You have just received ₹1.2 lakh from a US startup for a project you completed last month. The money cleared your bank account, the client is happy — and then you wonder: does India even know about this? Do you owe tax? What about GST? Most Indian freelancers earning from foreign clients face this exact situation. The confusion is understandable. The client is abroad, the payment came in dollars, and nobody deducted TDS. None of that, however, changes the basic rule: foreign income tax in India applies to resident freelancers on their global earnings. This article walks you through the full picture — income tax, GST, 44ADA, DTAA, and ITR reporting — in plain freelancer language.

Quick Answer: Foreign Income Tax in India for Freelancers

Foreign income tax in India applies to resident freelancers on overseas client earnings, generally after converting foreign receipts into ₹ and reporting them in ITR. If tax payable after TDS exceeds ₹10,000, advance tax may apply. GST, DTAA, 44ADA eligibility, and foreign tax credit need separate checks.

Key Takeaways

- If you are a resident Indian for tax purposes, income from overseas clients is part of your global income and is taxable in India — the client’s country does not change this.

- Foreign freelance receipts must generally be converted into ₹ (at the rate on the date of credit or an accepted accounting basis) before calculating taxable income.

- Section 44ADA presumptive taxation at 50% of gross receipts may apply if you are a specified professional and your gross receipts are within the applicable threshold — verify current limits before filing.

- GST does not disappear just because the client is outside India; export-of-services rules under the IGST Act require LUT filing or documentation — check thresholds and eligibility at gst.gov.in.

- If the foreign client or country has withheld tax abroad, you may be able to claim a foreign tax credit under DTAA using Form 67 — this is a separate process from your ITR.

- Maintain your invoice, contract, bank remittance advice, and FIRC/FIRA as evidence; these are your primary documents if your income is queried.

- Advance tax instalments may apply if your estimated tax liability exceeds ₹10,000 for the year — missing instalments attracts interest under Section 234B and 234C.

Key Facts at a Glance

| Area | What Applies | Where to Verify |

|---|---|---|

| Who must report | Resident Indians with foreign freelance/professional income | incometax.gov.in |

| Income currency | Convert foreign receipts into ₹ at applicable rate before reporting | Bank statement / RBI reference rate |

| Advance tax threshold | ₹10,000 estimated tax payable triggers advance tax obligation | incometax.gov.in — verify current limit |

| GST on overseas services | May qualify as export of services — LUT required for zero-rated supply | gst.gov.in — verify current thresholds |

| ITR form | Generally ITR-3 (business income) or ITR-4 (if using 44ADA presumptive) | incometax.gov.in — confirm applicable form each year |

| Documents to keep | Invoice, contract, bank advice, FIRC/FIRA, foreign tax certificate | Maintain for at least 6 years |

| DTAA / foreign tax credit | Claim via Form 67 if tax withheld abroad; submit before ITR deadline | incometax.gov.in — verify Form 67 process |

How Foreign Income Tax in India Actually Works for Freelancers

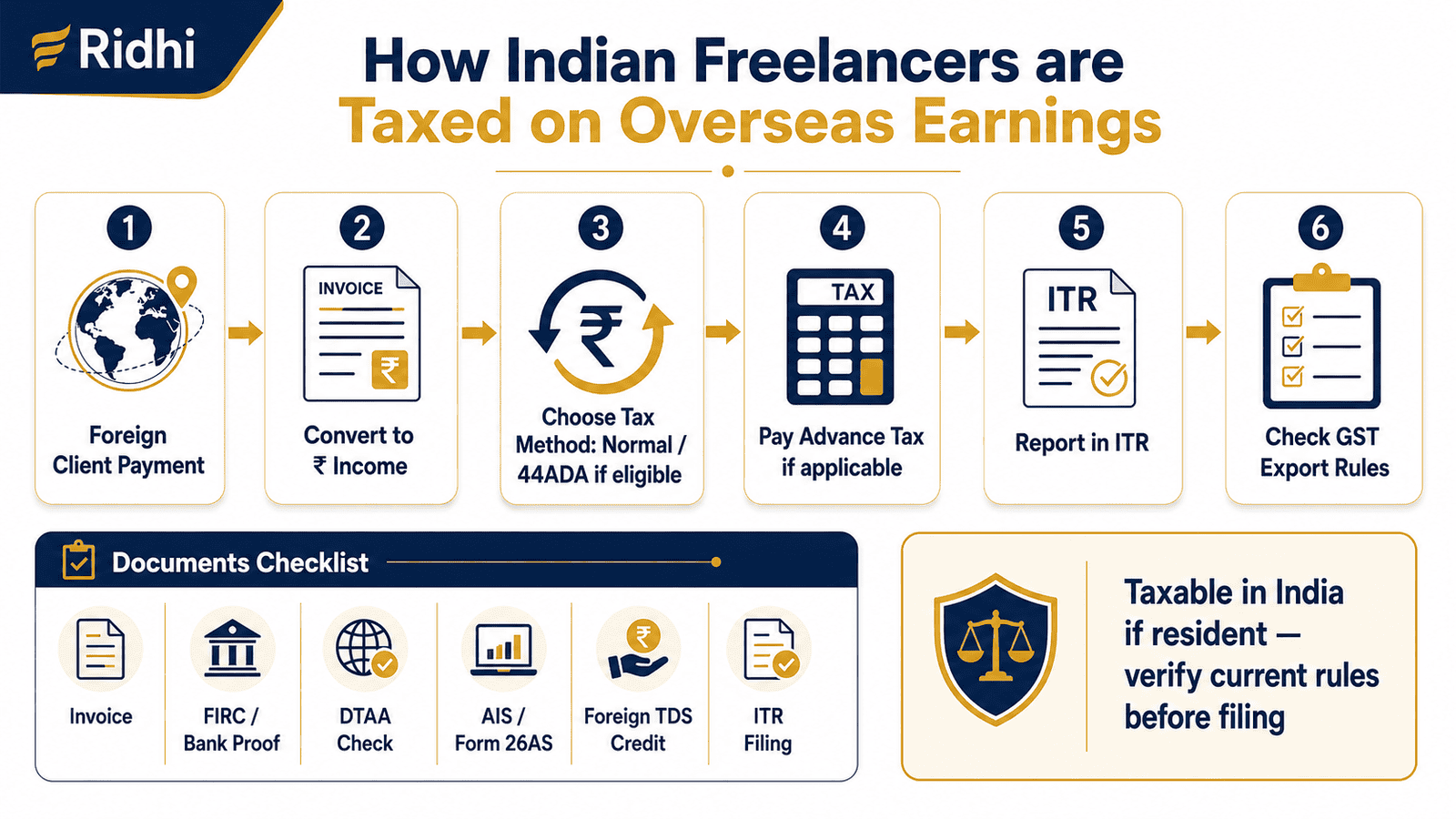

The single most important concept here is residential status. Under the Income Tax Act, 1961, if you are classified as a Resident and Ordinarily Resident (ROR) in India, your global income is taxable in India — regardless of where the client is located, which currency they paid in, or whether any tax was withheld abroad.

Most freelancers who live and work in India throughout the year are ROR. Non-resident (NR) or Resident but Not Ordinarily Resident (RNOR) status applies in specific circumstances — for example, if you have spent significant time abroad or recently returned. If you are unsure of your residential status, confirm it at incometax.gov.in before filing.

Foreign Client ≠ Tax-Free Income

This is the most common misconception. If a US company pays you $2,000 for a software module, that $2,000 (converted into ₹ at the applicable exchange rate on the date of receipt or credit) is your professional receipt for that period. It is treated identically to receiving ₹1,66,000 from a domestic client. The client’s address does not create a tax exemption.

For a fuller introduction to how Indian freelancers are taxed in general, read our guide on freelancer tax basics before going further.

Calculating Taxable Income from Foreign Receipts

Once you have your total ₹-equivalent receipts for the year, you have two methods to arrive at taxable income:

- Normal / actual expenses method: Gross receipts minus legitimate business expenses (internet, equipment, software, professional fees, etc.) equals net profit — which is your taxable income.

- Presumptive method under Section 44ADA: If you are a specified professional (software development, legal, medical, engineering, accountancy, architecture, and certain others) and your gross receipts are within the applicable threshold, you may declare 50% of gross receipts as taxable income without separately proving each expense. Confirm your profession is listed and verify the current gross receipts ceiling from incometax.gov.in before using this route.

Income Tax vs GST — Two Separate Questions

Income tax and GST are completely independent. Income tax on your net profit goes to the Central Government via the ITR. GST is a transaction-level tax on supply of services. Overseas freelance income may qualify as export of services under the IGST Act if it meets the conditions: the supplier is in India, the recipient is outside India, the place of supply is outside India, and payment is received in convertible foreign exchange.

If your service qualifies as an export, it is zero-rated — meaning no GST is charged to the client. But you still need to either file a Letter of Undertaking (LUT) on the GST portal before raising your export invoice, or charge IGST and later claim a refund. Most freelancers use the LUT route. GST registration itself is only mandatory beyond a certain annual turnover threshold — verify the current limit at gst.gov.in.

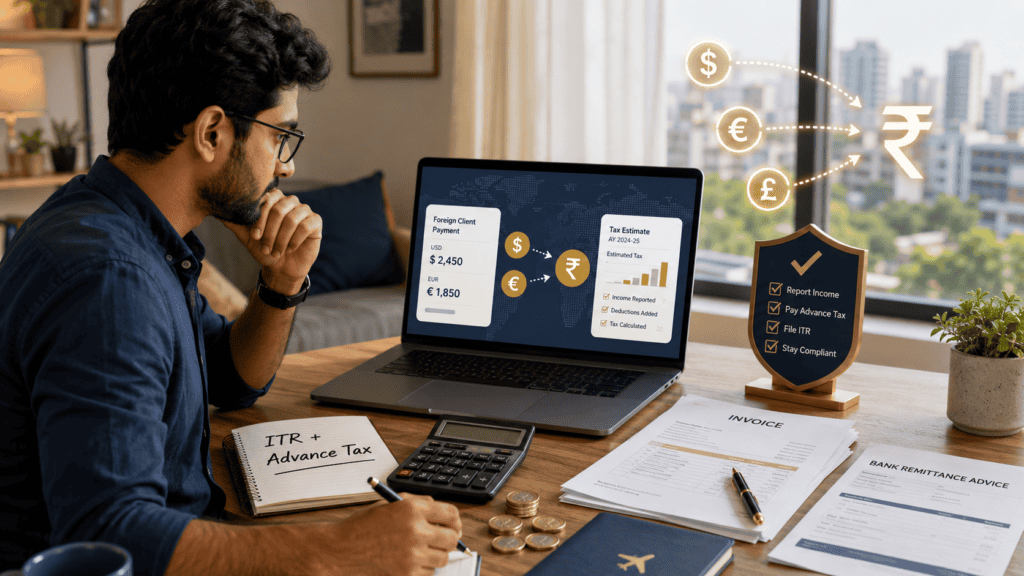

Real Example: Rohan’s Overseas Freelance Receipts

Rohan, 29, is a freelance software developer based in Bengaluru. In FY 2024–25, he received payments from two US clients — $8,000 from a startup and $6,000 from an agency — totalling $14,000. His bank credited the equivalent of approximately ₹11.6 lakh across the year after conversion at the prevailing bank rates.

Rohan’s first step is confirming that all ₹ credits match his invoices and bank statements. He checks his AIS on the income tax portal to see if any income has been auto-populated. Since his US clients did not deduct Indian TDS (they are foreign entities with no Indian TDS obligation in most cases), no TDS appears — but his income is fully reportable.

He then checks whether he qualifies for Section 44ADA. Software development is a listed profession. He verifies that his gross receipts are within the applicable ceiling. If eligible, he can declare 50% of ₹11.6 lakh — approximately ₹5.8 lakh — as taxable income. He then applies the applicable tax regime slabs to estimate his liability. Because his estimated annual tax exceeds ₹10,000, he must also check advance tax instalment dates. Separately, he checks whether he has crossed the GST registration threshold and whether he has filed an LUT for his export invoices.

The key insight: Rohan’s compliance checklist is the same whether his client is in Bengaluru or Boston — it just adds a currency conversion step and a few export-of-services checks.

How to Calculate Tax on Overseas Freelance Income

Taxable Income (Normal Method) = Gross Foreign Receipts in ₹ − Allowable Business Expenses

Taxable Income (44ADA Presumptive) = 50% × Gross Foreign Receipts in ₹ (if eligible)

Using Rohan’s figures from the example above (₹11.6 lakh gross receipts, 44ADA method):

| Scenario | Key Inputs | Estimated Taxable Income |

|---|---|---|

| Presumptive (44ADA) | ₹11.6L gross × 50% | ≈ ₹5.8 lakh — verify eligibility and current threshold |

| Normal method — low expenses | ₹11.6L gross − ₹1.5L expenses | ≈ ₹10.1 lakh |

| Normal method — high expenses | ₹11.6L gross − ₹4L expenses | ≈ ₹7.6 lakh |

Apply current income tax slabs (new or old regime) to your taxable income to estimate tax payable. If the result exceeds ₹10,000 for the year, advance tax instalments apply. For a step-by-step guide on choosing between 44ADA and normal method, see our article on the presumptive tax option.

Note: actual tax depends on your regime choice, eligible deductions, other income sources, and whether any foreign tax credit applies. The figures above are illustrative only.

Comparison: Income Tax vs GST vs DTAA on Overseas Freelance Income

| Area | What It Covers | Key Action for Freelancers |

|---|---|---|

| Income Tax | Tax on net profit from global income for resident Indians | Report in ITR-3 or ITR-4; pay advance tax if liability exceeds ₹10,000 |

| GST — Export of Services | Supply of services to foreign clients where payment is in foreign exchange | File LUT for zero-rated supply; check registration threshold at gst.gov.in — Verify threshold |

| DTAA / Foreign Tax Credit | Relief if source country withheld tax on your income | File Form 67 before ITR due date; claim credit against Indian tax — Form 67 required |

| Section 44ADA | Presumptive tax at 50% for eligible professionals within gross receipts ceiling | Confirm profession is listed and gross receipts are within limit — Verify limit |

| ITR Reporting | Disclosure of foreign income, assets, FIRC details in the correct schedule | Use Schedule FSI and Schedule TR if applicable; match with AIS and Form 26AS — Do not skip |

For a detailed look at when GST registration becomes mandatory for freelancers, read our guide on GST registration rules.

How to Decide What’s Right for You

You are a Resident and Ordinarily Resident in India — THEN your foreign freelance income is part of your global income and must be reported in your Indian ITR, regardless of whether any foreign tax was deducted.

You are a specified professional (software developer, lawyer, architect, etc.) and your gross receipts are within the 44ADA ceiling — THEN check whether the presumptive method at 50% results in lower taxable income than the normal method, and verify current limits before choosing.

The foreign country withheld tax on your payment (common with some US, UK, or EU clients who operate under their domestic rules) — THEN file Form 67 before your ITR due date to claim a foreign tax credit under the relevant DTAA, so you do not pay tax twice on the same income.

Your annual service turnover crosses the GST registration threshold — THEN register on gst.gov.in, file an LUT each financial year, and raise export-of-services invoices to foreign clients without charging IGST.

Your estimated tax liability for the year is likely to exceed ₹10,000 — THEN plan and pay advance tax in quarterly instalments to avoid interest under Section 234B and 234C. See our guide on advance tax payments for exact dates and calculation.

You have income from multiple foreign countries with differing tax treaties — THEN consult a chartered accountant before filing; the DTAA provisions, Form 67 requirements, and Schedule FSI disclosures can interact in ways that are easy to get wrong.

You are not sure of your residential status, do not have proper FIRC/FIRA documentation, or receive income through platforms that report inconsistently — do not self-file foreign income without professional review; an incorrect disclosure is harder to correct than a late one.

Common Mistakes to Avoid

Assuming Foreign Client Income Is Tax-Free

Many freelancers believe that because the client is abroad or payment came in USD, the Indian tax department has no visibility. This is incorrect.

Banks report foreign remittances through the banking system, and the Income Tax Department receives data through AIS and other reporting channels. Unreported foreign income can trigger scrutiny and attract penalties under Section 270A, which can be up to 200% of the tax evaded in cases of misreporting.

Report all foreign professional receipts in your ITR every year, even if the amount seems small.

Not Maintaining Invoice and Remittance Documentation

Many freelancers rely on PayPal, Wise, or Stripe statements but do not keep the original invoice or contract that matches the payment.

During an income tax inquiry, you need to show that the credited amount corresponds to a specific professional service. Without matching invoices, bank credits can be treated as unexplained income. Save your FIRC (Foreign Inward Remittance Certificate) or FIRA (Foreign Inward Remittance Advice) for every payment.

Maintain a simple folder — one invoice, one bank advice, one contract reference — for each foreign payment.

Skipping GST / Export-of-Services Documentation

Even if you do not charge GST to your foreign client, you still need to handle the GST paperwork if you are registered.

Not filing an LUT before raising export invoices means your supply is not treated as zero-rated, and you may be liable for IGST on the full invoice value. This is a recoverable error but involves refund applications and delays.

File your LUT on the GST portal at the beginning of each financial year if you regularly receive foreign payments. Learn more about documentation in our guide on freelance invoice format.

Assuming Section 44ADA Applies Automatically

Not every freelancer qualifies for the presumptive scheme. Your profession must be in the specified list under Section 44ADA, and your gross receipts must be within the applicable annual ceiling.

Using 44ADA when you are ineligible — for example, if your profession is not listed or you exceed the gross receipts limit — can result in a defective return notice or reassessment. Verify your eligibility each year before opting in.

If you are unsure, use the normal method and maintain proper expense records.

Forgetting to File Form 67 for Foreign Tax Credit

If any country has withheld tax on your freelance income, you are entitled to claim that as a credit against your Indian tax under the applicable DTAA.

But the credit is not automatic. You must file Form 67 on the income tax portal before your ITR due date. Missing this deadline means losing the credit entirely for that year — which can result in double taxation on the same income.

Check your payment receipts, wire transfer memos, and client tax forms to identify any foreign tax withheld.

Ignoring Schedule FSI and Schedule TR in ITR

ITR-3 contains specific schedules for foreign source income (Schedule FSI) and taxes paid outside India (Schedule TR). Many freelancers fill in their income but leave these schedules blank.

Incomplete disclosure of foreign income is treated as a filing error and can trigger a defective return notice. Fill these schedules correctly for every foreign receipt, with the currency, country, and income amount.

Waiting Until March to Estimate Tax

Freelancers with irregular monthly income from overseas often underestimate their annual receipts until the last quarter. By then, advance tax deadlines for the first three instalments have already passed.

Interest under Section 234C applies for each missed instalment — even if you pay the full amount in March. A rough mid-year estimate in September or October can save you ₹2,000–₹8,000 in interest depending on your income.

Use the September instalment deadline as a checkpoint to reconcile foreign receipts and revise your advance tax estimate.

When This May Not Be the Right Choice

Self-filing may not be appropriate if your residential status is RNOR or non-resident — these categories have different global income rules and require careful analysis before filing.

If you are managing a team of subcontractors or have employees, your tax treatment may shift from professional income to business income, changing your ITR form, expense deduction rules, and 44ADA eligibility.

Freelancers earning from clients in multiple countries where tax has been withheld face a more complex scenario — each country’s DTAA with India has different rates, credit rules, and documentation requirements that are difficult to self-navigate.

If your income comes from global platforms (Upwork, Fiverr, Toptal) and the platform reports income differently from your actual receipts, reconciling AIS, Form 26AS, and bank credits requires professional review to avoid mismatch notices.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Before filing your return, verify the following directly from official sources. Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- Income Tax Department — incometax.gov.in: Current tax slabs, advance tax thresholds, 44ADA gross receipts limit, applicable ITR forms, Form 67 process, Schedule FSI and Schedule TR instructions, and AIS/Form 26AS reconciliation.

- CBIC / GST Portal — gst.gov.in: GST registration turnover threshold, LUT filing process, export-of-services conditions under the IGST Act, and place-of-supply rules for overseas clients.

- RBI — rbi.org.in: FIRC and FIRA documentation standards, permissible payment modes for export of services, and reference exchange rates where applicable.

For step-by-step instructions on filing your return as a freelancer, see our guide on freelancer ITR filing.

Expert Tips

- Open a dedicated savings or current account for all foreign client payments. This makes bank reconciliation, FIRC collection, and GST compliance documentation significantly faster — and reduces the chance of mixing personal and professional credits that can confuse AIS matching.

- Save every FIRC or FIRA the day it is issued by your bank. Many banks issue these documents only within a limited window after credit. Once the remittance record ages, retrieval becomes difficult and may require a formal request.

- Reconcile your income with AIS and Form 26AS by October every year — not in March. Foreign remittances are often reported by banks under separate codes; catching mismatches early gives you time to correct them before the ITR filing window closes.

- If you are in the 20% or 30% tax bracket and your gross receipts are within the 44ADA limit, compare both methods before opting in: presumptive income at 50% may be lower than actual net profit, but only if your documented expenses are well below 50% of receipts.

- File your LUT for GST export-of-services at the very start of every financial year (April 1). Do not wait until you raise your first invoice. A missing LUT at invoice date is the most avoidable compliance gap for freelancers with foreign clients.

- Check whether your client’s country has a DTAA with India before the year-end. If they have withheld any tax, contact them for a tax withholding certificate — this document is required to support your Form 67 claim at incometax.gov.in.

- Do not assume PayPal, Wise, Stripe, or Payoneer income is invisible. The RBI and the income tax system receive remittance-related data through banking channels. Report every credit as professional income, regardless of the platform used.

Frequently Asked Questions

Is foreign freelance income taxable in India?

Yes, if you are a Resident and Ordinarily Resident (ROR) in India. Indian tax law taxes your global income — meaning income from overseas clients is fully taxable in India, just like domestic client income. The client’s country does not create an exemption. Non-residents or RNORs have different rules; confirm your residential status from the Income Tax Act or consult a CA.

Can I use Section 44ADA for income from foreign clients?

You may be eligible if your profession is in the specified list under Section 44ADA and your total gross receipts (including foreign income) are within the applicable annual ceiling. Eligibility does not depend on whether the client is Indian or foreign — it depends on your profession and turnover. Verify the current gross receipts limit at incometax.gov.in before opting in.

Do I need GST registration if my clients are all outside India?

GST registration is based on your total annual turnover, not your clients’ location. If your turnover crosses the registration threshold (verify current limits at gst.gov.in), you must register regardless of where your clients are. Once registered, overseas service income typically qualifies as export of services — file an LUT to supply it as a zero-rated service without charging IGST.

What if the foreign client or their country withheld tax on my payment?

You may be able to claim credit for that foreign tax against your Indian tax liability under the Double Taxation Avoidance Agreement (DTAA) between India and that country. File Form 67 on the income tax portal before your ITR due date, along with a tax withholding certificate from the foreign client or their tax authority. Verify the current process and deadline at incometax.gov.in.

Which ITR form should a freelancer use to report foreign income?

Generally ITR-3 if you are reporting business or professional income under the normal method, or ITR-4 if using the presumptive scheme under Section 44ADA. ITR-4 has certain restrictions on foreign asset and income schedules — if you have foreign assets or significant foreign income, ITR-3 may be required. Confirm the applicable form for the relevant assessment year at incometax.gov.in.

Should I report income received via PayPal, Wise, Stripe, or Payoneer?

Yes. All professional receipts — regardless of the platform — constitute income and must be reported in your ITR. These platforms transfer money that originates as payment for your services. The mode of receipt does not change the tax character of the income. Report the ₹-equivalent amount credited to your bank account.

What is a FIRC and why does it matter for foreign freelance income?

A FIRC (Foreign Inward Remittance Certificate) or FIRA (Foreign Inward Remittance Advice) is a document issued by your bank confirming that a specific foreign remittance was received. It serves as proof that your income was earned in convertible foreign exchange — which is one of the conditions for treating it as export of services under GST. It also helps match your income with invoices during any tax inquiry. Collect it for every foreign payment.

Can I claim business expenses against foreign freelance income?

Yes, under the normal method. Expenses directly related to earning that income — internet costs, software subscriptions, equipment depreciation, professional fees — are generally deductible. Under Section 44ADA, you declare 50% of gross receipts as income and cannot separately claim further expenses. Choose the method that applies to your actual expense level after verifying eligibility each year.

What happens if I forget to declare foreign income in my ITR?

Foreign income omitted from an ITR can be treated as concealment of income. The tax department may issue a notice, and penalties under Section 270A can range from 50% to 200% of the tax payable on the undisclosed amount, depending on whether it is treated as under-reporting or misreporting. File a revised return before the deadline if you missed any foreign income in an earlier filing.

Is advance tax mandatory for freelancers with foreign client income?

If your estimated tax liability for the year exceeds ₹10,000 after accounting for any TDS, advance tax instalments are mandatory. Freelancers earning from foreign clients typically have no TDS deducted, which means advance tax planning is especially important. Missing instalments attracts interest under Sections 234B and 234C. Verify current instalment dates and thresholds at incometax.gov.in.

Final Verdict

Foreign income tax in India is not a separate or special tax — it is the same income tax framework applied to your global earnings as a resident freelancer. The fact that your client is in the US, UK, or Singapore does not reduce your Indian tax liability. What changes is the paperwork: you need to convert receipts into ₹, maintain FIRC/FIRA documentation, check 44ADA eligibility against verified limits, handle GST export-of-services rules separately, and file Form 67 if any foreign tax was withheld. Freelancers who stay ahead of advance tax deadlines, reconcile AIS early, and file a correct ITR with foreign income schedules will have very little to worry about. Those who ignore overseas income or leave it out of their return face a much harder conversation later. Use the official portals — incometax.gov.in and gst.gov.in — as your primary sources, and work with a CA for DTAA and multi-country situations. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Amit Verma writes about money management for Indian freelancers, consultants, creators, professionals, and self-employed workers. His content focuses on income planning, tax basics, GST awareness, cash flow, invoicing, business expenses, and financial stability for people who do not receive a fixed monthly salary.

He covers topics such as Section 44ADA, presumptive taxation, professional income, advance tax, GST basics, TDS for freelancers, invoice planning, business expense tracking, ITR filing for self-employed professionals, emergency funds, health insurance, retirement planning, and irregular income management.

Amit’s writing is practical, relatable, and built around the realities of independent work. He understands that freelancers often deal with delayed payments, uneven income, unclear tax deductions, missing employer benefits, and uncertainty around compliance. His guides help readers organise their financial life better, but they are educational and not a substitute for professional advice. Since tax rules, GST limits, filing requirements, and deduction treatment can change, readers should verify current rules from official sources or consult a qualified professional.