Most first-time car buyers in India hear one number from the dealership — the EMI — and decide the purchase is affordable. It rarely is. The real first car cost in India includes road tax, registration, comprehensive insurance, loan interest, fuel, servicing and parking: costs that together can push your monthly outflow to nearly ₹24,000–₹26,000 on a ₹10 lakh car, even if the EMI alone looks like ₹16,600.

The difference between showroom price and on-road price alone can be ₹1 lakh or more, depending on your state. Add a five-year loan and the true cost of that car crosses ₹18 lakh before you factor in a single litre of petrol.

This guide walks through every cost layer, runs a complete first-year and five-year calculation, and gives you a clear monthly budget framework so there are no surprises after the booking slip is signed.

Quick Answer: First Car Cost in India

First car cost in India means the full 5-year ownership cost, not only the showroom price. It includes down payment, loan EMI and interest, insurance, road tax, registration, fuel, parking, maintenance and resale impact, so first-time buyers should check total monthly outflow before booking.

How to Calculate the True Cost of Your First Car

The calculation splits into two parts: one-time costs at purchase, and recurring costs over the ownership period. Use the car loan EMI guide to work out your monthly repayment before layering in the other expenses below.

Formula 1: Total First-Year Cost

Total First-Year Cost = Down Payment + (Monthly EMI × 12) + Year-1 Insurance + Road Tax + Registration + Processing Fee + (Monthly Fuel × 12) + Annual Maintenance + (Parking/Tolls × 12)

Formula 2: Total Loan Cost

Total Loan Cost = Loan Principal + Total Interest Paid + Processing Fee + Other Lender Charges

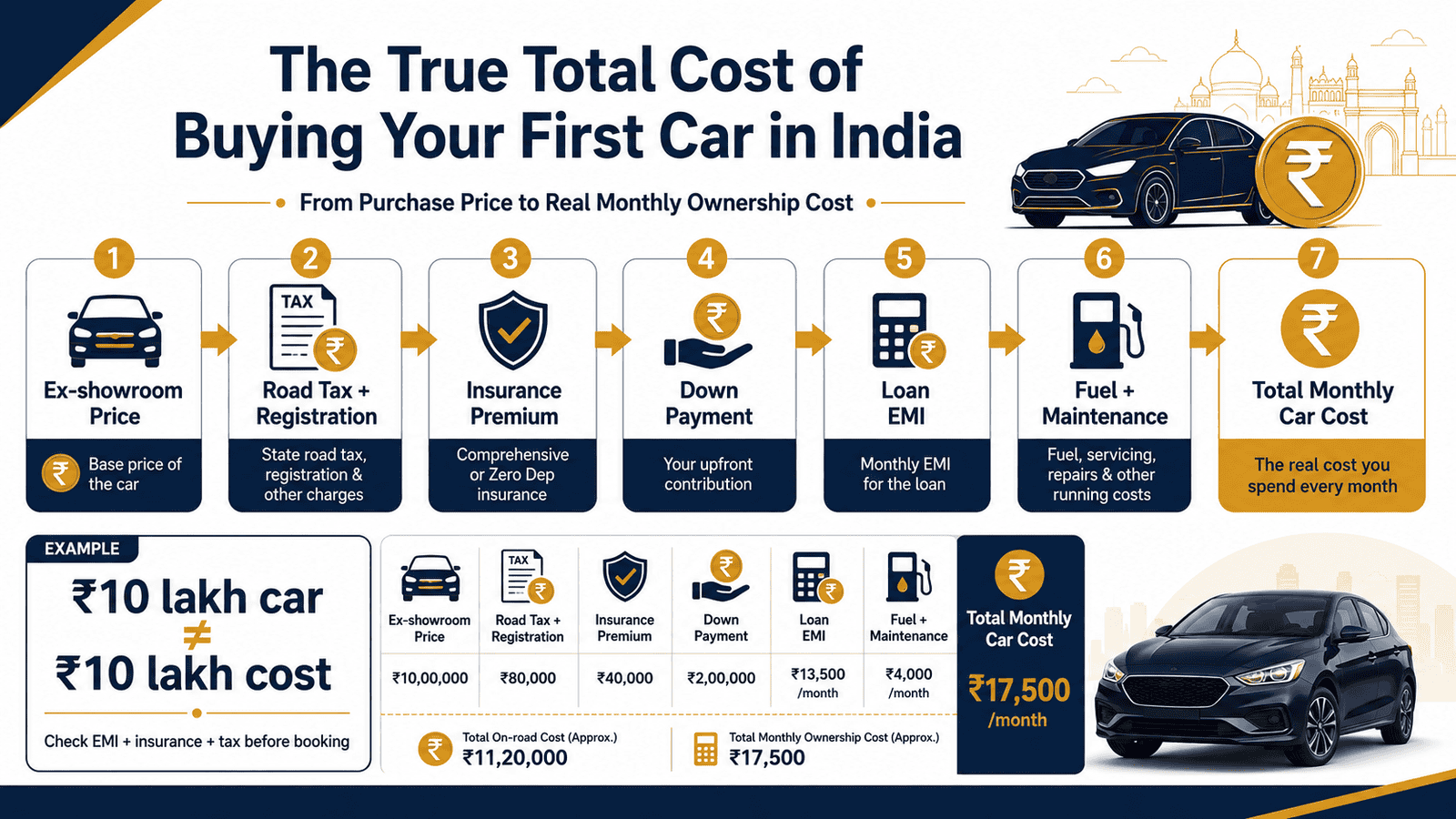

Sample Calculation: ₹10 Lakh Ex-Showroom Car

The table below uses illustrative figures only. Actual loan rates, road tax, insurance premiums and registration charges vary by state, lender and insurer — verify all before booking.

| Cost Item | Illustrative Figure | Notes |

|---|---|---|

| Ex-showroom price | ₹10,00,000 | Base price, example only |

| Road tax (state-specific) | ₹1,10,000 | Varies widely by state |

| Registration charges | ₹8,000 | Varies by RTO |

| Year-1 comprehensive insurance | ₹25,000 | Varies by insurer and IDV |

| Approx. on-road price | ₹11,43,000 | Excludes dealer accessories |

| Down payment (20%) | ₹2,00,000 | Of ex-showroom price |

| Loan amount | ₹8,00,000 | At 9% p.a., 60 months |

| Monthly EMI | ₹16,607 | Illustrative rate only |

| Total interest (5 years) | ₹1,96,420 | At illustrative 9% rate |

| Processing fee (approx. 1%) | ₹8,000 | Varies by lender |

| Monthly fuel | ₹4,500 | Approx. 1,200 km/month |

| Monthly maintenance (avg.) | ₹1,000 | ₹12,000/year amortised |

| Monthly parking/tolls | ₹1,200 | City-dependent |

Recurring monthly outflow after purchase: EMI ₹16,607 + Fuel ₹4,500 + Maintenance ₹1,000 + Insurance amortised ₹1,200 + Parking ₹1,200 = ₹24,507 per month. That is 2.5 times the headline EMI — and the most common reason first-time buyers are financially stretched within three months of delivery.

Cost Scenarios by Car Segment

| Scenario | Key Inputs (Illustrative) | Estimated Monthly Car Budget |

|---|---|---|

| Entry hatchback | ₹6L ex-showroom, ₹1.2L down, 9%, 5 yr | ₹14,000–₹17,000 |

| Mid hatchback | ₹10L ex-showroom, ₹2L down, 9%, 5 yr | ₹22,000–₹26,000 |

| Compact SUV | ₹15L ex-showroom, ₹3L down, 9%, 5 yr | ₹33,000–₹40,000 |

Key Takeaways

- The on-road price of a ₹10 lakh car can exceed ₹11.4 lakh after road tax, registration and insurance — before you pay a single EMI.

- Total loan interest on ₹8 lakh at 9% over 5 years adds approximately ₹1,96,420 to your true purchase cost, making the loan’s real cost ₹9,96,420, not ₹8 lakh.

- Monthly fuel, maintenance and parking typically add ₹6,500–₹8,000 on top of EMI — budget for the full outflow, not just the repayment.

- Road tax rates differ significantly across states and can add 8–15%+ to the ex-showroom price; always get a state-specific on-road quote from the dealer before comparing cars.

- A 5-year comprehensive insurance and running cost total for a ₹10 lakh car routinely crosses ₹3–4 lakh even without major repairs.

- Using emergency savings as a down payment leaves you financially exposed; set aside the down payment separately over 6–12 months before booking.

Key Facts at a Glance

| Cost Component | What It Covers | Typical Range (Illustrative) |

|---|---|---|

| Ex-showroom price | Manufacturer’s base price including GST | ₹6L–₹20L+ (hatchbacks/compact SUVs) |

| On-road price | Ex-showroom + road tax + registration + insurance | 15–25%+ above ex-showroom |

| Down payment | Upfront payment by buyer | 10–20% of ex-showroom (lender-specific) |

| Car loan interest rate | Annual rate on financed amount | 8.5–12% p.a. (varies by lender/profile) |

| Processing fee | One-time lender charge on disbursement | 0.5–1% of loan amount |

| Comprehensive insurance (Yr 1) | Own damage + third-party cover | ₹18,000–₹30,000+ |

| Road tax | One-time state levy on vehicle registration | 8–15%+ of ex-showroom (state-specific) |

| Annual maintenance | Service, tyres, consumables | ₹10,000–₹20,000/year |

| Monthly fuel | Petrol/diesel based on km driven | ₹3,500–₹6,500+ |

For a detailed explanation of why loan processing charges increase your actual borrowing cost beyond the interest rate, see our dedicated guide.

Understanding Every Cost Component of Your First Car in India

Ex-Showroom Price vs On-Road Price

The ex-showroom price is the manufacturer’s price including GST and applicable cess. It is the number advertised in brochures and on most comparison websites. It is not what you actually pay at delivery.

The on-road price adds road tax, registration charges, first-year comprehensive insurance and dealer handling charges on top of the ex-showroom price. In Maharashtra, road tax on a petrol car can be around 11% of ex-showroom cost. In Karnataka or Tamil Nadu, it can differ significantly. Always ask the dealer for a written on-road price breakup before comparing models — a ₹50,000 difference in ex-showroom can sometimes become smaller or larger on-road depending on which city you register in.

Down Payment and Loan Amount

Most lenders in India finance 80–90% of the ex-showroom price, or sometimes the on-road price, depending on the lender’s policy. The remaining 10–20% is your down payment. A higher down payment lowers your loan principal, which directly reduces total interest paid and monthly EMI.

Putting down 20% on a ₹10 lakh car means financing ₹8 lakh instead of ₹9 lakh — a difference of roughly ₹2,000 in monthly EMI and approximately ₹25,000 in total interest over 5 years at similar rates.

Car Loan EMI, Interest and Processing Fee

Car loan interest rates in India typically range between 8.5% and 12% per annum depending on the lender, your credit profile and the tenure chosen. The processing fee — usually 0.5% to 1% of the loan amount — is charged upfront and increases your real cost of borrowing.

Choosing a 7-year tenure to reduce EMI is tempting, but total interest paid grows significantly compared to a 5-year tenure. On ₹8 lakh at 9%, extending from 5 to 7 years reduces EMI by roughly ₹2,800 but increases total interest by over ₹55,000. The lower EMI costs you more overall.

Insurance: Third-Party, Own Damage and Comprehensive

Third-party motor insurance is legally mandatory under Indian law for every registered vehicle. It covers injury or damage to a third party but offers no protection for your own car. According to IRDAI guidelines, third-party premium rates are set by the regulator and vary by engine capacity.

Comprehensive insurance adds own-damage (OD) cover and is strongly recommended for a new car, especially if it is financed. The Insured Declared Value (IDV) — the market value your insurer uses to calculate the OD premium and settle total-loss claims — depreciates each year. A lower IDV at renewal reduces your premium but also reduces your claim payout if the car is stolen or totalled.

Add-ons such as zero-depreciation cover, roadside assistance and engine protection increase the premium but can significantly reduce out-of-pocket costs at the time of a claim. For a financed new car, zero-depreciation is worth considering in at least the first two years.

Road Tax and Registration

Road tax is a one-time levy collected by the state government at the time of registration. Rates are not uniform across India and are typically a percentage of the ex-showroom price, with some states also considering the vehicle’s age, fuel type and engine capacity. Registration charges at the RTO are separate and generally lower.

Fuel, Maintenance, Parking and Resale

Fuel is your largest recurring variable expense. A petrol hatchback averaging 15–18 km/litre driven 1,200 km per month will consume roughly 70–80 litres, translating to approximately ₹4,000–₹5,500 per month depending on current petrol prices in your city.

Annual servicing, tyre wear, consumables and minor repairs typically cost ₹10,000–₹20,000 per year for a standard hatchback within warranty. Expect this to rise after year four as the warranty period ends.

Resale value matters for total cost calculations. Cars depreciate fastest in years one and two. A ₹10 lakh car may be worth ₹6–7 lakh after five years — which reduces your net ownership cost but only if you actually sell it at that point.

Real Example: Aarav Buys His First Hatchback in Pune

Aarav is 29, a software engineer in Pune earning ₹95,000 per month. His take-home after TDS and EPF deductions is approximately ₹75,000. He is looking at a hatchback priced at ₹10 lakh ex-showroom.

He arranges a ₹2 lakh down payment saved separately over eight months. The loan of ₹8 lakh at an illustrative 9% per annum over 60 months gives him an EMI of approximately ₹16,607. Road tax, registration and Year-1 insurance add roughly ₹1,43,000 to the upfront cost at delivery.

His monthly budget breakdown: Rent ₹20,000 + Household expenses ₹15,000 + SIP/savings ₹12,000 + Car EMI ₹16,607 + Car running costs ₹6,700 + Insurance amortised ₹1,200 = ₹71,507. That leaves roughly ₹3,500 as buffer — very thin. Aarav decides to consider a ₹7 lakh car instead, which brings his total monthly car budget to approximately ₹18,000 and restores a healthier monthly surplus.

Use the total EMI calculator to run different loan amounts, rates and tenures side by side before you approach a lender or dealer. All rates and charges used here are illustrative — verify current figures from your lender and insurer before booking.

Comparison: New Car vs Used Car

| Parameter | New Car | Used Car (3–5 years old) |

|---|---|---|

| Purchase price | Higher (full ex-showroom) | Lower (30–50% of new price typically) |

| Loan availability | Easier — most banks finance new cars readily | Variable — rates and LTV differ by car age and lender |

| Warranty coverage | Yes — manufacturer warranty, typically 2–3 years | Usually no — unless certified pre-owned with dealer warranty |

| Insurance premium | Higher IDV, higher own-damage premium in Year 1 | Lower IDV, lower premium — but older cars carry higher risk |

| Maintenance cost | Lower risk in early years; authorised service available | Higher repair risk; may need pre-purchase inspection cost |

| Regulatory compliance | Current — latest emission norms (BS6) | Check — older cars may not comply; verify before buying |

| Resale predictability | More predictable depreciation curve | Harder to estimate; depends heavily on car condition |

For a detailed breakdown of the insurance implications of each choice, read the car insurance comparison guide before estimating your ownership cost.

How to Decide What’s Right for You

Your monthly surplus after rent, household expenses and savings is at least ₹25,000 — a ₹10 lakh hatchback is within reach if you have a separate down payment ready.

Your monthly surplus is ₹15,000–₹20,000 — look at cars in the ₹6–7 lakh range; a lower EMI preserves breathing room for fuel, insurance and an unexpected repair bill.

You have an existing personal loan or home loan EMI — add that to the car EMI and total running costs before deciding; your total fixed obligations should not exceed 40–45% of take-home pay.

You have not yet built an emergency fund of 3–6 months of expenses — delay the car purchase until the fund is in place; using it as a down payment leaves no cushion for a job disruption or medical bill.

You drive under 500 km per month — a used car or a lower-segment new car is more cost-efficient; the depreciation and insurance cost of a premium hatchback is hard to justify on low usage.

You cannot fund the down payment without touching emergency savings, or your total monthly obligations would exceed 50% of take-home — this is not the right time to buy; delay and save for 6–12 more months.

Use the monthly budget planner to map your full household cashflow before committing to a car purchase.

Common Mistakes to Avoid

Booking Based Only on EMI

The EMI covers only the loan repayment — nothing else.

A ₹10 lakh car with a ₹16,607 EMI also costs ₹4,500 in fuel, ₹1,000 in maintenance and ₹1,200 in insurance monthly. The real monthly cost is closer to ₹24,500 — a difference of nearly ₹8,000 that quietly drains savings.

Always calculate total monthly car budget, not just EMI, before booking.

Ignoring the On-Road Price

Comparing cars on ex-showroom price across cities is misleading.

Road tax varies significantly by state. A ₹10 lakh car can cost ₹11.1 lakh on-road in one state and ₹11.7 lakh in another. If you are buying near a state border, the difference can be worth comparing.

Ask every dealer for a written on-road breakup before deciding.

Choosing Maximum Tenure to Minimise EMI

Stretching a 5-year loan to 7 years to lower the EMI by ₹2,800 costs you an additional ₹55,000+ in total interest at a 9% illustrative rate.

Choose the shortest tenure your monthly budget can support comfortably, not the one that makes the EMI look smallest.

Using the Emergency Fund as Down Payment

Depleting your emergency fund to fund a down payment leaves you financially exposed from day one of ownership.

If your car is damaged, if you face a medical expense, or if your income is disrupted, you have no buffer. Save the down payment separately over 6–12 months before booking.

Not Comparing Insurance Outside the Dealership

Dealer-arranged insurance is convenient but not always the best-priced option. The IDV offered and add-on coverage can differ between policies.

Check insurer websites and aggregators before accepting the dealership quote, where your lender’s terms permit it.

Ignoring the Credit Score Before Applying

Your credit score affects the car loan rate your lender offers. A borrower with a score above 750 may get a noticeably better rate than one below 700, which can translate to thousands of rupees in interest over five years.

Check your credit score at least 3 months before applying and resolve any errors or overdue payments first.

Skipping the Loan Agreement Before Signing

Processing fees, prepayment penalties and foreclosure charges are in the loan agreement — not in the brochure.

Read the key terms before signing, especially if you plan to prepay the loan early.

When This May Not Be the Right Choice

Buying a car now may not be the right financial move if your monthly surplus after all fixed expenses and savings contributions is below ₹20,000 — the full car budget (EMI plus running costs) will leave almost nothing for unexpected expenses.

If you already carry a personal loan or significant credit card debt, adding a car EMI raises your total debt obligation and increases financial stress during any income disruption.

If your commute is fully covered by company transport, metro or a short walk, and you would use the car mainly on weekends, the annual ownership cost — insurance, maintenance, depreciation — may not be justified by the actual usage.

If you are planning a major expense within 18 months — a home, a wedding, or further education — a car purchase may delay those goals significantly. Cab services and short-term car rentals can be more cost-efficient for occasional use.

If any of these apply to your situation, it may be worth exploring alternatives before committing.

Official Rules and Where to Verify

Rules, limits, and rates on this topic can change with each Budget or regulatory update. Always verify current figures directly from the official source before making any financial decision.

- RBI — rbi.org.in: For reference on lending norms, fair practices code and borrower rights for car loans.

- IRDAI — irdai.gov.in: For third-party insurance premium rates, policyholder guidelines and insurer-specific queries.

- Your state transport department / RTO: For current road tax rates and registration charges applicable in your city — these are state-specific and subject to revision.

- Your lender’s official website: For current car loan interest rates, processing fees, prepayment terms and foreclosure charges before applying.

- Your insurer’s official website or policy document: For current IDV, premium breakup and coverage terms before renewing or buying comprehensive insurance.

Expert Tips

- Before visiting a showroom, decide your maximum on-road budget — not ex-showroom — and tell the salesperson that number. This prevents the conversation from anchoring on a price that balloons by ₹1–1.5 lakh before delivery.

- Ask the dealer for a full on-road price breakup in writing: ex-showroom, GST, road tax, registration, insurance, dealer charges, and any mandatory accessories. Compare this document, not verbal quotes.

- Run your EMI calculation at an interest rate 0.5–1% higher than the advertised rate — lenders sometimes quote best-case rates that apply only to top-tier credit profiles. Budget conservatively.

- Consider setting up a car sinking fund: ₹1,000–₹1,500 per month into a separate savings account from the first month of ownership. This covers annual insurance renewal, the next service, and tyre replacement without hitting your main budget.

- Check whether your lender imposes a prepayment penalty before choosing tenure. If you can prepay in years 3–4, a shorter tenure saves less interest than a prepayment on a longer tenure — run the numbers both ways.

- If you are considering a used car, budget ₹3,000–₹5,000 for an independent inspection by a certified mechanic before purchase; it can prevent a much larger repair bill within the first six months.

Frequently Asked Questions

How much down payment is needed to buy a first car in India?

Most lenders in India require a minimum down payment of 10–20% of the ex-showroom price, though policies vary. A larger down payment reduces the loan amount, total interest paid and monthly EMI. Verify the minimum requirement directly with your lender before planning your savings target.

Is the car EMI the same as the total monthly car cost?

No. The EMI covers only the loan repayment. Your actual monthly car cost also includes fuel, insurance amortised monthly, maintenance, parking and tolls. For a ₹10 lakh car financed at an illustrative 9% over 5 years, the EMI is approximately ₹16,607 but the total monthly outflow can reach ₹24,000–₹26,000 once running costs are included.

What is included in the on-road price of a car?

The on-road price includes the ex-showroom price (which already includes GST and applicable cess), road tax, registration charges at the RTO, first-year insurance premium and any dealer handling fees. It is the actual amount you pay to take possession of the car. Always ask for a written on-road quote before comparing models or dealers.

Is comprehensive car insurance mandatory for a new car loan?

Third-party motor insurance is legally mandatory for all registered vehicles in India. Comprehensive insurance — which adds own-damage cover — is not legally mandated but is typically required by the lender as a condition of the car loan. Even without a loan, comprehensive cover is strongly advisable for a new car given the replacement cost at stake.

Should a first-time buyer choose a new car or a used car?

This depends on budget, intended usage and risk tolerance. A new car offers warranty, current emission norms and predictable maintenance in the first three years. A used car can reduce upfront cost significantly but carries higher uncertainty around condition, repair history and financing terms. If you have a limited budget and cannot afford both the down payment and a reasonable monthly buffer, a lower-priced new car or a well-inspected certified used car may be safer than stretching for a new premium model.

How does my credit score affect the car loan interest rate?

Lenders assess your credit score — maintained by credit bureaus regulated under RBI guidelines — when setting the interest rate for your car loan. A higher score generally signals lower credit risk and can result in a better rate offer. A lower score may lead to a higher rate or stricter loan terms. Check your score before applying and resolve any discrepancies with the bureau to improve your negotiating position.

Can I prepay a car loan early to save on interest?

Yes, prepaying a car loan reduces outstanding principal and total interest payable. However, some lenders charge a prepayment penalty, especially on fixed-rate loans during the initial years of the tenure. Review the loan agreement for prepayment terms before deciding on tenure or planning early repayment.

What happens if I miss a car loan EMI?

A missed EMI typically incurs a late payment charge and is reported to credit bureaus, which can lower your credit score. Persistent defaults can lead to the lender recovering the vehicle under the loan agreement. If you anticipate difficulty, contact your lender proactively — some offer restructuring options depending on your repayment history and profile.

Is it better to take a shorter or longer car loan tenure?

A shorter tenure means a higher EMI but significantly less total interest paid and faster debt clearance. A longer tenure reduces EMI but increases your total borrowing cost substantially. The right tenure is one where the EMI fits your monthly budget without eliminating your savings or emergency fund contributions — not the longest tenure that makes the EMI look lowest.

Final Verdict

The first car cost in India is not a single number. It is a stack of one-time charges at delivery, loan interest spread over years, annual insurance renewals and monthly running costs that together shape what the car actually costs you. A ₹10 lakh ex-showroom car can have a true 5-year ownership cost of ₹17–18 lakh once interest, insurance, fuel and maintenance are counted — and that is before accounting for depreciation in resale value.

Buy only after running the full calculation: on-road price, total loan cost, insurance, and monthly running budget. Choose a car that protects your savings and emergency fund, not one that maximises the feature list at the edge of affordability. Use the car loan EMI guide to stress-test different scenarios before you pay the booking amount.

Always verify the latest rules from official sources or consult a qualified professional before making any financial decision.

This article is for educational purposes only and should not be treated as personalised financial, tax, investment, insurance, or legal advice. Tax rules, interest rates, regulatory limits, and product features can change with each Budget or policy update. Please verify current rules from official government sources or consult a qualified and registered professional before making any financial decision.

Sanya Malhotra writes about everyday personal finance for Indian individuals and families. Her content focuses on budgeting, saving, emergency funds, debt control, net worth tracking, family money decisions, and practical habits that help readers manage money with more confidence.

She covers topics such as monthly budgeting, expense planning, saving habits, emergency fund behaviour, debt repayment, household financial planning, family discussions about money, financial mistakes, net worth tracking, short-term vs long-term goals, and beginner personal finance concepts.

Sanya’s writing style is warm, simple, and realistic. She avoids making personal finance feel intimidating and instead explains money decisions through relatable Indian examples, ₹ budgets, checklists, and step-by-step frameworks. Her articles are useful for students, freshers, couples, parents, and families who want to improve daily money habits. Her content is educational and does not provide personalised financial advice. Readers should adapt examples to their own income, family responsibilities, city, debt level, risk comfort, and financial goals.