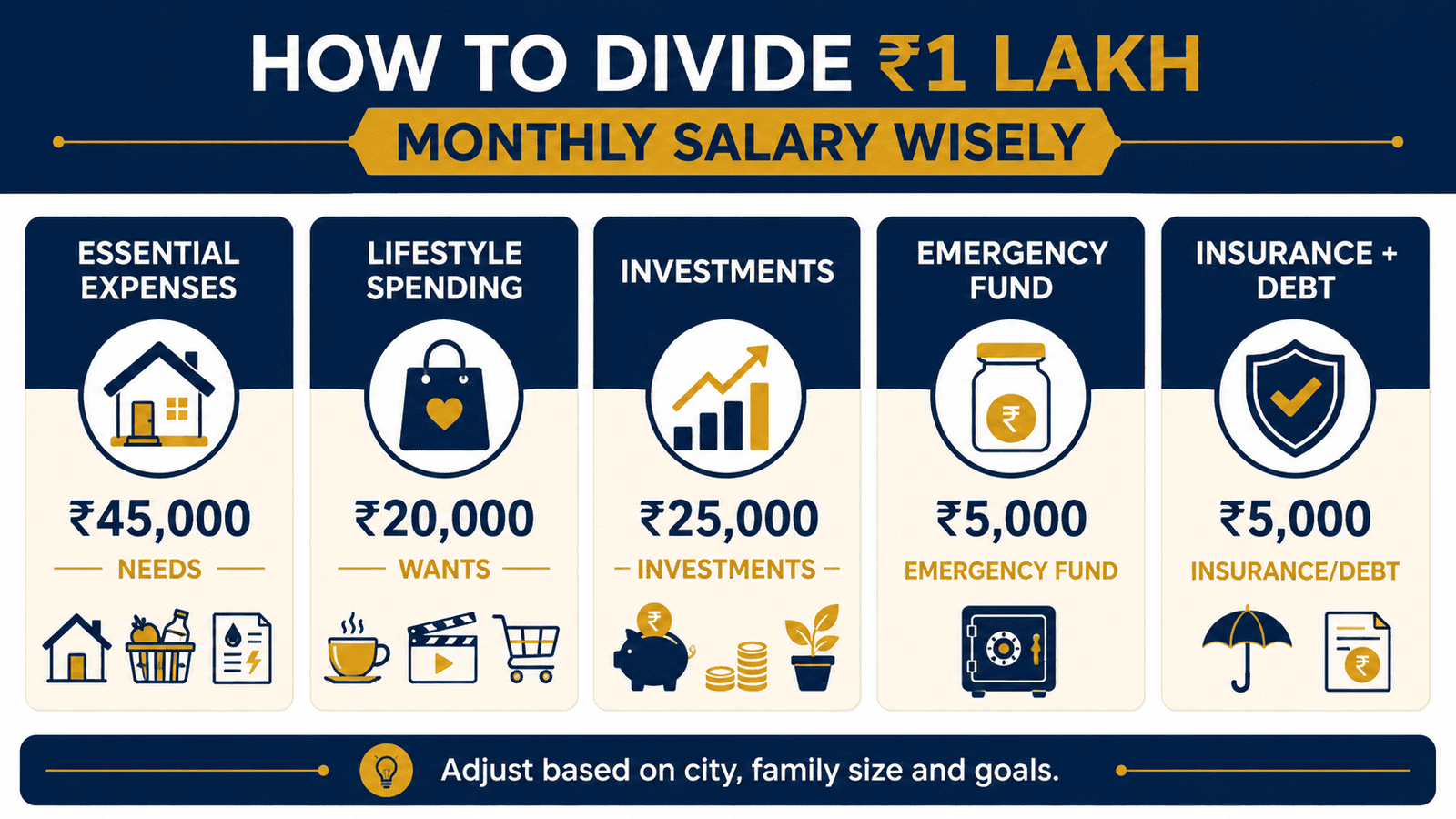

A 1 lakh salary budget should first cover essentials, then protect your family, then invest for goals. A practical split can be ₹50,000–₹60,000 for needs, ₹20,000–₹30,000 for SIPs and savings, ₹5,000–₹10,000 for insurance or emergency fund, and the rest for lifestyle, travel, or debt prepayment.

Key Takeaways

- Always budget from your monthly bank credit — not your CTC. EPF contributions, income tax, and professional tax can bring a ₹1 lakh gross salary down to ₹78,000–₹88,000 in hand, depending on your tax regime and salary structure.

- Keep fixed needs — rent, EMIs, groceries, utilities, and commute — under 55–60% of take-home. That means no more than ₹55,000–₹60,000 on essentials before any discretionary rupee moves.

- Build an emergency fund of 3–6 months of essential expenses before increasing SIP amounts or moving into riskier investments. For most ₹1 lakh households, this means saving ₹1.5 lakh to ₹3.3 lakh in a liquid fund or savings account first.

- Your combined EMI burden — home loan, car loan, personal loan — should ideally stay under 40% of take-home. That is roughly ₹35,000–₹40,000 maximum if you also want room for savings and insurance.

- Term insurance and a family health cover together typically cost ₹4,000–₹8,000 per month as a rough planning figure. Actual premiums vary by age, health status, and insurer — verify with IRDAI-registered providers.

- Mutual fund SIPs are subject to market risks. Past performance does not guarantee future returns. Even so, automating ₹15,000–₹20,000 per month consistently over 10–15 years creates a meaningfully different financial outcome than ad hoc investing.

- Review your budget every quarter and rebuild it immediately after any major life change — salary increment, new EMI, baby, or job switch.

Key Facts at a Glance

| Budget Category | Suggested Range | % of Take-Home |

|---|---|---|

| Needs (rent, EMI, groceries, utilities, commute, school fees) | ₹50,000–₹60,000 | 50–60% |

| Savings and Investments (SIPs, PPF, EPF voluntary top-up) | ₹20,000–₹30,000 | 20–30% |

| Protection (health insurance, term insurance, emergency fund top-up) | ₹5,000–₹10,000 | 5–10% |

| Lifestyle and Wants (dining, subscriptions, shopping, travel) | ₹5,000–₹10,000 | 5–10% |

| Emergency Fund Target | ₹1.5L–₹3.3L total | 3–6 months of essential expenses |

| Safe EMI-to-income ceiling | Max ₹35,000–₹40,000 | Under 40% of take-home |

| Budget base | Monthly bank credit | Not CTC or gross salary |

Before building any budget, confirm your actual take-home salary. Use the take-home salary estimate to see what actually lands in your account after EPF, tax, and all deductions.

How to Build a 1 Lakh Salary Budget: Step by Step

Step 1 — Start with What You Actually Receive, Not What Your Offer Letter Says

This is where most budget plans collapse before they begin. A ₹1 lakh CTC and a ₹1 lakh take-home salary are almost never the same number. Your employer deducts 12% of your basic salary toward EPF before the money reaches your account. Income tax — whether under the old regime or the new regime — takes another slice. Add professional tax, group insurance contributions, and any advance salary deductions, and many employees with a ₹1 lakh package actually receive ₹74,000–₹87,000 in their bank account each month.

The right budgeting base is the amount credited to your account on salary day — nothing else. Pull up your last three bank statements and use that average as your starting point. Building a budget on CTC is one of the fastest ways to permanently feel short.

Step 2 — Separate Fixed Expenses from Variable Ones

Fixed expenses are the ones that arrive whether or not you have a good month: rent, EMIs, school fees, and insurance premiums. Variable expenses fluctuate: groceries, fuel, utilities, dining, and shopping. Most people underestimate their fixed expenses and overestimate their control over variable ones.

Write down every fixed expense first. Add them up. If this number is above ₹55,000–₹60,000, you have a structural problem that no budgeting tip can solve — you need to either reduce a fixed commitment (EMI, rent) or acknowledge that your lifestyle and investment allocations will be smaller until income grows.

Step 3 — Understand the 50-30-20 Rule and Why India Needs an Adjusted Version

The 50-30-20 budgeting framework divides income into three buckets: 50% for needs, 30% for wants, and 20% for savings. It is a useful starting structure — but it was designed for western salaries with lower rent-to-income ratios and employer-funded healthcare. In Indian metros, rent alone can consume 25–35% of take-home salary. A family in Bengaluru paying ₹28,000 rent on ₹85,000 take-home has used up 33% on rent before a single other expense.

A more practical Indian version for a ₹1 lakh salary looks like this: 55–60% for needs (including rent, EMI, school fees, groceries, utilities), 20–25% for savings and investments, 5–10% for protection (insurance and emergency fund), and 10–15% for lifestyle. The exact split changes by city, family size, and debt situation — which is why this article gives four different templates rather than one fixed rule.

Step 4 — Build Your Emergency Fund Before Investing Aggressively

Most first-time investors start SIPs before building any liquidity buffer. This works fine — until a medical emergency, a delayed salary, or a sudden job loss makes it necessary to redeem equity funds at the worst possible time.

As per general financial planning guidance, a salaried employee should aim for 3–6 months of essential expenses in a liquid instrument before increasing equity exposure. For a household with ₹55,000 in monthly essential expenses, this means building ₹1.65 lakh to ₹3.3 lakh in a savings account or liquid mutual fund first. Use the emergency fund amount calculator to find your specific target based on your household expenses.

This fund is not an investment. It is an insurance policy against disruption. Do not put it in equity. Do not merge it with your regular savings account if you tend to dip into it. A separate zero-balance account or a liquid fund with instant redemption access works best for most salaried professionals.

Step 5 — Plan Insurance Before Planning Investments

Health insurance and term insurance are not lifestyle upgrades. They are the foundation that protects every other financial decision you make. A single hospitalisation without health cover can wipe out two years of SIPs. A breadwinner’s death without term insurance can leave a family with no income and an active home loan.

As regulated by IRDAI (irdai.gov.in), insurance products vary significantly by coverage, exclusions, and premium structure. A rough planning figure for a 30–35-year-old earning ₹1 lakh per month: a family floater health cover of ₹10–₹20 lakh and a term life cover of at least ₹1 crore. Combined, these can cost ₹4,000–₹8,000 per month depending on age, health, insurer, and policy type. Insurance is a subject matter of solicitation — always read the policy document carefully before purchasing.

Step 6 — Allocate Investments Based on Goals, Not Enthusiasm

SIPs, PPF, ELSS, and NPS are all valid instruments — but which one you choose depends entirely on your financial goal, time horizon, and risk appetite. A ₹20,000 monthly investment going into a 3-year ELSS is very different from ₹20,000 going into a liquid fund for a home down payment in 18 months.

According to SEBI guidelines, mutual fund investments are subject to market risks. Past performance does not guarantee future returns. Map every investment to a specific goal before starting — child education in 12 years, home purchase in 5 years, retirement in 25 years — and choose instruments accordingly. Generic advice to “just start SIPs” without a goal leads to premature redemptions and poor outcomes.

Real Example: Four ₹1 Lakh Budget Templates for Indian Households

Rohan, 32, works as a software professional in Pune and takes home ₹86,000 per month (after EPF and tax on a ₹1 lakh gross package). Here is how the budget changes across four realistic household situations.

| Category | Single (Metro Renter) | Family with Child |

|---|---|---|

| Rent | ₹22,000 | ₹28,000 |

| Groceries and household | ₹7,000 | ₹12,000 |

| School fees and child expenses | — | ₹8,000 |

| Utilities, fuel, commute | ₹5,000 | ₹6,000 |

| Insurance (health + term) | ₹3,500 | ₹6,000 |

| EMI (if any) | — | ₹10,000 |

| Emergency fund top-up | ₹5,000 | ₹3,000 |

| SIP (mutual funds) | ₹25,000 | ₹8,000 |

| Lifestyle and dining | ₹12,500 | ₹5,000 |

| Total | ₹80,000 | ₹86,000 |

The key insight: Rohan’s SIP drops from ₹25,000 to ₹8,000 once he has a child and a home loan EMI. That is not a failure — it is a realistic life-stage adjustment. The goal is to protect the emergency fund and insurance before cutting investments, not the other way around. As income grows — through salary increments — SIPs should be increased proportionally. Use the monthly SIP planning tool to see how even ₹8,000 per month compounds over different time horizons. Mutual fund investments are subject to market risks and illustrative returns do not guarantee actual outcomes.

How to Calculate Your Personal ₹1 Lakh Budget Allocation

Usable Discretionary Budget = Take-Home Salary − (Fixed Needs + Insurance Premiums + EMIs + Emergency Fund Top-Up)

Here is a step-by-step worked example using Rohan’s numbers.

Step 1: Establish take-home salary → ₹86,000

Step 2: Add up fixed needs → Rent ₹22,000 + Groceries ₹7,000 + Utilities and commute ₹5,000 = ₹34,000

Step 3: Add insurance premiums → ₹3,500

Step 4: Add emergency fund top-up (until target is reached) → ₹5,000

Step 5: Subtract total from take-home → ₹86,000 − ₹42,500 = ₹43,500 left for investments and lifestyle

Step 6: Allocate SIP first (₹25,000), then lifestyle (₹12,500), with ₹6,000 buffer.

| Scenario | Fixed Needs + Protection | Available for Investment + Lifestyle |

|---|---|---|

| Single, no EMI, metro rent ₹22,000 | ₹42,500 | ₹43,500 |

| Couple, home loan EMI ₹20,000, rent-free | ₹48,000 | ₹38,000 |

| Family, child school fees ₹8,000, EMI ₹10,000 | ₹65,000 | ₹21,000 |

These are sample amounts and not personalised recommendations. Use the monthly budget calculator to enter your exact expense figures and get a customised allocation instantly.

Comparison: Which Budgeting Framework Works Best for a ₹1 Lakh Salary?

| Framework | Best For | Risk If Misused |

|---|---|---|

| 50-30-20 Rule | Single earners with stable income and low EMIs; good as a starting template | Fails for families with high rent or child expenses — lifestyle bucket shrinks to zero |

| Zero-Based Budget | Detail-oriented professionals; every rupee assigned a job before the month starts | Requires consistent monthly effort; fails if you skip even one monthly review |

| Goal-First Budget | Investors with specific targets (home in 5 years, education fund, retirement) | Can over-invest in SIPs before emergency fund is built; liquidity risk in downturns |

| Debt-First Budget | Households with high-interest credit card debt or personal loans above 14% interest | If debt repayment consumes all surplus, no emergency fund forms and insurance lapses |

| Family-First Budget | Families with dependents, parents, or school-going children with variable monthly needs | Lifestyle and investment buckets often get squeezed; needs a strict annual review |

How to Decide What’s Right for You

The right budget split is not the one that looks cleanest on a spreadsheet — it is the one that reflects your actual life.

You are single, pay rent under ₹20,000, have no EMI, and live in a Tier 2 city — THEN the standard 50-30-20 split works well. You can direct ₹20,000–₹25,000 toward SIPs while still maintaining a healthy lifestyle budget.

You have a family with a child and a home loan EMI above ₹15,000 — THEN prioritise emergency fund completion and insurance before increasing SIPs. Your investment allocation may realistically be ₹8,000–₹12,000 per month until income grows.

Your total EMIs (home loan plus car loan plus personal loan) exceed ₹40,000 per month — THEN your budget is structurally stressed. Reduce or prepay high-interest debt before starting new investment commitments.

You have credit card revolving debt at 36–42% annual interest — THEN pay that off completely before any SIP. No equity mutual fund consistently beats 36% guaranteed savings from debt elimination.

You support ageing parents financially — THEN treat that support as a fixed need, not a discretionary expense. Budget it upfront alongside rent and EMIs before allocating to investments or lifestyle.

You do not yet have 3 months of expenses saved in a liquid account — THEN this is not the right time to lock money into long-term or illiquid investments like ELSS or PPF. Build your emergency fund first. Check your target with the health insurance budget planner to also confirm your family’s protection costs are adequately planned.

You are planning to buy a home in the next 3 years — THEN keep your down payment savings in a debt fund or recurring deposit, not in equity SIPs. Market volatility can erode a 3-year equity corpus at exactly the wrong time.

Common Mistakes to Avoid

Budgeting from CTC Instead of Bank Credit

Many salaried employees mentally plan expenses based on their offer letter figure — ₹1 lakh — but receive ₹78,000–₹87,000 in their account after EPF and tax deductions.

This gap of ₹13,000–₹22,000 means rent, SIPs, and lifestyle spending all feel harder than they should — because the budget was built on a number that never arrives. Consistently spending as if you earn ₹1 lakh when you receive ₹84,000 creates a monthly shortfall that quietly builds into credit card debt.

Check your last three months of bank credits and use the lowest as your budget base. Salary delays, variable components, or LOP months make the average more reliable than the headline number.

Ignoring Annual Expenses in Monthly Planning

Annual expenses — term insurance premium, vehicle insurance, school admission fees, medical checkups, home repairs, and vacation — arrive infrequently but hit hard when they do.

A ₹25,000 annual premium paid in January is the same as ₹2,083 per month. If you do not budget it monthly, January becomes a financial emergency every year. Over 10 years, this unpredictability causes unnecessary credit card usage and redemption of investment funds.

Estimate all annual expenses at the start of the year, divide by 12, and move that amount into a separate sinking fund account each month.

Starting SIPs Before Building an Emergency Fund

Starting equity SIPs without a liquid emergency buffer is a common mistake among first-time investors eager to begin wealth creation.

When a job loss, medical emergency, or large repair expense arrives, the investor is forced to redeem equity SIPs — often at a loss, during a market correction, and with short-term capital gains tax. The emergency fund that would have prevented all of this could have been built in 6–9 months of disciplined saving.

Build ₹1.5 lakh to ₹3 lakh in a savings account or liquid fund before increasing equity exposure.

Paying Only the Minimum Due on Credit Cards

Credit card minimum due payments are designed to look manageable while the revolving balance compounds at 36–42% annual interest.

Paying ₹3,500 minimum due on a ₹35,000 outstanding balance means the remaining ₹31,500 accrues interest at 3% per month. Over 6 months, this can cost ₹5,000–₹8,000 in interest alone — money that could have funded an entire SIP. Use the debt repayment plan to calculate the fastest payoff path for your outstanding balances.

Always pay the full outstanding balance each month. If you cannot, stop using the card until the balance is cleared.

Letting Lifestyle Inflate Immediately After a Salary Increment

Salary increments are the most powerful opportunity to accelerate wealth building — and the most common moment when spending permanently jumps instead.

A ₹10,000 increment directed entirely into lifestyle spending adds ₹1.2 lakh per year to expenses with zero financial return. The same increment split as ₹5,000 to SIP and ₹5,000 to lifestyle keeps quality of life improving while also compounding investments. The habit of splitting every increment between investments and lifestyle is one of the most reliable wealth-building behaviours available to a salaried professional.

Increase your SIP by at least 50% of every increment amount. Automate it on the same day salary hits the account.

Treating EPF as Invisible and Not Part of the Financial Plan

EPF contributions — 12% of basic salary from your account and a matching employer contribution — silently accumulate in your provident fund account each month. Many employees forget to factor this into their total savings rate.

For someone with a ₹40,000 basic salary, EPF adds ₹4,800 per month from the employee side alone — ₹57,600 per year — into a government-backed, interest-bearing corpus. Check your EPF balance and contribution history on the EPFO portal (epfindia.gov.in) and include it in your annual savings calculation. EPF interest rates are declared annually by the government; check the current rate on epfindia.gov.in before making projections.

Never withdraw EPF unless you have been unemployed for more than two months and have genuinely exhausted other liquidity options.

When This May Not Be the Right Choice

The sample budget templates in this article are built around a stable ₹1 lakh monthly take-home salary with predictable expenses. They may not suit your situation if:

- Your income is variable — freelance, commission-based, or project-linked income does not allow fixed SIP and EMI commitments to be planned reliably on a monthly basis.

- You have heavy medical or family obligations that consume more than 20–25% of income, leaving insufficient room for both protection and investment simultaneously.

- You are carrying high-interest personal loan or credit card debt above ₹3 lakh, where every investment rupee earns less than what the debt is costing you in interest.

- You are planning a home purchase within 18–24 months — the down payment requirement will demand a different savings and liquidity strategy than a standard budget split allows.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Budgeting guidance is evergreen, but the specific tax limits, EPF rates, insurance regulations, and investment rules that underpin your plan are subject to change with each Union Budget or regulatory update. Always verify current figures from official sources before making decisions.

- Income tax slabs and Section 80C, 80D limits: Income Tax Department — incometax.gov.in

- EPF contribution rates and interest rate declarations: EPFO — epfindia.gov.in

- Mutual fund regulations, SIP disclosures, and SEBI-registered advisors: SEBI — sebi.gov.in

- Health insurance and term insurance product terms, IRDAI-registered insurers: IRDAI — irdai.gov.in

- Credit, EMI, and lending rate guidelines: RBI — rbi.org.in

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Automate savings on salary day — not at the end of the month. Set up a standing instruction to move your SIP amount and emergency fund top-up to a separate account within 24 hours of salary credit. What leaves first gets saved; what stays gets spent.

- Create a dedicated annual-expense sinking fund. Estimate all yearly bills (insurance premiums, school fees, vehicle maintenance, vacation) at the start of the year, divide by 12, and park that fixed amount each month in a recurring deposit or liquid fund earmarked only for these.

- Use two bank accounts for daily spending: one for bills and fixed expenses, one for discretionary spending. When the discretionary account runs dry, it runs dry — no transfers, no borrowing. This single habit eliminates most lifestyle overspending without willpower.

- Review every active subscription on the 1st of each month. Streaming platforms, gym memberships, app subscriptions, and cloud storage bills accumulate silently. A 15-minute monthly audit often recovers ₹800–₹2,000 that can be redirected to savings.

- After every salary increment, immediately increase your SIP by at least 50% of the increment amount before adjusting lifestyle spending. A ₹12,000 increment split as ₹6,000 to SIP and ₹6,000 to lifestyle is far more powerful over 10 years than ₹12,000 going entirely into spending.

- Keep your rent-to-income ratio below 30% of take-home salary if at all possible. Paying ₹30,000 rent on ₹86,000 take-home (35%) leaves almost no room for both investment and lifestyle. If rent exceeds 30%, either negotiate a move or acknowledge that other buckets must compress until income grows.

- Set a quarterly budget review date — same day every quarter, 30 minutes on the calendar. Use it to check whether expenses have crept up, whether goals have changed, and whether the split still makes sense. Most financial drift is invisible until a quarterly review makes it visible.

Frequently Asked Questions

Is ₹1 lakh salary enough for a family in India?

Yes — in most Indian cities, a ₹1 lakh take-home salary can support a family comfortably if expenses are planned. In Tier 2 cities, ₹1 lakh allows for rent, child expenses, insurance, a moderate SIP, and a reasonable lifestyle. In high-rent metros like Mumbai or Bengaluru with EMIs, it requires tighter control of lifestyle spending. The key is structuring the budget before the month begins, not after.

How much should I save from ₹1 lakh salary?

A general planning range is 20–30% of take-home salary — roughly ₹17,000–₹26,000 if your take-home is ₹86,000. This includes SIPs, emergency fund contributions, and any voluntary EPF or PPF top-ups. The exact number depends on your existing EMIs, family size, rent level, and whether your emergency fund is already built. Saving less than 15% on a ₹1 lakh package for more than a year is a signal that expenses need review.

Can I invest ₹30,000 per month from ₹1 lakh salary?

If your take-home is ₹86,000 and fixed needs including rent, groceries, utilities, and insurance total ₹45,000, then ₹30,000 in monthly investments leaves only ₹11,000 for lifestyle. That works for a single professional with no EMI and moderate lifestyle. It does not work for a family with a child and home loan EMI. Mutual fund investments are subject to market risks — the right amount to invest is what you can sustain consistently without redeeming in an emergency.

How does the 50-30-20 rule work in India?

The 50-30-20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings. On an ₹86,000 take-home, that means ₹43,000 for needs, ₹25,800 for wants, and ₹17,200 for savings. In practice, most Indian households with rent, EMI, and child expenses find the 50% needs bucket insufficient — especially in metros. The rule works better as 60-20-20 or 55-20-25 for families. Treat it as a starting framework, not a fixed law.

How much emergency fund should a salaried person keep?

The standard planning guidance is 3–6 months of essential monthly expenses. For a household with ₹55,000 in fixed essential costs, the target is ₹1.65 lakh to ₹3.3 lakh. Keep this in a savings account or liquid mutual fund — not in equity funds, fixed deposits with premature withdrawal penalties, or locked-in instruments. Build it to minimum 3 months before increasing SIP amounts.

Should I invest first or repay debt first?

It depends on the interest rate on your debt. If you carry credit card debt at 36–42% annual interest, repaying it is guaranteed higher than any typical investment return. Pay that off first. For a home loan at 8.5–9%, you can reasonably invest alongside prepayment. For a personal loan above 14%, prioritise partial prepayment before increasing SIPs. High-interest debt and equity investment running simultaneously almost always results in a net negative outcome.

How much rent is safe on ₹1 lakh salary?

A commonly used planning benchmark is to keep rent below 30% of take-home salary. On an ₹86,000 take-home, that means keeping rent at or below ₹25,800. Paying ₹35,000 in rent on ₹86,000 take-home leaves only ₹51,000 for everything else — groceries, EMI, insurance, SIP, and lifestyle — which creates consistent financial stress. If your city makes sub-₹26,000 rent impossible, factor that into your investment expectations and lifestyle allocations rather than trying to follow the standard template.

How should a family budget ₹1 lakh per month?

A family with one child and a home loan EMI on ₹86,000 take-home might allocate: ₹28,000 rent, ₹12,000 groceries and household, ₹8,000 school fees, ₹6,000 utilities and commute, ₹10,000 home loan EMI, ₹6,000 insurance, ₹3,000 emergency fund top-up, ₹8,000 SIP, and ₹5,000 lifestyle. That totals ₹86,000. The investment amount is smaller than for a single person — but it is realistic, sustainable, and leaves insurance and protection intact. Increase SIPs as the home loan is paid down and school fees stabilise.

What happens if I cannot follow the budget for one month?

One difficult month does not break a well-structured budget — but it should trigger a review. If a month goes over budget due to a one-off expense (medical bill, repair, festival), use the emergency fund if needed and replenish it over the next 2–3 months. If the budget breaks every month, the issue is structural — either income is insufficient for current obligations or a fixed expense (rent, EMI) needs renegotiating. A budget that works on paper but fails in practice is telling you something specific about your expense structure.

Is zero-based budgeting realistic for Indian salaried employees?

Zero-based budgeting — where every rupee is assigned a specific job before the month starts — is powerful but requires monthly effort. It works best for detail-oriented professionals who want complete visibility into spending. It is less practical for households with highly variable monthly expenses (irregular medical costs, seasonal festival spending, fluctuating fuel costs). A hybrid approach — automate savings and fixed bills, then use a simplified tracker for the remainder — suits most Indian salaried employees better than a full zero-based system.

Final Verdict

A well-structured 1 lakh salary budget is one of the most effective financial tools available to any Indian salaried household. The professionals who feel financially free on ₹1 lakh are not spending less than those who feel stretched — they are spending in a sequence that puts protection and savings ahead of lifestyle, not after it.

Start by confirming your actual take-home salary. Build your emergency fund before increasing equity exposure. Protect your family with health and term insurance before optimising investment returns. Set up SIPs on the day salary arrives. Review the budget every quarter and after every major life change. Use the monthly budget calculator to turn this framework into a personalised monthly plan.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.