Can ₹50,000 a month actually buy you a home? In theory, yes. In practice, the answer depends on far more than what is printed on your salary slip. Indian lenders do not simply multiply your income by a fixed number and hand you a cheque. They look at your existing EMIs, credit score, property value, down payment, and chosen tenure — all before arriving at the amount they are willing to lend.

For most salaried borrowers, the confusion starts here: the bank’s maximum approval figure and the EMI you can comfortably carry for 20 years are almost never the same number. The biggest mistake is optimising for the first while ignoring the second. This article explains exactly how home loan on 50000 salary eligibility is calculated, what FOIR and LTV actually mean for your application, and how to arrive at a loan amount that is both approvable and genuinely affordable — not just the highest figure a lender will quote.

Quick Answer: Home Loan on ₹50,000 Salary

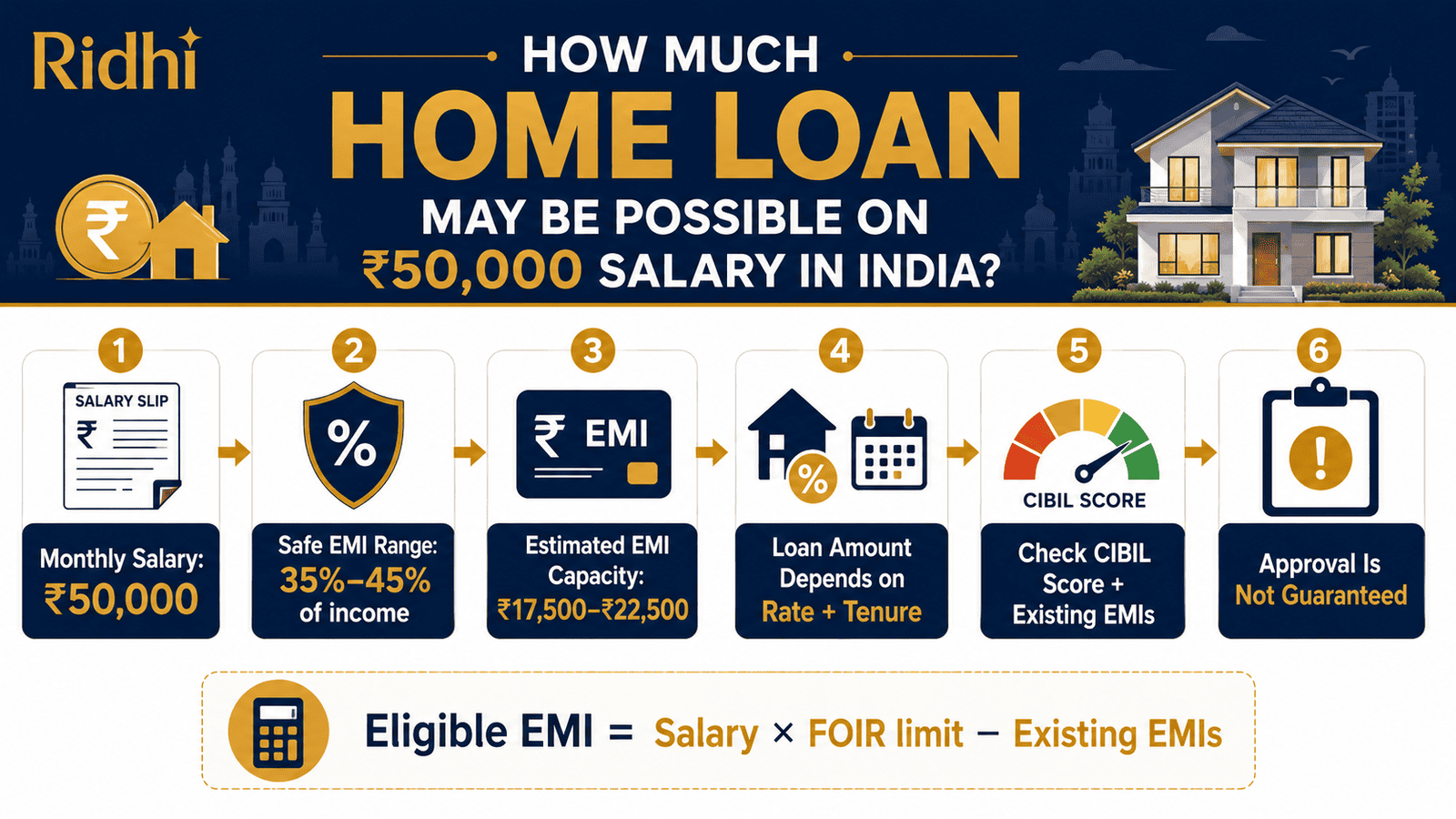

Home loan on 50000 salary is usually estimated from your safe EMI capacity, existing EMIs, credit score, interest rate, tenure and lender FOIR rules. As a rough planning range, a ₹50,000 monthly salary may support about ₹17,500–₹22,500 EMI before other EMIs, but final approval depends on the lender. Existing EMIs reduce this range immediately — a ₹7,000 car loan EMI could bring your available home loan EMI down to ₹10,500–₹15,500. Lender policies, interest rates, and FOIR limits can change. Calculate your EMI before applying.

How to Calculate Your Home Loan Eligibility on ₹50,000 Salary

Banks and NBFCs use a metric called FOIR — Fixed Obligation to Income Ratio — to decide how much total EMI you can carry. Most lenders allow all EMIs combined (including the proposed home loan) to be 40%–50% of your net monthly income. Here is a step-by-step breakdown using a ₹50,000 salary:

Step 1: Net monthly income = ₹50,000

Step 2: Safe FOIR range (40%–45%) → Maximum total EMI = ₹20,000–₹22,500

Step 3: Deduct existing EMIs (personal loan, car loan, credit card) → Available home loan EMI

Step 4: Convert available EMI into loan amount using the applicable interest rate and tenure

Step 5: Check that loan amount does not exceed lender’s LTV limit on the property value

The table below shows illustrative loan amounts at different EMI and tenure combinations. All figures use an assumed indicative rate of 8.75% per annum — verify the latest rate from your lender before planning.

| Available Home Loan EMI | Tenure | Approx. Loan Amount |

|---|---|---|

| ₹17,500 | 20 years | ~₹19.8 lakh |

| ₹20,000 | 20 years | ~₹22.6 lakh |

| ₹20,000 | 30 years | ~₹25.4 lakh |

| ₹22,500 | 20 years | ~₹25.5 lakh |

These are planning estimates only — not bank-approved amounts. Total cost matters as much as the loan amount. At ₹20,000 EMI for 20 years at 8.75%, total repayment on a ₹22.6 lakh loan is approximately ₹48 lakh — ₹22.6 lakh principal plus roughly ₹25.4 lakh in interest. A 30-year tenure on the same EMI increases your eligible loan to ~₹25.4 lakh but pushes total interest substantially higher over the extended period.

Use the EMI calculator India to run your exact numbers once you have a formal rate quote from the lender.

Key Takeaways

- A ₹50,000 net monthly salary translates to an available home loan EMI of ₹17,500–₹22,500 before existing obligations — not a fixed guaranteed loan amount.

- Every ₹5,000 in existing EMI reduces your available home loan EMI by the same amount — a ₹7,000 car loan can cut your eligible loan by ₹7–9 lakh or more.

- A CIBIL score below 700 can reduce your loan amount or raise the interest rate, increasing total repayment cost by lakhs over the full tenure.

- Choosing a 30-year tenure over 20 years raises your eligible loan by ₹2–3 lakh but can add ₹10–20 lakh or more in total interest paid over the loan’s life.

- Lenders finance only 75%–90% of property value under RBI’s LTV norms; the rest must come from your own savings as a down payment.

- Bank eligibility (maximum they will approve) and personal affordability (what you can comfortably repay) are two different numbers — plan for affordability, not maximum eligibility.

Key Facts at a Glance

| Factor | What It Means for Your Loan |

|---|---|

| Monthly income basis | Most lenders use net take-home salary, not gross or CTC |

| Safe EMI planning range | 40%–45% of ₹50,000 = ₹20,000–₹22,500 total EMI capacity (before existing EMIs) |

| Existing EMI impact | ₹7,000 existing EMI reduces available home loan EMI to ₹13,000–₹15,500 |

| Minimum CIBIL score | Most lenders prefer 700+; 750+ generally improves rate and approval chances |

| Tenure effect | Longer tenure raises eligible loan amount but increases total interest paid |

| LTV ratio | Lenders typically finance 75%–90% of property value; balance is your down payment |

How Home Loan Eligibility on ₹50,000 Salary Is Actually Calculated

Gross Salary vs Net Take-Home: Which One Counts?

The most misunderstood point in home loan planning is this: lenders base eligibility on your net monthly take-home salary, not your CTC or gross pay. If your monthly CTC components add up to ₹62,000 but your actual in-hand credit after PF deductions, TDS, professional tax, and LWF is ₹50,000, the bank uses ₹50,000. Planning your eligibility on gross figures leads to a surprise at the lender’s desk when the sanctioned amount comes in lower than expected.

This distinction also matters for salaried employees who receive a portion of pay as reimbursements — fuel allowance, meal coupons, or LTA. Many lenders count only the fixed taxable component of salary for FOIR purposes. If a part of your income is variable or reimbursement-based, confirm with the lender how they treat it before assuming full ₹50,000 as the income base.

What Is FOIR and Why Does It Determine Your Loan Amount?

FOIR — Fixed Obligation to Income Ratio — is the central metric Indian lenders use to assess how much of your income is already spoken for. The working is straightforward:

FOIR = (Total existing EMIs + Proposed home loan EMI) ÷ Net monthly income

At ₹50,000 net income and a FOIR limit of 45%, your total permissible EMIs — existing and proposed combined — are ₹22,500. If you already pay ₹7,000 per month on a car loan, the available home loan EMI drops to ₹15,500. That is the figure the lender runs through the EMI formula at their applicable rate and tenure to arrive at a loan amount — not a salary multiple.

This is why two people earning identical ₹50,000 salaries can receive very different approvals: one has no existing debt and a clean credit profile; the other carries personal loan and credit card EMIs that consume 25% of income before the home loan enters the picture. Understanding FOIR is the foundation of realistic loan planning. For the broader framework on how income-to-EMI ratios work in loan decisions, see our explainer on safe EMI ratio.

Why Your CIBIL Score Changes the Loan Amount and Rate

Your credit score influences two outcomes: whether you are approved and at what interest rate. A CIBIL score of 750 and above typically qualifies you for the best available rates from most lenders and makes underwriting straightforward. A score between 650 and 700 may still secure approval, but at a higher rate — which directly raises your EMI and reduces the loan amount a given EMI capacity can support. A score below 650 often results in rejection or heavily restricted sanction amounts.

According to RBI guidelines on credit information companies, banks are required to pull your credit history before sanctioning any loan. A single 30-day missed payment on a previous EMI or credit card bill can remain on your report for up to 36 months. If you are planning a home loan in the next six to twelve months, pull your full credit report from CIBIL, Equifax, or Experian today and resolve any outstanding discrepancies before approaching a lender.

How Property Value and LTV Cap Your Final Loan

Even if your income and FOIR support a higher loan, lenders will not fund 100% of the property’s registered value. The Loan-to-Value ratio, governed by RBI norms, caps how much of the property cost the bank will finance. For properties valued up to ₹30 lakh, lenders may extend up to 90% LTV. For properties priced above ₹30 lakh and up to ₹75 lakh, LTV typically falls to 80%. Above ₹75 lakh, it generally drops to 75%.

For most ₹50,000 salary borrowers, the binding constraint is the EMI limit — not the LTV — unless you are targeting a property significantly above ₹35 lakh, where the down payment requirement can become the harder problem to solve from existing savings.

How Tenure Changes Your Eligible Loan Amount

A longer tenure reduces the monthly EMI required to repay the same loan, which means the same EMI capacity supports a larger loan when stretched over more years. At ₹20,000 available EMI and 8.75%, a 20-year tenure supports roughly ₹22.6 lakh; the same EMI at 30 years supports about ₹25.4 lakh. The difference of ₹2.8 lakh in eligible loan amount comes at the cost of ten additional years of interest payments. Tenure is not a free variable — every additional year adds to total cost, even if the monthly number looks manageable today.

Real Example: Rohit’s Home Loan Calculation in Pune

Rohit, 31, works as a project coordinator at a private firm in Pune. His net monthly take-home salary is ₹50,000. He wants to understand his home loan eligibility before approaching a lender. His situation plays out in two scenarios.

Scenario A — No existing EMI: Rohit has no outstanding loans or credit card EMIs. At 45% FOIR, his maximum permissible total EMI is ₹22,500. At an indicative rate of 8.75% over 20 years, this supports an approximate loan of ₹25.5 lakh. Total estimated repayment: ₹25.5 lakh principal plus roughly ₹29.7 lakh in interest — approximately ₹55.2 lakh over the full tenure. That is the real cost, not the headline EMI figure.

Scenario B — Existing ₹7,000 car loan EMI: Rohit’s ongoing car loan EMI reduces available home loan EMI to ₹15,500. At the same rate and tenure, this supports an approximate loan of ₹17.6 lakh. Total estimated repayment: roughly ₹38 lakh over 20 years.

The key insight: a single ₹7,000 existing EMI shrank Rohit’s possible home loan by approximately ₹7.9 lakh — a 31% reduction. Foreclosing short-duration loans before applying for a home loan is often worth the prepayment cost.

Comparison: Different Borrower Situations on ₹50,000 Salary

| Situation | Impact on Eligibility | Key Consideration |

|---|---|---|

| No existing EMI | Higher eligibility | Full FOIR headroom available for home loan EMI |

| ₹7,000+ existing EMI | Lower eligibility | Eligible loan may fall by ₹7–9 lakh or more |

| CIBIL score 750+ | Best terms | Lower rate, lower total cost, easier approval |

| CIBIL score below 700 | Reduced eligibility | Higher rate or partial sanction; improve score first |

| 20-year tenure | Moderate eligibility | Lower total interest; higher monthly EMI requirement |

| 30-year tenure | Higher eligible amount | More loan for same EMI but significantly more total interest |

| 20% down payment | Better LTV position | Smaller loan needed; less EMI pressure overall |

| Minimum down payment | Higher loan required | Confirm FOIR stays within lender’s acceptable limit |

How to Decide What’s Right for You

you have no existing EMIs, a CIBIL score above 750, and can manage a 20% down payment — THEN a home loan on ₹50,000 salary is workable if the property cost is proportionate to your ₹20–26 lakh eligibility range.

you carry existing personal loan or car loan EMIs — THEN consider clearing those with shorter remaining tenures before applying; the freed EMI capacity may raise your eligible home loan by ₹5–8 lakh.

you are considering a 30-year tenure to push up your eligible loan amount — THEN calculate total interest outgo at that tenure before deciding; the extra ₹10–20 lakh in interest may not be worth the additional ₹2–3 lakh in loan.

your monthly surplus after the proposed EMI will fall below ₹15,000 — THEN review whether household expenses, insurance premiums, and emergencies can genuinely be managed on what remains.

your employment is contractual, commission-dependent, or you recently changed jobs — THEN delay the application; lenders assess employment stability, and a recent switch can reduce approval chances or require a longer wait period.

your income is stable, you hold a clear emergency fund of at least three months’ expenses, and total EMI stays under 45% of net income — THEN stretching to the bank’s maximum approved amount without first mapping your full monthly outgo is not advisable. See our monthly salary budget guide to check whether a home loan EMI fits your actual ₹50,000 monthly allocation.

Common Mistakes to Avoid

Chasing the Maximum Loan Amount

The bank’s ceiling is not your target. Borrowing at the maximum FOIR limits your monthly buffer to almost nothing — any job change, medical expense, or home repair becomes a crisis.

Borrow what your budget can absorb over 20 years, not the highest number the lender will sanction on paper.

Forgetting Existing Credit Card or Loan EMIs

Even a ₹3,000 minimum payment on a credit card is counted toward your FOIR. Two open EMIs totalling ₹10,000 per month can reduce your eligible home loan by ₹10–12 lakh. Many borrowers only discover this after receiving a lower-than-expected sanction letter.

List every current EMI obligation before approaching a lender — including minimum credit card dues.

Applying With a Weak CIBIL Score

A rejected application is recorded on your credit report and can make the next application harder. If your score is below 700, a rejection or significantly higher rate is likely. Spend six to twelve months improving your credit — clear dues, reduce credit card utilisation below 30%, and correct errors in your report — before you apply. Understand exactly what moves the needle with our CIBIL score basics guide.

Ignoring Processing Fees and Upfront Charges

Processing fees, legal valuation charges, technical inspection fees, and mortgage stamp duty can add ₹20,000–₹50,000 or more to your upfront outgo depending on the lender and loan amount. These are separate from the loan and must come from your own funds at disbursement. Get a full fee schedule in writing before signing any form. Read our guide on loan processing fees to know exactly what to watch for.

Looking Only at Monthly EMI, Not Total Repayment Cost

A ₹25 lakh loan at 8.75% for 30 years involves repaying approximately ₹71 lakh in total — ₹25 lakh principal and about ₹46 lakh in interest. Evaluating only the ₹19,700 monthly EMI without seeing the full ₹71 lakh is the single biggest blind spot in home loan decisions.

Always ask the lender for the total amount payable over the full tenure — and compare this figure, not just the EMI, across lenders and tenures.

Planning Eligibility on Gross Salary Rather Than Net Take-Home

Calculating your ₹22,500 FOIR limit against a ₹65,000 gross salary when your actual bank credit is ₹50,000 leads to a significant overestimate. Use your salary account statement credit, not your offer letter or CTC, as the income base for all eligibility calculations.

When This May Not Be the Right Choice

A home loan on ₹50,000 salary may not make practical sense right now if:

- Your existing EMIs already consume 30% or more of your income, leaving insufficient FOIR headroom for a home loan EMI that falls within lender-acceptable limits.

- You do not have an emergency fund covering at least three to six months of total expenses — taking on a 20-year commitment without a buffer makes any income disruption immediately dangerous.

- Your employment is contractual, seasonal, or you have been in your current role for less than one year; most lenders require 2–3 years of continuous employment or business stability.

- The property you are targeting costs significantly more than ₹30–35 lakh, making the gap between your loan eligibility and actual purchase price too large to bridge from current savings even before accounting for stamp duty and registration charges.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Home loan eligibility norms, interest rates, FOIR limits, LTV ratios, and processing charges are set by individual lenders and regulated by the Reserve Bank of India. Confirm the following directly before making any decision:

- Reserve Bank of India — rbi.org.in — for LTV norms, fair lending practices, and borrower rights under RBI guidelines

- Your lender’s official website — for current interest rates, FOIR criteria, tenure limits, documentation requirements, and fee schedules

- CIBIL / Equifax / Experian / CRIF High Mark — for your current credit score and full credit report before applying

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision. For the full process from eligibility check to key handover, see our step-by-step guide on the home loan process in India.

Expert Tips

- Pull your CIBIL report at least six months before applying. Even a small outstanding balance on a forgotten credit card can suppress your score and cost you a higher rate — or rejection. Fixing errors in a credit report typically takes 30–45 days per dispute cycle.

- If you hold a short-duration personal loan or car loan with 12–18 months remaining, consider foreclosing it before submitting your home loan application. The EMI that frees up could raise your eligible home loan by ₹5–8 lakh depending on the rate and tenure.

- Increase your down payment by ₹2–3 lakh if your savings allow — a smaller loan means lower total interest and a more manageable monthly budget over two decades.

- Compare lenders on total cost of loan — principal plus total interest plus all fees — not just the monthly EMI figure or the advertised rate. A 0.25% rate difference on ₹25 lakh over 20 years amounts to roughly ₹80,000–₹1 lakh in total savings.

- Keep six months of salary slips, the latest Form 16, three months of bank statements, and your PAN and Aadhaar ready before approaching any lender. Incomplete documentation is one of the most common reasons for processing delays.

- Ask the lender for a full amortisation schedule before signing — this shows you exactly how much of each EMI goes toward principal versus interest in every year of the loan, and lets you plan partial prepayments strategically to reduce total interest cost.

Frequently Asked Questions

How much home loan can I get on ₹50,000 salary?

As a rough planning estimate, a ₹50,000 net monthly salary can support a home loan of approximately ₹20–26 lakh, depending on existing EMIs, the interest rate, tenure, and lender policy. This is an illustrative range, not a guaranteed figure. Final sanction also depends on your CIBIL score, employment history, property valuation, and the lender’s specific underwriting criteria. Always calculate total repayment cost — not just the loan amount — before committing.

Is ₹50,000 salary enough to get a home loan in India?

It depends heavily on the property cost and your city. In Tier 2 or Tier 3 cities where property values are in the ₹20–35 lakh range, ₹50,000 salary can be sufficient for a manageable home loan. In metros like Mumbai, Bengaluru, or Delhi, property costs often far exceed what this salary can support — meaning either a substantial co-applicant income or a larger down payment is needed to make the numbers work.

What EMI is safe on ₹50,000 salary?

A commonly used guideline is to keep total EMIs — including the home loan — at or below 40%–45% of net income. On ₹50,000, that ceiling is ₹20,000–₹22,500 in combined EMIs. For just the home loan, staying at or below 35% of net income — around ₹17,500 — leaves meaningful room for savings, emergencies, insurance, and daily expenses. Exceeding 45% total FOIR is possible but creates a tight budget with no buffer.

Does my CIBIL score affect home loan eligibility on ₹50,000 salary?

Yes, significantly. A score of 750 and above generally qualifies you for the best rates and makes approval smoother. A score between 650 and 750 may still result in approval but typically at a higher interest rate, which raises your EMI and reduces the loan amount your EMI capacity can support. Scores below 650 frequently lead to rejection or heavily restricted sanction amounts. Your score also affects whether lenders will stretch their FOIR limits in your favour.

Can an existing personal loan reduce my home loan eligibility?

Yes, directly. Every ₹5,000 in existing monthly EMI reduces your FOIR headroom by the same amount. If you are paying ₹8,000 per month on a personal loan, your available home loan EMI shrinks by ₹8,000. Depending on rate and tenure, this can reduce eligible home loan by ₹9–11 lakh or more. Clearing short-term debt before applying is often one of the most effective ways to raise home loan eligibility.

Should I choose a 30-year tenure to get a higher home loan amount?

A 30-year tenure does increase your eligible loan amount — the same EMI supports a larger principal over more years. But the total interest cost rises sharply. A ₹25 lakh loan at 8.75% for 20 years costs roughly ₹25.5 lakh in interest; stretched to 30 years, total interest can approach ₹45–46 lakh on the same principal. Choose the shortest tenure your monthly cash flow can genuinely support, not the longest the bank permits.

What happens if I apply for a home loan with a low CIBIL score?

The lender may reject the application, approve a lower amount than you requested, or offer the loan at a materially higher interest rate. A rejection is also recorded in your credit report and can make subsequent applications harder. It is almost always better to spend six to twelve months improving your score — paying dues on time, reducing credit card utilisation, and disputing any errors — before submitting a home loan application.

Can I improve my home loan eligibility on ₹50,000 salary by adding a co-applicant?

Yes. A co-applicant with additional income raises the combined income base and FOIR ceiling. If a co-applicant earns ₹30,000 per month with a clean credit profile, combined eligibility could rise from ₹20–26 lakh to ₹35–45 lakh, depending on the lender’s policy on combined income assessment. The co-applicant’s CIBIL score also factors into the rate offered, so both profiles should be strong before applying jointly.

Are home loan interest rates the same across all banks for ₹50,000 salary borrowers?

No. Rates vary by lender, loan amount, credit score, employment type, and whether the product is fixed or floating. Floating rates — more common in India — move with the RBI’s repo rate. It is worth getting formal rate quotes from at least three lenders before finalising. Even a 0.25% difference on ₹25 lakh over 20 years can mean ₹80,000–₹1 lakh difference in total repayment.

Final Verdict

A home loan on 50000 salary is achievable — but the number that matters is not the bank’s maximum approval; it is the EMI you can carry comfortably for the next 20 years without hollowing out your finances. Work from your net income, deduct all existing EMIs, apply a realistic FOIR, and always evaluate total repayment cost alongside the loan amount. A ₹22.6 lakh loan at 8.75% for 20 years means repaying approximately ₹48 lakh in all — that is the number to plan around, not the ₹20,000 monthly EMI alone.

Borrow for affordability, not for maximum eligibility. Keep your tenure as short as your monthly cash flow genuinely allows. And if your CIBIL score or existing debts are limiting your options today, addressing those first will save you considerably more than any rate negotiation later. Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Vikram Sethi writes about loans, EMI planning, credit score impact, borrowing costs, and repayment decisions for Indian borrowers. His content helps readers look beyond the monthly EMI and understand the full cost of borrowing, including principal, interest, processing fees, GST, insurance, prepayment charges, foreclosure fees, late payment penalties, and credit score impact.

He covers topics such as EMI calculators, home loan eligibility, personal loan eligibility, debt-to-income ratio, flat interest rate vs reducing balance, missed EMI consequences, loan prepayment vs part payment, home loan balance transfer, processing fees, gold loan vs personal loan, car loan vs cash purchase, top-up home loans, loan against PPF, and credit score basics.

Vikram’s writing style is practical, cautionary, and calculation-driven. He uses Indian examples, ₹ amounts, comparison tables, and decision frameworks to help borrowers compare options more carefully. His articles are educational and do not guarantee loan approval, interest rates, or savings. Readers should verify current rates, charges, eligibility, and terms directly with lenders before applying or refinancing.