Your kitchen tiles are cracking. The bathroom wall shows damp patches. The electrical wiring is thirty years old and trips the MCB every other week. You need to spend money on the house — but you do not have ₹5–8 lakh sitting idle. Borrowing feels logical. But the phrase “home improvement loan” covers more than one product, the tax benefit is narrower than most people assume, and the total interest cost rarely gets calculated before the application goes in.

This article explains what a home improvement loan actually means in India, when interest may qualify for deduction under Section 24(b), how to calculate the true cost before you commit, and how to compare it against practical alternatives. If you are in the planning stage, this is where to start.

Quick Answer: Home Improvement Loan

A home improvement loan is money borrowed to repair, renovate, renew, or upgrade an existing house. In India, interest may qualify for deduction under Section 24(b), but limits such as ₹30,000 for repairs or renovation must be verified before filing. Always compare EMI, total interest, and tax-regime impact.

Key Takeaways

- A home improvement loan is for upgrading or repairing an existing residential property — not for buying or constructing a new one. The purpose distinction matters for both the lender and the tax department.

- Interest paid may qualify for deduction under Section 24(b) of the Income Tax Act, but the deduction limit for repair, renovation, and reconstruction on a self-occupied property is subject to conditions — verify the current limit from incometax.gov.in before filing.

- Principal repayment on a renovation or repair loan does not automatically qualify for Section 80C deduction the way a home purchase loan does — do not assume it does without professional guidance.

- If your total EMI burden after adding the renovation loan exceeds a safe debt-to-income ratio, the tax benefit does not offset the cash-flow strain. Calculate affordability first.

- A top-up home loan often carries a lower interest rate than a dedicated renovation loan or personal loan for existing home-loan borrowers — compare products before applying.

- Preserve every invoice, contractor estimate, and lender interest certificate if you plan to claim a tax deduction. Missing paperwork is the most common reason tax claims get questioned.

- Tax benefit under Section 24(b) is currently available only under the old tax regime for self-occupied property — if you have opted for the new regime, this deduction is not available. Verify the current regime rules before filing.

Key Facts at a Glance

| Parameter | Detail | What to Verify |

|---|---|---|

| Loan purpose | Repair, renovation, renewal, reconstruction of existing residential property | Confirm with lender what end-use is accepted |

| Tax angle | Interest may qualify under Section 24(b) of the Income Tax Act | incometax.gov.in — verify current limits and conditions |

| Self-occupied deduction limit (repair/renovation) | ₹30,000 per year (subject to change — verify before filing) | Income Tax Department official notification |

| Let-out property | Full interest may be deductible; verify current rules | incometax.gov.in — Section 24 |

| Principal repayment under 80C | Generally not applicable for repair/renovation loans | Consult a tax professional for your case |

| Key cost heads | Interest rate, processing fee, GST on fee, prepayment charges, insurance bundling | Lender sanction letter |

| Core documents | Loan sanction letter, interest certificate, renovation estimate, contractor invoices | Lender and your tax advisor |

| Tax regime caution | Section 24(b) deduction available under old tax regime for self-occupied; not available under new regime as of last confirmed rules | incometax.gov.in — verify for current assessment year |

What Is a Home Improvement Loan?

A home improvement loan is a loan taken specifically to repair, renovate, renew, or reconstruct an existing residential property that you already own. It is not for buying a new house or for funding a plot purchase. That distinction matters because the tax treatment, eligibility, and lender documentation requirements are different from a regular home purchase loan.

In India, there is no single universal product called a “home improvement loan.” Different lenders package the same concept differently. You may see it described as a home renovation loan, a home repair loan, or a home extension loan depending on the bank or NBFC. The underlying principle is the same: you borrow to improve a house you already own, and the end-use is verified through invoices, contractor estimates, and possession documents.

What Qualifies as Home Improvement?

According to the Income Tax Act, the relevant terms for Section 24(b) include repair, renewal, and reconstruction. In practical borrowing terms, most lenders accept the following as eligible renovation purposes:

- Waterproofing, roof repair, and seepage treatment

- Kitchen remodelling, bathroom renovation, and plumbing overhaul

- Electrical rewiring and upgrading the fuse board or MCB panel

- Flooring replacement — tiles, marble, or wood

- Painting, plastering, and false ceiling work

- Room additions or extensions where structurally permitted

Purely cosmetic or luxury additions — a new home theatre setup, a decorative garden, or high-end furniture — may not be treated as home improvement by all lenders and may not support a tax deduction claim. Always confirm the scope with your lender in writing before applying.

How Is It Different from a Personal Loan?

A personal loan is unsecured — you borrow on the basis of your salary and credit profile, and no property is pledged. A home improvement loan is typically secured against your property (or processed as an extension of your existing home loan). Because of the security, the interest rate on a renovation loan is usually lower than a personal loan. The trade-off: more paperwork, longer processing time, and end-use verification by the lender.

For a full breakdown of how home loan tax rules work including Section 24(b) interest treatment, see our guide on home loan tax rules.

Three Product Types You Will Encounter

When you approach a lender, the home improvement loan may be structured in one of three ways depending on your existing borrowing relationship and property profile:

- Dedicated renovation loan: A fresh loan with renovation as the declared purpose. The lender may disburse directly to the contractor or in stages against invoices.

- Top-up home loan: If you already have an active home loan with the same bank, a top-up on your existing loan at a similar or slightly higher rate is often faster and cheaper than starting a fresh application.

- Loan against property (LAP): For larger amounts, some borrowers mortgage their property and use the funds for renovation. This carries a different risk profile — if you default, you could lose the property.

The product you choose affects the interest rate, documentation, processing time, and tax eligibility. It is not a trivial decision.

Section 24(b) and Tax Benefit: What Borrowers Need to Know

Under Section 24(b) of the Income Tax Act, interest on money borrowed for the purpose of purchase, construction, repair, renewal, or reconstruction of a house property may be claimed as a deduction from income from house property. This is the legal basis for claiming interest paid on a home improvement loan as a deduction.

However, the deduction limits are different depending on whether the property is self-occupied or let out:

- Self-occupied property: The total interest deduction under Section 24(b) — combining purchase/construction interest and repair/renovation interest — is subject to an overall annual limit. For repair, renewal, and reconstruction specifically on a self-occupied house, the limit has historically been ₹30,000 per year. Verify the current limit from the Income Tax Department before filing.

- Let-out property: The full interest paid is generally deductible without a fixed ceiling, subject to set-off and carry-forward rules. This is a meaningful difference for landlords who borrow to improve a rented property.

Critically — this deduction is available only under the old tax regime. If you have opted for the new simplified tax regime under Section 115BAC, the Section 24(b) deduction for house property is not available for self-occupied property under the new regime as per last confirmed rules. Verify this before the current assessment year from incometax.gov.in, as regime rules can change with each Budget.

Principal repayment on a renovation or repair loan does not qualify for Section 80C deduction. Section 80C covers repayment of principal on a loan taken to purchase or construct a house — not for repair or renovation. Do not assume principal repayment on a home improvement loan gives you the same 80C benefit as a home purchase EMI.

Real Example: Rohit and Neha Plan a ₹6 Lakh Renovation

Rohit, 38, is a senior product manager in Pune earning ₹18 lakh per year. He and his wife Neha own a flat. After six years of daily use, the kitchen needs full work — the cabinets are warped, the countertop is cracked, and the tiles have hollow spots. The bathroom has a leaking pipe behind the wall. Waterproofing is overdue on the terrace-facing bedroom. The total contractor estimate: ₹6 lakh.

They explore four options. Their emergency fund is ₹3.5 lakh — enough for about two months of expenses. Using savings would wipe most of it out. Rohit’s existing home-loan EMI is ₹28,000. His take-home salary is approximately ₹1.1 lakh per month.

A personal loan for ₹6 lakh at approximately 13–15% per annum over 4 years would carry an EMI of roughly ₹16,000–₹17,000. Total interest paid: approximately ₹1.6–1.8 lakh. No deduction available under the new regime they are currently in.

A top-up on Rohit’s existing home loan at approximately 9–10% per annum over 5 years would carry a lower EMI — approximately ₹12,000–₹13,000. Total interest: approximately ₹1.3–1.5 lakh. The rates here are illustrative — actual rates will vary based on lender, credit profile, and timing.

They check their debt-to-income position. Their existing home-loan EMI plus the top-up EMI would be approximately ₹40,000–₹41,000 against take-home of ₹1.1 lakh — within a manageable range. They decide to go with a top-up home loan, preserve their emergency fund, and keep all invoices and the lender’s interest certificate for the tax advisor to assess once they revisit their tax regime choice at the next financial year.

The key insight: Rohit treated the tax angle as a secondary check — not the primary reason to borrow.

How to Calculate the True Cost of a Home Improvement Loan

Most borrowers focus on the monthly EMI. The right calculation starts with total repayment.

Total repayment = EMI × Number of months

Total interest paid = Total repayment − Principal borrowed

True loan cost = Total interest + Processing fee + GST on fee + Other charges

Here is a worked example using illustrative figures. These rates are assumed for calculation purposes — actual lender rates vary and must be confirmed from the lender’s sanction letter.

| Scenario | Key Inputs (assumed) | Result (approximate) |

|---|---|---|

| Home improvement loan | ₹5 lakh at 10% per annum, 5 years | EMI ≈ ₹10,624 / Total interest ≈ ₹1.37 lakh |

| Personal loan | ₹5 lakh at 14% per annum, 4 years | EMI ≈ ₹13,672 / Total interest ≈ ₹1.56 lakh |

| Top-up home loan | ₹5 lakh at 9% per annum, 5 years | EMI ≈ ₹10,381 / Total interest ≈ ₹1.23 lakh |

These numbers are illustrative only. Rates change with RBI policy, lender margins, and your credit profile. Add the processing fee (typically 0.5–1% of the loan amount) and GST on the fee to get the true cost. Use our EMI calculator India to run your own numbers before you commit.

Tax benefit should be calculated separately — as a potential annual saving on the interest component — not as a reduction in EMI. If you pay ₹1 lakh in interest in a year and are in the 30% tax slab under the old regime, the deduction saves you approximately ₹30,000 in tax. But you still paid ₹1 lakh in cash first.

Comparison: Home Improvement Loan vs Alternatives

| Option | Best suited for | Key trade-offs |

|---|---|---|

| Home improvement loan | Borrowers without an existing home loan; larger renovation amounts; tax benefit relevant | More documentation; lender may verify end-use; processing takes longer |

| Top-up loan option (top-up home loan) | Existing home-loan borrowers at the same bank; often lower rate and simpler process | Increases home-loan exposure; property remains security; longer tenure risk |

| Personal loan | Urgent work; small amounts under ₹3 lakh; borrowers without property security to offer | Higher interest rate; no tax deduction available; no end-use restriction but higher EMI |

| Savings | Small cosmetic work where emergency fund will not be depleted | No interest cost; weakens liquidity; opportunity cost if savings were invested |

| Credit card / BNPL | Very small purchases like hardware, fittings; short-cycle repayment within 45 days | High risk for large renovation — interest rate 36–42% per annum on revolving balance |

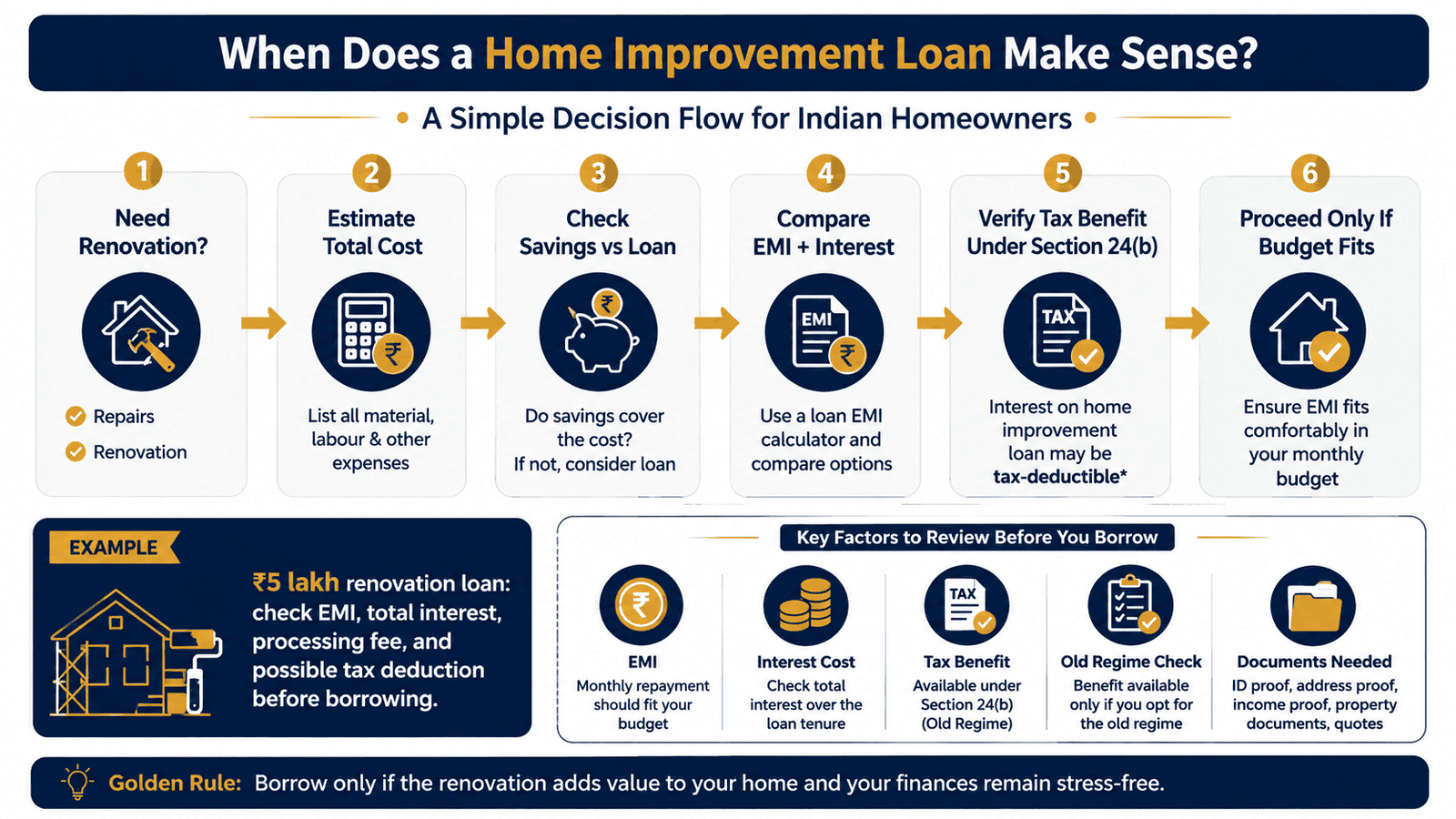

How to Decide What’s Right for You

The renovation is structural, safety-related, or prevents further damage (leaking roof, faulty wiring, water seepage) — THEN borrow if needed. Delaying structural repairs usually costs more later.

You already have a home loan with the same bank and the renovation need is above ₹3 lakh — THEN check a top-up home loan first. The rate is often 1–3% lower than a fresh renovation loan or personal loan.

Your total EMI after adding the renovation loan EMI will exceed 40–45% of take-home pay — THEN reconsider the loan amount, extend tenure cautiously, or phase the renovation. Check safe EMI limit guidelines before applying.

You are on the new tax regime and the only reason you are considering a renovation loan is the tax benefit — THEN the tax argument is weak. Section 24(b) deduction for self-occupied property is not available under the new regime as per last confirmed rules.

The renovation is cosmetic (paint, decorative lights, new curtains) and can be deferred 12 months — THEN use a monthly SIP-style savings plan instead and avoid interest cost entirely.

The property is let out and you are on the old tax regime — THEN a renovation loan for the rental property may carry a stronger tax case, since let-out property has a different and often more favourable interest deduction treatment under Section 24(b). Verify from incometax.gov.in and consult a professional.

You have a clean documentation trail (contractor invoices, lender interest certificate, sanction letter) — THEN do not attempt a Section 24(b) deduction claim. Missing documentation is the most common point of scrutiny in tax assessments involving house property deductions.

Common Mistakes to Avoid

Borrowing Only Because a Tax Benefit Seems Available

Many borrowers take a renovation loan primarily because they hear “it gives tax benefit.” The deduction is subject to regime choice, a low annual ceiling for self-occupied property, and documentation requirements.

If you pay ₹50,000 in interest over a year to save ₹15,000 in tax, you are still net negative by ₹35,000 in cash. Tax benefit is secondary; affordability is primary.

Calculate total interest cost first. Treat any tax saving as a bonus — not the logic for borrowing.

Ignoring Processing Fee, Insurance Bundling, and GST

A lender quotes 9.5% per annum. You sign. The sanction letter shows a 1% processing fee (₹5,000 on a ₹5 lakh loan), plus GST of 18% on the fee (another ₹900), plus a bundled loan insurance premium that adds ₹8,000–₹12,000 to the outgo.

These charges do not appear in the EMI — they reduce the effective amount disbursed or are added upfront. Review the loan processing fee structure carefully before signing.

Ask for the total cost of the loan including all fees before comparing lender offers.

Not Preserving Invoices and Contractor Documents

If you plan to claim a Section 24(b) deduction, the interest certificate from your lender is necessary but not sufficient. Tax assessors may also ask for the purpose of the loan, the renovation estimate, and contractor invoices to confirm the end-use was genuine home improvement.

Digitise every invoice and store them with your tax documents for the relevant financial year.

Assuming Personal Loan Interest Qualifies for Home Loan Tax Treatment

A personal loan taken informally “to fix the house” does not automatically qualify for Section 24(b) deduction. The Income Tax Act requires the loan to be borrowed for the specific purpose of repair, renewal, or reconstruction of house property — and you need documentation to support that purpose.

If you take a personal loan and use it partly for renovation and partly for other expenses, the tax claim becomes difficult to justify cleanly. Keep renovation borrowing separate.

Stretching Tenure Only to Reduce EMI

A ₹5 lakh loan at 10% over 3 years carries an EMI of approximately ₹16,134 and total interest of approximately ₹80,800. The same loan stretched to 7 years drops the EMI to approximately ₹8,306 — but total interest climbs to approximately ₹1.98 lakh.

Match the tenure to the useful life of the renovation — not your desire for the lowest possible EMI. Paying for a kitchen renovation over seven years when the work lasts four makes no financial sense.

Not Checking Foreclosure Rules Before Signing

If you expect a bonus, a salary hike, or a property sale in the next two years, you may want to prepay the loan early. Some lenders charge a foreclosure penalty of 2–4% on the outstanding principal — even on floating-rate loans, though RBI guidelines limit this for individual borrowers on floating-rate home loans.

Check the prepayment and foreclosure clause in the sanction letter before you sign, not after.

When This May Not Be the Right Choice

When the renovation is cosmetic and can wait. If the work is purely visual — a paint refresh, new handles on kitchen cabinets, decorative lighting — and your emergency fund is below three months of expenses, delay the loan. There is no financial urgency in borrowing for aesthetics.

When your existing EMI burden is already high. If your combined EMIs (home loan, car loan, or other) are already at 45% or more of take-home pay, adding a renovation EMI pushes your debt-to-income ratio into a zone where an income disruption — a job change, a medical event — can cause genuine stress.

When your credit score is below 700. A weak credit profile means higher offered rates, tighter terms, and possible rejection. Borrowing at 15–17% for a renovation that a lender with a better rate would have funded at 10% changes the cost-benefit entirely. It may be worth waiting three to six months to repair the score first — unless the renovation is urgent and structural.

When documentation for tax claim is unclear. If the work involves multiple informal contractors, cash payments, and no proper invoices, the tax claim for interest deduction becomes difficult to support. Borrowing partly for the tax angle while having no documentation trail is a poor position.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Tax rules, deduction limits, interest rates, and lender terms change. Do not rely on articles — including this one — for the figures that apply to your current assessment year.

- Income Tax Department — incometax.gov.in: Verify Section 24(b) interest deduction limits, conditions for self-occupied and let-out properties, and regime-specific treatment. Check the applicable assessment year’s provisions, not a prior-year summary.

- RBI — rbi.org.in: For guidance on lender conduct, prepayment rules on floating-rate loans, and borrower rights.

- Your lender’s official domain: Check the current interest rate, processing fee, sanction letter terms, prepayment rules, and insurance requirements directly from the bank or NBFC website before applying.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Get at least two written renovation estimates before applying for the loan. Banks and NBFCs may ask for an estimate as part of documentation. Having one ready also forces you to anchor the loan amount to an actual cost — not a rounded number.

- Improve your credit score before applying if the renovation is not urgent. Moving from a score of 680 to 740–760 can reduce your offered interest rate by 0.5–1.5 percentage points on a secured renovation loan. On ₹6 lakh over five years, that is a saving of ₹15,000–₹25,000 in interest. See our guide on credit score basics to understand what drives your CIBIL score.

- Match tenure to renovation life. A fresh coat of exterior paint lasts 5–7 years. Kitchen cabinetry may last 10–12 years. Avoid funding a 5-year-life renovation on a 7-year loan — you will be paying interest on work that has already faded.

- Maintain a documentary trail if a tax deduction is your plan: before-and-after photos of the work, dated contractor invoices, digital payment receipts, and the lender’s annual interest certificate. Keep these for a minimum of six years from the relevant assessment year.

- If you are an existing home-loan borrower, call your current lender before approaching a new one. Top-up loans at your existing bank may carry zero or low processing fees for loyal borrowers, and the rate is often aligned with your home-loan rate — better than a fresh unsecured renovation loan from a different lender.

- Compare the annual percentage rate (APR) across lenders — not just the headline interest rate. APR incorporates processing fees and charges, giving you a more accurate cost comparison between offers.

- If you are planning to rent out the improved property, the tax treatment of interest changes. Let-out property has a different deduction framework under Section 24(b). Consult a registered tax professional before filing for this scenario.

Frequently Asked Questions

What is a home improvement loan?

A home improvement loan is a loan taken to repair, renovate, renew, or reconstruct an existing residential property you already own. It is not for purchasing a new house or a plot. Lenders may call it a home renovation loan, home repair loan, or offer it as a top-up on an existing home loan. The purpose must be genuine home improvement, and most lenders require documentation such as contractor estimates and invoices to confirm end-use.

Is home improvement loan interest tax deductible in India?

Interest paid on a home improvement loan may qualify for deduction under Section 24(b) of the Income Tax Act, subject to conditions. For a self-occupied property, the deduction limit for repair, renovation, and reconstruction is subject to a ceiling — verify the current limit from incometax.gov.in before filing. This deduction is available under the old tax regime. If you have opted for the new tax regime, this deduction is not available for self-occupied property as per last confirmed rules.

Can I claim principal repayment under Section 80C for a renovation loan?

Generally no. Section 80C allows deduction for principal repayment on a loan taken to purchase or construct a house. Repair and renovation loans do not qualify for the Section 80C principal deduction. Do not assume the same 80C treatment applies — verify with a tax professional for your specific loan purpose and structure.

Is a home improvement loan better than a personal loan for renovation?

Usually yes, on interest rate — because a home improvement loan is typically secured against property, the rate is lower than an unsecured personal loan. However, processing takes longer and documentation requirements are higher. A personal loan may suit you if the amount is small (under ₹2–3 lakh), the need is urgent, or you have no property to offer as security. Calculate total interest cost for both options before deciding.

What documents are needed for a home renovation loan?

Typical documents include: property ownership proof, KYC documents (Aadhaar, PAN), income proof (salary slips, Form 16, ITR), bank statements, a renovation estimate from a contractor, and sometimes photographs of the property. After disbursement, the lender may ask for invoices to verify end-use. Requirements vary by lender — check the specific list from the bank or NBFC before applying.

Can a tenant take a home improvement loan?

Generally no — most lenders require you to be the owner of the property being improved. A tenant does not have ownership rights and cannot mortgage or pledge the property. Some landlords take renovation loans on properties they rent out, which may have different tax treatment under Section 24(b). If you are a tenant and want to fund improvements, a personal loan is the more likely option — but whether you can recover those costs from the landlord is a separate legal matter.

Can I use a home improvement loan for furniture and interior decoration?

This depends on the lender’s policy. Structural renovation — floors, walls, plumbing, electrical — is generally accepted. Loose furniture, home appliances, and pure decoration may or may not be accepted as eligible renovation expense. Even if the lender disburses for such items, they may not support a Section 24(b) tax deduction claim. Clarify with the lender and a tax professional before treating these as deductible.

Does the new tax regime allow Section 24(b) deduction for a home improvement loan?

As per last confirmed rules, the Section 24(b) deduction for self-occupied house property is not available under the new tax regime. If you have opted for the new regime, the interest paid on a home improvement loan for your self-occupied flat may not give you a tax deduction. Verify the current rules from incometax.gov.in for the relevant assessment year, as Budget changes can alter this.

What happens if I miss an EMI on a home improvement loan?

Missing an EMI triggers a late payment penalty (typically 1–2% on the overdue amount) and is reported to credit bureaus, damaging your CIBIL score. On a secured renovation loan, continued default can eventually trigger a recovery action against the property. Do not take a renovation loan unless you are confident the EMI is affordable even if your income temporarily dips.

How is a top-up home loan different from a home improvement loan?

A top-up home loan is an additional amount borrowed on top of your existing home loan with the same lender. It is often available at a rate close to your existing home-loan rate, which is typically lower than a fresh renovation loan from a new lender. The top-up is secured against the same property. If you already have an active home loan, checking a top-up first is almost always worthwhile before applying for a separate product.

Final Verdict

A home improvement loan can be a practical and cost-effective way to fund necessary renovation — when the EMI is affordable, documentation is clean, and the work genuinely improves the usability or structural integrity of your home. It is strongest for borrowers on the old tax regime who are funding eligible repair and renovation work and will maintain proper documentation for the Section 24(b) claim.

It is weakest when the renovation is cosmetic, the documentation trail is thin, your EMI burden is already stretched, or you are on the new tax regime where the deduction benefit disappears. In those cases, saving in advance or choosing a product better suited to your profile makes more sense.

Compare total interest cost — not just EMI — across a top-up home loan, personal loan, and savings before committing. Treat any tax benefit as a secondary check, not the primary reason to borrow. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Neha Kulkarni writes about the financial side of home buying, renting, property decisions, and real estate costs in India. Her content helps readers think beyond the EMI and understand the total cost of owning or buying a home.

She covers topics such as rent vs buy, home loan planning, down payment, stamp duty, registration charges, brokerage, maintenance cost, property tax, furnishing cost, home insurance, builder payment plans, resale property checks, home loan affordability, total cost of ownership, and hidden costs in property decisions.

Neha’s writing is practical, family-focused, and cost-conscious. She uses Indian city examples, ₹ calculations, and decision checklists to help readers evaluate whether a property decision fits their income, savings, loan eligibility, and long-term plans. Her articles are useful for first-time home buyers, salaried couples, families, and people comparing rent with home ownership. Since property rules, stamp duty, registration charges, local taxes, home loan rates, and legal requirements vary by state and city, readers should verify current details from official state, lender, and legal sources.