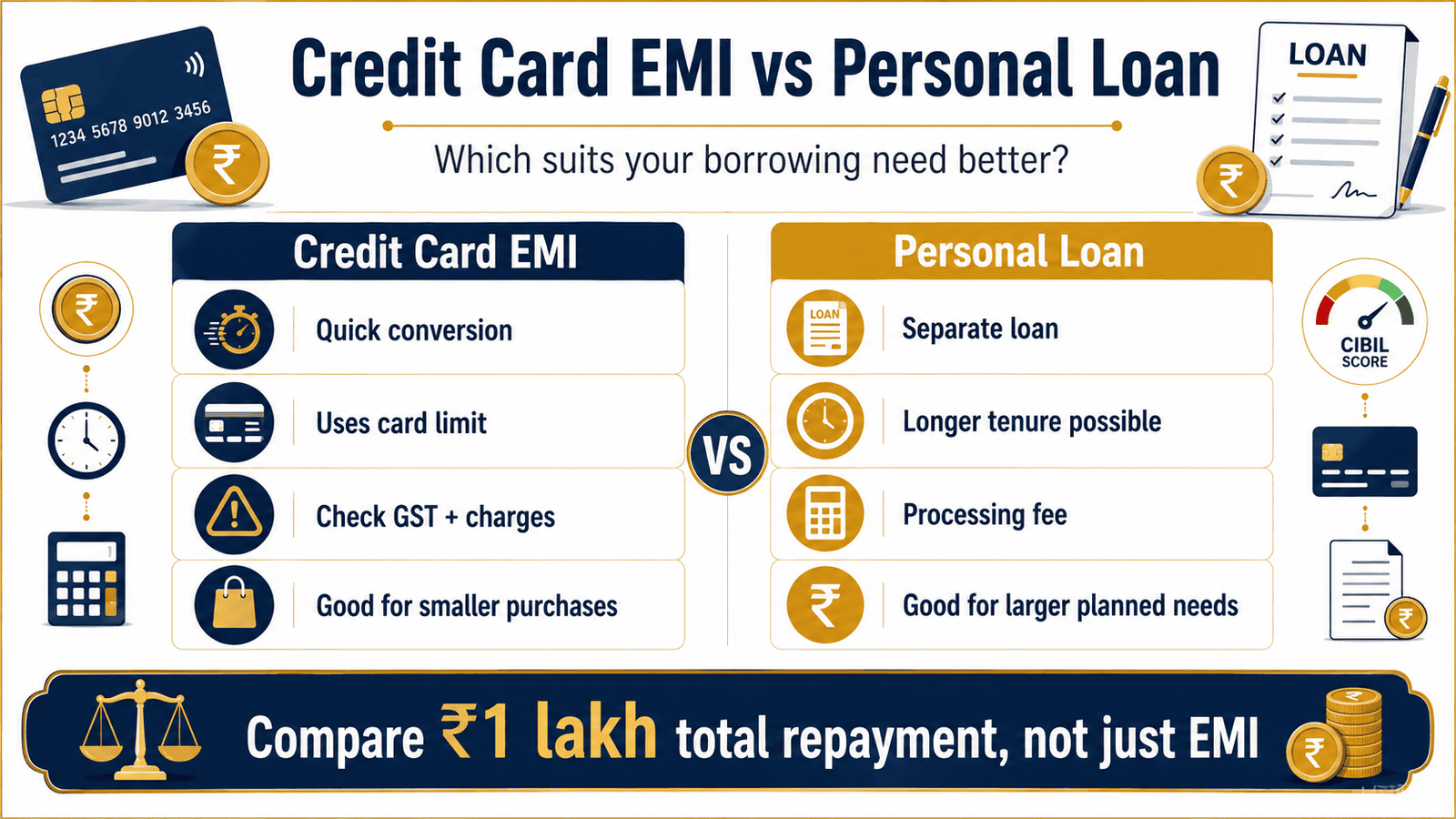

You found a ₹1 lakh expense — a washing machine, a medical bill, a last-minute trip — and two borrowing options appeared almost simultaneously. Your credit card app offered to convert it to EMI in one tap. Your bank sent an instant personal loan offer at what looks like a lower rate. The credit card EMI vs personal loan decision comes down to more than which screen you tap first.

Indians reach for both options for appliances, repairs, medical costs, travel bookings, and short-term cash shortfalls. The confusion is real: the monthly EMI amounts can look similar, but the total repayment can differ by ₹5,000 to ₹15,000 on a ₹1 lakh borrowing — depending on interest rate, tenure, processing fee, GST, and foreclosure terms.

This article compares credit card EMI and personal loans on total cost, CIBIL impact, credit utilisation, tenure flexibility, and repayment discipline — so you can make an informed comparison before choosing. This is not personalised borrowing advice.

Quick Answer: Credit Card EMI vs Personal Loan

Credit card EMI vs personal loan depends on total cost, tenure, processing fees and flexibility. For a ₹1 lakh purchase, compare the card EMI interest, GST and foreclosure terms with a personal loan EMI before choosing. The cheaper option is usually the one with lower total interest plus charges, not lower monthly EMI alone.

Key Takeaways

- Credit card EMI is convenient for smaller purchases already eligible on your card — no separate application, instant conversion — but it blocks a portion of your credit limit until the balance clears.

- A personal loan may offer a lower interest rate for larger borrowing needs, but adds a processing fee, 18% GST on that fee, and a hard enquiry on your credit report at the time of application.

- No-cost EMI is not always free — some schemes carry a flat processing fee, 18% GST on that fee, or require you to forgo a cashback or discount that would have applied on a full payment.

- Missing even one EMI payment on either product is reported to credit bureaus and can damage your CIBIL score.

- A lower monthly EMI does not mean a lower total cost — a ₹1 lakh loan at 15% p.a. for 24 months costs significantly more overall than the same loan at 12% p.a. for 12 months, even though the EMI is smaller.

- If your existing EMIs already exceed 40–50% of take-home salary, adding either obligation increases your financial risk meaningfully.

Comparison: Credit Card EMI vs Personal Loan

| Parameter | Credit Card EMI | Personal Loan |

|---|---|---|

| Interest rate | Varies by card issuer, card type, and borrower profile. As of recent data, card EMI rates tend to be higher than personal loan rates for eligible borrowers — verify current MITC document. | Varies by lender, borrower credit score, and salary. Eligible borrowers with strong profiles may qualify for rates lower than typical card EMI rates — verify sanction letter. |

| Processing fee | Nil on some offers; flat fee on others. 18% GST applies on any fee charged. | Typically 0.5%–3% of loan amount. 18% GST applies. Confirm with lender’s schedule of charges. |

| Tenure | Typically 3–24 months. Limited flexibility beyond the issuer’s standard options. | Typically 12–60 months. Wider tenure choice available at the time of sanction. |

| Impact on credit limit | Reduces available card limit by the full outstanding EMI amount until balance is repaid. | No impact on card limit. Reported as a separate loan account in the credit bureau file. |

| Prepayment / foreclosure | Prepayment may not be permitted on some card EMI schemes. Foreclosure charges may apply if allowed. | Usually permitted; prepayment or foreclosure charges apply as per lender policy. Confirm before signing. |

| Best fit | Short-tenure, card-eligible purchase where the offer is transparent and the card limit remains healthy after conversion. | Larger planned expense, longer repayment need, or when cash disbursal (not just purchase conversion) is required. |

Key Facts at a Glance

| Fact | What You Should Know |

|---|---|

| Card EMI blocks your credit limit | Converting a ₹1 lakh purchase to EMI reduces your available credit limit by ₹1 lakh until the outstanding balance reduces with each payment. This can affect other purchases on the same card. |

| Personal loan is a separate credit account | A personal loan does not touch your card limit, but it shows as a new loan liability in your credit bureau file and can affect your credit utilisation and debt-to-income ratio. |

| GST applies on charges for both | 18% GST is levied on processing fees, prepayment charges, and other service charges for both credit card EMI and personal loans. This increases the effective cost beyond what the interest rate alone suggests. |

| Revolving card debt is expensive | Any credit card balance not converted to EMI and not paid in full attracts revolving interest — often significantly higher than EMI interest rates. Verify the current rate in your card’s Most Important Terms and Conditions (MITC). For more on how card interest works, read Know card interest. |

| Rates and features can change without notice | Interest rates, processing fees, and EMI terms offered by banks and NBFCs can change at any time. Always verify the current applicable terms from the official source before accepting any offer. |

How Credit Card EMI and Personal Loans Actually Work

What Credit Card EMI Means

When you make a purchase on your credit card and convert it to EMI, you are agreeing to repay the purchase amount in equal monthly instalments over a fixed tenure. The card issuer charges interest on the outstanding principal for each month of the tenure. This interest is added to your card statement as part of the EMI, and each payment reduces the outstanding balance.

The conversion happens within the card’s existing credit limit. If you have a ₹2 lakh limit and convert a ₹1 lakh purchase to EMI, your available limit drops to roughly ₹1 lakh until the EMI balance reduces. This matters for credit utilisation — the ratio of your outstanding balance to your total credit limit. A high utilisation ratio, even from EMI, can affect your CIBIL score.

No-Cost EMI, Merchant EMI, and Regular Card EMI — These Are Not the Same

Regular card EMI charges you interest at the rate set by your card issuer. The rate varies by card, tenure, and issuer policy. Merchant EMI (also called no-cost EMI) appears to have zero interest — but the merchant may pay the interest cost as a subvention to the bank, and in some cases the merchant recoups this by removing an upfront discount you would have received on a full cash or card payment. So the effective cost may not be zero.

Some no-cost EMI schemes also carry a flat processing fee — typically a few hundred rupees — plus 18% GST on that fee. Always check the exact terms before converting, rather than assuming zero cost because the label says “no-cost.”

Some banks also offer a credit card loan — a cash disbursement to your bank account against your card limit. This is separate from a card purchase EMI and typically carries its own interest rate and fee structure.

What a Personal Loan Actually Is

A personal loan is a separate, unsecured credit facility sanctioned by a bank or NBFC. You apply, the lender evaluates your salary, credit score, existing obligations, and employer profile, and if approved, disburses cash to your bank account. You repay it in fixed monthly instalments over a fixed tenure. The interest is calculated on a reducing balance basis — each EMI pays some principal and some interest, and the interest component reduces as the outstanding principal reduces.

A personal loan is not linked to your credit card limit. It is a separate credit account that appears in your credit bureau report as a loan liability. This means it contributes to your debt-to-income ratio and can affect future loan eligibility. According to RBI guidelines, all scheduled commercial banks and NBFCs must report loan accounts to credit information companies. So both hard enquiries at the time of application and repayment behaviour are visible to future lenders.

How Approval Differs

Credit card EMI is typically pre-approved — your issuer decides your eligibility based on your existing card usage and repayment history. There is no fresh credit enquiry in many cases, though some issuers do check. Personal loan approval involves a formal credit assessment. The lender pulls your credit report — a hard enquiry — which may reduce your CIBIL score by a small amount in the short term. Multiple applications in a short period can signal credit-hungry behaviour to future lenders.

For borrowers with a CIBIL score below 700, personal loan approval may be declined or the offered rate may be significantly higher. In that scenario, card EMI (if available) may be the accessible option, though it comes with its own cost structure. To understand why repayment behaviour and loan enquiries affect your credit profile, read Check credit score basics.

Why Tenure Choice Matters More Than Most Borrowers Realise

Both options allow some range of tenure choice. The temptation is to pick the longest available tenure to minimise the monthly EMI. This is one of the most expensive decisions a borrower makes. Extending tenure from 12 to 24 months on a ₹1 lakh loan at 12% p.a. can add over ₹6,000 in additional interest — for a lower monthly payment that lasts twice as long. The calculation section below shows this with actual numbers.

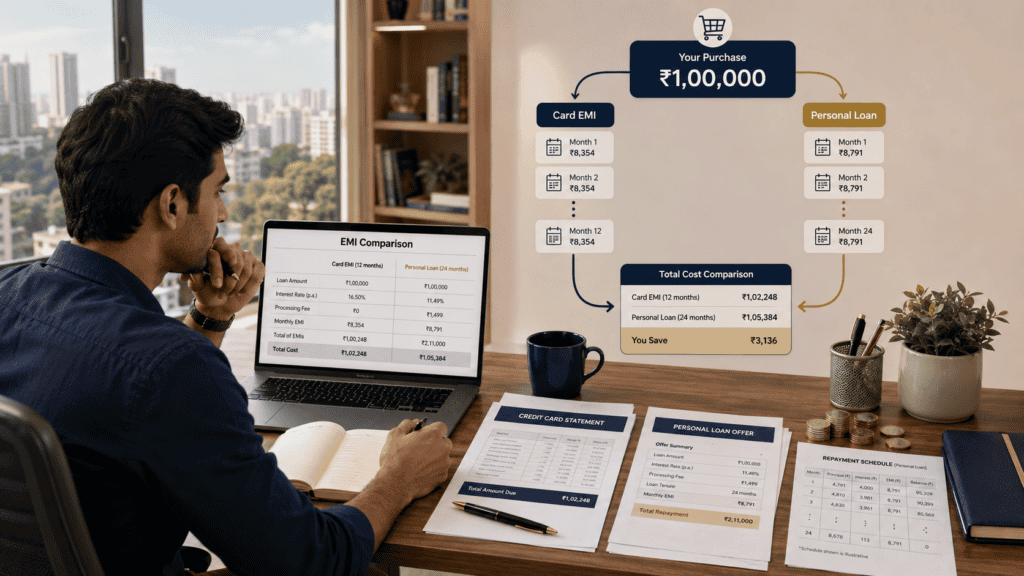

Real Example: Rohan’s ₹1 Lakh Decision in Pune

Rohan, 31, a salaried software engineer in Pune earning ₹85,000 per month, wants to buy a ₹1 lakh washing machine. His credit card app is offering to convert it to a 12-month EMI at a sample illustrative rate of 15% per annum. His bank is simultaneously offering a personal loan at a sample illustrative rate of 12% per annum for 12 months, with a 1% processing fee.

Using these illustrative figures:

Credit card EMI at 15% p.a., 12 months: Monthly EMI works out to approximately ₹9,026. Total repayment over 12 months: approximately ₹1,08,312. The card issuer is also charging a flat ₹499 processing fee plus 18% GST (₹90), adding ₹589 to the cost. Illustrative total cost: approximately ₹1,08,901.

Personal loan at 12% p.a., 12 months: Monthly EMI works out to approximately ₹8,885. Total repayment: approximately ₹1,06,620. The processing fee of 1% (₹1,000) plus 18% GST (₹180) adds ₹1,180. Illustrative total cost: approximately ₹1,07,800.

Despite the higher processing fee, the personal loan costs Rohan about ₹1,101 less overall — because the lower rate saves more than the fee erases. The key insight: the cheaper option is the one with lower total cost, not lower monthly EMI. Verify current lender rates and fees using the Use EMI calculator before finalising any offer.

How to Calculate Which Option Is Cheaper

Total Cost = Principal + Total Interest + Processing Fee + (GST on Processing Fee) + Foreclosure or Prepayment Charges (if applicable)

Use this formula for both options, using the same principal and the same tenure, before comparing. Most lender EMI calculators show the monthly EMI and total repayment — but they may not automatically include the processing fee or GST on that fee. Add these manually.

For Rohan’s ₹1 lakh example, the outcome across three illustrative scenarios:

| Scenario (Illustrative Sample Rates Only) | Approx. Monthly EMI | Approx. Total Cost (interest + fee + GST) |

|---|---|---|

| Card EMI at 15% p.a., 12 months | ₹9,026 | ₹1,08,901 |

| Personal loan at 12% p.a., 12 months | ₹8,885 | ₹1,07,800 |

| Personal loan at 12% p.a., 24 months | ₹4,707 | ₹1,14,148 |

The 24-month option has the lowest monthly EMI but the highest total cost — more than ₹6,000 higher than the 12-month personal loan. Note that these are illustrative figures using sample rates for educational purposes. Actual rates, fees, and GST amounts vary by lender, card issuer, and borrower profile. Always verify current terms with your lender before deciding. You can model different scenarios using the Use EMI calculator.

For card EMI specifically, also factor in the credit limit blocked. If ₹1 lakh of Rohan’s ₹2 lakh limit is locked, his credit utilisation rises to 50% or higher if he uses the card further. This can affect his CIBIL score independently of repayment behaviour. For personal loans, check whether the new EMI pushes your total monthly obligations above a safe threshold relative to your salary.

How to Decide What’s Right for You

your purchase amount is under ₹50,000, the card EMI tenure is 12 months or less, the offer shows transparent charges, and your card limit stays above 30% after conversion — THEN credit card EMI may be the more convenient option with no separate application.

your borrowing need is ₹1 lakh or more and you want a tenure of 18–48 months with a structured repayment schedule tracked separately from your card — THEN a personal loan may offer a cleaner, lower-cost structure, especially if your credit score is 750 or above.

you need cash credited to your bank account rather than a purchase conversion — THEN only a personal loan can meet this need. Credit card EMI only converts a card purchase; it does not release cash unless your issuer specifically offers a card-to-account loan product.

the card EMI processing fee is nil, the interest rate matches or beats the personal loan, and the total cost calculation confirms card EMI is cheaper — THEN there is no reason to go through a separate personal loan application.

your CIBIL score is below 700 — THEN a personal loan application may be declined or offered at a materially higher rate. Card EMI (pre-approved on your existing card) may be the available option, but verify the actual rate and total cost before accepting.

your total existing EMIs already consume 40% or more of your take-home salary — THEN adding either obligation increases your financial risk. Use the Understand EMI safety guide to check whether your salary can absorb another commitment, and review Check loan eligibility before applying for a personal loan.

you are not certain what the total repayment will be including all fees, GST, and foreclosure terms — do not accept any borrowing offer before completing the full cost calculation. No offer is urgent enough to skip the numbers.

Common Mistakes to Avoid

Comparing Only the Monthly EMI

The most common mistake is choosing based on which option has the lower monthly payment.

A longer tenure always produces a smaller EMI — but also always produces higher total interest. On a ₹1 lakh loan, stretching tenure from 12 to 24 months can add ₹6,000–₹8,000 in interest even at the same rate.

Always calculate and compare total repayment before making any decision.

Assuming No-Cost EMI Has Zero Cost

The “no-cost” label refers to the interest component being subsidised — usually by the merchant. It does not mean all charges are zero.

Some no-cost EMI schemes still carry a flat processing fee (typically ₹200–₹499 or more) plus 18% GST. Others apply only when you forgo an existing cashback or discount. The net cost can be non-trivial on smaller purchases.

Read the checkout page or MITC carefully before confirming a no-cost EMI offer.

Ignoring GST on Charges

Borrowers often factor in the processing fee but forget that 18% GST applies on it. A ₹1,000 processing fee becomes ₹1,180 after GST. On larger loan amounts with higher processing fees, this adds up.

Include fee plus GST in every cost comparison you make.

Paying Only the Minimum Amount Due Instead of the Full EMI

If you have both an active card EMI and unpaid non-EMI card purchases, you may be tempted to pay only the minimum amount due on your card statement.

Doing this leaves the non-EMI balance subject to revolving interest, which is significantly higher than your EMI rate. This can silently inflate your total borrowing cost month after month. Read Avoid minimum due trap to understand exactly how this works.

Choosing a Longer Tenure Just to Make the EMI Look Comfortable

A ₹4,700 per month EMI looks manageable. A ₹8,900 per month EMI looks tighter.

But the 24-month option can cost ₹6,000–₹8,000 more overall on a ₹1 lakh loan. If you can afford the higher EMI, the shorter tenure saves money. Choose tenure based on what you can genuinely sustain — not on what looks comfortable on a screen.

Not Checking Foreclosure Terms Before Signing Up

Life can change. You may receive a bonus or salary increment and want to repay early.

Some card EMI schemes do not permit foreclosure mid-tenure. Others charge a flat fee or a percentage of the outstanding amount. Personal loans generally permit foreclosure but with a prepayment charge. Not knowing this in advance means paying a penalty you did not budget for — or being locked into an obligation you could have exited.

Ignoring the Credit Limit Reduction on Card EMI

When you convert a ₹1 lakh purchase to card EMI, your available credit limit reduces by ₹1 lakh until the balance clears.

If you rely on the same card for daily expenses, travel bookings, or emergencies, a reduced limit can be inconvenient or costly. It also raises your credit utilisation ratio, which credit bureaus factor into your score.

Accepting Pre-Approved Offers Without Comparing

Pre-approved card EMI offers are designed to be accepted quickly. The rate may or may not be competitive.

Take two minutes to also check a personal loan offer for the same amount and tenure. If the personal loan total cost is materially lower, the pre-approved convenience is costing you money.

When This May Not Be the Right Choice

Neither credit card EMI nor a personal loan is the right move in all circumstances. Consider stepping back if any of these apply to your situation:

Your income is variable or uncertain. If your salary is commission-based, contractual, or could reduce in the next 6–12 months, committing to a fixed monthly obligation increases financial risk during low-income periods.

Your credit card outstanding is already high. If your existing card balance is already significant, adding an EMI commitment on the same card further strains your repayment budget and raises your credit utilisation ratio.

Your existing EMIs are already at an unsafe level. If your total EMI obligations are already at or above 40–50% of take-home pay, adding another EMI — regardless of how small it looks — pushes you into territory where any income disruption or unexpected expense becomes a crisis.

The expense is discretionary, not necessary. Borrowing for a genuine household need or a medical expense is different from borrowing for a lifestyle upgrade or an impulsive purchase. Paying interest on a want is always more expensive than waiting and saving.

You do not fully understand the charges or repayment schedule. If the offer is not entirely clear — on total interest, processing fee, GST, foreclosure terms, and credit bureau reporting — do not accept it until you have the complete picture.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Before accepting any credit card EMI or personal loan offer, verify the current terms directly from the relevant official source. No third-party article — including this one — is a substitute for the actual document governing your specific product and lender.

- RBI (rbi.org.in): The Reserve Bank of India regulates banks and NBFCs that offer personal loans and credit cards in India. RBI circulars govern interest rate disclosure, prepayment norms, and fair lending practices.

- Your bank or NBFC’s official schedule of charges: All lenders are required to publish their schedule of charges, including processing fees, prepayment charges, and late payment fees. This is the authoritative document for your specific loan terms.

- Your credit card MITC document: The Most Important Terms and Conditions document for your specific card lists the applicable EMI interest rate, processing fee, foreclosure terms, and GST applicability. This is different across card variants even from the same issuer.

- Your loan sanction letter and repayment schedule: Once a personal loan is sanctioned, the sanction letter and amortisation schedule detail every EMI, the interest component, and the outstanding balance at each step.

- Your credit bureau report: CIBIL, Experian, Equifax, and CRIF are the four licensed credit information companies in India. You can access your credit report directly from their official websites to understand existing obligations before taking on new borrowing.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Ask for the amortisation schedule before finalising. Any lender or card issuer should be able to show you a month-by-month breakdown of principal, interest, and outstanding balance. If you cannot get this before signing, that is itself a reason to pause.

- Compare total repayment for the same tenure, not just EMI. Lock both options to the same tenure — say 12 months — and compare total repayment plus fees. If you then choose a different tenure, make the choice consciously, knowing the total cost impact.

- Check whether foreclosure is allowed and at what cost before signing up. Some card EMI products lock you in. If you plan to repay early — for example, after a bonus — a personal loan with a known foreclosure charge may be more flexible than a card EMI with no early exit.

- Keep credit utilisation under 30% after card EMI conversion. If converting a purchase to EMI will push your card utilisation above 30–35% of your limit, check whether you have another lower-balance card for daily expenses, or whether you want to reconsider the tenure to speed up the balance reduction.

- Never roll non-EMI card debt after converting a purchase to EMI. Once a purchase is on EMI, the rest of your card statement must be paid in full each month. If you start carrying unpaid non-EMI balances, the revolving interest on those balances will far exceed the EMI rate you thought you locked in.

- Check your eligibility before applying for a personal loan. A hard enquiry on your credit report happens at the time of application, not approval. Multiple rejections in a short window can lower your score. Use Check loan eligibility to understand what lenders look for before you apply.

- Use “as of current date” terms, not what you read six months ago. Rates change. Fee structures change. An offer that seemed expensive last year may now be competitive — or vice versa. Treat every new borrowing decision as a fresh comparison.

Frequently Asked Questions

Is credit card EMI cheaper than a personal loan?

It depends on the specific rate, processing fee, and tenure for both options. For many borrowers with good credit profiles, a personal loan may offer a lower interest rate than card EMI. However, card EMI can be cheaper if your issuer offers a low or nil processing fee and the interest rate is competitive. Always compare total repayment — not just monthly EMI — for the same tenure before deciding.

Does credit card EMI affect my CIBIL score?

Yes, in two ways. First, the EMI balance reduces your available credit limit, which can raise your credit utilisation ratio. A high utilisation ratio can negatively affect your CIBIL score even if you are repaying on time. Second, like any credit obligation, missing or delaying an EMI payment is reported to credit bureaus and can damage your score.

Is no-cost EMI really free?

Not always. Some no-cost EMI schemes charge a flat processing fee plus 18% GST. Others may require you to forgo a discount or cashback that would have applied on full payment. The merchant or platform absorbs the interest cost in a genuine subvention scheme — but any associated fees and forfeited discounts are a real cost to you. Always check the total amount payable before confirming a no-cost EMI.

Can I prepay or foreclose a credit card EMI?

This varies by card issuer. Some issuers allow foreclosure with a flat fee or a charge on the outstanding balance. Others do not permit it at all during the tenure. Check your specific card’s MITC or contact your issuer before committing, especially if you anticipate a bonus or lump sum that you might want to use for early repayment.

Which is better for a ₹1 lakh purchase — card EMI or personal loan?

For a ₹1 lakh purchase, calculate the total cost — principal, total interest, processing fee, and GST — for both options at the same tenure. If your card EMI rate is higher than the personal loan rate by more than 2–3%, the personal loan may save more than its processing fee costs. If both rates are similar and the card EMI has no processing fee, card EMI is likely more convenient. The answer depends on your specific offers, not a general rule.

Which is better for emergency cash needs?

For cash needs — where you need money credited to your bank account — only a personal loan or a card-to-account loan product (if your issuer offers it) can serve the purpose. Standard credit card EMI only converts a card purchase to instalments; it cannot release cash. If speed is critical, a pre-approved personal loan or an overdraft facility may be faster than a fresh personal loan application.

What happens if I miss an EMI payment on either option?

A missed EMI triggers a late payment fee, interest on the overdue amount, and a negative entry in your credit bureau report. For credit card EMI, the missed payment may also attract the card’s standard interest rate on the overdue amount, which is typically much higher than the EMI rate. For personal loans, late payment charges as per the lender’s schedule of charges apply.

Does a personal loan application create a hard enquiry that hurts my CIBIL score?

Yes. When you apply for a personal loan, the lender pulls your credit report — a hard enquiry. A single hard enquiry typically causes a minor, temporary score reduction. However, multiple applications in a short period signal credit-hungry behaviour to future lenders and can collectively lower your score more meaningfully. Apply only after comparing offers and deciding to proceed, rather than applying to multiple lenders simultaneously.

Can I get a personal loan if I already have a high credit card outstanding balance?

It depends on the lender’s assessment. A high credit card outstanding raises your debt-to-income ratio and can reduce your chances of personal loan approval or lead to a lower sanctioned amount. Some lenders will also factor in your credit utilisation ratio. It is worth checking your credit bureau report and reducing outstanding card balances where possible before applying for a personal loan.

What is the difference between credit card EMI and a credit card loan?

Credit card EMI converts a specific purchase on your card into equal monthly payments. The amount is linked to that purchase and charged against your credit limit. A credit card loan (sometimes called an insta loan or credit card cash loan) is a separate facility where the lender disburses a cash amount to your bank account, usually against your card limit or a pre-approved limit. Both have separate rate and fee structures — verify each independently.

Final Verdict

Credit card EMI vs personal loan is not a question with one universal answer. Credit card EMI works well for short-tenure conversions of card-eligible purchases where the charges are transparent, the interest rate is competitive, and your card limit stays healthy after conversion. A personal loan may be the better option when the borrowing amount is larger, a longer or more structured repayment schedule is needed, or when cash disbursal — not a purchase conversion — is required.

What the decision should never be based on: which screen looked more convenient in the moment, or which had the lower monthly EMI. The cheaper option is the one with the lower total cost including all interest, fees, and GST — for the same tenure and the same principal.

For more on whether your current salary can absorb another obligation, read Understand EMI safety before accepting any offer. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.