Most car buyers in India start with one question: what will the EMI be? That is the wrong starting point. The right question is what will the car actually cost — and what happens to your savings — whether you pay the full amount upfront or spread it over five years through a loan.

For a ₹12 lakh family car, taking a car loan versus paying cash can mean a difference of over ₹2 lakh in interest alone. Add processing fees, insurance bundling, and the opportunity cost of tying up your savings, and the comparison gets more complex than most dealers or lenders will explain at the showroom.

This article breaks down the car loan vs buying with cash decision using total cost, monthly cash flow, emergency fund safety, and lender charges — so you can make the choice that actually suits your income, savings, and situation. Loan interest rates and fees vary by lender, credit profile, and tenure. Verify all figures directly with your lender before signing.

Quick Answer: Car Loan vs Buying with Cash

Car loan vs buying with cash depends on total cost and liquidity. For a ₹12 lakh car, cash avoids loan interest, while a 5-year loan may add interest and fees. Cash is better if emergency savings remain safe; loan works only if EMI is comfortably affordable.

Key Takeaways

- For a ₹12 lakh car financed over 5 years at a typical retail car loan rate, total interest alone can add ₹2–₹2.5 lakh to your purchase cost — always compare total outflow, not just the monthly EMI figure.

- Cash is almost always cheaper on paper — but only if your emergency fund (3–6 months of household expenses) remains fully intact after the purchase.

- A longer loan tenure reduces monthly EMI but substantially increases total interest paid — the difference between a 3-year and a 7-year tenure on the same loan amount can exceed ₹1.5 lakh in extra interest.

- A higher down payment reduces the loan principal directly — this cuts both your EMI and total interest without requiring a lower interest rate from your lender.

- Car loans in India use the reducing balance interest method — interest each month is charged only on the outstanding principal, not on the original loan amount.

- The true cost comparison must include: down payment + all EMIs + processing fee + foreclosure charges for the loan route, versus on-road cash price + lost earnings on deployed savings for the cash route.

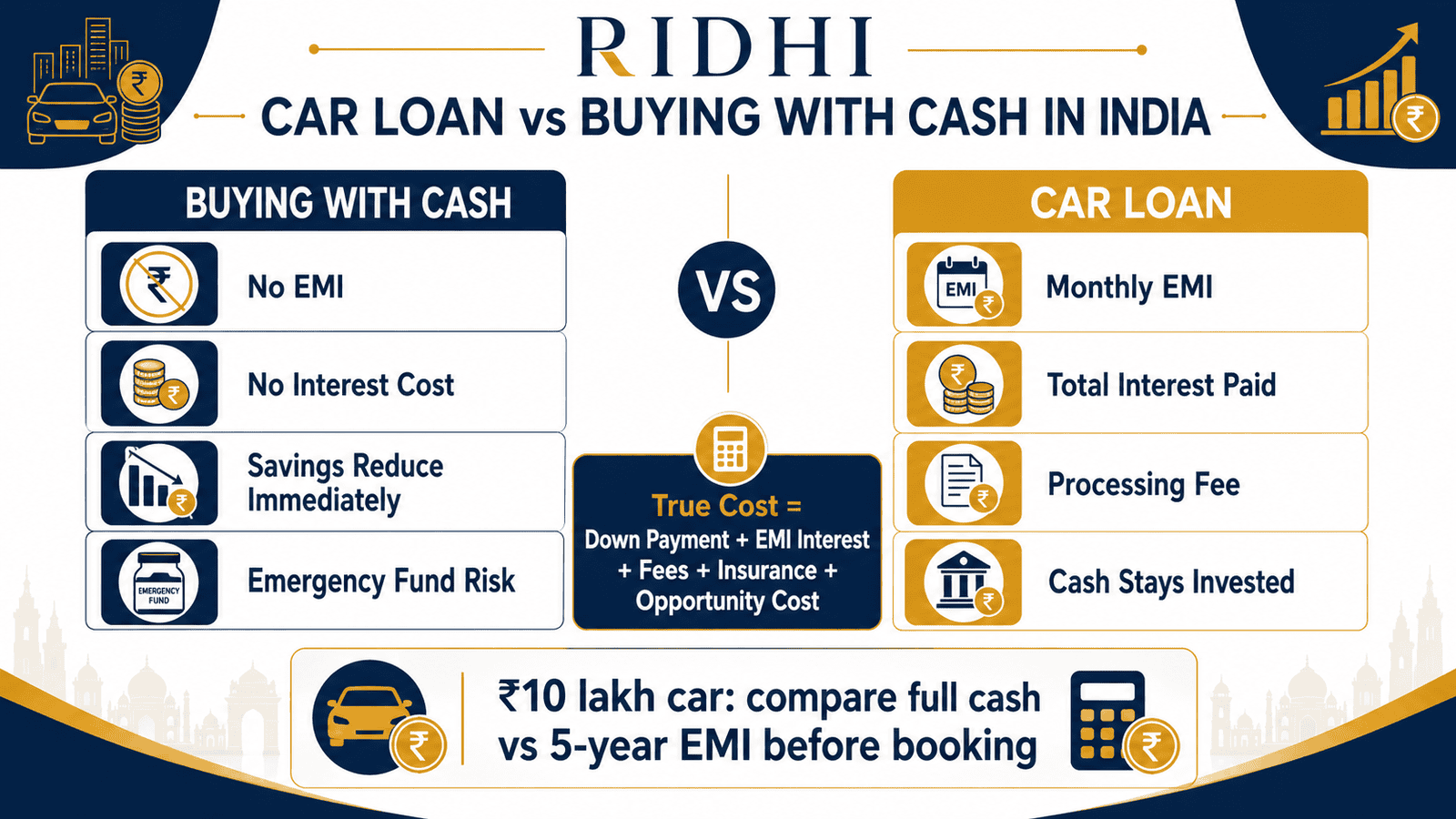

Comparison: Car Loan vs Buying with Cash

| Parameter | Buy with Cash | Car Loan |

|---|---|---|

| Total purchase cost | Lower — no interest or fees added | Higher — interest and charges added |

| Monthly cash flow pressure | None — no EMI obligation | Fixed EMI every month for the full tenure |

| Emergency savings impact | Savings reduced sharply on day of purchase | Savings partially preserved |

| Interest burden | None | Significant — depends on rate, tenure, and loan amount |

| CIBIL / credit score effect | No loan record created — no impact | Improves score if repaid on time; damages score if missed |

| Ownership and flexibility | Full — car in your name, no lender involved | Car hypothecated to lender until full repayment |

| Best suited for | Buyer with surplus savings intact post-purchase | Buyer with stable income and safe EMI-to-income ratio |

| Biggest financial risk | Emptying savings, losing financial buffer entirely | Underestimating total interest and fee burden over tenure |

Key Facts at a Glance

| Factor | Cash Purchase | Car Loan |

|---|---|---|

| On-road price (ex-showroom + road tax + insurance + registration) | Paid in full on purchase day | Down payment upfront; balance financed |

| Interest cost | ₹0 | Varies by lender, rate, tenure, and loan amount — verify with your lender |

| Processing fee | Not applicable | Charged as a flat amount or percentage of loan; see loan processing fees for details on how this charge works |

| Loan tenure options | Not applicable | Typically 1–7 years — verify with your specific lender |

| Prepayment option | Not applicable | Usually allowed; foreclosure charges may apply — always confirm in your loan agreement |

| Car hypothecation | No — you own it outright from day one | Yes — car is pledged to lender until loan is fully repaid |

How Car Loan vs Cash Purchase Actually Works in India

What Buying with Full Cash Means

When you pay cash for a car, you pay the complete on-road price out of your savings or liquid investments on the day of delivery. There is no EMI, no lender, and no interest charge. The car is registered directly in your name — no hypothecation endorsement on the RC book, no lender’s permission needed if you want to sell or modify the vehicle later. Your savings are reduced by the full amount immediately, but your monthly cash flow stays completely free.

The hidden cost of paying cash is not interest — it is opportunity cost. The ₹12 lakh you deploy on the car is money that can no longer earn returns in an FD, a mutual fund, or any other instrument. If your savings were earning 7% per annum in a fixed deposit, that income stops the day you break the FD to buy the car. This cost is real, even if it does not appear on any statement.

What Taking a Car Loan Means

A car loan lets you pay a portion of the car price upfront as a down payment and borrow the rest from a bank or NBFC. You repay through fixed equated monthly instalments over a chosen tenure. The lender charges interest on the outstanding principal — this is the most important number to understand before comparing options.

Car loans in India are structured on the reducing balance interest method. Interest each month is calculated only on the remaining outstanding principal, not on the original loan amount. As you repay, the principal falls and so does the interest component of each EMI. Your early EMIs carry a heavier interest share; later EMIs carry more principal repayment. This is important because it means prepaying in the early years saves significantly more interest than prepaying in the later years.

This structure also explains why monthly EMI can hide the total borrowing cost. An EMI of ₹20,750 per month looks manageable on a ₹1.8 lakh salary. But multiply that EMI by 60 months and the total amount paid to the bank is over ₹12.4 lakh — on a loan of ₹10 lakh. The ₹2.4 lakh difference is the real cost of borrowing, and it deserves your full attention before you compare it to the cash option.

Why a Car Is a Depreciating Consumption Asset

A car is not an investment. From the moment it leaves the showroom, its market value drops — often by 15–20% in the first year, and steadily thereafter. You are borrowing money to buy something that loses value. This is not a reason to refuse buying a car; most households genuinely need one. It is a reason to be disciplined about price, tenure, and borrowing amount. Stretching tenure or loan size to afford a more expensive model means paying interest on a larger principal — for a vehicle that depreciates the same way regardless of what you borrowed.

According to RBI guidelines, banks and NBFCs are required to provide borrowers with a clear loan statement showing the annualised interest rate, EMI schedule, total interest payable, and prepayment terms before disbursement. If you are comparing two lenders, compare all these figures — not just the headline rate. A lender offering a slightly lower rate but high processing fees or restrictive foreclosure terms may cost more in total than a lender charging a slightly higher rate with zero prepayment charges.

What the On-Road Price Actually Includes

A common calculation error is using the ex-showroom price in loan and cash comparisons. The on-road price — which is what you actually pay — adds road tax (varies by state and vehicle category), registration charges, first-year comprehensive insurance premium, dealer handling charges, and any accessories or extended warranty. For a ₹10–12 lakh ex-showroom car, the on-road price is typically 8–12% higher depending on your state. Every comparison — down payment, loan amount, and total cost — must use the on-road figure, not the showroom sticker.

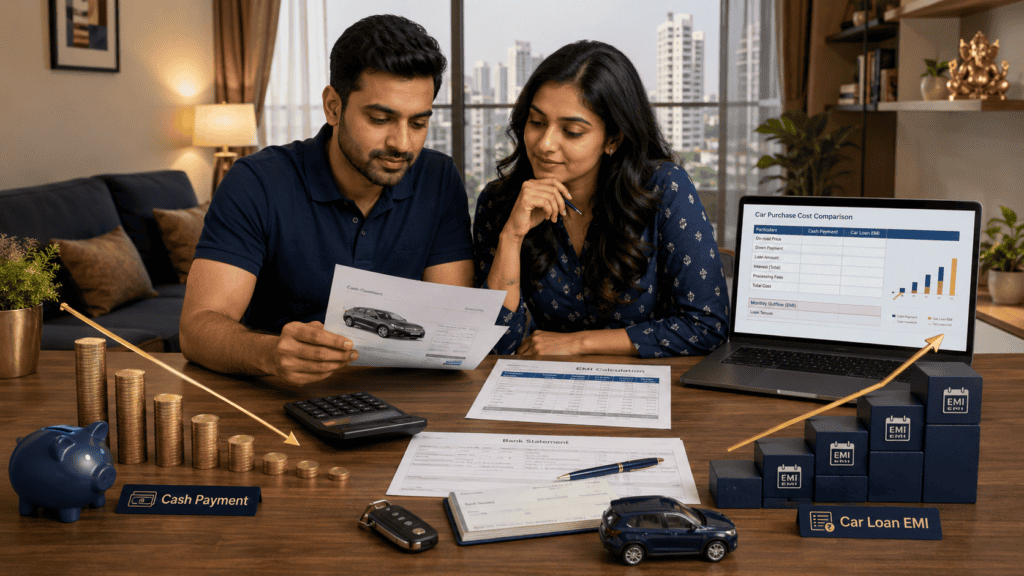

Real Example: Rohan’s ₹12 Lakh Family Car Decision

Rohan is 34, works as a senior software engineer in Bengaluru, and takes home ₹1.8 lakh per month. He wants to buy a ₹12 lakh on-road family car — the household’s first. He has ₹18 lakh saved: ₹6 lakh in a liquid emergency fund and ₹12 lakh in a fixed deposit earning an illustrative 7% per annum. He is weighing two options.

Option A — Full cash purchase: Rohan breaks the FD and pays ₹12 lakh outright. No EMI, no lender, no interest. But his total savings immediately drop to ₹6 lakh — which is exactly his emergency fund. There is no separate buffer left for a job disruption, a medical emergency, or a major home repair. He also loses the approximately ₹84,000 per year he was earning as FD interest.

Option B — Car loan with down payment: Rohan pays ₹2 lakh as a down payment and borrows ₹10 lakh at an illustrative 9% per annum for 5 years. His EMI works out to approximately ₹20,750 per month. Total EMIs over 60 months: approximately ₹12,45,000. Add the ₹2 lakh down payment and a processing fee — total outflow is approximately ₹14.5 lakh. He retains ₹10 lakh in his FD and keeps his emergency fund fully intact. For a full breakdown of what a first car purchase actually costs beyond the loan, see the first car total cost guide.

The key insight: Rohan’s loan option costs approximately ₹2.5 lakh more in total than paying cash. But it is not a sign of financial carelessness — it is the price he consciously pays to retain liquidity and keep his financial buffer intact. Whether that trade-off is worth it depends entirely on whether ₹20,750 per month sits comfortably within his income after rent, school fees, insurance premiums, and household expenses.

How to Calculate the True Cost: Cash vs Car Loan

Total loan cost = Down payment + (Monthly EMI × Tenure in months) + Processing fee + Any foreclosure charges paid

Total cash cost = On-road price paid + Opportunity cost of savings deployed

Using Rohan’s figures at an illustrative 9% per annum rate (verify current rates with your lender before any decision):

| Scenario | Key Inputs (Illustrative) | Total Outflow (Illustrative) |

|---|---|---|

| Cash purchase | ₹12L on-road, FD broken, emergency fund intact at ₹6L | ₹12,00,000 |

| Car loan — 3-year tenure | ₹10L at 9% p.a., ₹2L down, ~₹31,800/month EMI | ~₹13,45,000 (approx. ₹1.45L interest) |

| Car loan — 5-year tenure | ₹10L at 9% p.a., ₹2L down, ~₹20,750/month EMI | ~₹14,45,000 (approx. ₹2.45L interest) |

All figures are illustrative and based on a 9% per annum assumption. Your actual rate, EMI, and total interest will differ based on your lender, credit score, vehicle, and tenure. Use the EMI calculator India to input the exact rate your lender quotes and calculate your precise total interest before comparing options.

On opportunity cost: if Rohan retains ₹10 lakh in an FD earning an illustrative 7% per annum while taking a loan at 9%, the FD could generate approximately ₹3.5 lakh over 5 years in interest income. The loan costs approximately ₹2.45 lakh in interest. On paper, retaining the FD looks like it produces a net positive — but this assumes the FD rate holds constant, the FD is not broken early, and the return is actually achieved. These are not guaranteed outcomes, and this calculation should be treated as illustrative context, not a reliable financial plan.

How to Decide What’s Right for You

you can pay the full on-road price in cash AND your emergency fund of 3–6 months of household expenses stays completely untouched — THEN a cash purchase is almost certainly the cheaper and cleaner choice.

paying cash would reduce your total savings below your emergency buffer — THEN take a car loan. Preserving that financial buffer is more important than saving ₹2–2.5 lakh in interest over five years.

the car loan EMI keeps your total monthly debt obligations within a safe share of your take-home income — THEN the loan is financially sustainable. Check the safe EMI limit guidance to assess whether your combined debt-to-income ratio remains manageable with the new EMI added.

you are currently repaying a home loan, a personal loan, or have active credit card balances — THEN adding a car loan increases your total monthly obligations significantly; assess whether the combined EMI load is genuinely sustainable before committing.

the car you want requires stretching either your savings or your EMI comfort zone — THEN consider a less expensive model rather than a longer tenure or a higher loan amount.

you are buying the car primarily for a lifestyle upgrade rather than a genuine household transport need — THEN delay and reassess; the ongoing ownership costs of fuel, servicing, insurance renewals, and parking add significant recurring obligations beyond the purchase price.

your income is stable, your emergency fund is intact after the purchase, and the EMI fits comfortably within your monthly budget — do not take a car loan. The interest cost is real, it compounds over years, and it adds nothing to the value of a vehicle that is depreciating at the same time.

Common Mistakes to Avoid

Comparing Only EMI, Not Total Interest Paid

The monthly EMI tells you what leaves your account each month. The total interest payable tells you what the loan actually costs. On a ₹10 lakh loan at an illustrative 9% per annum for 5 years, total interest is approximately ₹2.45 lakh — a figure that never appears in the dealer’s EMI brochure.

Always request the total interest payable figure from the lender in writing before comparing it with the cash option. This single number changes how the decision looks entirely.

Choosing a Longer Tenure Just to Afford a More Expensive Car

A 7-year tenure substantially reduces the monthly EMI on the same loan — but the total interest paid is far higher than on a 5-year or 3-year tenure. Some buyers stretch tenure specifically to justify upgrading to a more expensive model. The lower monthly number feels affordable; the extra ₹1–1.5 lakh in total interest does not register until the loan is nearly repaid.

Use tenure to manage monthly cash flow — not to inflate your purchase budget.

Spending All Savings on Down Payment or Cash Purchase

A larger down payment reduces your loan principal and saves interest — sound logic in isolation. But not if it drains your emergency fund. A household with zero savings buffer after buying a car is one medical bill or one redundancy notice away from serious financial distress. Always keep 3–6 months of essential monthly expenses liquid and untouched, regardless of which option you choose.

Underestimating On-Road Price, Insurance, and Maintenance

Road tax, registration, first-year insurance premium, dealer handling charges, and accessories can add ₹50,000 to over ₹1 lakh to a ₹10–12 lakh ex-showroom car depending on your state and the insurer. Many buyers budget for the ex-showroom figure only and are caught short at the dealership. Insurance premium varies by insurer, vehicle model, location, selected add-ons, and your claims history — always get a direct quote from at least two IRDAI-registered insurers before accepting a dealer-bundled policy.

Assuming Investment Returns Will Definitely Beat Loan Interest

The logic of keeping savings invested and taking a cheap loan can work in some situations. But equity mutual fund returns are uncertain and not guaranteed. An FD rate can change at renewal. A loan interest obligation is fixed. Making a leveraged borrowing decision on the assumption that future variable returns will reliably exceed a fixed loan cost is a risk — evaluate it consciously, not as a foregone conclusion.

Ignoring Prepayment Options After Signing

If your salary increases or you receive a bonus, partial prepayment on a car loan can significantly cut total interest — but only if your lender allows it without prohibitive foreclosure charges. Many borrowers never revisit the prepayment option after the loan is disbursed. Check the terms at the time of signing, and revisit the option whenever your cash flow improves meaningfully.

When This May Not Be the Right Choice

Buying a car — by any method — may not be the right financial move if your income is unstable or your employment situation is uncertain. A fixed EMI obligation on a depreciating asset is one of the harder commitments to sustain through a job change, a reduced salary, or a family income disruption.

If you are already carrying a home loan, an active personal loan, or unpaid credit card balances, adding a car loan increases your total monthly outflow and reduces the financial cushion available for other priorities. The car may feel necessary, but the combined EMI burden deserves an honest stress test before you commit.

A car bought primarily as a lifestyle statement — rather than for a genuine transport need — is worth pausing on. Fuel, periodic servicing, insurance renewals, parking, and maintenance add recurring monthly costs that persist well beyond the showroom excitement and the early EMIs.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Car loan interest rates, processing fees, prepayment rules, and foreclosure charges are set by individual lenders — not by a single regulatory rate ceiling. Before signing any loan agreement, verify the following directly from official sources:

- RBI (rbi.org.in) — For regulated lending guidelines, Fair Practices Code obligations of banks and NBFCs toward borrowers, and borrower rights related to loan disclosures, interest rate transparency, and grievance redressal.

- Your lender’s official website or sanction letter — For the exact annualised interest rate, EMI schedule, processing fee amount, prepayment policy, and foreclosure charges specific to your loan.

- IRDAI (irdai.gov.in) — For understanding motor insurance policyholder rights and for guidance on insurer grievance procedures if a bundled insurance product is being offered with your loan.

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

Expert Tips

- Negotiate the car price first — the loan separately. Dealers often route financing through their preferred lenders and add a margin on the rate. Get the best confirmed on-road price in writing before approaching any lender. Then compare loan offers from at least two banks and one NBFC, including your own salary account bank where you may receive a preferential rate.

- Ask for the total interest payable figure, not just the EMI. Before comparing any two loan offers, request the full amortisation schedule or a written total interest payable amount. A lender quoting a lower EMI with a longer tenure may cost more in total than one with a slightly higher EMI over a shorter tenure.

- Increase your down payment only if your emergency fund stays fully intact. Paying ₹3–4 lakh as a down payment instead of ₹2 lakh on a ₹12 lakh car meaningfully reduces both the loan principal and total interest. But not if it leaves you with no liquid buffer. The interest saving is not worth the risk of having no financial cushion.

- Choose the shortest tenure your monthly cash flow can safely absorb. The difference in total interest between a 3-year and a 5-year tenure on the same ₹10 lakh loan can exceed ₹1 lakh. If a slightly higher monthly EMI is manageable, the shorter tenure pays off significantly over the loan life.

- Check prepayment rules before signing. If you are likely to receive annual bonuses or salary increments, a loan with zero or low foreclosure charges lets you cut principal — and future interest — whenever cash flow improves. Understand the prepayment versus part payment distinction before deciding how to deploy lump sums against an active car loan.

- Never accept bundled insurance without comparing. Some lenders offer or require insurance products bundled with the car loan. You are not obligated to purchase motor insurance from a lender’s tied insurer. Compare comprehensive insurance premiums from at least two IRDAI-registered insurers directly and choose the policy that gives you the right coverage at a fair premium.

Frequently Asked Questions

Is it better to buy a car with cash or a loan in India?

Cash is the cheaper option in total cost because it eliminates all interest and lender charges. But cash is the right choice only if your emergency fund — 3 to 6 months of household expenses — stays fully intact after the purchase. If paying cash depletes your savings buffer, a car loan at a rate and EMI your income can comfortably carry may be the safer decision. The answer genuinely depends on your savings position, income stability, and existing financial obligations — there is no universal rule.

How much total interest do I pay on a ₹10 lakh car loan?

Total interest depends on the rate and tenure. As an illustration: a ₹10 lakh loan at 9% per annum for 5 years generates approximately ₹2.45 lakh in total interest. The same loan for 3 years at the same rate generates approximately ₹1.45 lakh. Actual figures will differ based on your lender’s rate and your credit profile. Use an EMI calculator with your lender’s exact quoted rate to compute the precise total interest before comparing it to the cash option.

Does a car loan improve my CIBIL score?

It can — provided you repay every EMI on time without a single miss. A car loan adds a secured credit line to your credit history, and consistent on-time repayment over the tenure can improve your CIBIL score. However, even one missed EMI is reported to credit bureaus and can lower your score meaningfully. A car loan improves your score through disciplined repayment behaviour — not simply by existing. No loan approval guarantees a score improvement.

How much down payment is ideal for a car loan?

Most lenders require a minimum down payment of 10–20% of the on-road price, though requirements vary by lender and loan profile. A higher down payment — say 30–40% of on-road price — reduces the loan principal substantially and cuts both EMI and total interest. The ideal down payment is the highest amount you can pay while still keeping your emergency fund completely intact. There is no single universal ideal percentage.

Is a zero down payment car loan a good idea?

Zero down payment loans are available from some banks and NBFCs. Borrowing the full on-road price means paying interest on the entire amount for the entire tenure — total interest will be significantly higher than a loan with a meaningful down payment. A zero down payment loan makes sense only if you have a specific productive use for the cash you retain and the resulting EMI remains comfortably within your monthly income after all other obligations. It is not automatically a poor choice — but the higher interest cost must be accepted knowingly.

Should I keep my savings invested and take a car loan instead?

This logic holds only if your post-tax investment return is reliably higher than the loan interest rate. If you are in the 30% tax bracket, post-tax FD returns are lower than the headline rate. Equity mutual fund returns are variable and not guaranteed in any year or over any fixed period. Taking a loan to keep savings invested is a form of leveraging — it works when returns exceed the loan cost and fails when they do not. Treat this as a conscious risk decision, not as a default assumption.

Can I prepay a car loan early?

Most banks and NBFCs allow car loan prepayment or foreclosure. Some charge a foreclosure fee — typically a percentage of the outstanding principal at the time of closure. Others allow zero-cost prepayment after a minimum number of EMIs. Prepaying in the early part of the tenure saves more interest than prepaying later because the outstanding principal is higher in earlier months. Confirm the exact prepayment terms and any applicable charges in your loan agreement before assuming the option is available at no cost.

What is the difference between ex-showroom price and on-road price?

Ex-showroom price is the manufacturer’s base selling price, before state-level charges. On-road price adds road tax (varies by state and vehicle type), registration charges, first-year comprehensive insurance premium, dealer handling charges, and any accessories or extended warranty elected at delivery. For a ₹10–12 lakh ex-showroom car, the on-road price is typically 8–12% higher depending on your state and insurer. All comparisons — down payment, loan amount, and total cost — must be based on the on-road figure.

What happens if I miss a car loan EMI?

A missed EMI is reported to credit bureaus and can lower your CIBIL score, sometimes significantly. Repeated missed payments trigger collection calls, penalty charges, and in serious cases, the lender can repossess the vehicle — the car is hypothecated as security against the loan. Even a single missed EMI can affect your eligibility for future borrowing. If you foresee a temporary cash shortfall, contact your lender proactively before missing a payment; some lenders offer restructuring or temporary relief options if approached in advance.

Final Verdict

The car loan vs buying with cash decision comes down to two things: total cost and liquidity safety. Cash is the financially cleaner option — no interest, no fees, no lender — but only when your emergency fund survives the purchase fully intact. A car loan is a reasonable trade-off when it protects your savings buffer and the EMI sits comfortably within your income after all existing obligations. Neither option is universally correct.

The most expensive outcome in this comparison is not the interest on a loan. It is buying a car — by any method — that stretches either your savings or your monthly cash flow past safe limits. Do not ask only whether you can afford the EMI; ask whether you can afford the car. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.